Gold: Identity Theft

share

share

share

share

share

share

share

share

share

share

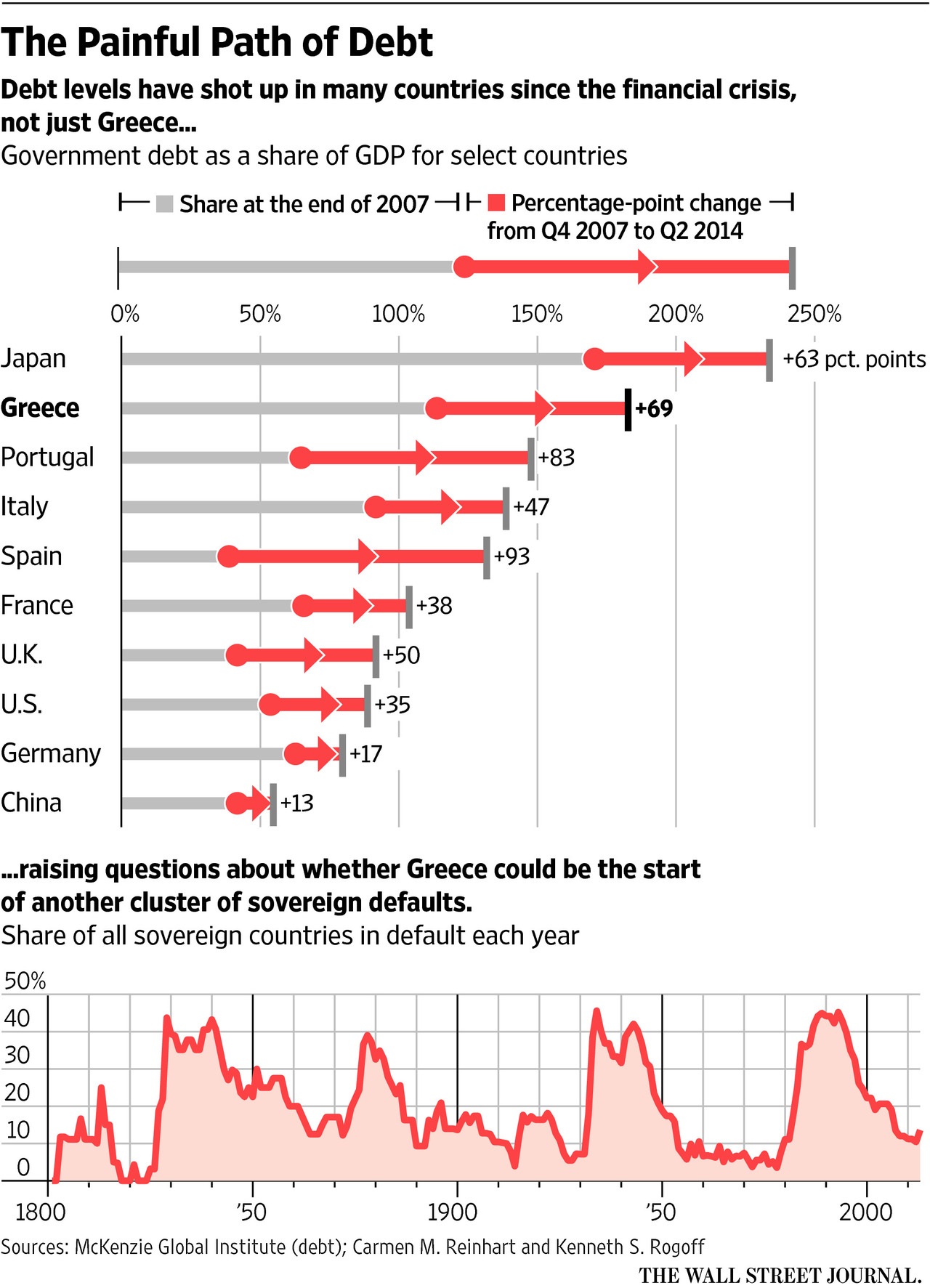

Identity problems? Rachel Dolezal wants to be black, Bruce Jenner a woman, or how about Donald Trump for President. Identity problems? No, it is identity theft comparable to the “happy times are here again” mania, fueled by cheap debt and a borrowing binge which has led to overvaluation and risk. In much of the globe, we have negative interest rates pushing investors into US dollar denominated assets like stocks, real estate and for a very long time, US bonds. The US dollar, once viewed as a sick currency less than a decade ago, is now viewed as a safe-haven following the Euro debacle. But the default risk was not just a Greek story. Overlooked is that Ukraine recently declared a “credit event”, raising the risk of default. To date there are more than ten countries that are vulnerable. Argentina is already in technical default and Puerto Rico filed this month owing $72 billion. The debt tide has turned.

It was wonderful while it lasted. For much of the past two decades gold was on a tear. Today, with gold trading at five year lows, we are told the good times are over. Bullion and gold shares have pulled back, breaking support levels. However, gold in euros was up 17 percent since yearend, an effective hedge against the euro mess. Nonetheless, what went wrong? The short answer is that the US dollar has replaced gold as the preeminent store of value. Dollars are highly liquid and America at least on a relative basis is on the mend after trillions went to repair its economy. The pool of dollars seem bottomless. Without that fill-up, America would be another Greek tragedy. However, as the ancient Chinese proverb warns: “no banquet in the world goes on forever”.

In finding a refuge in dollars, we believe the market has replaced gold as a life preserver, but tied to an anchor. America has a serious problem with the overvalued dollar hurting the competitiveness of its exporters. Consumption is only buoyed by the trillions pumped into the market printed with a click of the mouse. And, that bastion of capitalism, the US market is considered corrupt, according to the SEC Commissioner, Luis Aguillar, calling out its players for rigging markets. And significantly, America itself is in a bubble going deeper and deeper into debt.

America, the Bubble

Meantime commodities have pulled back, due more to supply coming on the market attracted by higher prices. China has slowed from the frothy double digit growth days that drove a global commodities boom. And the spectacular stock market implosion erased 30 percent of gains after a 150 percent move, pales in comparison to the Nasdaq dot.com bust, or the TSX Venture monumental collapse. However China’s industrialisation is irreversible as is its insatiable appetite for both resources and investment. Beijing will continue to boost consumption as well as infrastructure spending against a backdrop of liberalising financial controls whilst weaning the economy off its reliance on credit and state sponsored investments.

But, while China builds factories, America has gone on a credit binge. Investment there has sagged while cheap money leveraged the stock market, real estate and currencies spurred by ultra-low rates. History shows that the toxic combination of cheap credit and debt has been tried before and is not sustainable – ask the Greeks.

But, while China builds factories, America has gone on a credit binge. Investment there has sagged while cheap money leveraged the stock market, real estate and currencies spurred by ultra-low rates. History shows that the toxic combination of cheap credit and debt has been tried before and is not sustainable – ask the Greeks.

The bond market was the first to crack as yields rose catching the market wrong footed. Looming in the background is the threat of a stronger and long lasting El Nino which threatens the inflation outlook. This “regular” black swan is expected to build-up in the second half of the year and is already linked to droughts in Southeast Asia and Australia as well as wet and cool weather in the Southern US. In 1997, El Nino hit a range of commodity markets causing billions of dollars in damage, food shortages and a spike in inflation. Today there was a price surge of olive oil from Italy after last year’s harvest infected at least one million trees. Olive oil prices after hitting lows in 2012, are at nine year highs and the jump is reminiscent of those missing anchovies which sparked the last Great Inflation in the Seventies.

Of course, all this comes as Mr. Obama, in attempting to revive his legacy and second term, once frustrated by stalled climate change legislation on Capitol Hill, needed the Republicans to pass ObamaTrade after being rejected by his own party. His ObamaCare law barely survived a Supreme Court challenge. In the Middle East for which Obama won the Nobel prize, America is somewhat worse off than when he first arrived on the scene. The Arab Spring has brought civil wars to Syria, Iraq and Libya and as America retreats, the vacuum is quickly filled by its enemies. And ironically amid this rubble, that former axis of evil, Iran, is now a keystone of Obama’s Middle East strategy against the objections of longstanding allies, Saudi Arabia and Israel. To no surprise, this lame duck president has lost confidence of both allies and enemies. And while in office, the US public finances are in shambles and getting worse.

For the last seven years there have been mainstream predictions that it was only a matter of time before interest rates moved up to historic norms which would of course drag down the stock market. Yet the already elevated stock market posts new daily highs as the day of reckoning and return to normalcy gets kicked down the road. Fed Chairwomen Yellen regularly threatens to raise interest rates but the never ending series of quantitative easing, reliance on credit and attendant mixed readings on the economy makes increasing rates dubious and an excuse to kick that can down the road. To be sure, the long term rate norm of four percent is pale in comparison to the hand wringing over the Fed’s intentions to raise interest rates by a miniscule 0.25 basis points.

But there’s more. While Mr. Obama flits like a butterfly from crisis to crisis, super low rates and quantitative easing have distorted markets, benefiting borrowers at the expense of savers, especially seniors. To be sure, risk has been altered. The main point however is that this money growth has not filtered down to Main Street. Any inflationary effects of cheap credit have until now been offset by labour participation at the lowest since 1978, yet wage inflation has picked up. Long term investments or job creation is an illusion of this false prosperity. It is worth remembering that America’s economy is simply a casino and the Fed is the croupier.

If the economy is to grow, corporate revenues must rise and investment must happen. However we believe it won’t happen because of concerns over the integrity of money and fading confidence in the Fed’s ability to manage the economy, important in an election year. The US has lived beyond its means for over half a century, spending more than it produces, financed by others and using unconventional monetary policies like rounds of quantitative easing to create money without limit, in order to pay bills and deficits. These funds have sloshed into financial markets, driving down currencies leading to a lack of confidence in the value of money and ability to unwind the Fed’s bloated balance sheet. Quantitative easing is founded upon a repression of a return to savers.

2015 is the new 2007

So, America finds itself in a bubble. As it goes deeper and deeper into debt, Wall Street, mainstream media and investors ignore the problem. Compare the balance sheet of the Fed or any household in the US twenty years ago. In 1980, the US Government’s net external debt was only one trillion. Today, it is a whopping $18 trillion and growing at an annual rate of $500 billion. In fact, the United States’ debt level remains frozen at $18 trillion because the statutory legal limit was reached more than three months ago and Congress refuses to raise the debt ceiling. The average rollover period is becoming shorter and shorter. Meanwhile despite a near-death experience in 2008, consumers’ debt continues to increase and remains more than 100 percent of disposal income. So awash in red ink, Americans lurch from bankruptcy levels that rival Greece’s.

To be sure, this great credit binge has tested the patience of its creditors. Rather than sit with some $1 trillion of $12.5 trillion pool of US Treasuries, China has been dumping dollar securities and purchasing other assets than dollars. Japan and Saudi Arabia too are among the biggest holders of US Treasuries and are also diversifying their portfolios. To be sure America’s indebtedness and asset price bubbles should be a central election issue in the upcoming $3 billion election, but every candidate avoids it like the plague, including Mr. Trump.

Another Day, Another Missed Deadline

Markets hate uncertainty. In the wake of Greece’s referendum, confusion reigned over the potential contagion that would drag in other members like Spain or Portugal. So far we only had a default, not the Grexit. Greece needed a third bailout of some $120 billion in emergency loans on top of the $300 billion it owes. To date there is an untested firewall which we believe is a defacto “redline”. Unfortunately the ECB has already used QE1 and have left little room in their arsenal. At best, we can assume yet then another round of quantitative easing– blurring the world’s second largest economic bloc’s redline.

For much of this year, investors have watched the escalating crisis in Greece with a degree of complacency. Where this is going is that history shows us that when investors distrust debt and currencies, hyperinflation ensues. Such a situation is occurring in Greece today where interest rates are already in the double digits and people bought Mercedes Benzes to hold value. Venezuela is another country where hyperinflation exists.

Yet the latest debacle carries a deeper resonance – debt must be paid. It might appear that the investors are impervious to the contagion from the Greek turmoil, but we believe that Greece will prove to be a catalyst that sparks a sense of urgency. One reason is that risk was thrown into the equation and investors will focus less on Greece and more on America’s spiralling problems. Chairwoman Yellen remains on the high wire reluctant to raise rates, hoping to postpone the day of reckoning. Yet borrowing costs have increased to their highest levels in months. If so, investors who profited from low interest rates run the risk of losses as interest rates edge higher.

Central banks, our supposed guardians of financial stability have hijacked our sovereign debt markets, leaving a trail of illiquidity and crushed bond markets in their wake. Equity bubbles have been allowed to inflate on the back of a series of quantitative easing, leaving only two outcomes for rescuing our highly leveraged financial system – writedowns and/or the current policy de jour, inflating away our debt. And, underpinning the dollar is a belief of higher rates as the Fed reduces its bloated balance sheet and of course, the exit is supposed to be painless. We believe in these uncertain times, that belief will be tested. One can detect the decline of confidence in every part of the world. The risk of a systemic event, larger than the financial crises of 2008, and the on-and-off again Euro-debacle only reinforces our leaders penchant to duck responsibility leaving gold as the only protector against our leaders whims. The consequences are not priced in equities, bonds, the dollar or gold.

Back to the Past

The Fed’s balance sheet has grown much faster than its capital and now makes up 25 percent of America’s GDP. Of note is that there were only two other times when the Fed’s balance sheet was so high - the Great Depression and World War II. In 1929 worried about a bubble in the stock market, the Fed raised rates despite signs that the underlying economy was “not too hot, not too cold”. The Fed’s balance sheet grew to 25 percent of GDP as it monetized assets to stimulate the economy. However, efforts to reduce the balance sheet exacerbated the crash which wiped out savings. Today, of course is not 1929. While the lessons of the Dirty Thirties are taught daily in our business schools, it took that student of Depression history, Chairman Bernanke, to kick-start and ironically duplicate the Fed’s current growth in balance sheet levels to a whopping 25 percent. Since 2007, the Federal Reserve has created more than $4 trillion out of thin air to bailout Wall Street, pay bills and for consumption. Over the same period, America’s enormous public debt jumped over $18 trillion.

We now find ourselves in a place vaguely reminiscent of the past. We certainly know the benefits of building up the Fed’s balance sheet. The real question is how to chose an exit elegantly. Like then, we are afraid unwinding this balance sheet will not prove to be painless. Investors, ignorant of the past, seem to be too complacent believing that interest rates will somehow stay low forever. What to do?

The US used a gold standard from its inception in 1789 until 1971, a period of 182 years.More telling was the Fed’s confiscation of everyone’s gold and gold coins in May 1933, paying them a paltry $20 an ounce removing a major competitor to the dollar. Gold then was a discipline ensuring governments did not print money unless backed by gold. That confiscation allowed the Fed to print more money in the Thirties to finance the spending that helped pull the US out of the Great Depression. In monetizing this debt, the unwinding had disastrous implications when rates increased in 1937 exacerbating the longest and most severe depression ever. In 1971, with the world flooded with too many dollars, the Fed removed the link to gold to stop a run on its gold reserves. Instead, within a modern era of floating exchange rates, the dollar became a fiat currency allowing America to run up huge deficits again and fund a series of wars. And, despite the move to reduce gold’s role, it has been onward and upward since 1971, reaching a record high of $1,940 in 2011. Until now.

Today, with the Fed’s balance sheet again at 25 percent of GDP, this grand experiment of fiat money creation with debt monetization and currency manipulation has been allowed to prosper. In doing so, the Fed’s policies have benefited government, at the expense of the private sector. And, the promises of repayment are underwritten by the ratcheting up in America’s debt in Greek-like fashion. We are afraid that the ending remains the same. However, unlike the Thirties, gold is not frozen in value and exists in a free market. For that reason, physical gold has recently been accumulated and even today is five times its low. It is not so different this time. The age-old discipline of supply and demand leaves the dollar with only one way to go. Gold will continue to rise and will have the same value whether owned by central banks or individual investors. Deja vu.

An “Old School” Solution

The lessons of the past are that paper currency systems have their limits. In 2008, we learned Wall Street’s alchemy was found to be worthless as it discovered that subprime mortgages can’t create wealth out of thin air. And in the past seven years we learnt that central banks can create money out of thin air utilizing the equity markets as a policy tool. Japan was the latest country to use monetary expansion aka money printing is a cornerstone of Abenomics. Although, money printing has failed to create inflation it debases or weakens their currencies causing a defacto currency war which decimates the central banks’ currency holdings in purchasing power terms. The dollar’s value is too subjective. To protect themselves, they are seeking alternatives. This is where the gold standard as a yardstick of value has its advantages.

Once considered a relic as a medium of exchange, gold is not so “old school” today. Gold in euros was up 10 percent during the Greek debacle. The problem is that there is a lack of confidence in currencies. No one trusts money due to the price of money and America’s financial protectionism. However, in the world of social media, we learn that value is in the eye of the beholder. No one is certain what a dollar can buy or what it is worth, so today, a computer generated Bitcoin possesses a growing audience.

Herein lies the appeal of the “old school” gold standard which frankly is the least ugly system in this era of paper currencies. To be sure, we can no longer trust the central banks to tell us what money is worth. Similarly there is no desire to repeat Britain’s mistake back in the 1920s when the US dollar replaced the sterling pound. The dollar has since seen a loss of almost 94 percent of its purchasing power. What to do? We believe that the Fed should convert some of their bloated assets into gold and return to gold backed dollars. It would return faith to the dollar and a major realignment between gold and the dollar. Debt could be converted with gold used as collateral. Gold would be a good thing to have.

Though the rigour of the gold standard is not a cure-all, unlike the dollar, gold has been time tested for thousands of years. For that reason, we believe that China’s drive to make the renminbi a global reserve currency creates opportunities for gold. China has broken its six year silence by disclosing it has increased its reserve holdings by 60 percent to 1,658 tonnes, in a diversification move away from the US dollar. China holds some $1 trillion of America’s debt, and its central banker recently declared the need for a new reserve currency. We continue to believe gold will provide a better return and protection than the current fad, cheap treasury bills of the governments that run the printing presses.

Recommendations; Obituaries Are Premature

Despite 4,000 years of history as a safe haven, gold lately has collapsed due in part to the resurgence of the US dollar, aided by a handful of derivative banks who previously were found guilty of manipulating everything from rate rigging interest rates to currencies to widely used benchmarks. We believe this massive manipulation is coming to an end as those participants have been forced to come out into the open following the replacement of many executives of some of those big banks. Nonetheless gold fundamentals remain intact. In fact, gold in euros was up 10 percent providing a safehaven during the Greek debacle. In addition, China continues to be a major factor, pushing for the internationalisation of the renminbi so it won’t need so many dollars. Russia too remains a big buyer of gold joining some nineteen central banks which hoarded gold last year. In the meantime, the supply of gold has been decreasing as the current gold price approximates the cost of production. Fewer new deposits will be coming on stream over the next few years due to the low gold price and constrained US production is at decade old lows.

On the technical side, gold is extremely oversold. Still, gold is an emotional metal that is sometimes driven by “rank” speculation rather than fundamentals. Gold’s pullback and failure to hold $1140 an ounce was a surprise. However the strength in the US greenback was more of a surprise. Technically, it appears the $1,080 level will find meaningful support. Most shares, are trading at the low end of their Bollinger Bands.

The dollar is the world’s currency but the global players have a vote. Because the US consumes much more than it produces and owes much more abroad, the world is awash in dollars. Someday, and soon the holders of those dollars might wake up and sell, After all, who could blame them?

The largest holders of gold remains the public and their holdings are sticky, particularly when economic implosions such as Greece surfaces. The second largest holders of gold are the central banks with some 33,000 tonnes held in their vaults. Central banks have been adding to their hoard and some have taken to repatriating their gold because of concerns over the security of their holdings. Austria recently repatriated 110 tonnes following Germany’s 120 tonnes and 122 tonnes returned to the Netherlands. In the meantime, gold equities have transitioned from “high growth” stocks to a “value” story. Gold stocks have fallen with gold just as global uncertainty and volatility have picked up. Consequently, valuations are favourable, in particular for the gold miners’ in-situ gold reserves which are indirect options on gold. Gold companies hold the largest “unallocated” reserves in the world at some 21,000 tonnes. We believe that the value of those reserves will become increasingly valuable, particularly in a world with too much paper gold and not enough physical gold.

Consequently we favour the liquid senior producers with abundant proven and probable reserves, together with improved balance sheets enabling them to exploit the development of those reserves. Cost control, particularly corporate costs has become a watchword and the industry has pretty well rung out excess costs of producing gold such that their AISC approximates the current price. The focus on cash flows and all-in costs have created a barbell approach among the gold producers with the growth seniors on one end and the mature, higher cost producers on the other. With miners depleting their asset bases, the replacement of those reserves are important in the long run.

For that reason, we like Barrick, and Agnico-Eagle who have enviable portfolios of producing mines and abundant in-situ reserves. Among the midcaps we like Eldorado and B2Gold. Of particular interest are the junior developers who have great brownfield projects, but financing these projects are onerous. While the cost of building these projects could be financed largely with debt, unfortunately many of these junior producers cannot come up with the equity in order to finance their projects. However, within an environment of depleting reserves, we believe those projects will become attractive and be among the first projects to be exploited. These juniors thus have 10 bag potential as well as the fodder for continued M&A activity. Notable is the formation of Oban Mining Corporation, which is a roll up of four producers under the umbrella of Dundee and Osisko. Oban has a stellar balance sheet and a multitude of development projects. To be sure, this new kid on the block should be followed.

Alamos Gold Inc.

Alamos Gold has successfully completed its merger with AuRico Gold. The rationale for the Canadian based merger was to combine the stronger balance sheet of Alamos with AuRico’ s debt laden balance sheet as a bridge until the Young Davidson underground was up and running. Alamos’ Mulatos in Mexico has a short life but the combined entity will have an all-in cost at more than $1,200 an ounce. Importantly the Young Davidson build-out is dependent upon the successful completion of the underground operation. Further capex will be needed and thus Alamos’ interest in Turkey becomes increasingly important in the interim. However Kirazli and Agi Dagi open pit projects in our opinion are more “development situations”. Lynn Lake too is an advanced development situation needing a higher gold price. Alamos is most likely to go sideways. Until the benefits of the Young Davidson build-out becomes apparent. With net cash of some $90 million, Alamos is not so attractive here.

B2Gold Corp

B2Gold is one of our favourite midcap producer with 5 million of proven and probable reserves. The company recently completed a $350 million revolving credit facility for Fekola open pit mine in Mali, ensuring the financing of that project. B2Gold has four operating mines and Fekola will be the fifth. B2Gold produced 384,000 last year and will produce 515,000 ounces this year with a contribution from newly constructed open pit Otjikoto in Namibia which has improved in every quarter. Mill expansion is scheduled for the second half of this year. B2Gold remains attractively priced here for its low cost production growth profile and its ability to execute with no surprises, together with a strong balance sheet and enviable development pipeline.

Barrick Gold Corporation

The world’s largest gold producer‘s shares have outperformed its peers due to the growing acceptance of John Thornton’s “Back to the Future” strategy. In addition, his dual presidency and management structure is being seen as not only a cost saving but a strategic move allowing the decentralized group to make quicker decisions. Also, head office staff was slashed by 50 percent and Barrick’s divestment of non core assets continues such that they will have no problems meeting the $3 billion target to bring down debt. And not surprisingly, Barrick found healthy interest in its asset sales, a reflection of the quality of Barrick’s assets. Most importantly, Barrick’s five core assets in Nevada and the Andes are considered flagship assets generating over 62 percent of its production base at an AISC of less than $800 an ounce. Reserve grade is also more than double of its peers. We particularly like Barrick’s huge in-situ reserves which are among the largest in the world even with the current divestments. Finally, Barrick’s extensive gold asset portfolio contains quality assets that could be monetized or used as M&A chips. We like the shares here.

Detour Gold Corp.

Detour has regained investor confidence as both mining and milling rates improve. Detour is developing the 100 percent owned Detour Lake Gold Project in northeastern Ontario and will produce almost 500,000 ounces making it the largest gold producer in Canada. With over a twenty year mine life and 15 million ounces of reserves, Detour has a long mine life despite only twenty percent of its property explored giving it blue sky potential. Guidance to date suggests an improved mining rate and higher grade material is expected to be mined in the second half of this year. Detour is reviving the mine plan that includes Block A, which could further exploit the low grade deposit. Cash and short term investments are at $116 million with $135 million facility. We like the shares here.

Eldorado Gold Corp

Global player Eldorado shares has been hurt by concerns over Greece as it seeks permits for greenfield Skouries in the Halkidi Mining District. Eldorado spent $2.4 billion to acquire European Goldfields and has spent over $1 billion so far and plans to spend another billion. Currently, Eldorado has six operating mines producing over 700,000 ounces at an AISC under $800 an ounce. But the Greek debacle has hurt its performance. Nonetheless, Eldorado’s main assets are in Turkey with flagship Kisladag and Efemcukuru producing almost 350,000 ounces this year. The Turkish mines are low cost with long lives. Eldorado’s other strength is in China where it has three mines and one in development. Eldorado recently received project permit approval (PPA) for the East Dragon project which is expected to produce 70,000 ounces of gold at a very low AISC of $400 an ounce. Currently, Eldorado’s Jinfeng produces about 140,000 at a cash cost of $660 an ounce due to robust 3.95 g/t grade. Tanjianshan produces 100,000 ounces at $500 and White Mountain, a 75,000 ounce producer at a cash cost $650 an ounce with a 3.28 g/t head grade.

We like Eldorado here despite the Greek problems. Turkey is being expanded and Efemcukuru is a high grade underground deposit with over 1 million ounces in reserves. We believe that the combination of Chinese and Turkish assets is an excellent cash machine. Eldorado’s Greek expansion of Skouries, Olympias, and Stratoni while not directly impacted by the Greek problems, remain in limbo as Greece works its problems out. Importantly, Greece will need development and we believe permitting is just a temporary problem. We would take advantage of Eldorado’s weakness and purchase here. Eldorado has almost $900 million of liquidity and a whopping reserve base of 25 million ounces.

Goldcorp Inc.

Goldcorp will produce 20 percent more ounces this year at an AISC of less than $1,000 per ounces. However Goldcorp will spend over $1.3 billion this year while a deteriorating balance sheet has caused its shares to underperform due in part due to concerns about an elevated capital spending program together with concerns about slower developments at Cerro Negro in Argentina and Eleonore in Quebec. To replenish its coffers, Goldcorp sold its Tahoe holdings for $1 billion. Penasquito the polymetallic flagship in Mexico is performing well but that mine is being harvested and Penasquito MEP will cost big dollars. Goldcorp has proven and probable reserves of almost 50 million ounces but investors are wary whether they have the financial wherewithal to exploit this all important resource. We prefer Barrick here.

IAMGold Corp

IAMGold continues to face problems. Recently the guidance at its Westwood mine in Quebec (opened July 1, 2014) was lowered to 60-75,000 ounces from 110,000 to 130,000 due to seismic activity. We believe that engineering and planning should have anticipated these problems. IAMGold has four operating gold mines and Westwood was to be a main plank in its growth. Thus the setback focuses on IAMGold’s other mediocre harvested assets (except Essakane). IAMGold sold its cash cow Niobec and to date there is nothing on the horizon to suggest that the company has turned around or replaced that cash flow. While the Company has a strong balance sheet, investors are concerned they might make another expensive takeover like over-priced Cote Lake or even purchase the balance of Sadiola. In addition, despite Essakane, IAMGold’s AISC is a heady $1,100 an ounce and IAMGold is simply trading dollars here. Sell.

John R. Ing

416-947-6040

share

share

share

share

share