Gold: America, The Bubble

Americans believe they have the best military in the world. That said, when was the last war that America has won? However, a by-product was the mighty American industrial machine that spent decades creating the supply/chain logistics, which lowered costs, boosted profits allowing their multinationals to spread globally. However today, this exceptionalism has led to shortages from semiconductors to lumber to gasoline as the pandemic exposed the vulnerability of America’s supply chains, leading to a spike in inflation.

We also believe that American exceptionalism puts democracy under siege. Numerous red lines have passed, and beset by negativism, expensive forever wars and Trump’s protectionism, trust in America’s competence was undermined. The decay of international trading norms made countries wary of the United States. Mr. Trump only capitalized on its weakness yet the election results exposed deep divisions between the federal government and state government. Of concern is that since the election more than a dozen Republican controlled states have enacted laws to make it easier to block opposition. Unfortunately, there is not a vaccine for Trumpism and the divisive politics of today has not disappeared.

American Exceptionalism

America remains divided, racially, politically and income-wise. It is no longer united. The pandemic laid bare its differences. Seventy odd million Americans voted for the loser of the last election and a margin of less than half of one percent in three states would have seen another four years of Donald Trump. The real problem is that while Biden is popular today, his approval numbers have lagged every president, but Gerald Ford whose popularity dropped due to the pardoning of President Nixon. Although Mr. Trump is gone, his party in cult-like fashion remains loyal to the Pied Piper, undermining the election result and democracy itself. For example, the Trumpian coda of a “stolen election”, has seen the adoption of tighter election laws in GOP led states, which only deepens the political divide. While there was much made of Republican Liz Cheney’s battle within her own party, little is said that she was pushed out because the voting members were afraid to buck their constituents who continue to support Mr. Trump.

The problem is that decades of partisan gridlock has created a vacuum in the middle and widespread disaffection with the system, undermining democracy itself. The attack on the Capital and Mr. Trump’s second impeachment exposed internal divisions. Mr. Biden’s conditional election and swing to the left further polarized a divided nation as well as his own party. And despite freedom being considered a foundation of their democracy, under lockdowns a good part of the population surrendered their personal liberties in return for the belief that the government would protect them from Covid-19. But the virus and its variants have not disappeared and surprisingly only half of the population is fully vaccinated.

Mr. Biden’s spending has transformed the state, helped by three rounds of stimulus checks in a form of guaranteed income and a major step towards a welfare state supported by the progressive wing of the Democratic party. Still to come is whether he can actually pass his spending plans through a divided Congress. His swing to the left, without a mandate from voters leaves a vacuum in the centre, making the more centrist Democrats vulnerable in the upcoming midterm elections which would jeopardize their razor-thin majority.

That said, we believe, the immediate lesson of the pandemic is the failure of government. Mr. Biden’s honeymoon ended with his trillions of dollars spending spree and his recent spending attempts are mired in another Congressional deadlock on both the right and left. While America’s economy has emerged from the pandemic-induced recession because of the trillions of state-aid that allowed spending and business to reopen, the economic aftershocks of high unemployment, a contentious election and failed business borrowings still linger. What’s more, with the legacy of massive debt-financed government spending and expansive monetary policies, inflation is the steepest since the Seventies. Inflation is America’s next crisis.

Inflation is Back

Bond yields around the world reached record lows last year as central banks slashed interest rates and launched mammoth debt buying programmes to cushion their economies from the pandemic. The United States led the way, spending more than 15% of GDP and instead of dropping dollars from helicopters, deposited funds directly into Americans’ bank accounts, stoking the demand-side of the equation. Playing a key role this time is wage growth as nearly half of the US small businesses reported unfilled job openings. Fittingly, is that business must compete with a generous government job replacement scheme that pushes up inflation and pays citizens to wait out the pandemic. So far, the Biden pandemic-era government stimulus programmes total a whopping $6 trillion of welfare spending on top of several rounds of economic stimulus and central bank intervention benefiting the wealthy. Ironically, to pay for this, Mr. Biden hopes to get the rich pay by increasing tax rates, raise capital gains and reduce dividends.

Also stoking inflation are the steps countries led by the United States take to reduce dependence on supply chains and globalisation, on security grounds. In dismantling the supply chains, just-in-time manufacturing costs increased as parts for airplanes to cars to semiconductor chips were in short supply. The decision to break up supply chains caused stockpiling, distorted supply and demand and pushed up higher prices. The pandemic only accelerated the structural change.

Then there is the cost of political change. With a conservative court and GOP state-controlled legislatures, a dysfunctional Congress has brought back old-time gerrymandering. Already $2 trillion in additional spending is stuck in Congress. Biden’s own party balked at the “For the People Act” voting rights bill, which was blocked ironically by a GOP filibuster. Then there was the cost of sending out of $1,400 checks to everyone, which even resonated with criminal elements who were reported to have stolen an estimated $400 billion in unemployment claims. That too is inflationary.

Transitory or Not?

After a quarter of a century in which inflation was non-existent, prices now threaten to rise faster than consensus expectations. The aforementioned structural supply chain constraints, labour shortages, port congestion and shifts in demand driven by rounds and rounds of government stimulus have pushed prices higher. The consumer price index (CPI), one the most closely watched inflation measures, soared in June by the most in nearly 15 years.

Because inflation was on a downward course for almost half a century, an entire generation of investors and portfolio managers haven’t experienced the ravages of inflation. While the situation is unfamiliar to the current crop of fund managers, it is worthwhile to learn from history a sense of what to expect. Similarly, the same lot is not familiar with the age-old remedy of slamming on the brakes, which caused a severe recession in the eighties when interest rates were jacked up to double digit levels to defeat inflation. Deleveraging and the end of the free lunch was devastating. Of immediate concern is a potential wake-up call when Congress again debates raising the debt borrowing limits before August. Time and time again, the default limit keeps getting kicked down the road. To prevent a default on US debt, Treasury Secretary Yellen recently warned, “the failure to do so would have absolutely catastrophic economic consequences”. Does the market care?

The Fed’s narrative however is that the pick-up in inflation is transitory. Not transitory is the Fed’s record of predicting inflation. Fed Chair Powell thought the upward pressure would “resolve themselves”. But when does transitory become sustaining? Today, the embers of inflation glow brighter with bubbles in commodities, cryptocurrencies, housing and markets, fuelled by the feedstock of liquidity. Beyond that lumber, steel, and iron ore hit new records before pulling back. Copper already reached record highs boosted by supply shortfalls. Corn, soybeans and wheat are at eight-year highs. Oil recently reached six-year highs. Home prices are at their highest levels in more than two decades as low inventory levels and borrowing costs fuel demand. To be sure Mr. Trump’s tariffs helped spark the commodity boom but much of the pick-up is due to deep roots stemming from the lack of investment, broken supply chains and pent-up demand.

None of this is transitory. And despite the pick-up in the economy, the Biden administration is trying to pass yet another stimulus bill adding fiscal rocket fuel to the potent mix. Although US inflation is above the Fed’s target, the Fed remains on a Testa-type autopilot, turning a blind eye underestimating the risk of higher inflation. In the interim, companies have issued record amounts of debt, on top of record federal debt of $30 trillion, that exceeds the size of the entire US economy.

Not only has the trillions of dollars boosted stock markets and commodities but the government debt machine through the Fed’s surrogates the Wall Street bankers, has put them under considerable strain because their balance sheets are stuffed with government paper. Large amounts of reserves and ultralow interest rates have made it difficult for the Wall Street powerhouses to lend out profitability such that the Fed’s overnight reverse repo programme developed indigestion when overnight reserves topped $700 billion, clogging up the Fed’s plumbing system. And, it is not getting better. Lately most large foreign buyers have fled the scene leaving the Fed to buy up more than 50 percent of total Treasury issuances. It is expected that the Fed’s balance sheet will breach $9 trillion by 2023 compared to just over $4 trillion the end of February 2020.

Fed’s Balance Sheet

Currently, no one believes that this is a problem. However, the pandemic’s legacy will be more than a spike in inflation. Notwithstanding that the world’s biggest economy has gone on a great credit binge, racking up the world’s biggest debt, we are told that governments must deliver more vaccines, more support, stimulus and economic growth. Debt? That problem is simply kicked down the road.

The Fed’s balance sheet will be made worse by Mr. Biden’s spending plans that will jump to $6 trillion in the coming fiscal year, eclipsing Donald Trump’s $4.8 trillion budget. That spending would amount to more than one quarter of America’s GDP with annual deficits of more than $3 trillion for the second year in a row. To pay for that spending, Congress will issue debt and when the Fed buys that Treasury debt, it creates money to pay for it.

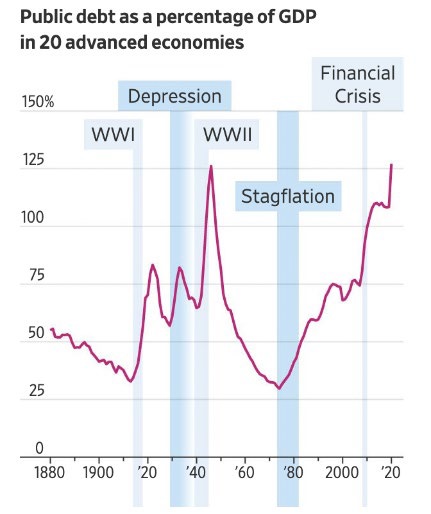

Starting with the sheer amount of debt, the Fed’s balance sheet alone has now reached $8 trillion after funding the stimulus packages of 15 percent of America’s GDP. As a result, the Fed’s assets are up 600 percent from the 2008 financial crisis. Of growing concern is that extraordinary level of monetary stimulus not only underpinned the global economy but resulted in the national debt topping the highest in history, but excludes the $65 trillion of unfunded liabilities for medicare and social security. None of this means that the United States is heading for a catastrophe tomorrow but should rates increase, or the dollar fall further or the virus has yet another variant, any nasty surprise could spell trouble.

Overlooked is that the Fed and other central banks have become important market participants holding stakes in their domestic markets. The Bank of Japan for example is the largest stakeholder owning 10 percent of Japan’s TOPIX index. The Fed too holds US corporate bond holdings including bankrupt Hertz paper, while the Bank of England owns almost 7 percent of its gilt market. Already, the International Monetary Fund (IMF) has calculated the debt to GDP of Germany at 69 percent, France at 113 percent, Canada at 188 percent and the United States at 127 percent.

However, despite the balance sheet woes, US treasury debt is tracking at near lows resulting in negative yields. While the large monetary and fiscal stimulus is out of proportion to the magnitude of the gap between supply and demand, this ugly duckling is running out of runway, as the Fed’s new doctrine of keeping rates low is tested by the ratcheting up in inflation and interest rates.

And, trade flows have changed. No other central bank has followed the Fed and the Fed’s complacency about inflation is similar to what happened in the 70s when the Fed lost control of prices. Negative rates also caused strains in the money market, forcing investors to pay to invest their funds. Today, there is a shortage of low-risk assets because the Fed’s billion dollar buying programme itself has shrunk the pool of debt. That in turn has caused distortions in the huge money market estimated at $ 4 trillion. Institutions cannot invest in negative yield instruments for too long without jeopardizing their own viability and thus some money market funds have waived fees because they are earning near zero – time is not on their side. The financial plumbing is clogging up.

What is clear is that in funding their deficits, governments have exhausted their unconventional ways to raid the private sector coffers and are left to introducing more taxes, such as taxing the one percent or the big tech players of Silicon Valley. In the quest for more revenues, governments will kill the golden goose instead of simply closing the multitude of loopholes created by themselves. Today’s complex tax code has become unwieldy, created by politicians fearful of unifying both the left and right in a common tax rebellion. It has happened before. As for the big multinationals, they can always find lower taxed jurisdictions so the threat of higher global taxes is empty. The taxpayer will again pay the brunt of taxes.

That Seventies Show

So, what could the Fed do? Abnormally low interest rates, even below the inflation rate haven’t repaired the economy. Structural problems have beset America’s international standing and the drift towards protectionism and higher rates won’t bring on new needed capacity or infrastructure. We believe that there are remarkable resemblances between the Seventies and today. Monetary conditions were loose back then and inflation was considered dormant. Markets too were complacent. Back then, the Fed also believed that the uptick in inflation was temporary since the anchovies would return and the end of the oil embargo would send prices lower. The Fed faced an awkward dilemma. They were wrong then.

Today, the Fed continues to finance the government’s budget deficits with newly minted dollars, believing that inflation is transitory. What isn’t transitory are wages, higher rents or rising prices for cars and homes. Government deficit spending policies are stoking inflation. Gambling that inflation will pull back, the Fed continues to underwrite an ultra-loose monetary policy which was the catalyst for the unexpected rise in inflation in the first place. Looking back, this is frightening. What if the Fed is wrong? The Fed as before will be late, much too late. History is repeating itself.

As the world wakes up from a pandemic-induced slumber, the talk of a return to the “Roaring Twenties” have investors and media pundits rejoicing in a “hedonistic” fervour contemplating a boom decade. Don’t get out those straw hats yet. The historical record shows that the Twenties was a sorry prelude to the Great Depression. A return to the norm is also unlikely as the persistence of the pandemic hotspots or variants means more lockdowns.

Most important is that the pandemic has exposed a widening rift between “them and us”, rich versus poor and vaccinated vs unvaccinated. Much of the income inequality is due to the fact that “the one percent” came out ahead during the pandemic while the other 99 percent needed government or state support, laying the ground for an expanded state presence, emergency powers and more legislation. These authoritarian measures, however, was at the expense of the private sector, and we believe, this “nationalisation” of the economy will likely to lead to stagflation (i.e., subpar growth, and rising inflation) as well as undermining democracy.

The expanded state presence also ushers in “income support” and as Canada discovered when it introduced a modified support scheme through “unemployment insurance”, labour shortages caused the importation of migrant workers to take over many of the jobs that Canadians now find too “low paying”. A shortage of workers also led to higher wages, better working condition and, higher inflation. All this means that the distribution of income to cover basic needs within an environment of “free money”, comes at a cost. Afterall, “womb to tomb” policies did not work in Western Europe when entitlement spending required higher taxes of 40 percent of GDP. Instead of doling out free stimulus money, why not boost neglected infrastructure or education or health-care systems. One lesson is that if we pay people not to work, they won’t. Of concern is that there is a positive relationship between democracy and economic development.

After Losing the Battle, Can We Win the Covid-19 War?

For the most part, it is that same state intervention that has resulted in failings, from the ad hoc pandemic response to PPE shortages, to lack of testing, to failure to protect seniors in long-term care home to an extraordinary death count. Governments may be able to deliver mail through rain or snow, but the failed response to Covid-19 showed an acute lack of checks and balances. Ironically, this America, the staunch defender of Hollywood and big pharma’s “intellectual rights”, is now pushing for vaccine waivers, to boost supplies, but the problem is not availability but vaccination rates are tapering off. Already the United States has declared victory over Covid-19 with full ball parks, crowded restaurants and packed airplanes.

Of concern is that the new mutations have not yet reached its peak and with the death toll climbing in low- and middle-income countries, there is a deepening gap between the rich and poor nations with the latter group facing a unvaccinated populace. The problem is not lack of money to buy vaccines but that the existing global supply and production is being hogged by the rich countries. The World Health Organization (WHO) has calculated that 11 billion doses are needed and the G7 countries only offered less than 900 million doses. The Western world has spent some $15 trillion to support its citizens but are tardy in coming up with only $50 billion for vaccines for the lesser developed nations. The global economy will rebound but growth will be uneven, depending on the jab rates in a race between the new virus strains and vaccines. It didn’t have to be this way.

Any post-mortem would reveal how governments despite advanced healthcare systems were woefully unprepared to tackle Covid-19. There was no plan for a pandemic even after SARs. There was no mass testing nor were there scientific bodies to opine on strategy because they were dismantled earlier by budget conscious governments. Then there was the grand plan to vaccinate the world’s poorest countries with a multibillion-dollar Covax programme, but that too fell short due to the lack of vaccines, particularly from India who was mired in their worst pandemic wave. Only 10 percent of the world has access to vaccines with the majority of vaccines made in the United States, China, India and the EU. Also, some of the richer nations, including Canada dipped into precious Covax supplies to inoculate their own citizens at the expense of the lessor developed nations. Lockdowns were even politicized!

Cost of Climate Change

Another problem is that for decades, scientist and activists have worried about climate change while governments were in ostrich-style denial. Now trillions are being spent on ESG (environmental, social and corporate governance). At long last companies and investors are increasingly viewing business through an ESG lens. Governments are trying to outgreen each other – it has become the “green de jour”, as a vehicle for election. Governments have installed tax advantaged wind, solar and e-vehicles with renewable energy becoming the new tax haven. Financial markets are less sure. Banning fossil fuels will turn Western Canada into an energy importer. Central bankers too have waded in, expanding their monetary powers to include ESG goals at the expense of overseeing systemic risks and ironically, it is under their watch that power hungry digital currencies have prospered.

Voters are holding governments and business to account. Investors are putting pressure on fossil fuel businesses to align themselves with the Paris Agreement. The limitation of carbon-free emissions is an enviable goal but few know or care about the economic cost. Politicians and wannabe greenies glibly push for the convenience of “net-zero” emissions or carbon zero, but the heavy cost of shutting down dirty power like the coal plants, fossil fuels, shale in the United States, oil sands in Western Canada or even the car industry is unknown. Another problem is that new supplies from wind and solar can’t cope with existing demand while existing coal and nuclear capacities are being phased out without replacements. Electricity grids are already maxed out and thus in the absence of supply, prices can only go up, which is inflationary.

Worrisome is that no country will meet their mandated targets for reducing emissions. The measures are not dissimilar to the massive stimulus packages to fight the pandemic, when few worried about the costs or the debt. While government dictates to shutdown local carbon emitting industries or sacrifice their economies, the reality is that with a world more globalized and integrated, one half has not bought into the new reality and thus it will be difficult to achieve scale or make the needed difference.

Climate Deniers

Ironically China today is often considered one of the biggest emitters yet China offsets this by becoming the largest manufacturer of zero-emission cars, solar panels and batteries. Europe is considered a leader in sustainability, legislating clean ETS benchmarks. On the other hand, America is the second largest emitter in the world and having opted out of the Paris agreement and Kyoto protocol, has yet to show leadership. No doubt Mr. Biden needs the support of a taciturn Congress but the freeze in Texas and power outages in the West has exposed America’s infrastructure and climate failings. It is not the climate that Americans should fear, it is their politicians’ intransigence to change. New technologies and new clean industries are needed. And, in the quest to quash carbon dioxide emitting industries, the cost and government subsidies will add pressure to rising inflation.

Also, looking for quick climate fixes, governments have put more controls on the private sector without government support. For example, after the pandemic and “voluntary” lockdowns were eased, industries are asked to pay a carbon tax but politicians, not surprisingly decided to funnel revenues into general government funds, not to reduce emissions. Similarly, once handy recycling programmes have become so expensive that our local governments shifted the costs to the private sector because the cost of subsidizing the recycling programmes skyrocketed when China stopped paying for our garbage. That cost will be downloaded to taxpayers. Of concern is that ESG is too important to leave to government – they already botched climate change. And, as part of burnishing their credentials, government are considering the imposition of carbon border taxes, which is yet another form of protectionism. Carbon taxes will also lift inflation.

And six years after the Paris Accord and despite trillions spent in the last decade in search of the “ESG holy grail”, measurements of carbon dioxide (CO2), averaged 419 parts per million in May, the highest level ever in human history.

China’s Ambitions Grow as Power Shifts Among Nations

For centuries, Imperial China was the Middle Kingdom, the world’s superpower. As early as the 1400s, China once taught the West about money when the Ming dynasty in 1425 introduced a silver-based currency. Silver from Latin America boosted the Chinese economy for centuries. But in the early 1800s, the Opium wars imported from the West was the beginning of China’s decline until the current century. However, in less than 100 years, China has returned as a global power, threatening to overtake the United States and again retain its commanding position.

China’s economy is set to grow nearly 9 percent this year, more than double that of the eurozone. With few Chinese travelling abroad and an upsurge in anti-China sentiment, Mr. Biden is trying to cobble a global coalition aimed at restraining China despite the G-7 making only up 40 percent of the world’s economy. China is the world’s largest manufacturer and exporter and is looking inward, beefing up its domestic markets, making consumer spending the economy’s main engine; needing Western markets even less.

Westerners believe that China’s growth was due to happenstance but like centuries ago, China’s market and goods were desired by the West. Today, China makes up 23 percent of US total agricultural exports, purchasing almost $40 billion of farm goods. China accounts for one third of global GDP, more than the United States and has become crucial source of investment and cutting-edge technology. China has a welfare system that provides subsidies, health care and pensions. Investors, particularly Wall Street are attracted to China’s financial markets, giving China another potent weapon to challenge US financial hegemony. China is the world’s the second largest economy with the second largest capital market and second largest bond market. However, this economic emergence has threatened the incumbent United States, raising the specter of a superpower tussle and being caught in the Thucydides’ Trap where in 12 of 16 past cases when a rising power confronts a ruling power, the end result was war.

America Is Worst for It

Today, China has created its own institutions, reshaped existing ones and norms, extending its influence globally from vaccines to high-speed trains to high tech to the $1 trillion Belt and Road Initiative. China last year had the strongest recovery after the pandemic of any major country and is likely to grow at nearly twice the US rate. We believe as more global investors hold Chinese assets, that will hasten the acceptance of the renminbi as a main rival to the US currency. In addition, the digitization of the renminbi and by partnering with SWIFT, they will nurture its own international payment system and reduce its dependence on the dollar. Still, China needs overseas capital to fund its growth and has opened its door to Wall Street, notwithstanding the anti-China rhetoric emanating from Washington. All this means that China following the well-worn path of America needing to demonize an adversary, first there was the Cold War against the Soviets, then Japan three decades ago and now a trade and technology war with China, America talks of outcompeting China, the reality is that America remains dependent on Chinese markets, for everything from rare earth metals, to semiconductors chips to iPhones to consumer goods. China produces half of all steel in the world and is exporter to the world. Simply, the world cannot recover from the pandemic without Chinese growth. While the West resents China’s success and recent rhetoric is a hatred of “anything Chinese”, the Chinese are well aware of their strengths. China has been waging an uphill battle for centuries, but China’s emergence as a super-power today is a strategic reality.

Be careful what you wish for. America’s ratcheting up of hostilities with China has taken another notch as blackball efforts to prohibit Americans from investing in China companies with purported links to China’s military or more stringent review of deals on “national security” grounds has elicited a reaction from China, which has increasingly turned inward pushing their tech giants to become more self-reliant. Beijing now plans to reverse the tide of Chinese investment, imposing tighter restrictions on overseas listings that threaten more than $2 trillion of shares and lucrative IPOs sending shockwaves through Wall Street. Currently there are more than 250 Chinese companies listed in New York with a market capitalisation of $2.1 trillion, according to the US-China Economic and Security Review Commission. The other big losers are the big exchanges, and of course the American investing public left on the sidelines as observers. China and the United States may get what they wish for, a lot sooner than they thought.

America’s withdrawal from Afghanistan, Iraq and Vietnam shows that the country has no stomach for another war. In the past decade, America’s shift toward protectionism and isolating China has brought consequences as China’s large economy is less dependent on demand from the West having pivoted to consumption-led growth. Investment on the other hand stands at 45 percent of national income, which remains important as the push for technological self-sufficiency has helped create China’s tech giants. Chinese leaders are also pursuing financial self-sufficiency building up its financial and trading systems, becoming “banker to the world” as well as “factory to the world”. And in a world recovering from the pandemic, the most important locomotive of growth is China, as it reasserts its place on the world stage. American businesses need China’s home markets, goods, and importantly financing. The West would be wise to collaborate rather than confront China. The danger is not China but American xenophobia.

The Dollar is Not Forever

To navigate this landscape, other central bankers have noticed, diversifying their reserves from dollars to hedge their bets against the slipping greenback, which recently hit a 4-month low on concerns that the Fed is monetizing their fiscal expansion. While it can be argued that money has no “intrinsic” value since the United States scrapped the gold standard system in 1971, the dollar is backed by the “full faith” of the government. However, with the mishandling of the pandemic, mistrust of big government, disparity in incomes and trade wars, faith in that government is lacking. History shows that this always ends badly.

US fiscal profligacy is not forever. Today the once mighty dollar’s hegemony, as a share of US dollar reserves held by central bank has fallen to 59.5 percent, the lowest in 25 years. The slide in part is due to the reduced international role that the United States plays, at only a quarter of the world’s gross domestic product. Because they are concerned about the US financial hegemony, Russia and China are diversifying from the dollar, buying gold. China has reduced its US reserves from $1.2 trillion to $1.05 trillion, a far cry from the peak at $4 trillion. Russia completed the Nord Stream gas pipeline to Europe and will take rubles instead of dollars. That is not all. Europe has unveiled the European Payment Initiative (EPI) to bypass the US payment oligopoly as a matter of sovereignty. The Biden administration will face a wider conundrum as it seeks to shift from fossil fuels to renewables to reach carbon neutrality. With Americans dependent on fossil fuels like petroleum, natural gas and coal, which accounts for almost 80 percent of their energy production, in the new green world, what happens to the dollar, exports and imports?

All this means investors no longer have confidence in placing most of their assets in dollars, particularly if those dollars are being inflated or affected by sanctions or climate. Also eroding their capital is the rounds and rounds of quantitative easing which flooded the market with newly minted Treasuries. As a result, international investors’ balance sheets have become top heavy with dollars, which are at risk because America’s twin deficits and red ink leaves it with rising debt, an inflation problem and a test of its credibility.

Déjà Vu

Between 1946 and 1971, the US dollar was backed by gold at the fixed rate of $35 an ounce. Then in 1971, the Nixon administration severed the gold link, devaluing the dollar because European countries demanded payment for their dollars in gold and the overseas claims on the dollar would have bankrupted the United States. While, the dollar is backed by the “full faith and credit” of the United States, instead of gold, the dollar is a fiat currency; a debt of the US government. Today, trillions of dollars are held by others because the US has become the world’s largest debtor. We believe America brings little creditability to the “full faith and credit” and the unprecedented stimulus has unleashed inflation. Tarnished, the dollar is undermined by America’s economic and financial mismanagement. It is overvalued without an anchor.

In practice this system allowed the United States to consume more than it produces and finances its everyday deficits with newly minted dollars. The question is now long can the world absorb these dollars? Once Britain was the wealthiest nation on earth and the British pound was the reserve currency for international payments. However, heavily in debt because of the Second World War, the pound was replaced by the dollar. Yet, before the dollar-led global order, history shows there was the Dutch guilder which followed florins and ducats. The dollar is not forever. No country can afford the deficits and debt that the United States is currently running.

The monetization of deficits is inflationary. The pick-up in inflation took the Fed by surprise. So likely, the next outbreak and return to the Seventies level of inflation. Covid-19 stimulus has lifted debt to record levels. No wonder money has become worthless. There is too much and holding cash will cost you. Money is free. Sovereign debt today earns nothing or less than nothing for the privilege of lending money to the government. Why should investors continue to lend money to the government, when a significant portion of that debt yields less than zero?

Above all, we have a looming financial crisis and despite a near miss collapse in 2008, the financial system like our health-care preparedness remains woefully exposed. Corporate debt stands at $11 trillion, about half the size of the US economy. In a legacy of lockdowns, fiscal deficits will rise as well as debt, and the currencies of those debtor nations, which fund their deficits by printing money will fall. Here, America is exceptional. Inflation is rapidly moving higher. Its democratic institutions are under siege. The Fed can’t afford higher rates with America’s massive debt load topping 115 percent of GDP. We believe the financial system is vulnerable to a major implosion as the United States digs itself into a deeper hole. Gold is an alternative to the dollar and the solution to those with too many dollars. The US has a serious problem with debt, deficits and the dollar. The cure, if there is a cure, will be painful. Gold is an asset that is both real, like real estate and liquid, like a currency. Today, it is a good thing to have.

Recommendations

Gold prices erased last year losses and within two months moved higher flirting with $1,900 an ounce because central banks were steady buyers, before slumping back on Jerome Powell’s sabre rattling of higher rates, in 2024. The stock market sold off 500 points, we believe gold’s pullback has created a new floor and we continue to believe gold’s next target is $2,200 an ounce. Gold demand remains strong with supplies limited. Fundamentally nothing has changed. Gold cannot be created by a click, except by very expensive mining processes, and that in only small quantities. Central Banks continue to add to the gold reserves as China, Serbia, Kazakhstan and Thailand added to its positions. The new Basel III regulations (Rule 96) will limit central bank involvement in the risky derivative gold paper metal markets, putting a floor under prices. To the central banks, gold is an alternative to the dollar.

The mining industry’s dilemma is that they are running out of reserves and under investment. Peak gold has arrived. Resource grade has also plummeted as open pits mature. In addition, the lack of discoveries hurt supply. Few of the miners have big mines in the works. Moreover, since to build the average mine it takes up to a decade or longer from “first pick, to discovery, to first pour”, the industry hit the supply wall. Also, the government propensity to keep plucking the golden goose has made investors cautious. For example, the Kyrgyz Republic’s nationalisation of Centerra or Papua New Guinea’s year long renegotiation of Barrick’s Porgera joint venture is part of an industry-wide trend of government scrapping agreements to gain bigger profits or additional ownership rights. The new Peruvian government has threatened to nationalize its mines. Unfortunately, the money grab is a fact of life and even in the state of Nevada, bureaucrats want to impose an “excise tax” on gold producers, holding many miners hostage, as they move the goal posts.

To replace depleting reserves, another option for the majors is to buy stakes in the junior explorers. Agnico Eagle for example has a portfolio of juniors, that serves as the “skunk works”. Rio Tinto recently spent $26 million for an 8 percent stake in Western Copper’s copper-gold Casino project in the Yukon. Evolution Mining of Australia widened its footprint in Canada by acquiring partially built Battle North Gold (formerly Rubicon). McEwen Mining has also taken stakes in juniors close to its mines.

The newest miners on the scene were Lundin Gold and Victoria Gold, yet their deposits were discovered more than a decade ago! Going forward there are not yet discoveries of size. Although there are exciting plays in BC and Newfoundland, exploration budgets are only now being increased as the gold miners report near record free cash flow. In fact, while budgets have increased, the miners have instead been paying out dividends and buying back shares as a return of capital to shareholders.

There are also new countries or frontiers and not all are hostile to mining and exploration. For example, Ecuador has welcomed Lundin Gold’s Fruta del Norte, which is the richest gold mine in the world. Solaris Resources has advanced its flagship copper-moly-gold project in southeastern Ecuador while Sol Gold’s Cascabel copper-gold porphyry keeps adding to reserves despite shareholder battles. Junior Aurania has not yet found its Lost Cities deposit from its huge property concessions, with investors eagerly awaiting drill results. Finally, Dundee Precious Metals bid for IVN Metals’ Loma Larga at a 63 percent premium reflects their desire to build another producer.

Agnico-Eagle Mines

Agnico is expected to report a stronger half following scheduled maintenance in the second quarter. The miner has $1.23 billion of available liquidity and will spend a whopping $163 million in exploration. Agnico replaced production, increased reserves by 12 percent to a record 24.1 million ounces. Near term growth will come from the LaRonde complex, Canadian Malartic and Amaruq in Nunavut. A $100 change in gold price translates to over $200 million in Agnico’s operation profit. We continue to view Agnico favourably with superior management and growth possibilities. Buy.

B2Gold Corp.

B2Gold is suing the Mali government in international arbitration because they have not been successful in securing the Menankoto renewal permit. The land is close to B2Gold’s Fekola flagship and would potentially add feed from the Anaconda zone at Menankoto. The Mali government owns 20 percent of Fekola so granting the permit makes sense.

B2 Gold will meet guidance this year from its three operating mines and share of Calibre in Nicaragua. The delay at joint venture Gramalote was disappointing but a fresh look, more drilling and new design could improve the outlook. B2Gold is spending $60 million on exploration this year so there could be surprises. We like the shares here.

Barrick Gold Corp.

Barrick has released more information from the Nevada Gold Mines joint venture with Newmont. Reserves represent almost half of Barrick’s and reserve additions are expected at Goldrush in line with the recent feasibility study. Exploration targets are many with almost 5 kilometers of potential ground around Turquoise Ridge where a third shaft is being sunk.

Operating cash flow was $800 million in the quarter and the framework agreement with PNG puts Porgera on track to resume operations possibly before yearend. Barrick will meet guidance with a stronger second half and boost from copper. At Loulo-Gounkoto in Mali, Barrick is developing the complex’s third underground mine. Barrick operates 5 of the world’s 10 largest gold mines and with a strategy of operational excellence, will become the go-to gold miner. Buy.

Centerra Gold Inc.

Centerra’s Kumtor mine in the Kyrgyz Republic filed for bankruptcy protection as the government threatened to takeover the mine in a blatant naturalization scheme. Centerra also filed for arbitration which forestalls the seizure by the government, but does not break the log jam. It appears that earlier attempts by the government to takeover Kumtor only “softened” Centerra and we expect an eventual forced sale, albeit on more favourable returns. A Kyrgyz court has fined Centerra more than $3 billion in an effort to “pile on” Centerra’s management. Nonetheless we expect a resolution will be favourable because the market expects the worst. Hold.

Kinross Gold Corp.

Kinross reported a fire at the Tasiast SAG mill which resulted in a halt in operations and the loss of almost 100,000 ounces resulting in Kinross lowering guidance for this year. However, the Tasiast expansion remains on track but the cost to restart is estimated at $50 million. Mining activities have resumed. Kinross will stockpile ore while the mill is down. Guidance was lowered to 2.1 million ounces from 2.4 million ounces (GEO) produced last year. Tasiast was to be Kinross’ growth mine and the fire sets back Tasiast’s timing. We prefer B2Gold here.

Lundin Gold Inc.

Lundin reported positive cash flow and processed a record 108,000 ounces in the second quarter. Production is estimated at 420,000 ounces at an AISC of $800 an ounce. Grade remains at 11.08 g/t or so and the company boosted exploration, in the quest to look for additional Fruta del Norte. Drilling at Barbasco should yield results in the next quarter. Fruta del Norte is one of the highest-grade operating gold mines in the world. We like the shares here.

John R. Ing

Please refer to the Legal Section of our website (maisonplacements.com) for our Research Disclosures for an explanation of our rating structure at https://maisonplacements.com/research-reports.

********