The Fed: A Century Of Looking At Inflation Through The Wrong End Of The Telescope

SUMMARY

- Economists - and central bankers - look at inflation through the wrong end of the telescope.

- Two good examples of this are the 1920s and what is going on today.

- In both cases, the Fed confused their observation that goods prices weren't moving much with a mistaken conclusion there wasn't any inflation.

- This mistaken belief in an absence of inflation allowed the Fed to continue to fuel enormous asset bubbles, long after these asset bubbles had begun to emerge.

- This happened in the 1920s and is happening today.

DISCUSSION

Wilhelm Ropke said of economists, "They look at inflation through the wrong end of the telescope and deflation through a magnifying glass." Proof of Ropke's observation can be found by reviewing what the Federal Reserve did in the 1920s and what it is doing now. In both cases, the Fed - myopically focused on goods prices - convinced itself there was no 'inflation' even as its monetary policies fueled two enormous bubbles.

With America's entry into World War I, prices soared and continued to do so long after the Armistice. However, in 1920, the US economy entered an enormous deflation and prices plunged well into 1921 as the economy purged itself of the considerable war induced excesses. Not surprisingly, in the aftermath of prices soaring and then collapsing, economists began to consider stable prices as a sort of economic holy-grail. The leading members of the Fed at the time - and their apologists ever since - routinely cite the fact consumer prices were not rising during much of the 1920s as evidence the Fed did not over-expand credit in the years leading up to the Depression. Indeed, just before the Depression broke, John Maynard Keynes praised the "successful management of the dollar by the Federal Reserve Board from 1923" as a "triumph" of currency management. (1) Much later, Milton Friedman claimed the "high tide" of the Fed was its success in maintaining stable prices throughout the 1920s. (2)

To put Keynes' and Friedman's praise of the 1920's Fed another way, how could anyone accuse the Fed of overstimulating the economy when consumer prices didn't move for years on end? The answer to this question is quite simple. The simple fact of the matter is a central bank's irresponsible monetary policies don't have to show up as rising prices for consumer goods. Indeed, in the case of the 1920's Fed, there was a very good reason the Fed's disastrous monetary policies didn't show up as higher prices for consumer goods; the Industrial Revolution.

The Industrial Revolution was a revolution in productivity. The increased productivity of the Industrial Revolution puts the productivity increases of today's 'high tech' era to shame. As a result of harnessing different forms of energy - first steam, later the chemical energy in gasoline and then electricity - man's physical burdens became much lighter. A few machines could do the work of hundreds of people. Heavy items could be loaded onto a steam-powered locomotive and moved effortlessly across the country. Trucks could then distribute these same items to individual homes and businesses. Electric motors drove pumps to provide irrigation to formerly barren lands or powered machines in factories to make production easier. As early as 1887, the Bureau of Statistics in Berlin, Germany noted that steam engines alone were doing the work of 1-billion men; three-times the working population of the earth at the time! (3)

By harnessing all this mechanical and electrical energy and directing it toward productive ends, the production of goods exploded. Not only did the production of formerly existing goods explode, but all sorts of inventions led to goods that never existed before. All this increased production put a downward pressure on prices. Because it was so much easier to produce goods and the quality of goods increased so quickly, it made perfect sense for the price of these goods to go down. However, economists of today believe there is nothing worse for an economy than falling prices. However, as the example provided by the Industrial Revolution proves, a healthy, growing economy that is experiencing large gains in productivity should produce falling prices for all types of goods.

Regrettably, the downward pressure on prices from the Industrial Revolution was almost completely counteracted by the monetary policy of the Fed. Instead of prices falling - which the productivity gains of the Industrial Revolution should have produced - prices for goods generally stayed the same because of the Fed's credit inflation. In essence, the price decreases produced by the Industrial Revolution were matched by the price increases created by the Fed via its inflationary monetary policies.

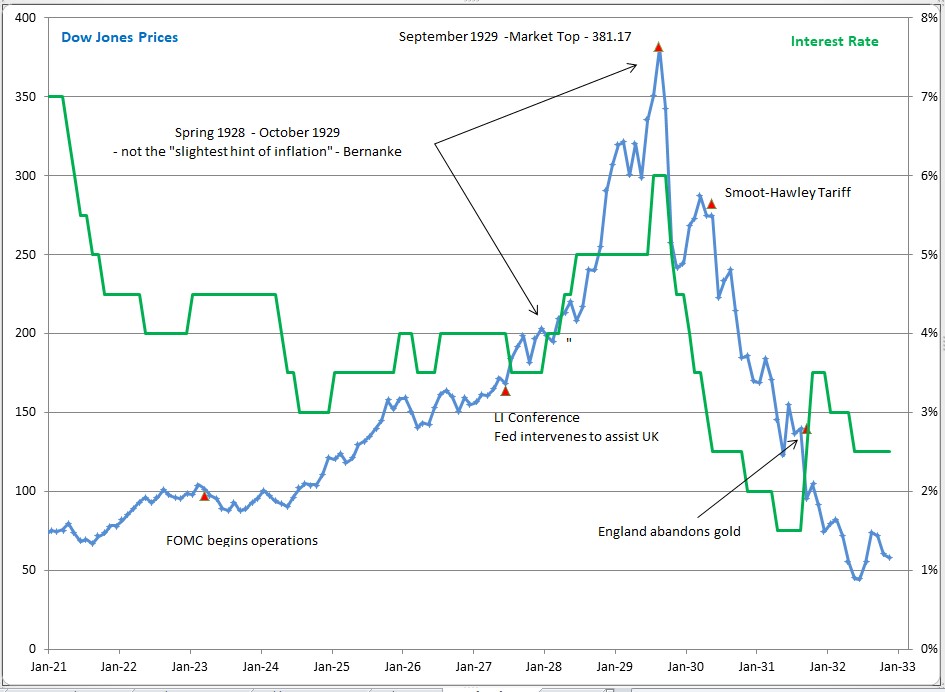

The Fed's credit inflation most obviously manifested itself in the price of assets like stocks and real estate. The productivity gains of the Industrial Revolution could do nothing to mask or mitigate the rise in asset prices during the 1920s. From April 1923 - the start of the Fed actively intervening in the economy via the FOMC - through September 1929 - the eve of the stock market crash - stock prices rose from 101 to 381; an average annual gain of nearly 23%. The rise in stock prices was being fueled - almost exclusively - by the Fed's disastrous monetary policies; the July 1927 conference of central bankers in particular. (4)

Writing in 1934, the great British economists, Lionel Robbins, was fully aware of how the Fed's apparent success in 'currency management' and holding the price level constant had actually set the stage for an enormous, world-altering economic disaster. Robbins wrote,

"From the point of view of the historian of the recent crisis, nothing can be more important than the propaganda for a managed currency. It encouraged the belief that the stable-price level was the be-all and end-all of monetary policy...It led to an extravagant admiration of the policy of the Federal Reserve System at a time when the policy of the Federal Reserve System was sowing the seeds of the slump." (5)

John Wayne famously said, 'life is hard; it's even harder if you're stupid.' Sadly, the Fed would prove itself stupid and repeat the exact same mistakes from the 1920s today. The Fed remains myopically focused on the consumer price level and continues to ignore enormous increases in asset prices. An example of this blindness to asset prices is provided by a speech Ben Bernanke gave on November 08, 2002. The occasion of the speech was Milton Friedman's 90th birthday, and Bernanke spoke about the Great Depression. In his speech, (6), Bernanke criticized the 1920s Fed for raising interest rates in the spring of 1928. Not only does Bernanke fail to mention the Fed's disastrous policies in the wake of the July 1927 conference of central bankers, which lit a fuse under the stock market, he claims in the spring of 1928 there wasn't the 'slightest hint of inflation.'

As Figure 1 shows, Bernanke's assessment of inflation in the spring of 1928 - even with the benefit of hindsight - is completely wrong. Sure consumer prices weren't going anywhere, but look at stock prices shooting straight up! What better evidence of the Fed's massive contribution to today's bubbles could there possibly be than for Ben Bernanke to fail to see the exact same contribution the Fed made to the bubble that led to the Great Depression.

FIGURE 1:

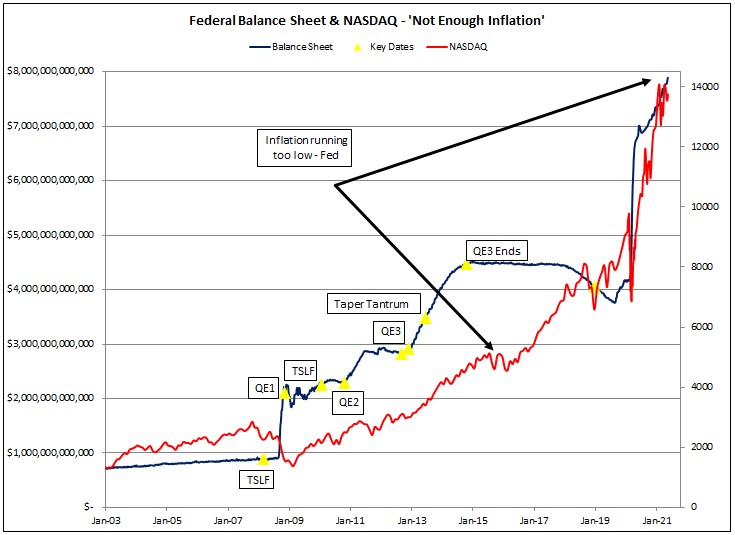

More recently, the Fed has bemoaned - for years on end - what it believes is the economy's biggest problem; insufficient inflation. Ignoring the hugely inconvenient fact that a healthy economy produces lower prices and an economy doesn't become healthy because of higher prices, look at Figure 2 and the NASDAQ's performance. From 2015 until now - a period of more than 6-years where the Fed claims there isn't enough inflation - the NASDAQ increased almost 200%.

FIGURE 2:

The NASDAQ 100 ended 2020 with a market capitalization of approximately $15-trillion, which would put it up $10-trillion since 2015. Yet the Fed would have us believe the economy doesn't have enough inflation and even more expansion of banking credit is required. This type of thinking didn't make sense in the 1920s and it doesn't make sense today.

********

After serving six years in the U.S. Air Force and obtaining the rank of Captain, Peter Schmidt has spent the rest of his professional career in the petrochemical, oil refining and power generation industries. He has worked as a rotating equipment engineer at chemical plants and refineries in Louisiana, New Jersey, St Croix and Texas, and has consulted in these industries as well. He has travelled to Angola, Argentina, Australia, Austria, England, France, Germany, Japan, Libya, Scotland, South Korea, Spain, Turkey and the UAE to complete various short-term assignments. Given his military and technical background, Peter was particularly struck by the fact so few attempts had been made to comprehensively understand the financial crisis. It was this that prompted him to prepare the information on this website as well as the book he is seeking to publish – Elites in Name Only – the Financial Crisis. Peter has B.S. and M.S. degrees in mechanical engineering from Lehigh University, is a licensed professional engineer in California and Louisiana, and a private pilot. He is the holder of two patents.

After serving six years in the U.S. Air Force and obtaining the rank of Captain, Peter Schmidt has spent the rest of his professional career in the petrochemical, oil refining and power generation industries. He has worked as a rotating equipment engineer at chemical plants and refineries in Louisiana, New Jersey, St Croix and Texas, and has consulted in these industries as well. He has travelled to Angola, Argentina, Australia, Austria, England, France, Germany, Japan, Libya, Scotland, South Korea, Spain, Turkey and the UAE to complete various short-term assignments. Given his military and technical background, Peter was particularly struck by the fact so few attempts had been made to comprehensively understand the financial crisis. It was this that prompted him to prepare the information on this website as well as the book he is seeking to publish – Elites in Name Only – the Financial Crisis. Peter has B.S. and M.S. degrees in mechanical engineering from Lehigh University, is a licensed professional engineer in California and Louisiana, and a private pilot. He is the holder of two patents.