Gold Is “Coiled” and Looks Set To Surge Like Natural Gas — Bloomberg Intelligence

– Gold’s “setup” is “similar to natural gas before its big rally”

– Gold is gaining favour over stocks, bitcoin and cryptos

– Metals may be primary beneficiaries of imminent greenback peak

– Silver “appears ready for a potential longer-term recovery”

– GoldCore editors note: Natural gas is 56% higher year to date

By Bloomberg Intelligence (appeared first on the Bloomberg Terminal)

Metals should be primary beneficiaries of an imminent greenback peak, with normalization in U.S. stock-market out performance, Federal Reserve tightening near a finish and the trade-weighted broad dollar approaching multiyear highs.

Though the dollar tops the list of this year’s best performing major assets, gold and copper show divergent strength. Industrial metals appear to be at a discount in a bull market with favorable demand vs. supply conditions.

Indications from precious metals, notably gold, offer a setup that’s similar to natural gas before its big rally.

Bound to historically compressed trading ranges with many typical pressure factors nearing multiyear extremes, precious metals appear close to a maximum loss of faith vs. the strong stock market and greenback.

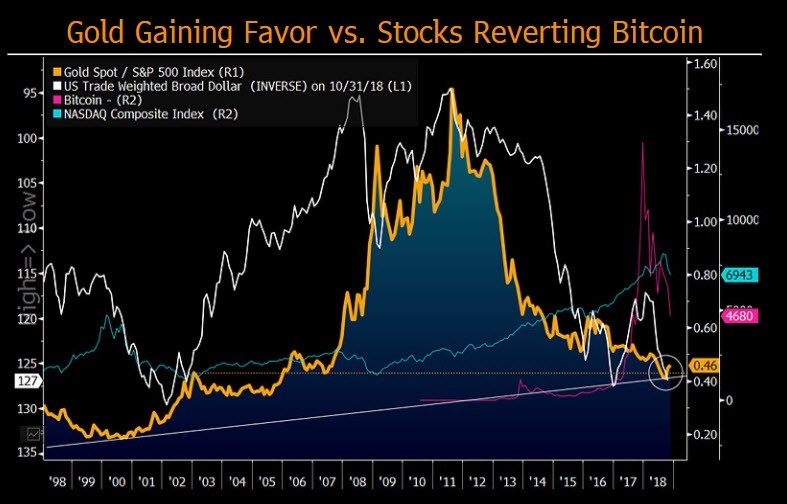

Gold is low vs. stocks if dollar has peaked

Gold should shine vs. stocks, particularly if the dollar stops advancing. Our graphic illustrates that the gold-to-stocks ratio is potentially bottoming from a good support level despite a resilient greenback. A declining U.S. equity market is a primary force to pressure the dollar, supporting metals. Mean-reversion risks in the trade-weighted broad dollar near the 2002 and 2016 highs may outweigh further appreciation potential.

Reversion in stock prices and Bitcoin toward their means is more than a coincidence, in our view. They’ve rallied together in the past few years with a common support factor — global quantitative easing.

Cryptocurrencies, considered alternatives to fiat currencies such as the dollar, gained plenty of advocates as global central banks rapidly increased money supply to offset deflationary forces.

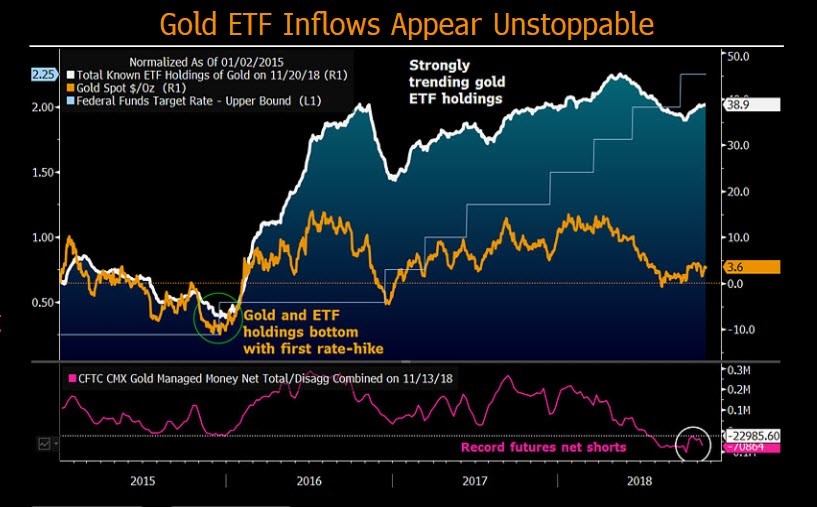

Gold ETFs to prevail vs. record short futures

Gold ETF inflows appear unstoppable absent a severe bear market, which is unlikely with inflation picking up, an extended stock market and the dollar near multiyear highs. Resolute gold ETFs are focusing on portfolio hedging and have greater upside vs. downside potential, in our view. Representing about 70% of all commodity ETFs, total known gold holdings have increased about 10x the rate of change in the spot price since the start of 2015. In this rate-hike cycle, ETF holdings are up about 50% vs. 15% for spot gold. ETFs’ gold positions continue to increase despite this year’s lower spot price.

Buy-and-hold-focused ETFs are facing off with more-speculative futures. Managed-money net gold positions haven’t recovered much from the record-short levels reached in October, which is providing a bid below the market.

Gold ready to follow the lead of natural gas

Much like natural gas earlier this year, gold has the drivers in place to rally from its compressed range. Increasing inflation and debt levels are positive companions, as is gold’s divergent strength to the dollar, which is vulnerable as it nears a good resistance level.

GoldCore editors note: Natural gas is 56% higher YTD

Since the start of the current Federal Reserve tightening cycle, and despite rallies in the metal’s traditional adversaries — the greenback (up 5% on a trade-weighted basis) and the stock market (S&P 500 up 36%), the dollar price of gold is up 14%.

With rate hikes nearing a potential end-game, gold is ripe to rally. The narrowest 24-month Bollinger bands for the longest period in 16 years indicate the metal’s upside. For gold to decline, it would likely need the dollar to remain above multiyear highs, plus a decline in equity-market volatility.

Silver backed to key support, dollar resistance

The trade-weighted broad dollar is near a peak and silver a bottom, in our view, and the potential for mean reversion should outweigh continuing-the-trend risks. Silver, among the most negatively correlated to the dollar and positively to industrial metals, appears ready for a potential longer-term recovery. For it to stay down — about 15% this year — we’d need to see sustained dollar strength and weakness in industrial metals and gold. That’s unlikely. Near multiyear highs, dollar risks are tilting toward reversion, notably if U.S. equities keep sagging.

Rate-hike expectations have begun to ease, stalling the greenback rally. Significant for silver — often called leveraged gold — would be a peak in the dollar. If silver catches up some to industrial metals, it would be closer to $20 an ounce, vs. about $14.50 today.

Access the full Bloomberg article here & the full Bloomberg Commodity Outlook (December 2018 Edition) here

*********

Mark O'Byrne is executive and research director of www.GoldCore.com which he founded in 2003. GoldCore have become one of the leading gold brokers in the world and have over 4,000 clients in over 40 countries and with over $200 million in assets under management and storage.We offer mass affluent, HNW, UHNW and institutional investors including family offices, gold, silver, platinum and palladium bullion in London, Zurich, Singapore, Hong Kong, Dubai and Perth.

Mark O'Byrne is executive and research director of www.GoldCore.com which he founded in 2003. GoldCore have become one of the leading gold brokers in the world and have over 4,000 clients in over 40 countries and with over $200 million in assets under management and storage.We offer mass affluent, HNW, UHNW and institutional investors including family offices, gold, silver, platinum and palladium bullion in London, Zurich, Singapore, Hong Kong, Dubai and Perth.