Gold And Silver Still The Leaders In 2017

Recall the Monty Python line "A minute passed quickly past"? 'Tis how the year 2017 feels to us. The geometrically-increasing pace of unrelated, and moreover, unimportant items beset upon us on a daily basis is blurring the very passage of time itself. Indeed, 99% of what now passes for "news" doesn't affect us a wit, nor is about which we even need know, let alone give a derrière du rat. Health & wealth, friends, family & self, (and yes the Yankees' score too), and we're good to go. Oh and yes, the price of gold.

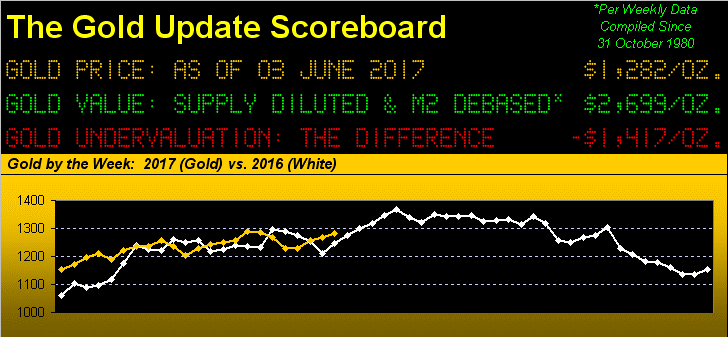

The above opening panel does show us Gold being ahead of where 'twas at this point a year ago, it nonetheless remaining wildly undervalued by currency debasement alone. But from the "Ya Gotta Start From Somewhere Dept.", gold and silver continue to be our leading markets year-to-date. So through the month of May, plus for June two days, below are how the BEGOS bunch stand by percentage performance. And therein note the boffing of "conventional wisdom" as gold is up 11% -- but Oil is down 11% -- so surely the stock market as measured by the S&P 500 must be down -- yet 'tis up 9%. Cue our favourite Vince Lombardi line "What da hell's goin' on out dere?!?!?!" and here are the standings:

Naturally, there's the age-old adage about the stock market climbing wall of worry, or has been the case in recent years, climbing a pall of no real earnings growth, (our "live" price/earnings ratio for the S&P at present up to 35.3x). Yet as permanently-correctionless as has become the S&P, a minority of non-complacent analysts are on the very edge of their seats. Here are some quick headline phrases we've noted these past few weeks:

■ high valuations make stocks dangerous (Shiller)

■ there's a strange disconnect in the market (Lee)

■ summer correction in the stock market (Gundlach)

■ dot com bubble deja vu (O'Rourke)

■ eerie similarity to 2007 before the bulls were slaughtered (Kass)

■ bad news says for stock market investors (Dalio)

■ buy dip party may be over (Shilling)

■ stock market is choosing to tune out any bad news (Pisani)

■ bracing for all hell to break lose on wall street (Singer)

'Course gold is on the flip side of all that, per currency debasement at half what it ought be, with the S&P per real earnings too high by doubly. Still, as we turn to gold's weekly bars from a year ago-to-date, we see price, as it did this past April, again poking its head above the purple-bounded 1240-1280 resistance zone in settling out the week yesterday (Friday) at 1282. And just as was the case a year ago, we'll continue to refer to that zone as "resistance" until a full week finds price above 1280, thus making it "support". The notion of that occurring sooner than later may be just 'round the bend given the price for the ensuing week to flip the parabolic trend to Long is just three points above here at 1285:

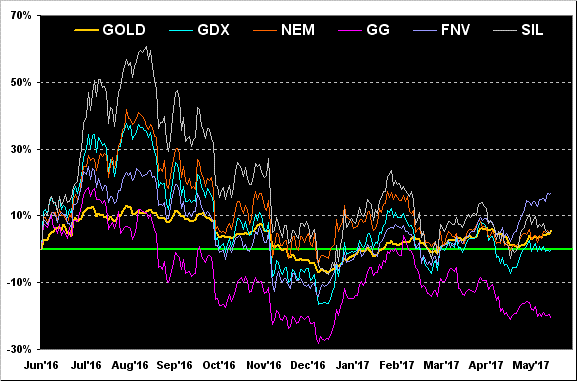

It essentially being month-end, 'tis time again to also bring up on a year-over-year basis the percentage tracks of gold and those in its equities fold. Now by the "leverage postulation" that the miners move at 3-to-1 the pace of gold itself, we find Franco-Nevada (FNV) being axiomatically correct, +17% from a year ago vs. gold +6%. Yet 'tis not the case for the balance of the bunch, as we see both Newmont Mining (NEM) and the popular exchange-traded fund of the silver miners (SIL) just +5%, the prominent exchange-traded fund of the gold miners (GDX) basically "unch", and Goldcorp (GG) still well off the boil given its managerial machinations, -21%. 'Course, looking back left across the chart suggests the leverage was getting a bit over-fried last summer:

Meanwhile what's being underdone of late is the Economic Barometer, with just eight trading days left until the Federal Open Market Committee's voting to raise its bank's Funds rate on 14 June. To be sure, this past week brought us reports of increases in Personal Income and Spending, the Chicago Purchasing Manager Index and the Institute for Supply Management Index (manufacturing). But then came the odd disparity between the private sector reporting by ADP of job creation in May of 253,000, but by the U.S. Department of Labor Statistics, payroll creation of just 138,000.

"You think that's a Labor Dept. jab at the President, mmb?"

I ought think such thought has occurred to some out there, Squire. But these two monthly measures have had wide differences in the past, this being the eighth-largest (with the ADP figure bigger and both numbers positive) since 2008. Either way, throw in a reduction in Consumer Confidence, a decline in Pending Home Sales, plus an increase in the StateSide trade deficit and we've got a Baro losin' its dinero:

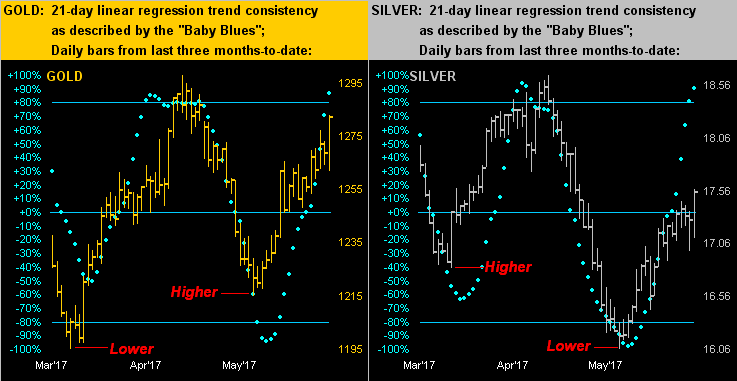

But rather than waning, again we've gold gaining as shown here in this two-panel display of daily bars from three months ago-to-date. Note with respect to the two labeled major troughs on both panels that for gold on the left the second trough was higher than the first, but not so for silver on the right. Regardless, for both metals, their "Baby Blues" have risen above their respective +80% axes, exemplary of the 21-day linear regression uptrends being firmly consistent:

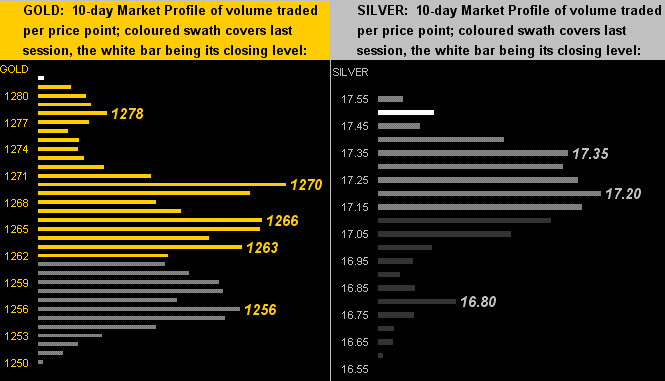

Upside consistency in turn brings us to life being good at the top of the 10-day Market Profiles as we next have here for Gold (left) and Sister Silver (right), their underlying trading support areas as labeled:

And thus with May in the books we arrive at our layer-defined Gold Structure as shown by the month since Gold's All-Time High. Note that the wee rightmost bar accounts for the first two trading days thus far in June: that bar is green, (which for you WestPalmBeachers down there means "up"). Should it so be the case by month's end, gold will have risen (net) in five of the past six months, (March being the only mild loser at -3 points). The last time gold posted a series of such "five-of-six" monthly increases was in a seven-of-eight run from September 2010 through April 2011, all of course en route to gold then making its All-Time High come September of that year. Oh to frustrate our little red friend!

So with gold and silver still the leaders in 2017 we'll depart for this week with these few quick hits and a logistical note.

■ Last year's Chicago Cubs may won have their first World Series after a 108-year drought, but this year there's little joy in Illinois as both Moody's and Standard & Poor's opened the month of June by cutting the State's bonds to an all-time American low of but one notch above "junk". One can only wonder what ole Honest Abe would make of today's political donnybrook. From the Land of Lincoln to the Land of Sinkin'.

■ Yep, 'tis but a round number, but one that gets noticed, the shares of Amazon (AMZN) this past week having crossed the $1,000 level. 'Tis only because we count in "base 10", for rather would the world instead run on "base 8", that price instead comes in already well beyond $1,000 at $1,750, likely to garner less notice. Regardless, here's the more important number: $5.43 -- that is the company's trailing 12-months earnings per share -- which at the present share price of $1,007 gives us a "live" p/e ratio of 185x. Remember that above stack of stock market headline phrases?

■ Finally, a great and good friend chimed in this past week over the word "galamsey". 'Tis a mouthful to say and a messy handful with which to deal. You might check it out, and again, feel fortunate to have your health & wealth, friends, family & self. And some gold!"

Logistical Note: Those of you valued readers who live to punctually press your browser's "refresh" button for The Gold Update at precisely 11:00 Pacific Time each Saturday, do not despair when so doing in a week's time if the upcoming 10 June edition doesn't readily appear. But have no fear, as we may well be "in motion" at that time in top gear. So don't shed a tear, let alone your refresh button shear. We expect the missive to be up on the web once a "wifi" is near!

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.