Evolution At Work

Evolution is often defined as “survival of the fittest”. Those who are better able to exploit opportunities offered by the circumstances in which the live, better at the process of adapting to changes and trends in their environments, even modifying their circumstances to improve fitness – they survive to enable their children and their children’s children to have their own better chances at survival. The same applies to countries. Changes happen and the United States of the past four years are no longer as they were up to the 1970s. Is this country evolution at work?

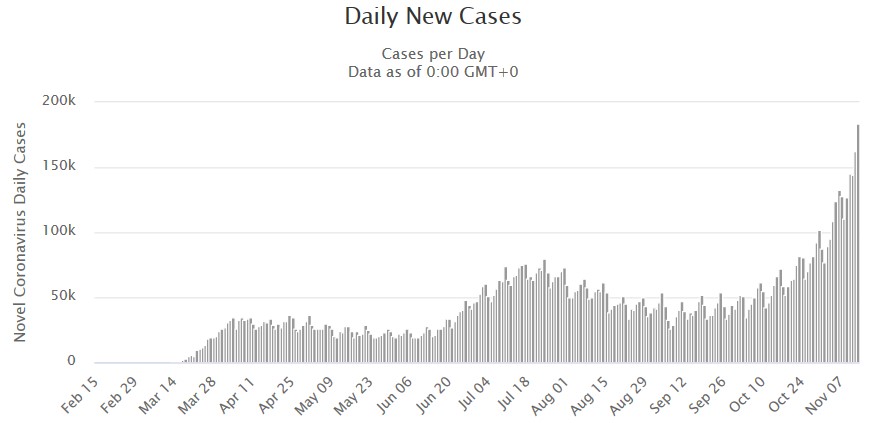

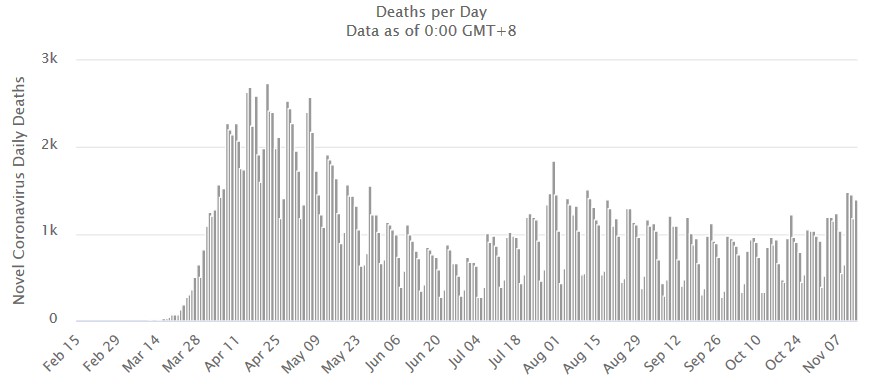

As usual, first a look at what COVID is doing. Last week, the COVID statistics for some states showed a wide range of states, all with more than 1000 deaths/million of inhabitants; both large and small and either urban or rural demographics,. With these differences, why do some states well, while others have high mortality?

Finding the answer to that question is now more important, when infections have skyrocketed. A week ago, the total number of US cases were 254 924 and it is now 276 366 – for an average of over 3000 new cases per day. The graphs show the upturn in the number of deaths has lagged the upturn in the number of cases by almost a month. This means the deaths from the new spike in the number of cases will not be counted until in December. Despite this, we see Wall Street close to new all-time highs! Can the stock market withstand it should it be decided during the next few weeks that lock-down is to be reinstated?

The US is not an exception; globally, the new infection rate has been spiking higher since early in October.

The US became the leading superpower of the 1900s as it employed a combination of hard working people and innovative technology to open up the natural resources and the space of the continent and build a wealthy civilisation. Aided by the stream of immigrants who pursued a dream of freedom from official and social constraints as these existed in their home countries; people who were willing to work hard to seek their dream it in a new country and contributed to its growth.

Over a century and a half their efforts enabled the US to twice become part of a global effort to counter major threats to the world order. This meant that by the end of WWII the US was the major global power, later to be challenged by the USSR. American workers – not primarily clerks and paper pushers – enjoyed their best years during the late 1960s into the 1970s. American factories were humming and ‘Made in the USA’ was a label much sought after elsewhere in the world.

The best measure of the state of household finances during the first half of the 20th century is that while the country flourished, only about 15% of married women was employed – one wage earner per family was sufficient to afford a good life for most households. By 1970, it had increases to 40% and then rose to the 80% by the mid-1990s after incomes began to lag economic growth. This trend is influenced by the change in culture; “Women’s Lib” has also contributed to this trend. The question to as is, “Can most households afford to live reasonably well on a single salary?”

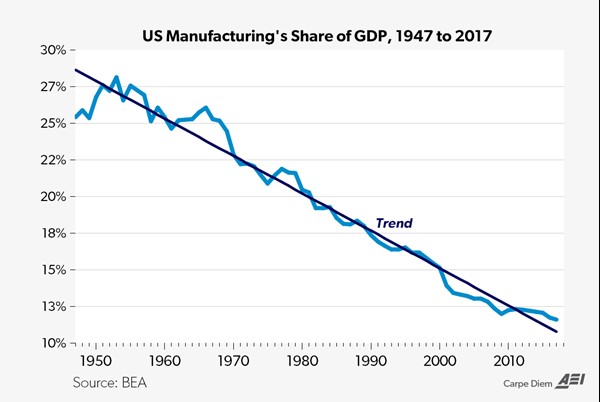

The trend in manufacturing’s share of the GDP has been in decline since 1950 and is now half of what it had been then. During all this time the variety and the prices of consumer goods that enable the good life have increased. Households wanted the luxuries of modern life and wanted to keep up to date with the latest technology had to offer. People had to take on debt to enjoy the many opportunities that have become available to enrich their life experience.

Despite the trend on the chart, this meant that much of what consumers bought had to be imported from elsewhere. America became beholden to other countries for the material wealth of its households. By about the change in centuries, the nature of work in the US has changed.

In 1976 86% of the S&P500 was from the industrial sector, with 6.1% financials. By 2001 industrials had fallen to 11% with financials and IT sharing 36%. By 2016 the industrial share was down to 9.7%, with financials and IT also lower at 34%. Over the past 50 years or so, the US has changed its activities from making things to the processing of documents and the maneuvering of money from one place to another, with many less well skilled people employed in the service sector at lower wages.

During this change a large fraction of its working age population has opted out of the active economy to survive on their access to government largesse and perhaps in the shadow economy. This change has also bred new generations fully aware of their entitlements and individual rights, but with no obligations in return. The idea that one has to actually work to earn (the right to) a living is no longer in vogue. In the 1800s, if one did not work, you starved – a way of life that lasted practically unchanged until well after WWI; for many Americans this is no longer acceptable.

That process and the trend of change over the past 50 years or so seem set to get a boost if Biden retains the presidency after the hooha of voter fraud has ended. It seems from the platform on which he and his VP stand that much of what Trump has tried to do to get America back onto the path that initially took it to greatness will be modified and much of it reversed by the new administration. The evolution of the US will be taken further down the path it has been on for the past decade or two – unless of course Trump is given another opportunity to force a right turn.

Evolution can take a breather whenever the environment becomes stable and no new threats or opportunities appear to require adaptation; thereby to be better at countering new threats or to exploit opportunities. It applies to humans as it does in the natural world. Technology can supply excellent examples. Some of us can remember the advances in home entertainment when the Betamax video machines offered quality home movies. Then VHS came along and Betamax was no more. We might all remember the first true cell-phones of which Nokia and Ericson dominated the market. Now it is Samsung and iPhone at the top, with Huawei and Xiaomi in the chase to the no 1 spot. The same happens with countries.

As Avis told the world for a long time, “As the no 2 we try harder”, or words to that effect. The implication follows that when one is number 1, it is necessary to work even harder to remain ahead. To remain in the top spot, the imperative is innovate and adapt – simply trying to do better what you have been doing for 5 years – or for a generation – is not going to be good enough. As it happens, the Avis slogan describes what China is accomplishing.

By the early 2000s China had started to exploit its human resource. At the time it was well known that China intended to bring 500 million people off the land into the cities, changing them from agricultural workers into a middle class. To do so, they first had to create infrastructure – roads, railways, electricity grid, power stations and cities to accommodate the migration from off the land to the city. In 2000 the Chinese middle class consisted of fewer than 40 million people. By 2018, more than 700 million Chinese enjoyed middle class life, with 30% of these with high incomes.

More recently they are reported to do the same with 300 million more agricultural and similar low level workers. The intention is to increase their own consumer base in order to expend their in-house consumer market. This will sustain their growth rate even should the US – and other countries – repatriate their manufacturing investments in China and thereby become less reliant on imports from China.

The race for the global number 1 spot has been on since Deng Xiaoping changed its national strategy to free the Chinese entrepreneurial spirit from the strait jacket in which Mao Zedong had trapped China. That change in effect made China no longer Communist or even Socialist. Not only do most Chinese have to work to live, just as in America in the 1800s, but they save up to 40% of their incomes to prepare for their old age when they no longer work. Their version of Social Security pay 1% of the indexed wage for each year of contributions, with a minimum of 15 years. That is not enough to live on and everyone has to make personal provision for old age.

As the election stands at the moment, Trump’s drive to see manufacturing return to the US as an evolutionary adjustment to changing global circumstances is likely be shifted to the back burner, if not dropped altogether. Given already high levels of debt and the need to increased debt to fund the repatriation effort, this would have been difficult to accomplish without increasing global tensions. At a guess, Biden will be less adversarial on the international stage and more focused on bringing about change within the US in line with the Democratic ideal, perhaps a culture as it is exemplified by California. If so, the recent trend in US evolution will continue.

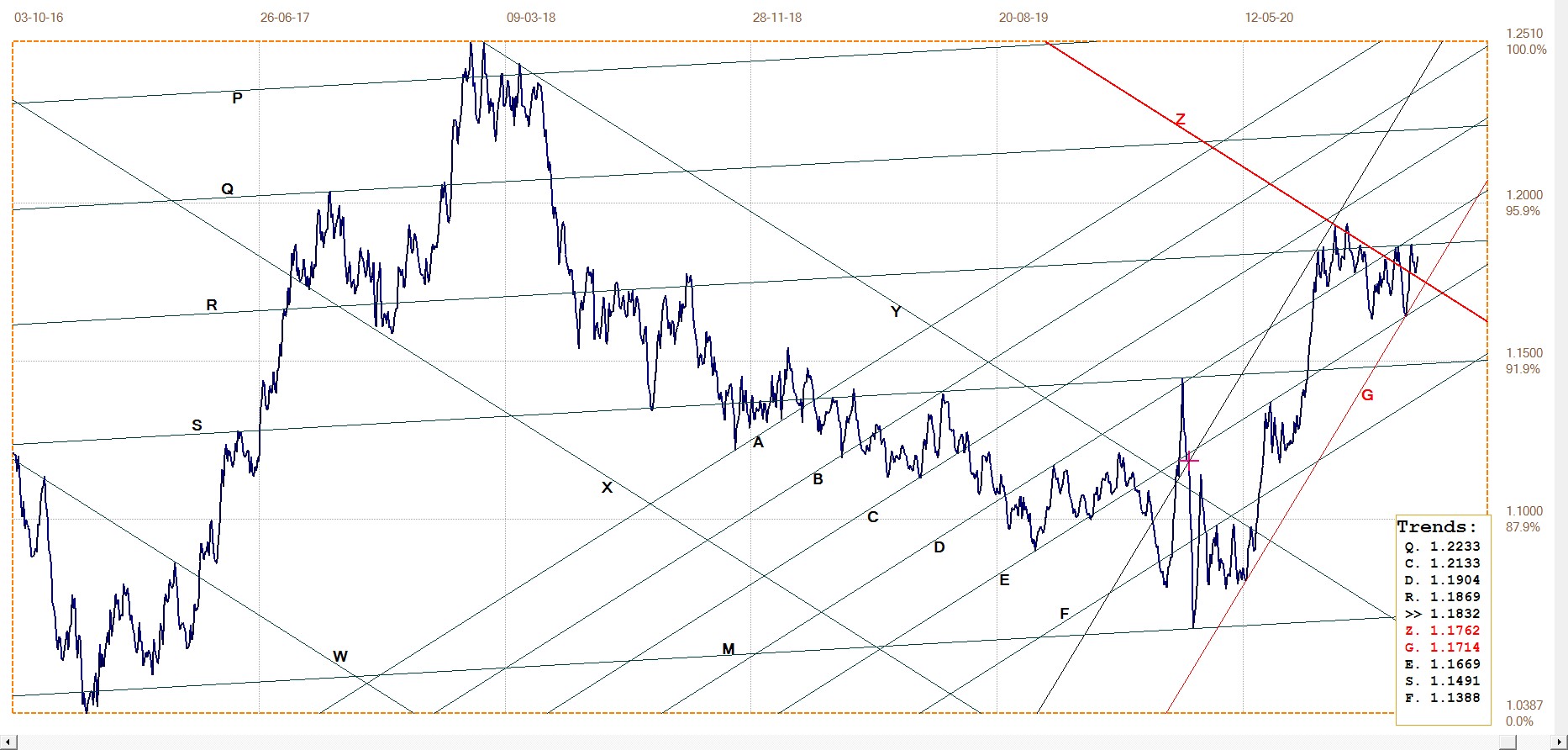

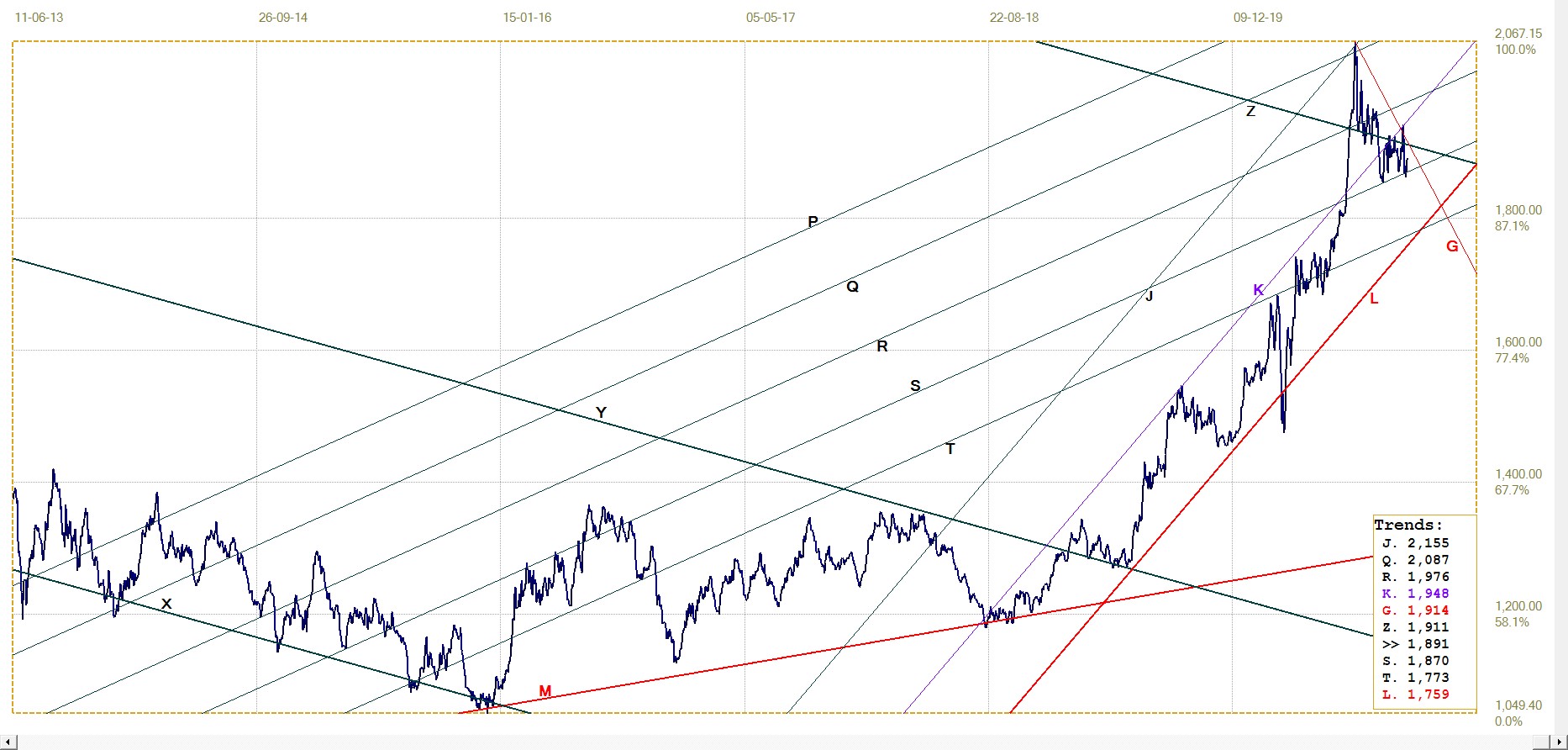

Euro–Dollar

Euro–dollar, last = $1.1832 (www.investing.com)

The euro rally following the recent bear spike down to line E ($1.1669) reached to line R ($1.1869) again and again failed to break higher. The reversal lower off line R found support at line Z ($1.1762), the top of broad bear channel WXYZ.

Having held the break above channel YZ is important and this could possibly be an example of a “goodbye kiss”; when the price breaks from a major chart formation only to return briefly to touch the formation before resuming the trend of the break. To confirm such a development, the euro has to break above line R and into channel DC.

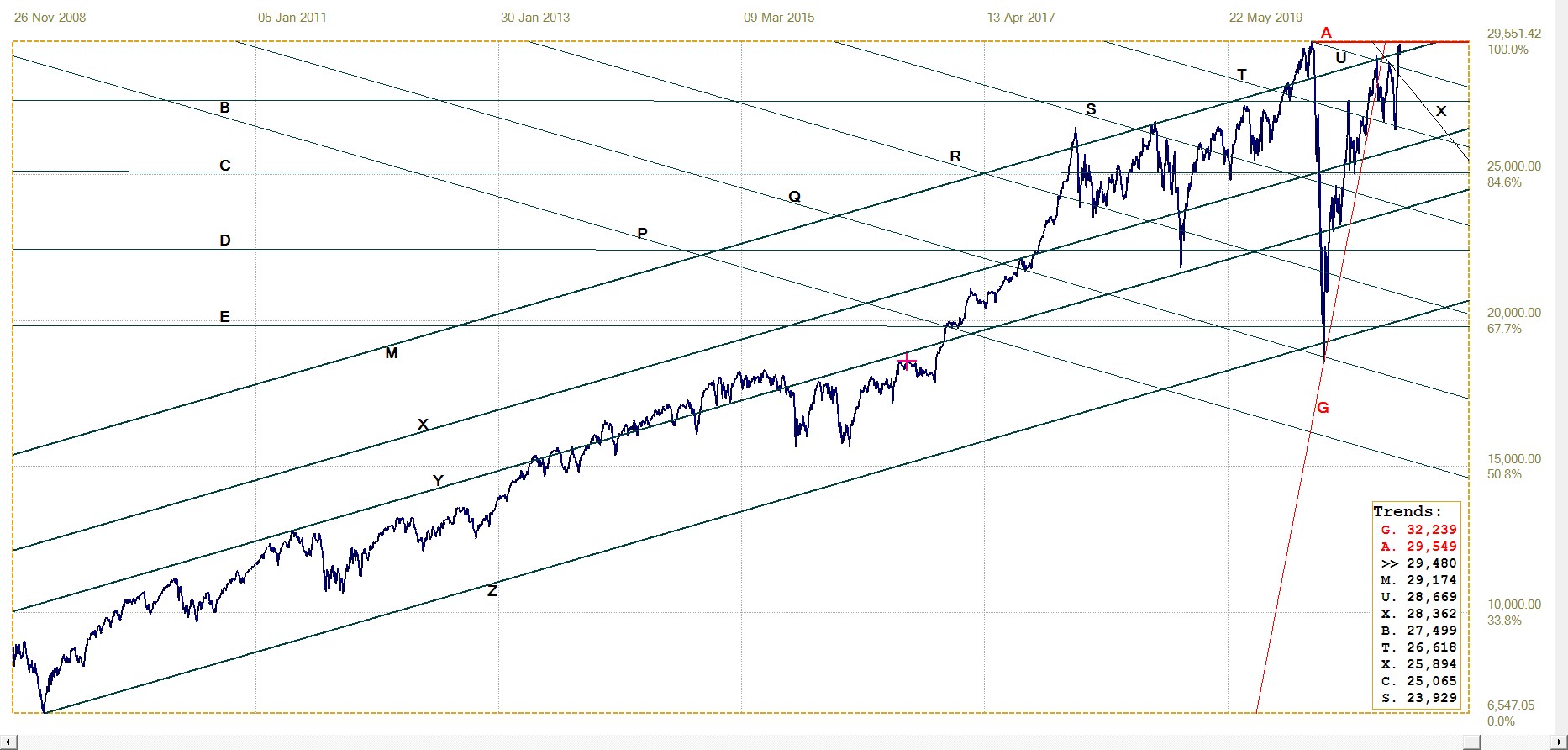

DJIA Daily close

DJIA, last = 29479.81 (money.cnn.com)

The spike lower to break marginally below line T (25 894) must have upset the equity bulls as Wall Street made its usual spike reversal higher to break above the main bull channel and reach almost to line A (29 549) and the all-time high at 29 551.42. The DJIA now has effectively formed a double top and tradition has such patterns offer strong resistance – a market has to have the bit set between the teeth to break higher.

COVID has been doing its best to infect more Americans and its success has formed a spike third wave. Will Wall Street have the momentum – and the funds support – to extend the rally to new all-time highs even while the threat of new measures to combat the pandemic is hanging over the economy? The normal course of events when fundamentals count, would see the market going into a retreat in the face of the unknown reaction by the government. But circumstances are not normal.

An interesting question is whether last week’s rally is in the hope that Trump will be able to overturn the result or general joy and happiness on Biden’s win?

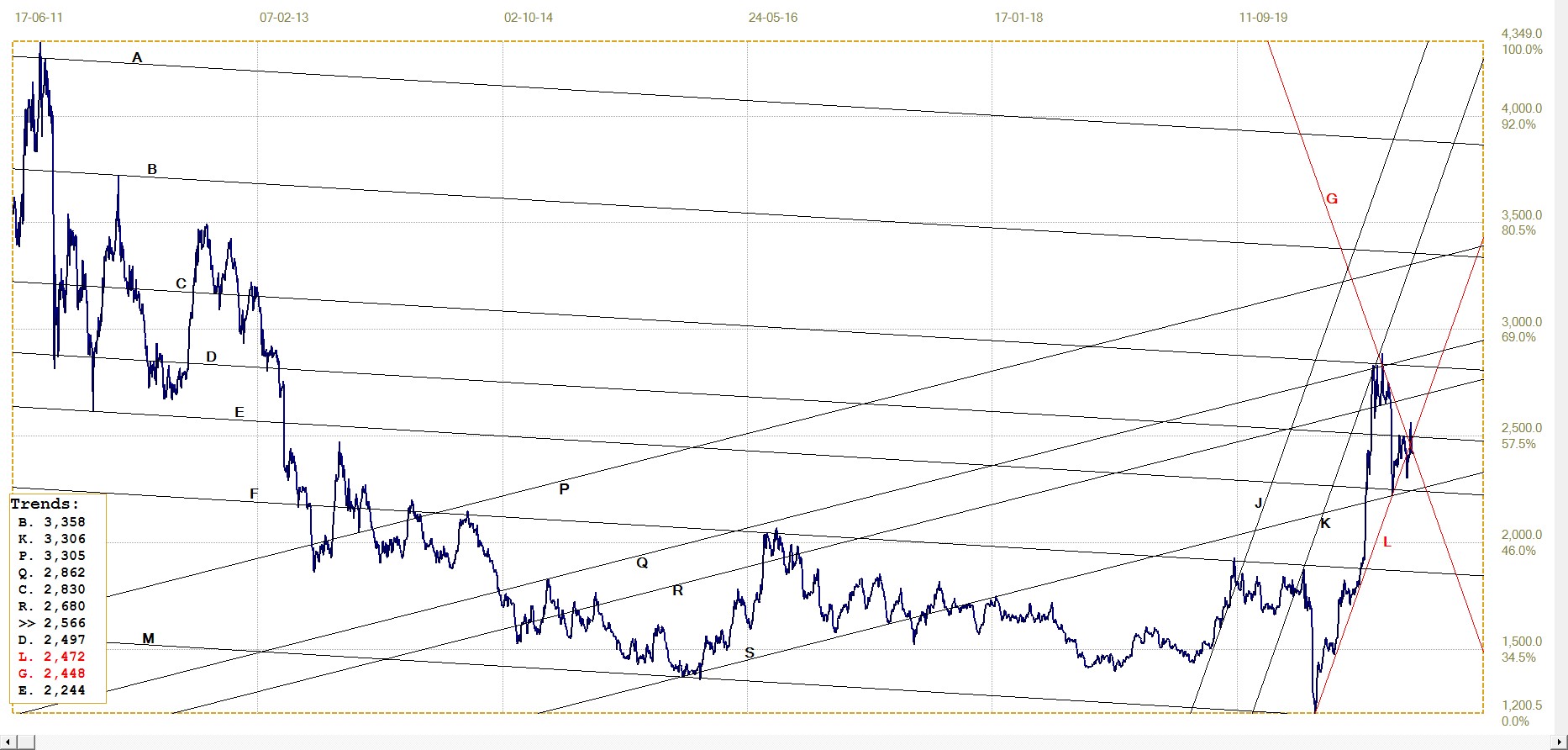

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1890.90 (www.kitco.com)

The break below the $1900 level was a signal that the short situation was becoming untenable – more so since the fundamentals pointed to increasing demand for gold during the months to come. Clearly, the intention was to frighten the longs to close their positions and relieve the stress of the short position. Some partial success was achieved as the Comex numbers showed that a decline in the OI, presumably short term speculators running for cover.

But more recently, the OI started to tick higher again - gold bulls gathering funds to take advantage of the current low prices. Will we see a new strong selling attack to clear the stops of the new purchases and test the resolve of the longer term bulls who have sat on their positions almost since the end of July? That would require the price of gold to drop probably well below $1850 and open the door for the really big players to grab positions at such low prices that December contracts would offer a near immediate profit and make for delivery of cheap gold to carry into 2021.

Euro–gold PM fix

The dollar has been sideways and range bound since early in August. The swings in its value has been high, but mostly held above 92.2 on the dollar index and below 94.0 – enough to keep the euro price of gold mostly reacting to the dollar price of gold and not much influenced by the value of the euro.

The late recovery in the dollar price last week, also had the euro price of gold moving higher to break marginally back above line B (€1593) and back into bull channel KL (€1593). Having held mostly above line G (€1569) since the break higher above that line, and now with the marginal breaks above resistance, the technical outlook for the euro price of gold is mildly bullish as long as the breaks higher hold.

If a rally should materialise, it is more likely to be on dollar gold strength than on euro weakness.

Euro gold price – PM fix in Euro. Last = €1600.27 (www.kitco.com)

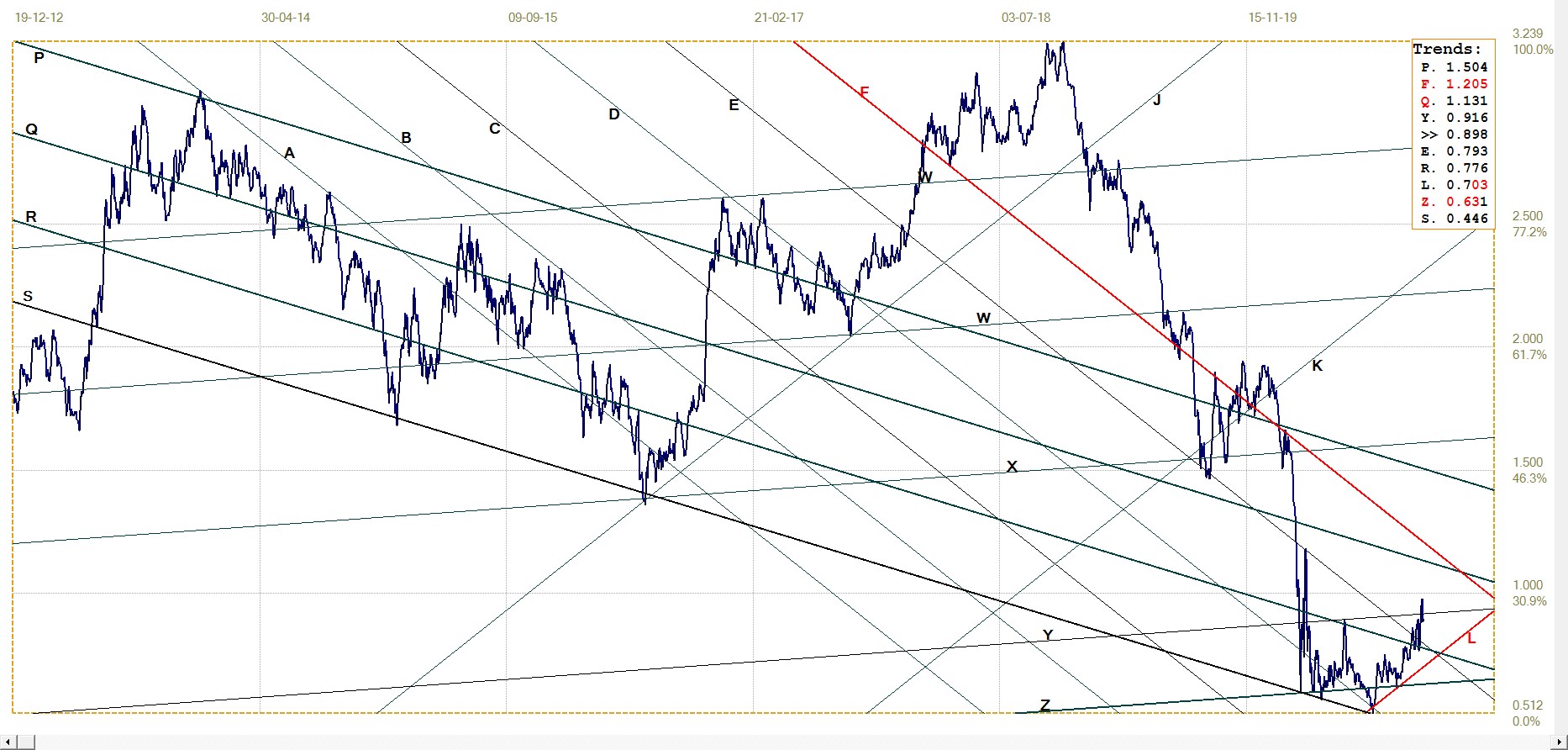

Silver Daily London Fix

The silver rally two weeks ago ended the week with the London silver fix at $25.66 and that was as far as it went. Last week saw silver pulling back – or being pushed lower – to break a little below bull channel KL ($24.72) and line G ($24.48). Then the fix became static for three days, being fixed practically unchanged from $24.24.

This again confirms that silver is the big fear of the banks.

Silver daily London fix, last = $24.245 (www.kitco.com)

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 0.898% (www.investing.com )

Long term analysis of the US 10-year Treasury note provides technical evidence that that current bull market has reached its end. This conclusion remains in place as long as the yield remains above channel SR (0.776%) and also within channel KL (0.703%).

However, given the situation as it had developed in the US during the past week or so, matters could change dramatically in either direction to affect the bond market, also in either direction.

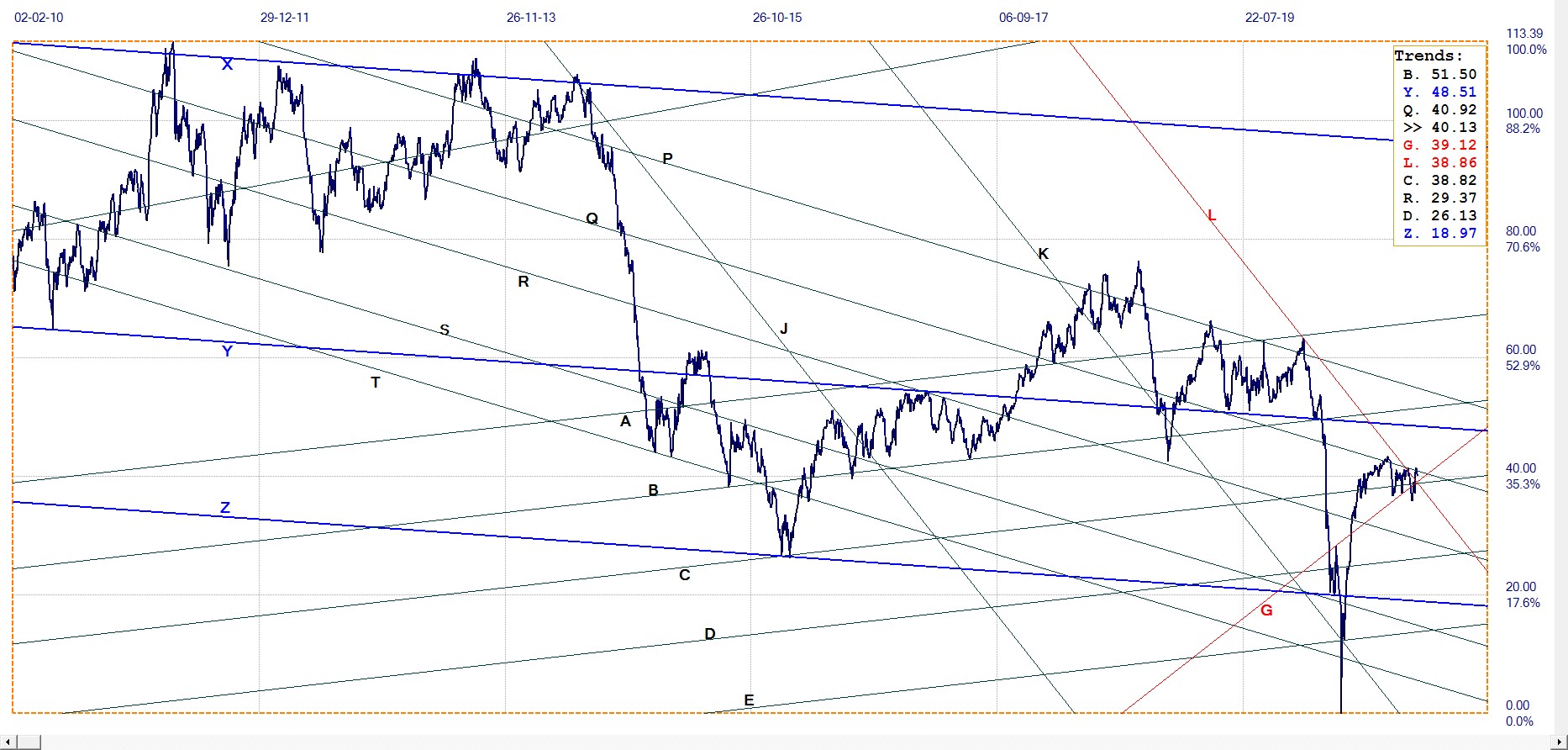

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $40.13 (www.investing.com )

The recent weakness in the price of crude was last week considered a result of the increasing number of COVID infections – which should still have had a similar effect this past week. Now the bounce in the price could be due to the resolution of who will be the new president – which implies that the rally could extend or reverse as suddenly as it had started depending on how the election is proceeding.

© 2020 daan joubert

*********