Gold Gains Pace; Shall It Fail At The Same Place?"

Gold just posted its best net weekly percentage gain (+2.6%) since that ending 13 April 2017, (and its best weekly points gain [+35] since that ending 29 April 2016).

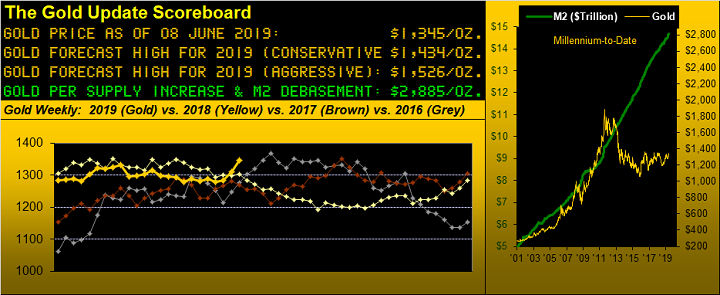

'Course as we oft quip: "Change is an Illusion whereas Price is the Truth." And in looking at the above Gold Scoreboard, 'tis somewhat encouraging to see that price to this point of the year is above where respectively 'twas for the past three years, (in fact the case for the past five years). Which for you WestPalmBeachers down there means price today has not been this high on this calendar date since 2013, in having settled out the week yesterday (Friday) at 1345.

So: is this "IT"? 'Tis the question we've on occasion asked in recent years upon Gold recording similar weekly leaps right 'round this same price area. And as we've seen time and again for nearly three years upon price having surged up into the 1340s-1360s range, in then have raced the range-bounders with enough selling force such that Gold turns tail such as to fail in re-taking Base Camp 1377. And until that infamous level is overtaken -- indeed until price breaks above all of these many past peaks for a settle at least up into the 1380s, "IT" ain't gonna be "IT" one bit. Or to quote Clint Eastwood as Josey Wales from back in '76: "That's just the way it is."

"But mmb: what do YOU think's gonna happen this time?"

Squire, 'tis the fair and poignant question. To be sure we've the widening fundamental realization for the folks at the Federal Open Market Committee to rescind at least one of their FedFunds rate raises. (As a brief refresher, after having held their Bank's rate at 0.25% from 2008, the FOMC in late 2015 began a series of nine raises culminating this past December at 2.50%).

Indeed as was universally disseminated this past Monday, St. Louis FedHead James "Now Not As Bullish" Bullard suggested a rate cut may be "warranted soon". Add to that yesterday's report of May's Stateside payroll creation being but a bleary 75,000 (vs. consensus for 180,000 on the heels of April's 224,000) and Gold got some added upside push as did the stock market, which in its modern-day paradigm views practically all news -- good or bad -- as positive (unsupportive earnings be damned), the exception of course being TrumpTariffTalk.

In fact, the FinMedia of today is sufficiently Trump-focused as he being the sole mover of markets. As an example, the News Corp/Dow Jones product MarketWatch, (which a very close trading colleague of ours back in San Francisco now deems as "useless"), ran a piece a week back inferring that the damage to the stock market through the month of May was comprehensively due to a 05 May TrumpTariffTweet: we combed through the entire article and nary once was the "E-word" mentioned. 'Course "E"arnings never matter until given blame in post-crash hindsight. Nope: these days sans Trump, there'd be no other rationale for market movement.

As for technical realization let's turn to Gold's weekly bars, the parabolic trend only having just flipped from Short to Long. And to draw from last week's missive: "...the average maximum upside...for [the] prior 16 Long trends is +7.5%. Were that to precisely pan out on this new run, we'd see price ascend to 1408...". But as noted with respect to change being an illusion, price being the truth is again in this area from which it tends to keel over. After all, Gold today is but a "barbarous relic", lacking the modern-day magnetism of bits**t and the frivolously-favoured FANG gang. Still, this present picture appears positive.

So in answer to Squire, we are somewhat reversal wary until Gold proves itself in breaking above what has been this ongoing upside barrier beneath Base Camp 1377. Short-term, (as oft is the case upon swift price moves), there are a rash of trading concerns, barring this bit turning into "IT":

■ Gold's daily trading volume yesterday was the weakest of the past six sessions;

■ Gold's MoneyFlow (as defined at the website per the 0-100 scale) is "95", whereas a level of "80" is considered exhaustive;

■ Gold's Market Value (also per the website) is +77 points above the smooth valuation line; and

■ Gold's deviation from the website's Market Magnet is an extreme +27 points.

To be sure, the mo-mo trader sees all such readings as positive; but again, this 1340s-1360s zone is from where Gold has become stuck time and again. And it shan't be "different this time" until 'tis and the move toward our conservative forecast high for this year of 1434 appears truly underway. Either price achieves Base Camp 1377, or "fergit about 'IT'!" Or more to the point: were one to conservatively wait for higher ground, we'd then see strong potential for still further, material upside.

As for the Fed turning toward rate reduction, we're not that surprised given A) "they're always behind the curve", and moreover B) without looking it all precisely up, it takes some nine months to a year of decline in the Economic Barometer for the Fed to actually realize growth is slowing if not outright regressing:

More broadly in reviewing Gold's daily closes since the highest back on 22 August 2011, one can starkly see price's having again arrived in that zone from which hesitation hits and we fall back to bits, (barring this being "IT"):

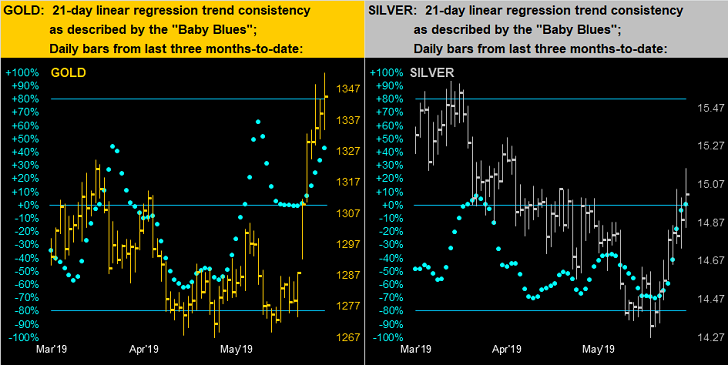

As for the precious metals' daily bars from three months ago-to-date, here they are below left for Gold and below right for Silver. And what's most evident is the comparatively lackluster look of the white metal versus the yellow metal and thus the ever-extreme reading for the past 16 months of the Gold/Silver ratio almost universally being above 80x. Gold today at 1345 clearly has surpassed its 25 March high of 1324; Silver now at 15.01 however hasn't reached near its 21 March high of 15.65. But at least for both metals, their respective baby blue dots of linear regression trend consistency are on the rise:

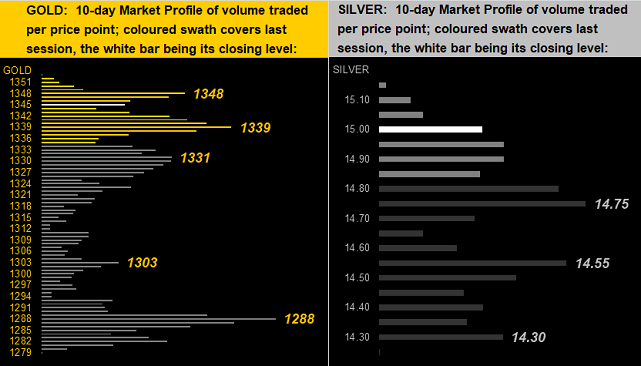

In turning to the 10-day Market Profiles, given the recent up-runs for both Gold (left) and Silver (right), we find their respective present prices near the top of each stack, their most voluminous trading price points as labeled:

The gauntlet thus (and hardly for the first time) has been thrown down for Gold to prove its worthiness (a vast understatement given that by U.S. currency debasement alone price today "ought be" 2885). Price's pursuance is plain: maintain the pace to bust up through this otherwise retreatable area of the 1340s-1360s toward retaking Base Camp 1377; else fail yet again 'round this very same place. Indeed from here in Monaco, one might refer to the following, seeming illogicity as a "canard": this is one of those exceptional times which suggests a higher risk of buying Gold now than from further up the road, for reversal from here breeds buyers' fear. Instead upon clearing 1377, Gold ought really look good to ascend!

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.