Gold Is Getting Frisky

share

share

share

share

share

share

share

share

share

share

We recently discussed the astonishing surge in net long positions in the US dollar, and the lopsided reading of associated sentiment surveys, which have broken all previous records (See “How Much Further Will the Dollar Rally?” for details). Here is a brief update in light of last week’s quite noteworthy commitments of traders report, which has seen an enormous additional increase in speculative net long positioning.

We recently discussed the astonishing surge in net long positions in the US dollar, and the lopsided reading of associated sentiment surveys, which have broken all previous records (See “How Much Further Will the Dollar Rally?” for details). Here is a brief update in light of last week’s quite noteworthy commitments of traders report, which has seen an enormous additional increase in speculative net long positioning.

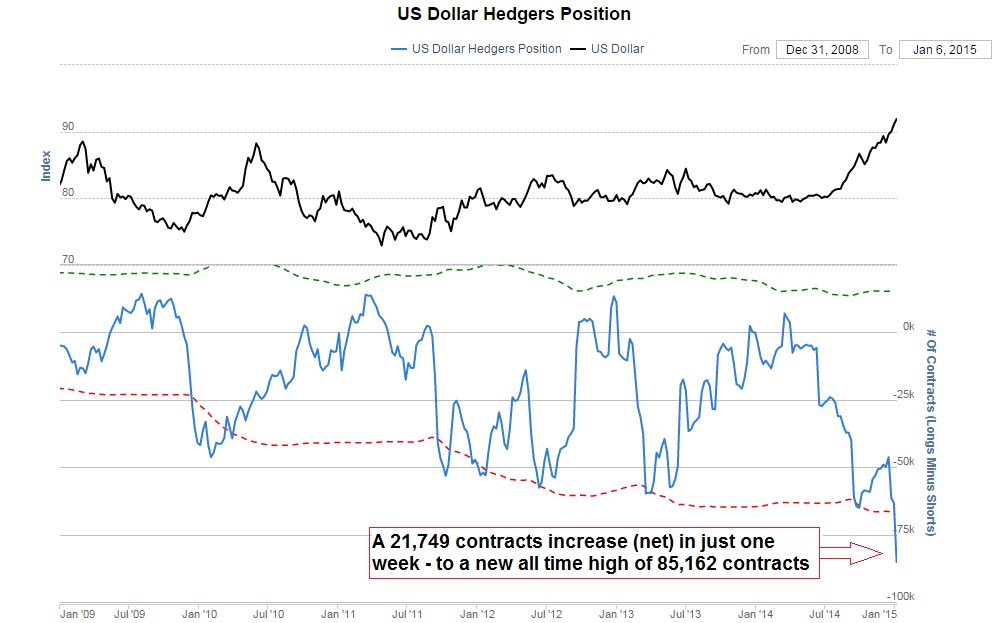

The chart below shows the net hedger position, which is the inverse of the net speculative position. Last week the net speculative long position in DXY futures rose by 21,749 contracts, which to our knowledge is one of the largest one-week surges in history, possibly even the largest.

Do Hot Flashes Have You Feeling Irritable?

Prescreen for a Menopause Research Study

Public sentiment (Optix, an amalgamation of all important surveys) continues to be stuck at 89% bulls. However, the short term oriented DSI (daily sentiment index) compiled by tradefutures.com recently clocked in at a reading of 98% bulls, which not surprisingly is an all-time high as well and suspiciously close to the never before attained 100% barrier.

The net position of hedgers in DXY futures, via sentimentrader. The new record high 85,162 contracts net short position of commercial hedgers mirrors the equally large speculative net long position. Last week’s surge of 21,749 contracts was huge for a single week – click to enlarge.

We should probably congratulate the 2% bears left in the DSI survey for their intestinal fortitude in light of what has been a quite relentless rally. Such extremes in positioning and survey data must of course be discounted by the fact that they are aligned with the trend. Both follow prices after all. They also don’t necessarily mean that a bull market is over. However, experience shows that DSI readings in the high 90s at the very least tend to coincide with short term peaks that are often followed by quite sizable corrections.

At times they also coincide with long term tops, but usually one sees a succession of extreme readings at short to medium term peaks before the final, long term peak occurs (the opposite holds for single digit readings, such as those recently recorded in gold).

From a fundamental perspective, the rationalization for the dollar’s rally is that the Federal Reserve is about to hike rates just as other major central banks have increased or are about to increase the pace of their monetary pumping. This expectation in turn is based on stronger macro-economic data reported by the US compared to other major currency areas. However, all of this has been known for quite some time, so at some point the market will presumably have discounted all that is already known. This leaves the possibility of disappointment if reasons to doubt these expectations should surface (note though that trend changes often occur before any “reasons” are discernible).

Lastly, large lop-sided speculator positioning in futures markets as such doesn’t end a trend. Especially in currency futures one must be careful with such conclusions, as the futures markets represent only a small portion of the total market. However, it is a statistically significant portion with respect to market sentiment. What it does mean, is that any counter-trend move is likely to be magnified.

Conclusion:

Right now is probably not the best time to buy the US dollar, in spite of the “obvious” and widely accepted fundamental rationalizations for doing so.

********

Courtesy of http://www.acting-man.com

share

share

share

share

share

More from Gold-Eagle