Gold

share

share

share

share

share

share

share

share

share

share

Oil has traded stronger on the threat of supply interruptions in the geopolitically sensitive Middle East (the Arabian Peninsula, the Levant, Turkey, Egypt, Iran, and Iraq). Sean Lusk, co-director of commercial hedging at Walsh Trading, told Kitco News he sees gold rising no matter what bond yields do, and oil providing an additional boost.

WTI crude was at $81 a barrel on Oct. 8, the day of the Hamas attacks on Israel; it last traded at $83.98.

Lusk noted the latest US CPI and PPI numbers, along with retail sales figures, all show that inflation is coming back. World events plus the US Congress being in disarray could mean pullbacks in the US stock markets, plus gas and energy prices are headed up and people are maxing out on their credit cards.

The Economist quoted Robert Gates, the former defence secretary who served Republican and Democratic presidents alike, who recently issued a bleak warning. America faces an unholy alliance of China, Russia, Iran and North Korea, yet cannot muster a coherent response.

“Dysfunction has made American power erratic and unreliable, practically inviting risk-prone autocrats to place dangerous bets—with potentially catastrophic consequences,” he wrote in ‘Foreign Affairs’.

While the job market is doing fairly well, a number of strikes led by the United Auto Workers union mean that wage inflation is probably going higher.

“So with those factors, if that’s not a perfect storm for precious metals or safer havens, I’m not sure what is anymore,” Lusk said, adding his prediction of $2,100 an ounce.

I couldn’t agree more, having committed my gold bull market prediction to an AOTH post just five days after the attack on Israel. I said now may be an opportune time to own gold considering the heightened level of geopolitical turmoil in the Middle East, combined with macroeconomic uncertainty, in particular stagflation and the weak fiscal position the United States finds itself in.

Geopolitics Stagflation and Gold – Richard Mills

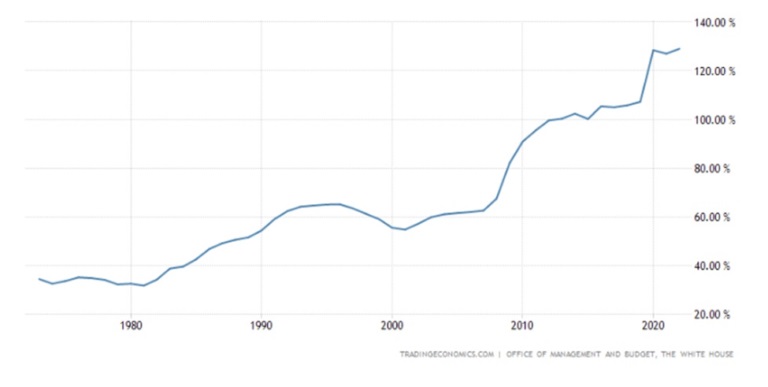

In an interview on CNBC, iconic investor Paul Tudor Jones said “It’s a really challenging time to want to be an equity investor and in US stocks right now,” noting “You’ve got the geopolitical uncertainty… the United States is probably in its weakest fiscal position since certainly World War II with debt-to-GDP at 122%,” a number which will keep rising to 195% in 2053 according to the Congressional Budget Office (CBO).

As we at AOTH have stressed, staggeringly high debt is what differentiates the current economic environment from previous periods, especially the inflationary late 1970s.

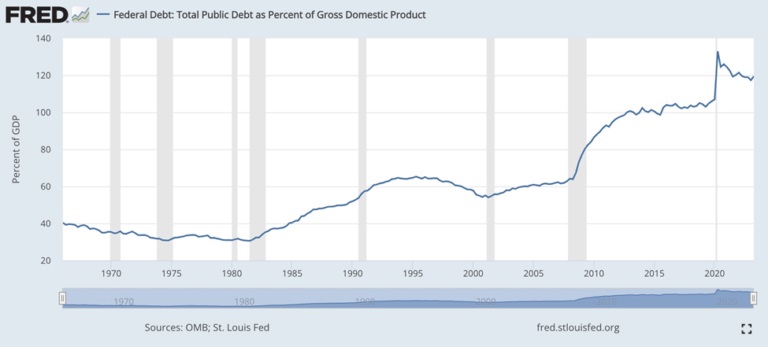

The US debt to GDP ratio in the ‘70s was around 35%. Today it is nearly three and a half times higher, at 119%.

Source: FRED

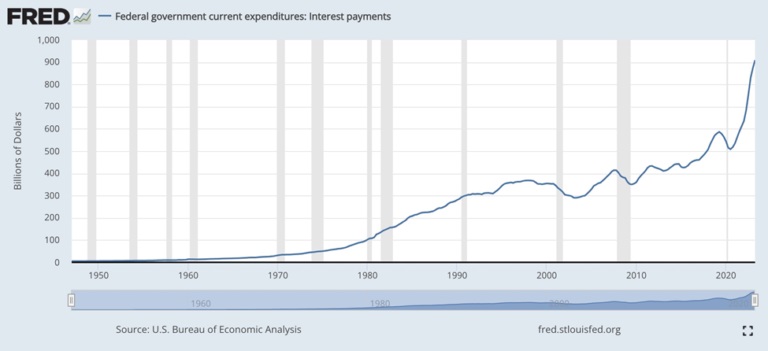

Source: FREDThis severely limits how much the Fed can raise interest rates, due to the amount of interest that the federal government is forced to pay on its debt.

During 2021, before interest rates began rising, the federal government paid $392 billion in interest on $21.7 trillion of average debt outstanding, @ an average interest rate of 1.8%. We calculated if the Fed raised the federal funds rate to 4.6%, interest costs would hit $1.028 trillion — more than 2021’s entire military budget of $801 billion!

Interest on the debt to track to exceed military expenditures

We’ve already blown past that. The FFR is 5.5%, compared to 3.5% a year ago.

Each interest rate rise means the federal government must spend more on interest. That increase is reflected in the annual budget deficit, which keeps getting added to the national debt, now sitting at a shocking $33 trillion.

Paul Tudor Jones agrees, stating that “as interest costs go up in the United States, you get in this vicious circle, where higher interest rates cause higher funding costs, cause higher debt issuance, which cause further bond liquidation, which cause higher rates, which put us in an untenable fiscal position.”

Source: FRED

Source: FREDNow throw in escalating Middle Eastern violence, which in the worst-case scenario could bring in a cascade of countries including the US, Iran, Egypt, Jordan, Syria and Saudi Arabia, and gold starts to look extremely attractive as a safe haven.

Gold analyst Adam Hamilton offers a different explanation for why gold is looking bullish. It has to do with the winding down of short positions that built up following the Fed’s late-September FOMC meeting. Fed officials slashed their 2024 rate cut projections from 100 basis points to 50bp, a move the market saw as hawkish. Investors flooded into US dollars, making Treasury yields soar, which “unleashed withering gold-futures shorting hammering gold lower,” Hamilton wrote.

Then came the attack on Israel.

“Resulting exploding geopolitical risks make it way more dangerous to short leveraged gold futures. So odds are the mean-reversion normalization buying to unwind those bets will continue. That will keep driving gold back higher, and the gold stocks will amplify its gains like usual. It sure looks like major uplegs are being born!” he wrote.

Returning to unsustainably high debt, Quoth the Raven notes that “we are standing “on the edge of volatility like never before.”

Point one: rates have been at 5% before but never with $33 trillion in debt outstanding. The chart below of US debt-to-GDP shows the ratio at around 130%.

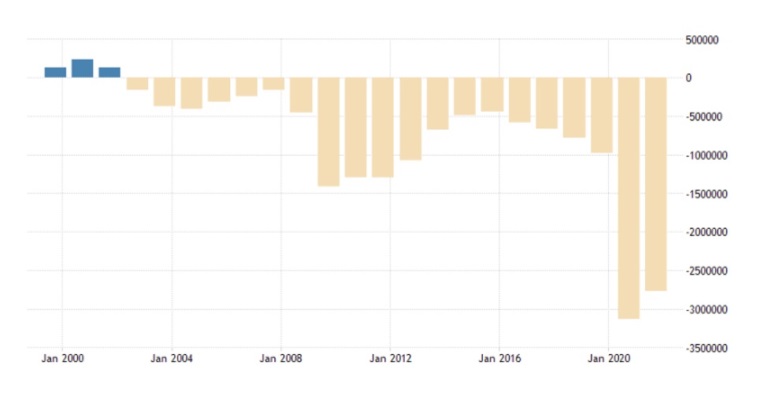

Point two: the problem is made worse by excessive government spending, which politicians cannot seem to control. The government has been in a deficit position since about 2003, and it has gotten progressively worse, as the yellow bars on the chart below show.

According to the Institute of International Finance (IIF), global debt rose $10 trillion to a record $397T in the first half of 2023, despite tighter credit conditions.

Shiffgold notes, Over the last decade, global debt has increased by a staggering $100 trillion. Combined government, household and corporate debt hit 336% of global GDP in the second quarter of this year. The global debt-to-GDP ratio has increased by 2 percentage points this year. Prior to 2023, the global debt-to-GDP ratio had declined seven straight quarters after reaching a record of 360% at the height of the global pandemic government lockdowns.

About 80% of the new global debt was piled up by developed nations, with Japan, the US, Britain and France leading the way. Among emerging markets, the largest economies saw the biggest debt increases, including China, Brazil and India.

“As higher rates and higher debt levels push government interest expenses higher, domestic debt strains are set to increase,” the IIF said in a statement…

The US government is over $33 trillion in debt. In fact, the Biden administration managed to add half a trillion dollars to the debt in just 20 days. Meanwhile, with rising interest rates, the federal government is now spending as much to make interest payments on the debt as it is for national defense.

And there is no end to the borrowing and spending in sight.

“On top of that, we have a market that has been artificially and exponentially pumped higher through passive ETF investments, trillions of dollars of COVID liquidity, and the weaponization of the options market,” Quoth the Raven writes, naming Tesla as the poster child for the latter assertion.

And then we have the US stock markets which have been edging higher even after inflation came in above estimates and after a war in the Middle East broke out.

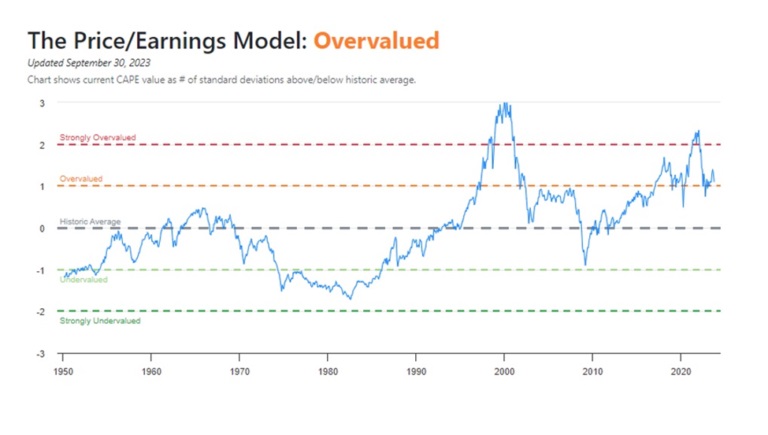

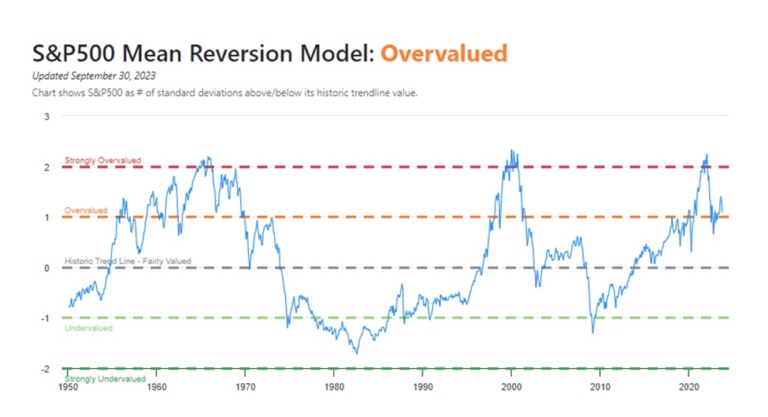

Quoth the Raven believes US stocks are overvalued, referencing the Buffett Indicator, and teetering on the edge of a big drop. If that happens, gold would clearly be on the receiving end of good news.

The old adage used to be that the stock market takes the stairs up and the elevator down. Now, with the increased liquidity, the market has taken a rocket ship up — meaning that when the elevator comes down, it won’t be an orderly ride down 5 floors on Central Park West. It’ll be like when that Red Bull guy did the 71,500 foot jump from the stratosphere…

Both the stock market and our national debt are on the last legs of a 4 a.m. Las Vegas bender…

As if this horrifying setup weren’t bad enough, there are also unprecedented geopolitical headwinds. Russia and China have paired up with nations like India and South Africa to start building a consortium seeking to do business outside the Western banking system. This ball is already rolling. That should be enough to give investors concern and encourage a risk-off climate by itself. When tacked onto our current fiscal and monetary disaster, it makes the situation truly unprecedented.

Bond markets too are also in dismal shape. The Economist notes that long-term rates began leveling out at year-end 2022 following a string of consecutive rate rises starting in March of that year.

Then in May, long-term rates continued climbing. On Oct. 1 the yield on 10-year bonds hit a 16-year-high of 4.7%. But because bond prices and yields are inversely rates, bond investors are suffering “the greatest bond bear market of all time,” states Bank of America.

It’s also bad for Uncle Sam, which has to finance America’s interest payments on its $26 trillion of public debt. According to the Congressional Budget Office, in the fiscal year ending Sept. 30, interest payments totaled $600 billion, compared to $457B the previous year. The CBO forecast such costs to be $442B, or 33% lower.

One aspect of the gold market investors shouldn’t worry about is demand.

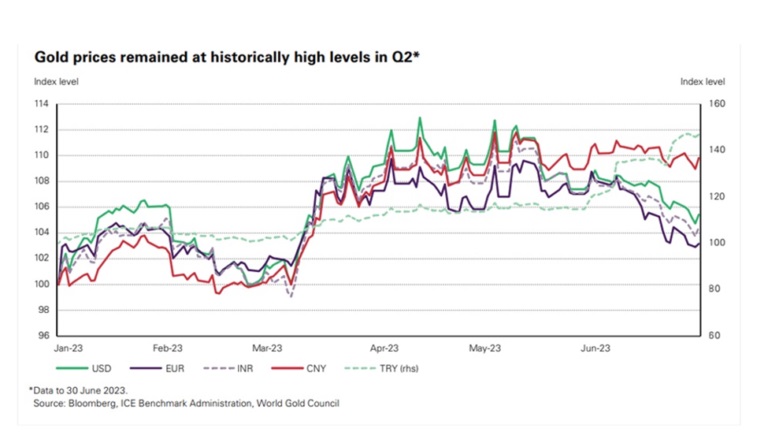

In August, the World Gold Council (WGC) put out a fresh quarterly report confirming the metal’s demand trajectory. In Q2 2023, gold investment was healthy compared with the same quarter of last year, up 20% to 256t. Jewelry consumption also strengthened modestly y/y, up 3% to 476t despite historically high (if not record) prices in most markets.

But the most talked-about source of demand is central banks, which bought a record 1,136 tonnes of gold last year and followed that up with another 228t in Q1, the most ever in a first quarter.

While central bank net buying slowed to 103t in Q2 2023, down 35% y/y from an extremely high base, the selling activity has done little to dent the underlying positive trend in central bank gold demand, which saw its highest first half on record dating back to 2000, the WGC said.

“Record central bank demand has dominated the gold market over the last year and, despite a slower pace in Q2, this trend underscores gold’s importance as a safe haven asset amid ongoing geopolitical tensions and challenging economic conditions around the world,” Louise Street, senior markets analyst at the WGC, commented.

Looking ahead, the Council expects the positive central bank trend to continue, and an economic contraction could bring additional upside for gold, further reinforcing its safe-haven asset status.

“In this scenario, gold would be supported by demand from investors and central banks, helping to offset any weakness in jewelry and technology demand triggered by a squeeze on consumer spending,” Street said.

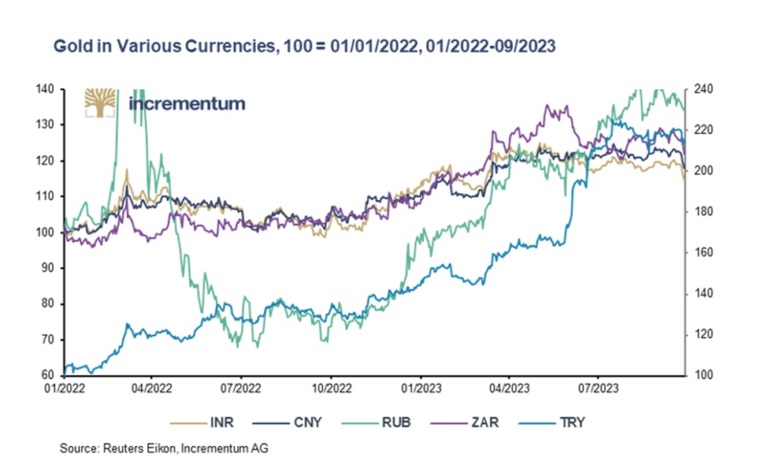

Gold Switzerland’s Ronni Stoeferle commented that shifts in economic, demographic and military weight are driving geopolitical adjustments, including gold flows, which are shifting from West to East.

In 2022, the enthusiasm for gold was seen mostly in non-Western countries. The year saw the largest purchases of gold by central banks since records began 70 year ago, at 1,136 tons. The first half of 2023 continued this trend.

China made the largest purchases, followed by Singapore, Poland, India and the Czech Republic.

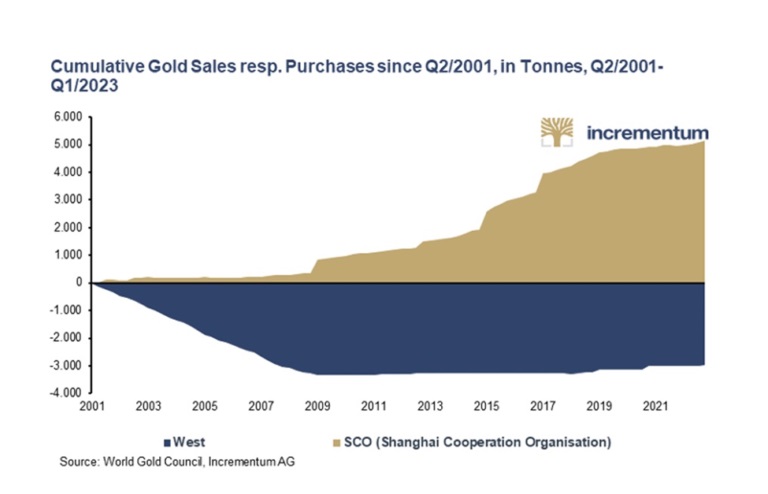

Switzerland Gold’s chart below compares the cumulative gold sales of Western central banks with the cumulative gold purchases of the Shanghai Cooperation Organization (SCO or SOC) since 2001.

Much of the buying was done by the BRICs, with central banks from four of the five BRICS countries — Brazil, Russia, India and China – buying a cumulative 2,932 tonnes of gold over 2010–2022.

At the same time, BRICS are reducing their share of US government debt by purchasing less US Treasury bonds and bills. As Gold Switzerland explains it, gold is becoming more and more interesting as a reserve asset because US Treasuries have been becoming less and less interesting as a currency reserve for more than a decade. The militarization of money by freezing Russia’s foreign exchange reserves just days after Russia’s invasion of Ukraine in late February 2022 added emphasis to this process, but did not kick it off.

The BRICS now hold only 4.1 percent of all US government debt, compared with 10.4 percent in January 2012. That is a decline of more than 60 percent…

A sign of this phenomenon: On Thursday Business Insider reported that a Treasury bond auction saw weak demand, adding to growing alarms that the explosion of US debt could overwhelm Wall Street. The US sold $20 billion of 30-year bonds but dealers had to take up 18% of the supply (compared to their usual 11%) after investors balked. In another sign of waning demand, the gap between the lowest bid price versus the average, called the auction tail, was the narrowest since 2021. The outcome was the 30-year Treasury jumping 12 basis points to 4.856% and the 10-yield yield surging 10bp to 4.7%, Business Insider wrote.

Countries such as China, the UAE and Russia are also expanding their gold trading infrastructure — allowing them to divert gold trading from traditional centers in London, New York and Zurich. As Gold Switzerland puts it, The East increasingly no longer sees itself as a customer of Western infrastructures, but offers the infrastructure itself.

Key developments include: cooperation between the Chinese and Russian gold markets; membership in gold-related institutions such as Chinese refineries now numbering 13 on the LBMA’s Good Delivery List compared to only six previously, and India opening a bullion exchange; the establishment of a Moscow World Standard; and private gold demand shifting to the East.

China and India accounted for almost half of global consumer gold demand in 2022, @ 1,600 tons, compared to just 28.7% in 2000. In the first eight months of the year, Asian gold ETFs increased their holdings by 7.7%, while

North America and Europe saw outflows of 2.3% and 6.1%. The price of gold in Eastern currencies has also increased significantly, bolstering its reputation as a wealth preservation tool.

In addition to geopolitical and macroeconomic factors supportive of gold, we also have the issue of supply. In an earlier article we proved the notion of peak gold.

The case for peak gold, silver and copper

Like peak oil, it refers to the point when gold production is no longer growing, as it has been, by 1.8% a year, for over 100 years. It reaches a peak, then declines.

in 2022 total gold supply including jewelry recycling reached 4,754.5 tonnes. Full-year demand was 4,741 tonnes, almost on par with 2011, an exceptional year for gold demand. The fourth quarter saw record demand of 1,337t.

No peak gold here, right? Demand is closely matched by supply.

But when we strip jewelry recycling from the equation, 1,144.1t, we get an entirely different result. i.e. 4,741 tonnes of demand minus 3,611.9 t of mine production leaves a deficit of 1,129.1t.

This is significant, because it’s saying even though major gold miners are high-grading their reserves, mining all the best gold and leaving the rest, they still didn’t manage to satisfy global demand for the precious metal, not even close. Only by recycling 1,144 tonnes of gold jewelry could 4,741 tonnes of demand be satisfied during 2022.

This is our definition of peak gold. Will the gold mining industry be able to produce, or discover, enough gold, so that it’s able to meet demand without having to recycle jewelry? If the numbers reflect that, peak gold would be debunked. We’ve been tracking it since 2019, and it hasn’t happened yet.

*********

share

share

share

share

share

More from Gold-Eagle