Gold: It Is Not So Different This Time

share

share

share

share

share

share

share

share

share

share

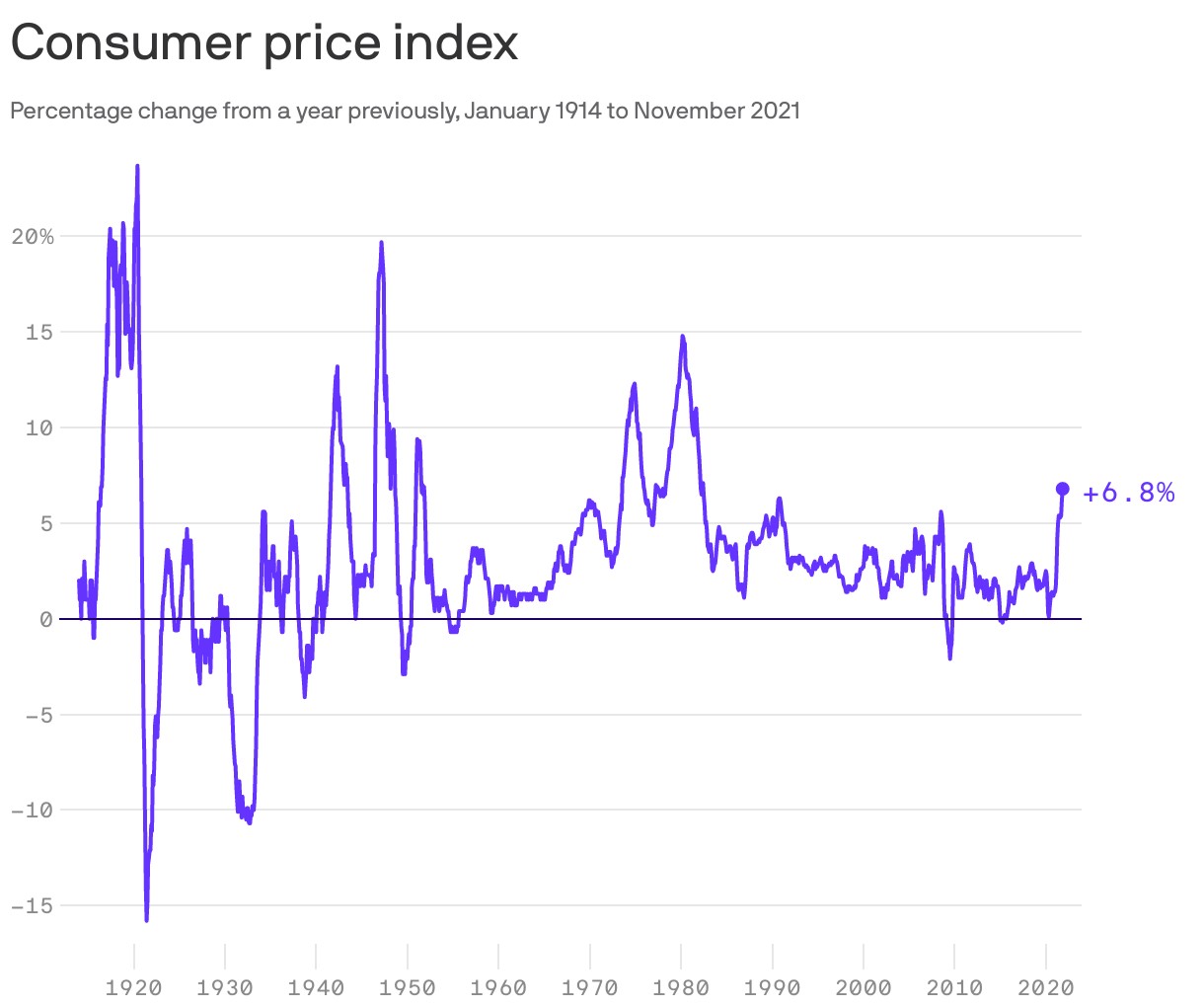

Central banks, politicians and policymakers are surprised that November inflation surged to 6.8 percent, a nearly four decades high, about triple the Fed’s decade old 2% target. US producer prices rose at the fastest pace on record. Having underestimated inflation, ironically they played down its significance and told us that the spike was transitory or a “bump in the road” and due more to one-off causes, such as supply chain disruptions. Soon everything will return to normal. They ignored the historic fact that outsized spending and too much credit is one of the main culprits of inflation. Having released the inflation genie from the bottle, they continue to pursue the identical path and policy responses as too much money chases too few goods, leading to distortions in both the equity and fixed income markets.

Supply chain bottlenecks, labour shortages and OPEC have been blamed for the rise in inflation. And now with out-of-control food, energy and housing prices putting upward pressure on prices, politicians and central bankers have rationalized that we need more post-pandemic spending since demand might abate once the bottlenecks are resolved. Yet higher prices have not blunted demand for more government services. Having issued record levels of debt at historic low interest rates, they have lost their fear of debt. Worrisome too is that since they missed the causes of the inflation surge, how can they come up with its remedy?

Fiscal Fiasco

What’s missed is the underlying long-term force – fiscal profligacy. Federal spending has jumped from an average 21% of GDP in the prior decade to more than 30% in fiscal 2020 and 2021, deepening the debt trap. In 2019, debt to GDP was 80%. Today debt to GDP is over 130%. The Federal Reserve’s balance sheet has bankrolled this spending, purchasing vast amounts of the government debt such that its balance sheet has doubled from $4.2 trillion at the end of 2019, to nearly $9 trillion in June 2021. Although real consumer spending is back to pre-covid levels due largely to the government spending 15% of GDP, the accommodative monetary and fiscal policies also sparked the biggest bull market in history, pushing security valuations to record highs.

In essence government has subsidized demand with billions of borrowed dollars, without having to pay for it. While the Fed’s massive asset purchases are soon to be “tapered” and Mr. Biden’s Build Back Better (BBB) bill might be dead, a modified version threatens to give inflation a second wind. Except for Senator Joe Manchin, government spending is an addiction, it seems. Central bankers are caught in a dilemma. If inflation is transient as they believe, the pre-pandemic landscape of low rates will return. But markets have been whipsawed with S&P 500 recording the worst Black Friday on record when news of the omicron variant spread, recovering when the Fed’s dovish pivot again lifted stock prices. The result is fiscal fiasco.

Another problem is that policy responses are moving at a glacial pace. The Fed continues to maintain the loosest monetary response in history despite above-average growth and inflation at 6.8%. According to the Congressional Budget Office (CBO), America’s fiscal deficit will average 14% of GDP and even a pared down “Build Back” bill will expand America’s safety net adding up to $3 trillion to the deficit over the 2022 – 2023 period. However, the Fed is running out of options when prices are rising at the current rate. Purchasing half of all US borrowing requirements, one arm of the government finances the other arm of government and prints freshly minted dollars adding more stimulus to the economy. The end result is more inflation. The common denominator of inflation pasts and future is money. The noted American economist Milton Friedman famously observed that inflation “is always and everywhere a monetary phenomenon”. According to the St. Louis Fed data, money supply M2 grew at an average rate of 20% in the last two years ending October. The aggressive monetary setting continued with money supply exploding at 35% in the past 12 months. Inflation however is not a tide that lifts all boats.

US Stock Bubble Biggest in History

With runaway inflation overshooting the Fed’s target and rising, the attendant risks have long reaching impact. Near term, the conditions are ripe for a correction. There is little that Fed Chairman Powell can do other than build-up expectations for early rate hikes in 2022. Although the Fed’s response is to start winding down its bond buying programme, they still have kept rates near zero, limiting their options. Interest rates have been kept too low for too long, rewarding debt, penalizing savers and encouraging risk taking. Flush retail and institutions fearful of missing out (FOMO) in the greatest bull market history have taken on more risk, increasing “moral hazard” on expectations that central banks will bail them out in the next market sell-off, keeping a floor under prices.

Reinforcing this complacency is a debt market which currently reflects the lowest rates in history, while inflation is at the highest level in nearly 40 years, generating a sense of false security. 10-year government yields remain at 1.66% creating a negative yield phenomenon that guarantees a loss if held to maturity. The roots of inflation go back to 2008 when governments unveiled massive stimulus programs to boost the asset economy through monetary inflation. While that Keynesian spending spree worked, the programs a decade later remain in place. Then the government doubled down in the wake of the pandemic, with new and improved stimulus packages. For much of the decade, an indulgent Federal Reserve has been the largest buyer of government debt and its pivot to reduce purchases will make it difficult to refinance existing debt. And if central banks raise rates by the 400 to 700 basis points needed to keep up with inflation, such a move would not only ratchet up the cost of borrowings, but remove the underpinnings to the biggest stock bubble in history.

Part of reason the market does not fear debt is that after the 2008 financial crash, central banks kept rates low and having exhausted their conventional tools, they introduced unconventional quantitative easing (QE) which saved the day and investors. And now they have adopted Modern Monetary Theory (MMT), another unconventional tool touted as the new saviour which allows government to create or issue money to pay for spending without ever “running out of money”. It is analogous to a teenager who argues that their credit card balance does not matter. It matters, when the card is declined at the next fill-up. We believe the rise of MMT raises the risk of moral hazard, popular today among investors. That a default has not happened is given as a reason to justify the continuation of MMT and, a “buy the pullback” strategy. However, overlooked is that MMT or free money also exists in once wealthy Turkey, Venezuela or South Africa where double-digit inflation has reared its head everywhere.

That Seventies Show

Data: Bureau of Labor Statistics. Chart: Baidi Wang and Felix Salmon/Axios |

The conventional wisdom is that inflation is bad for stocks. Reminiscent of the seventies when the US had a prolonged period of inflation, cracks are emerging. We can recall the Great Inflation from the mid 60s to the early 80s when the Fed kept rates so low that stock prices boomed as rising profits coincided with rising inflation. In fact, the parallels today with the 1970s keeps growing. Companies then, like today were able to pass on rising costs because stimulus-led demand was strong, swamping available supplies. In 1971, the Fed hiked rates from 3.75% to 5% with inflation at 3.5%. During the decade inflation averaged 7.5% before peaking out at 15%. Noteworthy was that supply-chain bottlenecks and geopolitical scrimmages were nonexistent then. However in the seventies, negative real Treasuries corresponded with a plunging stock market when in 1974, yields reached a low of negative 4.9%, the S&P 500 fell 37%. Today real yields are a negative 4.7% but with some $17 trillion of debt yielding negative rates of return, the S&P 500 is up 30% not down 30%.

Also in the 1970s, housing prices too soared such that the Fed dropped the cost of shelter from the Consumer Price Index (CPI), replacing the input with “imputed rent” calculated on a hypothetical cost that one would have to pay for shelter. That move masked the real extent of prices going up. Today the 6.8% current inflation rate would be more than 10% if the old CPI index was used since housing prices are up 20%, but owner rents are only up 3%. Of course, housing prices today are not only driven by supply and demand, but demand is spurred by the cheap cost of financing or credit – that too was not the case in the seventies. It is different this time, a variant so to speak.

Today policymakers point to the daily highs recorded by the stock market as vindication for their unorthodox money policy. Markets have become lulled into complacency. However, the recent bout of turbulence is cause for concern, particularly the upcoming education of the meme traders. The retail market has been latecomers to the party, spurred by reddit traders jumping from bubble to bubble or meme to meme in the hopes of a fast buck. From the South Sea bubble, tulip mania, dot-com bust and the Japanese bubble, history is littered with investors who have lost their heads, and then their shirts. Former Fed Chairman Alan Greenspan called the bubbles “irrational exuberance”. Today meme stocks, Tesla and FAANG stocks are up in the stratosphere, nothing rational about that. Simply, investors have piled into these stocks in the belief that the market will keep going to the moon even as central banks tighten monetary policy. However, as these traders lose money, their education will prove expensive as their “investments” come down to earth. Like Pavlov’s dog, markets are inured to risk, but markets today are bigger, more leveraged and untested.

America’s Energy Price Shock

Inflation has become a thorny problem for Mr. Biden. With energy prices up 60%, the president was quick to blame the “price gouging” energy sector and Wall Street. Scapegoating the corporate sector for everything from high grocery prices, to gas at the pump, to meat producers is a desperate act when policymakers lack solutions. America’s energy crisis is partly due to the deep hole that the Democrats have dug for themselves, from Mr. Biden’s own policy of cancelling pipelines needed to bring oil to market or to take away gas, to the tightening of regulations that blocked exploration drilling. Along with other sectors, the US oil and gas industry faces financial, labour and supply chain constraints. None of Mr. Biden’s initiatives boosted supplies or his popularity. To lower inflation, he could remove the punitive tariffs (of up to 25%) on Chinese goods which would reduce the prices being paid by consumers. But to progressive Democrats, that would be bad politics today. Or instead of working with ally OPEC, Mr. Biden has vilified them calling on them to reduce prices. To stem spiralling gasoline prices, the president released 50 million barrels of crude which was not enough to reduce prices or provide the energy security or help in the decarbonizing effort. He even unsuccessfully begged them and Russia to increase production in order to bring down prices.

Russia instead announced a new oil supply contract with India supplying Indian Oil Corp. almost 15 million barrels of crude as part of 28 investment deals signed between the two countries. Amid fears of a Russian invasion of the Ukraine, gas prices rose partly due to an assertive Russia limiting supplies, weaponizing its gas hegemony. Then Washington threatened to block the $11 billion Russian backed Nord Stream 2 Pipeline which needs final approval sending prices in Europe to record highs. As a result of higher energy prices, German producer prices are at the fastest pace in 70 years and German purchases of gold in their currency are at 12-year highs.

Domestically, the president is under siege in all directions. At risk is that the energy crisis has hurt the president in the polls losing Virginia in the recent election, a state he won a year ago by a large majority. And in fighting Covid-19 and its variants, more Americans have died from the viruses last year than 2020. He also faces an ever-increasing challenge to balance pledges to decarbonize with efforts to keep energy prices down.

Greenflation

Fossil fuel is the sunk cost of capital. When politicians, scientists and business people converged at COP26 in Glasgow to tackle climate change, they were told that there is the need for a whopping $4 trillion a year to transition from fossil fuels to a decarbonized world. Much of the blame for emitting greenhouse gases is on the road transportation industry which only accounts for 11% of the total, according to Oxford University. Despite much of America’s electricity coming from fossil fuel, subsidies for electronic vehicles, tax breaks for solar and carbon tax subsidies have become part of the growing cost of decarbonization. Predictably, the greening of our economy has led to a spike in prices, undermining the affordability of switching to renewables as fossil fuels become scarcer.

The International Energy Agency (IEA) calculated that current fossil fuel capacity is 4,800 GW (gigawatts). However, new renewable power capacity (windmills, solar, etc.) amounted to only 290 GW this year or 6% of current capacity, far below needed to achieve the net zero emission target by 2050. The problem is that countries are shutting down fossil fuels and ironically carbon free nuclear production at a faster pace than the creation of renewables and today, soaring energy prices are the result. Left unsaid is that the cost of the switch to renewables is already showing up in soaring commodity costs, particularly green metals, widening the gap between fossil fuels and the production of solar and wind energy. Simply, greening the economy will be inflationary.

Energy renewables unlike fossil fuels cannot be easily stored and there are not enough recharging stations today. The trucking industry still is in a nascent stage with a variety of fuels, from hydrogen to liquified natural gas to ammonia not yet economic. Moreover, the requirement for huge tanks with the ability to discharge 70 kg in 15 minutes to have parity with diesel fuel and, the required downtime to recharge trucks on tight schedules, precludes a mass rollout. The bottom line is that decarbonization must offer a higher general standard of living not less, otherwise it won’t be accepted by those who eventually foot the bill.

Money Meets Climate

Governments must do more rather than look for jingoish simplistic solutions or political posturing or even ill-conceived video summits. In the clean energy transition, more must be done to boost supplies of renewable energy and its transition. Investors have become increasingly focused on environmental, social, governance (ESG) metrics. There are no simple solutions. Pipelines don’t even add to global emissions. Specifically, while ESG will increasingly dominate the government agenda, the blocking of pipelines, or natural gas generation or halting drilling or starving the oil and gas industry from capital, exacerbates the problem and will not increase the supplies needed today. Talk of net zero it seems, is mostly that, talk.

With China’s Xi Jinping channeling Mao Tse Tung, President Biden has channeled Lyndon B. Johnson and Franklin D. Roosevelt’s presidency for inspiration. Biden is wrong on FDR who enjoyed majorities in both houses allowing him to pass legislation like Medicare and Social Security. The fiscal excesses of the Vietnam War also helped Lyndon Johnson become a big spender and a legislative majority too helped finance his “guns and butter” policies which paved the way for the Great Society, civil rights and, ironically the Great Inflation. To date, Mr. Biden is losing the popularity battle at a time when inflation is at its worst in nearly 40 years. He was around when the Great Inflation of the 70s ended when Fed Chairman Volcker was forced to throttle back money, driving interest rates to double-digit levels which caused a recession to crush inflation. Obviously channelling presidents is not working and as before, giving people their own money back has not resonated with the American people, with the end result, more inflation.

Don’t Shoot the Messenger

Mr. Biden has also blamed Wall Street for his administration’s problems. A healthy capital market is needed to finance America’s debt. Inflation is insidious and healthy markets are needed to repair its damage. Capital markets are the glue that binds corporations, governments and industries together. Corporations have board of directors, shareholders and management that set the course of business. Decisions are set and capital markets are the medium that allows these decisions to be financed. However, in the era of blame, Wall Street is vilified as well as their advisors. It is sort of like blaming the LCBO for drunks. In reining in Wall Street, it is clear, so too are the potential drawbacks.

As a result, trust in government has fallen. Mr. Biden is in a relatively weak position down in the polls from 51% to 44% and caught in the middle of an ideological battle within his own party. And, despite a slim majority he is dealing with a divided Congress just before the midterms. After the January 6 Capital riot in Washington, challenged election results (BIG LIE) and now some states’ limitation to voting rights, the political winds are blowing from a different direction just as America’s election cycle begins. To better control the electoral process, Mr. Trump is putting loyalists in government, Congress, state legislatures and his supporters have even changed local state voting laws. Mr. Trump and his acolytes are re-shaping the GOP in his image, setting up another battle in 2024, where votes will matter, but control of the counting of the electoral votes might matter more.

Dueling Nations Decouple

The escalation of tensions between the US and China will dominate the next half century. Having lifted 770 million people or twice the population of the United States out of poverty, China’s industrialization sparked a two-decade supercycle, and that growth allowed the rising power of the 21st century to dominate markets. China’s growing economic and military ambitions are raising alarms in the US. To date, trade tariffs, sanctions and blackballing listings have not worked to stem China’s rise. Mr. Biden continued the Trump imposed trade tariffs intensifying the geopolitical war between China and America. Mutual interests like climate change or trade or fighting the pandemic or globalization itself have unfortunately been relegated to the backburner in the current war of words. The escalation of the cold war is moving to a nasty end in which neither side will be able to declare victory.

Through a series of escalating battles, the world’s two great powers are set on a collision course. The Zoom summit is unlikely to cool tensions against the backdrop of growing tensions between the two superpowers as trade, technology and commerce battles escalate. China is ascendant and is the only plausible economic and geopolitical challenger to America’s role as the world’s sole superpower. The US sees China as an existential threat to its global hegemony. The diplomatic boycott of the Beijing Winter Olympics only raises the stakes, putting athletes in the middle between the sandwich of politics and sport. Coexistence is unlikely when both sides seem so far apart.

The Demonization of China Will Have Its Costs

Notwithstanding innovation and globalization, the United States is heavily dependent on China’s markets and the Chinese, western investment and technology. A greener America will need China’s help, which currently dominates much of the world’s clean energy technologies, but it seems never the twain shall meet. In addition to China’s help with climate change, America needs help dealing with rogue states like Iraq, Iran or North Korea. Although both sides need each other, they remain locked in competition, and amid the deteriorating relations, both have turned inward. In less than a year of taking office, instead of enlisting China’s help to deal with Russia, Mr. Biden opened up a two-front battle, taking on both rivals despite history showing disputes on two fronts tend to be disastrous.

The deepening rivalry has extended to the capital markets. The Chinese no longer need access to US capital markets. Chinese stock markets have soared with daily volumes of $174 billion or almost 4 times of Europe. Only US markets are larger in terms of volume. Despite an exodus of listings, a Congressional listing ban and blacklisting DJI and seven others, Chinese data company iFLYTEK were among the big winners. Already China has accelerated the decoupling from US capital markets by forcing uber-type app Didi to delist in the US in favour of a listing in Hong Kong. Chinese big data companies are at the forefront as China pushes for capital and tech self-sufficiency. And, today China has become the world's largest electric vehicle market with companies such as Nio, BYD and LI Auto actively traded. In a step towards independence, China has not listed its next generation of AI or big data, bypassing Western markets, ensuring that Wall Street will miss out on the next fundraising bonanza. Banning Chinese companies has proven counterproductive and will only exacerbate the rivalry between the US and China. Who is zooming who?

Ahead of the United States, China has aggressively secured supplies of green metals, rare earths and processing needed to power the “green revolution” of EVs and clean energy. In the race for strategic battery materials, China is in the forefront, even securing the mining rights for all-important lithium and copper in Afghanistan, only months after the US left. Critically, China has a near monopoly on solar, wind and EV battery manufacturing, which exacerbates the relationship between the US and China. US sanctions and an “America First” program created a technical battle where technology and computer chips have become pawns, yet America risks losing the war because of its growing dependence on China for supplies of green materials. Biden’s green politics has reduced raw materials of all kind. Given that on a per capita basis, the United States is the world’s biggest emitter of emissions, they can ill afford to lose this race.

All this adds up to a very fragile period in world history. American political scientist, Professor Graham T. Allison of Harvard once wrote of the risks of the US falling into Thucydides Trap, when an emerging power challenged the ruling incumbent power, in 12 of 16 times, the end result was war. Today this war might not shed blood, instead it might prove to be a different type of war, a capital war with America’s dollar-based banking system its casualty. China with $3 trillion of reserves is better prepared than America, the world’s biggest debtor. To be sure a capital war would hurt both countries, but America is more levered so corporate America and Wall Street will be among its biggest casualties. However, the biggest victim will be the US dollar, currently the world’s reserve currency. Already China has the largest mobile payment system with mobile phones and 5G replacing bricks and mortar. And there are plans to digitize the renminbi to lessen their dependence on the US financial ecosystem. Thus, in the face of Washington’s poorly timed wish for decoupling from China, who will finance the US government and its ballooning deficits?

America’s Debt Is Its Achilles Heel

China has become the world’s largest creditor, while the US its largest debtor. With the prospects of higher interest rates, a capital battle with China looms. If China overtakes the US economy, the US won’t have enough physical assets to back its currency. The US Treasury market at $22 trillion is the largest market in the world, funding Uncle Sam’s day-to-day activities. It is also one of the most liquid in the world. US Treasuries are the benchmark for all other markets. However, given America’s profligacy and record spending, the US has never been more dependent on the market to pay its bills. Recently however, signs of indigestion and liquidity tremors are surfacing when the 30-year Treasury auction in November met low coverage of interest due to China’s absence.

As the world’s reserve currency, the dollar has been the pillar of the America-led world order since the 1940s. That privilege gives the United States the monopoly power to print dollars at will, at a cost of nothing but the paper and ink it is printed on. The US balance of payments are running the largest in 15 years, pumping more dollars into the global system. Its twin deficits are unsustainable, too high for the health of the globe. And with America’s retreat from the world stage, its profligacy, lack of progress against Covid and inflation undermines the trust in its competency and faith in the US dollar.

China was absent in the Treasury’s recent auctioning of debt needed to finance its growing deficits. Didi’s delisting raises the US-China decoupling risk and in a tit for tat move, China created a blacklist to put curbs on technology investments by toughening “variable interest entities (VIE). In addition to its technological prowess, China is ramping up its financial infrastructure with a host of stock, future and commodity exchanges to finance China’s growing appetite for commodities, goods and savings. Recently opened, the Beijing Stock Exchange (BSE) is a Chinese version of NASDAQ.

China is also the largest gold producer in the world and consumer of gold. Its gold companies have short-life reserves and citizens rely on gold imports for most of their requirements. China also has more control over the gold market purchasing gold for its reserves, becoming the 5th largest holder in the world, dumping dollars. The Shanghai Gold Exchange has become the world’s largest physical gold market. In the last few years, China’s state-owned gold companies have been buying and financing gold mines, and often joint ventured with various western companies. In the third quarter, Chinese consumers bought 221.5 tonnes, up 26% from a year earlier. Instead of dollars, other central banks around the globe have been buying gold. With so much dollar debt in foreign ownership, once again there is talk of devaluing the US dollar, as in the Plaza Accord in 1985 when the US devalued the dollar. The dollar is not forever.

For the past four decades, the West and China have engaged with each other economically and diplomatically to the benefit of both. This year will be important for Mr. Biden and his party if they lose their majority in the midterm. This year is also important for Mr. Xi as China’s 20th Party Congress holds their leaders to account. It is in both sides interest to reach an accommodation since both leaders face internal forces that threaten their position. Protectionism reigns in both countries, so half a loaf may be better than no loaf.

Recommendations

For all the talk of high inflation, a cold war and rising debt, the stock market remains on a tear and a prime beneficiary of the decade of easy money which also stoked demand for corporate debt and real estate, driving up prices across all markets. The Standard & Poor’s 500, the Russell 1000 and NASDAQ Composite Index are trading near record highs as ultralow rates and a combination of monetary and fiscal stimulus inflated bubble assets in everything from the Bruce Springsteen catalog, to bonds, to NFTs, to stocks, and to classic cars. Apple’s market cap increased $1 trillion in 2020 but in less than a year added another $1 trillion to $3 trillion today. Cryptocurrencies have become a $3 trillion market and a new asset class. To date, global public offerings have outpaced their previous record last year at $600 billion and a product of too much cash chasing too few opportunities, often another signal that a bull market is coming to an end. Newly formed carmaker Rivian’s market cap is $100 billion, more than the market cap of Ford Motors or GM despite producing only 100 cars.

Worrisome is that the animal spirits are back with stocks in expensive exuberance territory, a level that has presaged bad returns in the past. Having exhausted most of their conventional tools, central banks have adopted unconventional quantitative easing and MMT which has convinced investors that the economic situation can be managed. To date, the excess liquidity has protected us from Covid and its variants, the real estate collapse in China and soaring inflation. However, the consequence is record debt at a time of rising interest rates, and uncontrollable inflation. We believe the printing press has eroded America’s position as the world’s dominant currency at a time when capital is leaving, which will prompt lenders to demand more concessions to write more checks, either in higher rates or a downward currency adjustment. Gold history shows, is an alternative to the dollar.

And yet, despite all this, gold and gold stocks have been disappointing investments, contradictory at a time when inflation is at its highest level in nearly four decades. While gold briefly broke out of its trading range, flirting with $1,900 an ounce at the beginning of the year, gold retreated into its $1,650 - $1,800 ounce range. What happened? Is it different this time?

Part of the reason of gold’s non-performance is that much of the fiscal stimulus flowed into stocks, bonds and other highly speculative assets. However, we think markets are poised to fall under the prospect of rising interest rates. Noteworthy is that in the 70s, rates went from 4.75% in 1977 to peak at 20% in 1998. During that same period, gold went from $38 an ounce to $850 an ounce. Today, little has changed. We believe that gold is a bet on the gradual destruction of the dollar as the Fed flooded the system with free money to finance a government which has become the biggest spender in American history.

In this report we have drawn parallels with the 70s when inflation was fuelled by deficit spending to finance government, two oil shocks, the Vietnam War and the stagflation economy. Gold’s bull market began subsequently when under the weight of too much debt, President Nixon devalued the dollar by severing the dollar’s linkage to gold in 1971. Gold jumped from $35 an ounce to a record high of $850 an ounce in 1980. Gold then sank back reaching a low in September 1999 at $250 an ounce before beginning its second bull market which peaked at $1,205 an ounce in the wake of the financial crisis. Gold’s third bull market began when the world's central banks again bailed out their economies from the 2008 global crisis using experimental tools in the form of quantitative easing to resurrect the global economy. Subsequently Mr. Trump’s spending and tax cuts widened the deficit. Gold was $700 an ounce in 2008 and peaked at $2,100 an ounce in August 2020. Today, we believe the fourth bull market has just begun which will see gold initially surpassing $2,200 an ounce. Of note, each peak has surpassed its previous peak.

The Never Normal

Consequently, we believe gold will retain its traditional safe-haven role, particularly when everything today seems so risky. We believe the biggest driver this era will be inflation and its effect on the dollar and interest rates. Billions, no trillions have poured into the markets, exchange traded funds (ETFs) and private equity funds who benefited from the cheap money. Higher rates will remove the main prop under equities. Cheap money will not last. Today gold looks particularly cheap in an overvalued world. Proliferating digital currencies and alternate payment platforms like Apple Pay or Alipay lessen the usage of the traditional dollar-based system. It is not different this time. As result, the world has too many dollars they do not want. The US has a serious problem with its deficits and overvalued dollar. When investors believe that the dollar is an overvalued currency and lack confidence in other currencies, the price of gold is a good index of currency fears.

The gold miners have pivoted from growth for growth sakes to pursuing free cash flow because investors want dividends and share buybacks. Both companies and investors have been haunted by acquisitions past where many overpaid. It is not so different this time. Today Argonaut Gold’s Magino project in Ontario is overbudget and likely in need of more financing. IAMGOLD’s billion-dollar Côté Lake too is overbudget and late. New Gold has yet to make a profit from Rainy River. Fundamentals then and now do matter. Meantime performance-minded investors have shunned the gold stocks in favour of the meme stocks and the more growth-oriented tech sector. Institutional fund managers too have avoided the group for some time resulting in an under-owned sector. Consequently, gold stocks are cheap.

The overriding dilemma for the mining industry is reserve replacement. Shunned by institutional fund managers, raising equity has been difficult for many juniors. Consequently, the seniors have been in a frenzied M&A activity since it is cheaper to buy ounces on Bay Street than explore. Last year alone, Agnico Eagle announced a merger with Kirkland Lake, establishing a major new senior player with Canada’s largest footprint. AngloGold acquired Corus, Dundee Precious Metal bought IVN Metals for its Loma Larga project in southern Ecuador. Australia's Evolution acquired Battle North for its Red Lake mine. Earlier Agnico bought TMAC resources in Canada's North. Kinross recently joined the fray, paying a whopping $1.8 billion for Bear Lake which is a project without a NI 43-101 reserve report. Newcrest has acquired Pretium in BC for $3.5 billion in cash and shares, following Newcrest’s purchase of the Red Chris Mine in BC for $800 million. Simply there's a game of musical chairs and not many empty chairs. The bottom line is that gold miners view reserves in the ground as cheap and thus we continue to expect the consolidation to continue, particularly because it remains cheaper to buy ounces on Bay Street. As such we continue to recommend Agnico and Barrick among the senior producers. B2Gold is favoured and developers like McEwen Mining which boosted production by 40% and undervalued Dundee are liked for their development projects.

Agnico Eagle Mines Ltd.

Agnico Eagle posted a strong quarter in advance of the merger with Kirkland Lake Gold. The combined company will produce between 2.5 million and 3 million ounces from 12 mines with combined reserves of 48 million ounces. Significantly both companies are known for their exploration teams and the combined exploration budget could exceed $300 million. Agnico’s future lies in the drill bit, particularly around their 12 mines. The combination will allow the acceleration of a number of promising development projects. A good example is Amaruq which will be brought into production taking advantage of Meadowbank’s infrastructure in Nunavut. At Macassa the #4 shaft’s completion will allow an increase in tonnage. Agnico Eagle will have a large footprint in the Abitibi belt (27 million ounces), combined with Kirkland's Detour ground and Kirkland Lake’s lands. The low-cost producer will be a cash machine. A $100 /oz increase in gold would add $350 million change in operating margins. We like the combination here.

Barrick Gold Corp.

Barrick will have a strong fourth quarter following the repair of the Goldstrike roaster and a strong contribution from the Nevada Gold Mines (NGM) joint venture as well as Barrick’s copper assets due to higher grades at Lumwana. Barrick is the world's second-largest producer with operations in Nevada and South America. With a strong balance sheet, high quality assets and management, the company is expanding its Pueblo Viejo joint venture in the Dominican Republic which will be completed this year. Barrick returned $1.4 billion to its shareholders through dividends and return of capital payments. Ironically Barrick is under-invested in Canada and has been shopping for assets – but so far none have met its tough guidelines. We like the shares here.

B2Gold Corp.

B2Gold had a mixed quarter from its operating gold mines in Mali, Namibia and the Philippines. At joint venture Gramalote, the company plans a revised feasibility study by the second half following more drilling and engineering studies, which hopefully improves its IRR. At low-cost flagship Fekola in Mali, the company has begun hauling ore from nearby Anaconda which consists of two licences hosting several sulphide targets. Fekola keeps on growing and the Cardinal discovery is a potential satellite. Meantime the government of Mali has yet to grant an extension of its license for Menankoto which is a separate license for exploitation. B2Gold sold its West African mining project Kiaka in Burkina Faso in a deal similar to the sale of B2Gold’s Nicaraguan assets to Calibre. B2Gold is one of the lowest cost gold producers in the world, has a debt free balance sheet of $540 million of cash. Producing a million ounces at a cash cost of under $550/oz, we like the shares here.

Centerra Gold Inc.

Centerra’s Kumtor mine was nationalized by the Kyrgyzstan government who decided to kill the golden goose instead of waiting for eggs, leaving Centerra with only two operating mines which produced 77,000 ounces at an all-in sustaining cost of $781/oz. Mount Milligan and Öksüt both generated free cash flow. Meantime there were dueling lawsuits with the Kyrgyz government and there is talk of an out of court settlement. While Centerra has a strong balance sheet and the financial wherewithal to outlast the expected series of court proceedings, the proposed settlement leaves Centerra cancelling the 26% stake held by the government and payment of back dividends. Hopefully as Kumtor’s gold production dwindles, the government will realize that half of a loaf was better than no loaf. Nonetheless given the long history of disputes with the government, the shares are dead money. Sell.

Eldorado Gold Corp.

Eldorado has operations in Turkey, Canada and undervalued Greek assets. Eldorado’s four mines generated free cash flow of almost $30 million and the balance sheet has about $439 million of cash against total debt of $493 million. Kisladag in Turkey did well and Lamaque’s Triangle decline to exploit Omaque will be completed this year. Eldorado has proven and probable reserves of 17 million ounces. Little information however was given on the Greek assets other than Skouries which is in need of a joint venture partner because of the huge capex. Nonetheless Skouries is attractive with IRR near 20%. Eldorado shares trade at a discount to its peers because of the Greek assets which are now protected under an agreement signed earlier last year. Hold.

IAMGOLD Corp.

It doesn’t rain but it pours as bad news haunts IAMGOLD. Côté Gold is overbudget and delayed with costs increasing. Construction is only 36% complete and almost $900 million remains to be spent at the 70% owned project. In addition, IAMGOLD had a security problem at Essakane in Burkina Faso which hurt production. IAMGOLD's problems continue at Rosebel in Suriname and Westwood. Both operations are likely in need of a new mine plan and the company’s big bet on Côté is too risky. Sell.

Kinross Gold Corp.

Kinross bid a whopping $1.8 billion in cash and shares for Great Bear's Dixie project located in the Red Lake area which has yet to publish a NI 43 – 101 resource estimate. Kinross’ shares fell on that news. Kinross has a flatline production profile so the aggressive move looks like a desperation gambit for growth. Moreover, paying a healthy premium does not make sense when so many recent mergers of equal deals eliminate the accounting fluff and temptation to overpay. Meantime Tasiast expansion is targeted mid 23 and La Coipa late this year. Russia still contributes 20% plus of Kinross’ production, which is geographically risky. Sell.

Lundin Gold Inc.

Lundin Gold had a strong quarter at Fruta del Norte (FDN) gold project in Ecuador. Fruta del Norte is the world’s highest-grade project and the company generated free cash flow of $52 million in the latest quarter. Lundin also began an exploration program looking for satellite deposits. The South Ventilation Raise should be completed early this year as part of the mine plan which will improve output. The company's regional drill program has been expanded to 11 km. Lundin will produce between 380,000 and 420,000 ounces at an all-in cost of around $800 an ounce. We like the shares here.

Newmont Corp.

Newmont had a disappointing quarter and lowered guidance. Still the company is a cash machine generating $400 million for every $100 increase per ounce in the price of gold above $1,200. Newmont’s Yanacocha sulphides price tag ($2.1 billion) went up because of inflation and the project won’t be built for years (2027). Boddington’s production in Australia was also a problem with production shortfalls partially because of heavy rainfalls affecting the ramp-up of the first and maybe last, autonomous haulage fleet. As a result, Newmont lowered production guidance to about 6 million ounces for the year and continues to work out problems in restructuring its portfolio from Coffee to Pamour to the Penasquito layback, inherited from the Goldcorp acquisition. We have long suspected that execution will be important and that it would take time for Newmont to work out the problems. Nothing to date has changed our view. Nonetheless free cash flow of more than $1.7 billion will allow the company to digest Goldcorp and spend $300 million on exploration. We prefer Barrick here.

New Gold Inc.

New Gold sold its Blackwater gold stream to Wheaton Precious Metal for $300 million. The sale price was attractive and salvages something following the sale of Blackwater to Artemis Gold. The transaction helps New Gold’s balance sheet loaded with long term debt of almost $500 million. The company is still working out problem-prone Rainy River in Northwestern Ontario. Total cash costs remain high at a gold equivalence basis at $1,400/oz. Frankly every ounce that New Gold produces at Rainy River is a loss. At New Afton, the new mine plan’s all-in costs are around $1,300/oz. On a positive note, the company did report positive cash flow in the quarter and looking ahead, New Gold hopes to optimize its underground mine plan for Rainy River where measured and indicated resource is 1.8 million ounces. Cash on hand is $180 million, allowing New Gold to make a handful of small exploration bets. We view New Gold as a source of funds.

Yamana Gold Inc.

In the latest quarter, Yamana's costs increased despite stronger production from El Peñón in Chile and joint venture Canadian Malartic. Cerro Moro in Argentina had a better quarter due to better grades. Yamana received the permit to expand flagship Jacobina to increase 10,000 tonnes per day. The permit will allow Jacobina to increase throughput boosting ounces after a 10% increase in production this year. On a positive note, a feasibility study on the MARA project is expected next year. Yamana is a Canadian gold producer but its shares have lagged its peers due to a debt load of almost $800 million. We prefer B2Gold here.

John. R. Ing

Please refer to the Legal Section of our website (maisonplacements.com) for our Research Disclosures for an explanation of our rating structure at https://maisonplacements.com/research-reports.

********

share

share

share

share

share