The Fed’s Normalization And Gold

share

share

share

share

share

share

share

share

share

share

The Fed hike is not the end of the world. The U.S. economy experienced many tightening cycles. Actually, many analysts are citing past rate hike environments as a guide to the future. However, three things make this tightening cycle (if there are more hikes at all) unique. First, the U.S. central bank increased interest rates when the economy is actually decelerating and the manufacturing sector is in a recession. This makes new hikes less probable, while increasing the odds for the U.S. recession in the new year. Both effects are fundamentally positive for the gold market.

The Fed hike is not the end of the world. The U.S. economy experienced many tightening cycles. Actually, many analysts are citing past rate hike environments as a guide to the future. However, three things make this tightening cycle (if there are more hikes at all) unique. First, the U.S. central bank increased interest rates when the economy is actually decelerating and the manufacturing sector is in a recession. This makes new hikes less probable, while increasing the odds for the U.S. recession in the new year. Both effects are fundamentally positive for the gold market.

Second, the Fed has never hiked before from almost zero. Thus, to normalize its monetary stance and provide itself with the necessary ammunition to fight the next downturn, the Fed should hike to at least 3.5 percent (usually, the U.S. central banks cut the federal funds rate by 350 basis points in each easing cycle). Given the slow and gradual tightening cycle, the Fed will be generally unprepared for another recession. The U.S. central bank will then be forced to implement another round of quantitative easing, or perhaps even to implement helicopter money and negative interest rates.

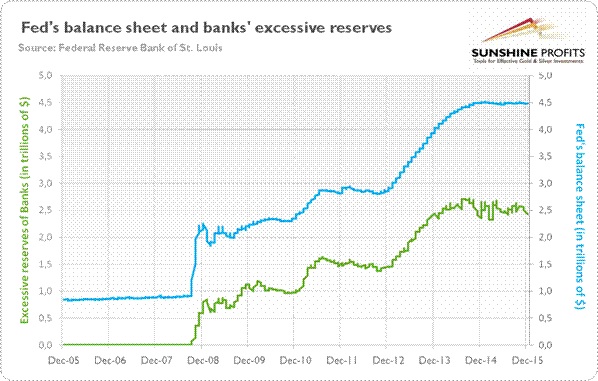

Third, the Fed has never raised its interest rates with the interbank lending market practically dormant, massive excess reserves at commercial banks (worth around $2.4 trillion) and enormously expanded balance sheets. The U.S. central bank’s balance sheet is now around $4.5 trillion, as opposed to the $800-900 billion range before the crisis (see the chart below).

Chart 1: The Fed’s balance sheet (blue line, right scale, in trillions of $) and the bank’s excessive reserves (green line, left scale, in trillions of $) from 2005 to 2015.

In normal times, the U.S. central bank controlled the federal funds rate by changing the supply of reserves via open market operations. When the Fed wanted to raise rates, it would sell securities, which led to a reduction of reserves in the banking system. As the reserves become scarcer, the interest rate increased. However, because of the Fed’s quantitative easing programs, the banks are now awash with reserves, so they do not need to borrow funds from each other as they used to before the financial crisis. It means that to raise interest rates by open market operations, the Fed would need to unwind all of its earlier purchases (around $3.6 trillion since 2008).

Therefore, the U.S. central bank will be using two other tools during the normalization process: interest on excess reserves (IOER) and reverse repurchase operations (RRP). The IOER is interest paid on funds held at the Fed in excess of what is required, and it would be the primary tool for raising the federal funds rate. According to the U.S. central bank, the IOER puts a “floor” on the main Fed rate, as no bank would want to lend money to other banks at lower rates than it may safely park cash at the Fed.

However, there is a notable problem with the IOER. It does not create a perfect floor since it is only available to depositary institutions (among other problems), which do not have accounts with the Fed, so they would lend money for less. This is when the reverse repurchase operations enter the scene. In the RRP, the Fed sells securities to the non-banks (such as money market funds) and agrees to buy it back the next day at a specified price. In essence, the U.S. central bank takes an overnight collateral loan, which also puts a floor under the federal funds rate, as no investor would lend money to commercial banks at a rate lower than what the Fed is willing to pay in the RRP. As one can see, the main difference between these two interest rates is different eligible entities. Since the investors who can participate in the RRP are the same ones who might undercut the IOER, the changes in both rates should push up the federal funds rate. Indeed, the Fed’s strategy has worked so far.

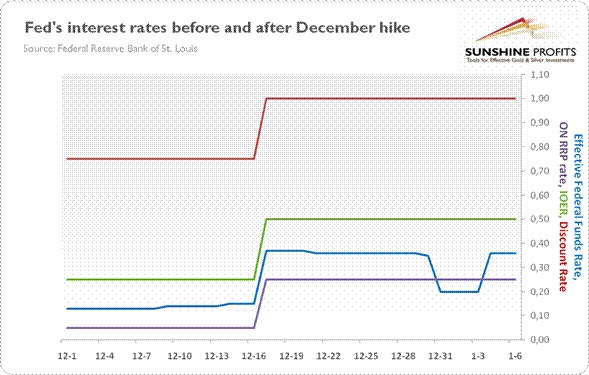

Along with the federal funds rate, the U.S. central bank raised the IOER to 0.5 percent, while the overnight RPP rate rose to 0.25 percent (it also increased the discount rate to 1.00 percent. That is, the rate charged to depository institutions on loans they receive from the Fed’s lending facility, which creates the “ceiling” on the federal funds rate, since no banks should want to borrow money from other banks at a higher rate than from the U.S. central bank. Consequently, the effective federal funds rate was traded on average at 0.375 percent after the Fed’s hike (a level three times higher than 0.125 percent in 2015 before the hike!). The chart below shows the Fed’s interest rates before and after the December hike. As one can see, the effective rate is actually formed between the ON RRP rate and IOER, which were set during December meeting at, respectively, the lower and upper bounds of the federal funds target.

Chart 2: The Fed’s interest rates (discount rate – red line; green line – IOER; blue line – effective federal funds rate; purple line – ON RPP rate) before and after December hike (between December 1, 2015 and January 6, 2015).

Therefore, it seems that the Fed, by using new tools, retained control over its main interest rates. However, there may be some unintended consequences of using them. First, paying banks for holding reserves at the Fed provides banks with easy money and discourages them from participating in the interbank market and from more intense restructuring (not to mention the ethical and political issues related to the fact that the U.S. central bank pays tens of billions of dollars to the banks not to use the trillions it paid them before). Second, the use of RPP would expand the Fed’s intermediation in short-term funding markets, which could crowd out private financing (the U.S. central bank is already the largest lender in the tri-party repo market), magnifying flight-to-quality flows and their repercussions during crises – as the investors will likely to seek the safety of the Fed (the ultimate ‘risk-free’ counterparty) instead of lending to private institutions – and promote ‘shadow banking’ (by transacting with non-banks) that are largely beyond the Fed’s regulatory scrutiny.

The bottom line is that the Fed raised the federal funds rate in December. After the end of quantitative easing, the hike was the next step toward the normalization of monetary policy. There is still a long way to return to normal monetary policy, as the Fed should raise interest rates significantly above zero and unwind its balance sheet. Therefore, the Fed stance will remain accommodative for a long time, as the U.S. central bank will not start selling its assets until the normalization of the federal funds rate is well under way. This is very good news for the gold market, since the quick normalization of the Fed’s balance sheet would boost the real interest rates, which are negatively correlated with the price of bullion. Another piece of positive news for the gold bulls is also that the tightening cycle would be slow and gradual, and based on the use of relatively new tools, such as IOER and RRP. As the Fed is entering unchartered waters, the use of these interest rates could alter financial markets in unpredictable ways and further impair the functioning of free markets and risk loss of the Fed’s credibility in case of losing the control over the federal funds rate in case of some negative shocks.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

share

share

share

share

share

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017. He is a board member of the Polish Mises Institute of Economic Education, author of several dozen scientific publications (including in such periodicals as the Journal of Risk Research, Prague Economic Papers, Quarterly Journal of Austrian Economics, and Research in Economics), and a regular contributor to GoldPriceForecast.com and SilverPriceForecast.com. His two books, Money, Inflation and Business Cycles and Monetary Policy after the Great Recession, are both published by Routledge. Arkadiusz is also a certified Investment Adviser, a long-time precious metals market enthusiast, and a free market advocate who believes in the power of peaceful and voluntary cooperation of people.