Gold: It Was Good While It Lasted

It was good while it lasted. But now the golden age of near-zero inflation and interest rates is over, and we are paying the price for living in a fool’s paradise since money is no longer free. All this is now changing. A new economic reality has ushered in. As the pandemic exposed the vulnerability of supply chains, the Russia invasion exposed the scarcity of energy and materials. Escalating prices have created a “cost of living crisis” ahead of the political and social agenda. Inflation is up everywhere. And after fooling themselves and the public on successfully wrestling inflation to the ground, central banks are now riding to the rescue, lifting interest rates to subdue inflation. They have a long way to go.

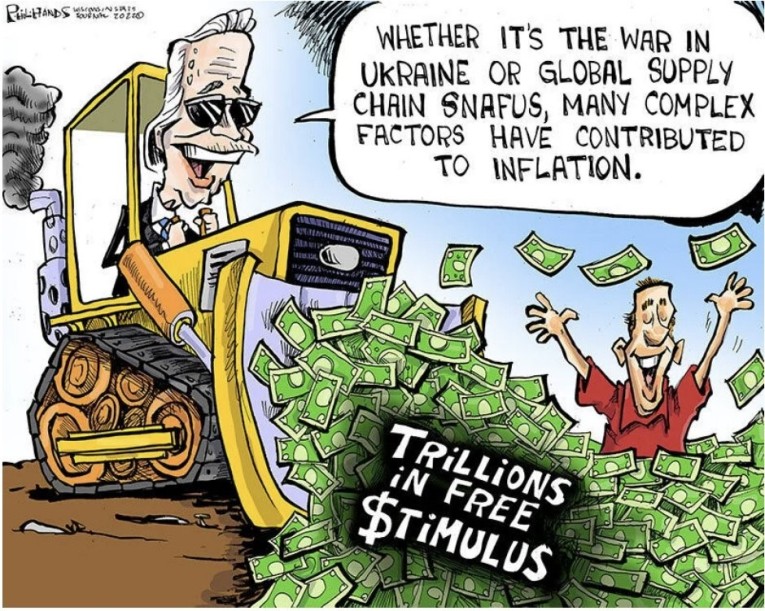

From Presidents Obama to Trump to Biden, all preferred to spend without raising taxes which led to a 40% surge in the broad monetary aggregates and subsequently today’s inflation. The feedstock of inflation is too much money. Compounding its mistakes, the Fed continues to pump liquidity shrinking its $9 trillion balance sheet at a snail’s pace. Instead to bring down the consequential high inflation, rates spiked and the casualties today are markets, bonds and currencies. Food in particular has become an inflationary problem as the spike in energy and the blowback from Western sanctions send commodity prices sky-high, eroding the spending power of consumers.

The Russian economic war no doubt helped contribute to the soaring inflation numbers. Fertilizer and food prices skyrocketed because the cost of nitrogen-based fertilizer which uses gas as a feedstock has doubled in price in the wake of the war. Russia, Ukraine, and Belarus are the big producers, and a shortage will impact this year's and next year's food harvest. Also with a good part of Ukraine’s arable land under bombardment, grain exports to the developing world slowed down, causing a geopolitical dilemma. The disruption of supplies on top of the pandemic puts events into overdrive as the biggest consumer in the world, China slowed down due to the impact of its zero-Covid lockdowns. China will be hard-pressed to hit their 5.5 percent growth target this year. Moreover, the slowdown also had a negative impact on demand for commodities which is expected to be temporary since China must restock already depleted critical mineral resources. This serves to underscore that today’s inflation is not illusory, nor backing down nor resolved by central banks’ tepid rate increases.

Winter Is Coming

The grim news keeps mounting. The biggest contributor of inflation is energy. Russia supplied the EU with 40% of its natural gas last year and the nearly 400% increase in natural gas prices is driving up electricity prices. Mr. Putin has done much to divide the globe, plunging Europe into an energy crisis as Russian supplies came to a halt sparking a cost-of-living crisis in retaliation for Western sanctions. Europe’s largest economy, Germany is at the centre of the energy shock on fears that consumers and businesses won’t have enough gas this winter. Germany’s economy and huge manufacturing base became dependent on cheap Russian gas as a power source with almost 50 percent of their gas via Europe’s main artery, the Nord Stream I pipeline. When Russia weaponized its energy exports, Germany instituted emergency closures, rationing, and restarted dirty coal plants, virtually ensuring they will not meet their net zero emissions commitment pledged only nine months ago in Glasgow. The German government also gave the go-ahead to build fixed liquefied natural gas terminals (LNG) but that won’t help until 2024, at the earliest. And the government was forced to a $15 billion bailout of Uniper, one of Germany’s biggest utilities and Europe’s largest buyer of Russian gas which faced bankruptcy when gas flows were suspended. While the stopgap measures and gas rationing are likely to avert a crisis, those plans cover only six percent of the country's electricity needs. German efficiency has become costly.

In turn, the EU urged its members to impose windfall taxes and cut usage 15% to avoid freezing this winter. However not all are cutting back, dividing the EU and playing into Mr. Putin’s hands. Europe’s energy intensive zinc and aluminum smelters were forced to curtail production because of the resultant 50% increase in electricity prices. Also the global heat wave boosted natural gas demand which provides roughly 40% of all electricity production. The historic drought condition also threatens water supplies joining energy as a scarce resource. With energy prices climbing, Western sanctions were undermined by Turkey who is the only NATO member that has expanded trade with Russia by paying for Russian gas in rubles. Mr. Putin continues to stir the pot where in Italy, three parties with close ties to the Kremlin capitalized on Italian discontent with the political class causing the collapse of the Mario Draghi government and plunging that country into a debt crisis. In the UK, British households’ electricity prices will go up 80% to $4,000 a year at a time of surging double-digit inflation. The energy poverty extended to Norway too where one of the biggest electricity exporters, Norsk Hydro warned that shortages would adversely affect energy-intensive aluminum production. Already some 900,000 tons of smelting capacity is shutdown causing Norway to limit exports of electricity to its neighbours because its hydropower reservoirs are historically low.

Inflation and Debt

Late this summer a decline in energy prices brought temporary relief sparking a rebound in the stock market. In the world’s biggest economy, crude oil dropped from around $125 a barrel in March to under $90/bl. Gas in the United States was $5.00 a gallon and is now below $4 per gallon. Lumber is off 60% since March, firing up hopes of a slowdown. The falling prices led to a “dead cat” bounce. As winter approaches we believe the respite was a false hope, and only a hiatus. It was good while it lasted.

Source: Twitter

War is not the only factor playing havoc with prices. First, prices earlier were in the stratosphere posting new records. The corrections only show deacceleration. Second, core inflation, stripping out energy and food remains stuck at 6%, or three times the Fed’s target. Inflation is shaping public life. Too much money is chasing too few goods or people precluding by the way, a much-feared recession. Third, the Fed kept interest rates too low for too long and are paying the price for their policy mistakes. Fourth, China the world’s second largest economy announced a rare contraction of -2.6 percent compared with the first quarter of this year registering an anemic 0.4 percent GDP growth year on year due largely to the lockdowns. China's restrictive Covid shutdowns affected 250 million people and almost 20% of China’s economic activity which crushed demand for goods and commodities from the rest of the world. Like others, China is suffering from a property market meltdown as homeowners reel from the impact of higher costs, now that free money is gone, causing China to introduce both support and stimulus programs to alleviate production shortages and supply chain issues. Nonetheless while the lockdowns have kept everybody at home, China's exports grew 18 percent in the latest quarter and when China emerges from the slowdown, it will need to replenish inventories causing again a global scramble for critical minerals.

Amid fears of a recession, there is a resilient US economy with vibrant auto sales, consumers flying visiting relatives, and going to theatres such that durable goods orders grew for the fifth month in a row. True, the stock market is lower than last year. But the market demonstrated again and again that as a harbinger of what is to come, the market has predicted 11 of the past 4 recessions. And, with consumer spending making up about 70% of America’s GDP, consumers with bank accounts topped up by pandemic checks continue to spend, holding a record-breaking $16 trillion in debt as they borrowed more on their credit cards.

Hawkish Talk, Dovish Action

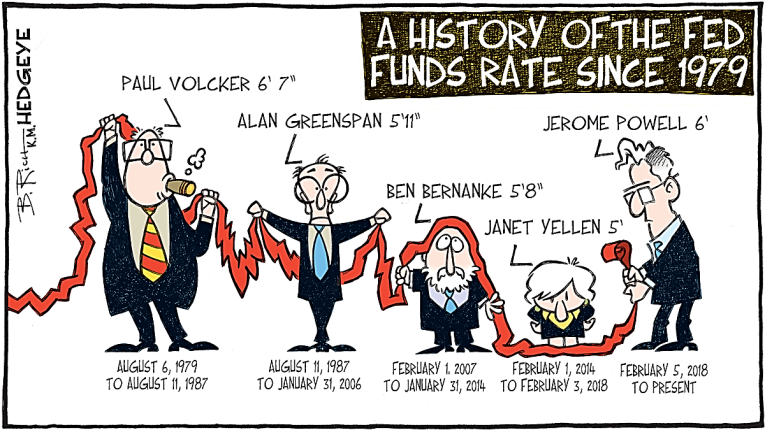

Consequently whenever America raises rates, everyone goes into a panic on a Volcker-type fear that higher rates will trigger a recession needed to bring inflation down. At Jackson Hole, Fed Chair Powell’s emergence as a Volcker acolyte scared the market. Higher rates can affect demand, not supply. Fear of higher rates caused the stock market to lose 17%, bitcoin shed 47% of its gains and corporations led by the tech stocks have lost some $12 trillion of market value. Walmart reported big losses from too much inventory. Noteworthy is that faced with a choice: raise rates gradually and slow the cost of credit for already overburdened homeowners or, raise rates quickly in a strong dose of medicine needed to pull inflation down, the choice we believe has already been made. 2024 is to be another presidential year.

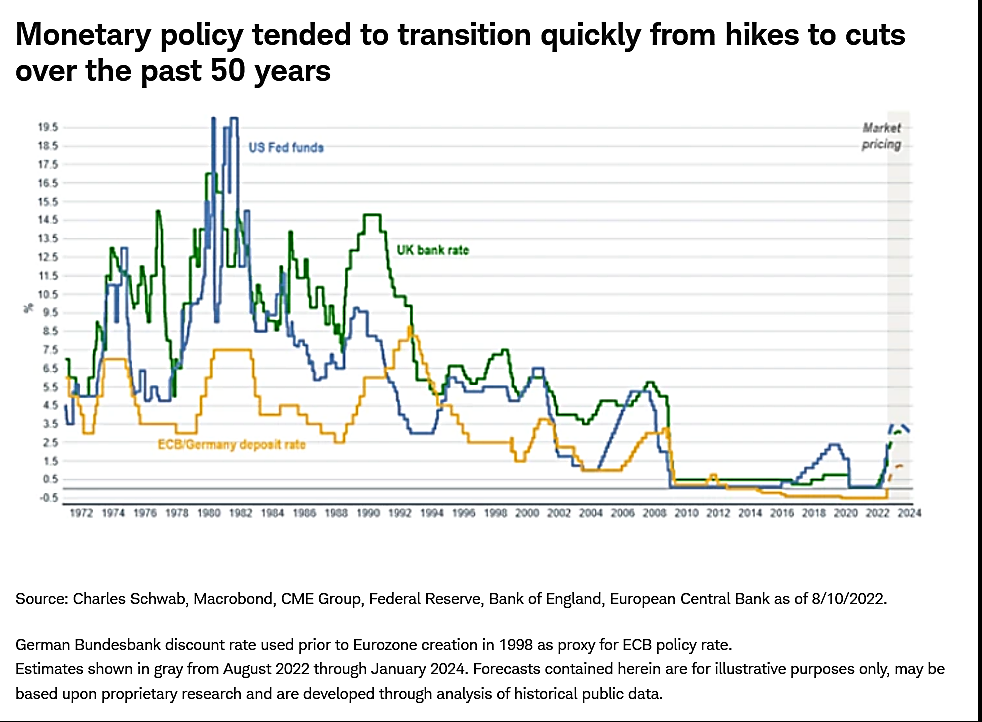

Simply, a Volcker-style rate shock recession is unlikely. Much has changed since the seventies. Rates averaged 11.2% in 1979 rising to almost 15% in 1980 prompting then Fed Chair Volcker to boost rates to 20%, bringing down inflation to 3% by 1983. Today rates are still negative but this time America’s debt to GDP is 130% instead of 32% in 1980. And today, inflation is higher than interest rates. Back then, interest rates were higher than inflation. We are only just beginning. Yet today, Asia has become the global locomotive powering the global economy with China and India making up 60% of emerging market output, up from 20% in the seventies. Asian balance sheets are stronger than the seventies when higher rates triggered an Asia debt crisis because their economies and debt were tied to the dollar. This time only 16% of their debt is in foreign currency, including the greenback. Debt laden America has little room to maneuver.

Summer of Discontent

Today Americans are being paid to stay home despite the current labor shortages that have plagued numerous sections of the economy. July job openings are a whopping 11.2 million jobs unfilled and August payrolls grew by more than 300,000 jobs. The job slowdown hasn’t materialized. Today airports are jammed because of a lack of workers not only in security lines, but pilots. Flying has become a problem with Heathrow limiting passengers to 100,000 a day. San Francisco’s office vacancy rate is 24% as workers stay home. Restaurants, airlines, schools and nursing homes are struggling to find workers. In the post pandemic world of labor shortages, it will take time for labor to come back and thus the upward pressure on wages, will further fuel inflation as demand for workers outstrips supply. As a result, wages grew at a record 5.3% pace last quarter.

Part of the reason is that the United States flooded the system with free money, spending $6 trillion on relief stimulus packages with the latest, a whopping $2.7 trillion package. The $1.9 trillion American Rescue Plan Act in 2021 for example went largely towards transfer payments with stimulus checks, tax credits and unemployment benefit totaling 8% of GDP. Simply, workers were paid to stay at home and they stayed. In Canada, two programs, Canada Emergency Response Benefit (CERB) and Canada Emergency Wage Subsidy supported the economy on top of UIC putting in place a guaranteed minimum income support scheme to two thirds of Canadian adults.

Not surprisingly, US unemployment has fallen to 3.7 percent, the lowest level in half a century and the same conundrum has spread globally as people are paid not to work. In addition to the buffer of people who have yet to return to the workforce there is also an aging workforce and boomers who decided to retire rather than expose themselves to Covid further shrinking the labour pool. The largesse of governments paying people not to work comes at a time when the world economy faces a global restructuring. Some say that after two years of being paid to stay at home, workers are expected to return as pandemic subsidies run out over the next 12 months. Others however say that a structural change is occurring with boomers gone and the government’s largesse really is a minimum wage scheme that provides income support financed by taxpayers. Either way, the cost is inflationary and unproductive.

The New Cold War

China is the elephant in the room and the lockdowns as a result of its zero Covid policy risks economic damage on a global basis. China represents about 20% of global GDP becoming one of the world’s pre-eminent economic and military powers without firing a shot. Cutting interest rates and introducing stimulus programs will ensure China’s growth trajectory to coincide in time for the 20th Party Congress at which President Xi Jinping will seek an unprecedented third term. And despite mounting tensions between the US and China, American corporations continue to develop closer supply chains, markets and technology to gain access to the world’s biggest market and manufacturing base. Business outsourced vast quantities of work to China in the past two decades and untangling those relationships threatens the relationship between business and the Biden’s administration. Both countries backed down on delisting 260 Chinese companies on US exchanges, worth about $1.3 trillion, maintaining US access to Chinese capital.

We face a new era of great multi-polar power competition where capital, energy and economies will dictate political and commercial relationships, no matter the borders. Today, Americans faces a hostile international environment, probably the worst since the Second World War as China seeks the same kind of global dominance over the next century that the US enjoyed during much of the last.

And despite the West’s wide-ranging sanctions, Russia’s energy revenues are higher than before the invasion of Ukraine. Although Moscow’s exports to the West have fallen by 2 million barrels a day, India, China and Turkey have stepped in, taking advantage of cheaper crude. On the other hand, the energy crunch has hit the West more, resulting in mass closures, rationing, and soaring inflation, with vast ramifications for the western economies which remain reliant ironically on China and Russia for energy, chips, food and crucial minerals. Although America’s allies appeared united on confronting Russia, that solidarity was undermined by the continuation of Trump’s tariffs, economic nationalism and Chinese relations. In fact, bilateral relations between the two superpowers are at the worst in 50 years and there is political momentum on a Sino-American decoupling following Speaker Nancy Pelosi’s trip to Taiwan, highlighting division between the White House and the President’s own party. Diplomacy has gone out of favour, replaced by sabre rattling or the odd provocative trip, kicking sand in China’s face poisoning a once healthy relationship. However amid the shifting geopolitical tectonic plates, hard power has replaced soft power and today, America has little power.

Part of the reason is that America over the past decade created an unsustainable entitlement state based on theory and a disregard for history. America spent $6 trillion plus on pandemic rescue support without raising taxes of which Biden’s $1.9 trillion stimulus bill alone represented 8% of American GDP. To finance that spending, the Fed conjured money from thin air using unconventional monetary policies like Quantitative Easing (QE) and later MMT where the government bought bonds that it created, paid with freshly minted dollars, increasing its balance sheet by $5 trillion in only two years.

And despite the resultant inflation at a sky-high 8.5% in July, a spendthrift White House continues to dole out more taxpayer money to college graduates, Tesla owners and solar factories, resulting in the lowest Biden’s popularity ratings. While inflation is raging, Biden chalked up a trio of legislative victories with a complacent Congress as part of an expensive vote buying exercise which widened the budgetary gap and stokes inflation. There was the prescription drug legislation spending, a $200 billion semi-conductor subsidy bill and a $700 billion climate, health and tax bill named ironically the “Inflation Reduction Act” which does nothing to bring down inflation. Instead the bill creates tens of billions of dollars of boondoggle giveaways for electric vehicles, wind and solar. But there was more, with the crucial November midterms around the corner, Biden used an emergency executive order to cancel the student debt of 27 million Americans under the government-run student loan program, transferring the debt to taxpayers in a worst time to pour half a trillion dollars on the inflationary fires. Pocket book protections that will help his November midterm chances? Nope. Just more fuel for inflation, maybe hyperinflation.

America is at War, with Itself

For most of the half-century America has been the superpower of the world. Its global hegemony allowed its currency to be used as the world's currency, militarily, geopolitically and culturally. America was the place to be. It was good while it lasted. However, America is in decline. What happened? America is in debt to the world. Its finances are in shambles with a trade deficit not only with China but 105 other nations. Its budgetary deficit as a percentage of GDP ranks higher than emerging nations. That result is clear, but like the government’s views on inflation or the recession, they are in denial.

Its military might too has been tested and failed, from the early days of withdrawal from the Vietnam War to the embarrassing exit from Afghanistan which followed the retreat from Iraq. To the war in Ukraine, America has countered with sanctions, rearming Ukraine a dose of tough rhetoric. Yet the war continues. The cost of US ineptitude rises every day. Blocked from the western payment infrastructure, China, Russia, and Iran created alternative payment systems working with the big energy producers and as well as consumers. Taking advantage of the geopolitical differences this group also aligned with energy-rich Middle East who will reap a huge $1.3 billion windfall in additional revenues over the next four years, according to the IMF, allowing them to substantially acquire more global assets, build-up energy production and renewable infrastructure with their surplus petrodollars.

America is the largest oil producer in the world but has little spare capacity after Biden cancelled pipelines, oil leases and limited fossil fuel production as part of his green commitment. Instead OPEC is considering cutbacks to keep the oil price up. America is finding itself with fewer allies. At home, domestic law and order has been tested and failed. The peaceful transfer of power on January 6th a year ago was not peaceful as hearings showed. The Supreme Court, the highest in the land reversed the constitutional right to abortion despite the majority of Americans in favour of keeping women’s rights. Federal agents raided an ex-president’s home just ahead of elections. At this time of political zealotry, cultural wars proliferate in America, hollowing out trust in democracy at home and abroad. America is at war with itself.

The High Cost of Free Money

Nonetheless the US dollar is trading at its highest level in two decades driven largely by higher interest rates and its safehaven status. However the era of low inflation and cheap energy is past. Risk is on. An energy reckoning looms. A strong US dollar annihilated US international companies with billion-dollar losses, especially among America’s big tech giants. IBM, Microsoft and SalesForce have issued warnings as the bulk of earnings come from offshore markets. The big tech companies account for 23% of the S&P 500 market cap. And the world’s biggest consumer companies like Coca Cola, McDonalds and Walmart are reporting big hits and announced price hikes which will have the effect of consumers having to pay more for basic staples. For the first time in 14 years, a Big Mac cheeseburger will cost more. All this will add to America’s inflation, and an erosion of its safehaven status.

Economically, for example America's reckless borrowing has resulted in the production of dollar claims which have come home to roost. In 2007, publicly held debt was 25% of GDP but after a financial crisis, two recessions and the pandemic, it is 130% of GDP, a level that has often foretold past currency crises. The national debt keeps mounting, and higher interest rates makes it harder to service. The interest rate on that debt has doubled from $500 billion to almost a $1 trillion a year. As before, Fed Chair Powell has brought out “tough” rhetoric, threatening to emulate Paul Volcker who defeated near hyperinflation by raising rates to double digit levels 40 years ago. But talk is cheap. The reality is a continuation of the “stop and go” policies with a dose of “tough” hyperbole. It will be not enough to stop this inflation. As an example, Powell promised to reduce the Fed’s $9 trillion balance sheet, a source of significant and sustained inflation. To date the largest balance sheet in the world has declined by a paltry $28 billion as of July 13, a rounding error. To work, the Fed would have to lift rates by four times and sell its stock of mortgage-backed securities in a no-bid market. The Fed tried in 2019 but abandoned the move when Wall Street retreated in a “taper tantrum.”

The US has weaponized the dollar’s hegemonic status and its control over the international financial system making spectacular use of its “exorbitant privilege” as Valéry Giscard d'Estaing, former French president observed in the 60s. Western sanctions against Russia have hurt, but the war continues. Similarly Russia too has weaponized its energy exports emulating the leverage that OPEC and Saudi Arabia hold over the West. This power is being used instead of missiles and soldiers (Ukraine aside). Geopolitical relations have been fractured as Europe faces an energy-induced recession, testing the Western rules-based order and forcing many countries to search for alternatives in a push for self-reliance. Moreover, fundamental imbalances bode ill for the dollar.

In the future, the most vulnerable is America with its string of deficits and highest per capita debt load in the world. America’s rhetoric and actions are not always aligned. History shows that the US follows the rules it created only when it suits its purpose. The cost of miscalculation is huge, given its precarious financial state.

US-China Financial War

In the case of US and China, Pelosi’s visit to Taiwan was an unneeded provocative move for a number of reasons. Taiwan’s biggest company is Taiwan Semiconductor Manufacturing Company (TSMC), the world’s dominant semiconductor chipmaker whose chips are used in everything from cars to military. America hoping to create a new champion introduced a paltry $52 billion subsidy to boost domestic production, a drop in the proverbial bucket or chip. More important is the need to source critical minerals such as nickel, copper, lithium, and cobalt as well as other rare earths to counter China’s dominance in green technology. By raising geopolitical tensions, America is forcing China to raise the stakes, in this case, chip stakes. However, Pelosi’s grandstand visit to Taiwan not only sparked numerous flyovers, missile launchings over the capital city Taipei, but set in motion an escalation when relations between China and the US were already in a dangerous state which could yet prove fatal for the island, and the world. America is vulnerable.

After flooding the system with free money, America has become the largest debtor in the world on the brink of a “made-in-America” recession, while China has become the world’s largest creditor. The problem today is that it is time to payback what America owes, and particularly since it is now much more expensive to payback. In today’s world amid the polarisation, who will bailout America?

America has printed more money in history since the US went off the gold standard. In spending more than they make, successive episodes of bigger and bigger bubbles were followed by bigger busts. The current climate combines both a sharp increase in energy prices with a restriction of supplies, an echo of the seventies when oil prices quadrupled and inflation spiked. This time inflation is far ahead of interest rates and there is no Paul Volcker on the horizon. The economy is overheated, real rates remain negative and policymakers are frozen by the election cycle. In Turkey, Argentina or Venezuela where hyperinflation persists, central banks won’t raise rates higher than inflation, needed to bring it down. In the United States, the Fed is also reluctant to take the necessary steps and hyperinflation is a possibility. America is currently experiencing a prolonged period of economic and political decline and inflation has reduced the idea of US exceptionalism despite warnings some 100 years ago when John Maynard Keynes wrote about rapid inflation in Europe, “By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily and, while the process impoverishes many, it actually enriches some.”

It seems, we are all Keynesians now.

In The Beginning, There Was Gold

The first World War so burdened the UK with huge debts that it was forced to leave the gold standard. The slump of the 1930s followed. Without the discipline of a gold standard, what followed was a series of booms and busts of the Twenties until July 1944 after World War II when the Bretton Woods Conference created the IMF and restored the gold standard. That lasted until the early 70s when President Nixon, following the damages and debt of the Vietnam War, severed the link between gold and the dollar. Since then the dollar became the world’s reserve currency. The dollar is a dominant, inconvertible currency which is its structural weakness. All other currencies face the discipline of the market.

The dollar backed by the full faith and credit of the United States is vulnerable with America’s growing mountain of debt and twin deficits. Lacking savings and the need to finance expenditures, the US has levered its exorbitant privilege, borrowing surplus savings from abroad. As debts pile up, America risks losing its special privilege. One can detect the erosion in confidence. What damages trust in the US, damages the world. After World War II, the US accounted for the largest share of world GDP at more than 25%. However, since the past few decades, economic growth has shifted to the East, at the expense of the US. China today is at the centre of this growth as its share of global GDP quadrupled to over 20%, roughly the same as the US today. In addition to China, the economies of Southeast Asia which includes India, have grown faster in part because of demographics, lower taxes and a boost from China. Energy rich Middle East too has grown over this period in wealth and influence.

While Europe is facing its worst energy and economic crisis, America the largest economy in the world initiated a Cold War with the Chinese, further dividing the world. One time America was a defender of a rules-based world order and democratic values using soft power to build consensus, encouraging the establishment of free markets, rule of law and institutions. However, the US no longer isn’t unblemished when it comes to rights. The seizure of Russian assets and foreign exchange reserves without due process casts a shadow where everything from sanctions to trade with allies have undermined trust in America. American sanctions’ political costs are mounting as throttling the flow of gas has caused an European energy crunch. Ironically, none of these moves have stopped the Russian invasion. America seems to be leading from behind and the vacuum is ironically being filled by America's competitors.

The Dollar Is Not Forever

As the US becomes more polarized and insular, dollar currency transactions have declined exacerbated by the Ukraine War, the energy crisis and the pandemic, amplifying its debt problem. In June, central banks bought 59 tonnes of gold and in the first half, they have purchased 270 tonnes despite Ukraine selling 12 tonnes to pay for the war. Like Europe’s addiction to Russian gas, America’s addiction to debt gives the potential for China to leverage that dependance in the future. China’s $3 trillion in foreign currency reserves is the largest stockpile in the world. Relations between China and the United States have worsened and ominously, China has reduced its holdings of US government bonds for the sixth month in May to $981 billion.

Russia and China have been building their gold reserves. The Fed has become part of the problem. Initially misdiagnosing what has become the worst inflation in four decades and then raising rates to catch up, but framing the increase as transitory, the Fed has accommodated the highest increase in federal spending ever including the multi-trillion-dollar war on Covid. Financing the US government has become costlier with the rate increase and the Inflation Reduction Act puts more fuel on its fire. Yet by keeping the Treasury’s real borrowing costs artificially low, the Fed adds more fuel to that fire. The Fed’s policies simply have benefited government at the expense of the private sector. History shows that heavily indebted nations see their currencies weaken when the rest of the world no longer trust they can pay their bills. Given America’s rising deficits, dysfunctional politics and dependence on foreigners to finance itself, the dollar is not forever. Gold will be a good thing to have.

Recommendations

To many, gold has been a major disappointment, declining 6% in the past year despite major geopolitical upheavals and soaring inflation. Yet looking more closely, gold has been an effective hedge, in terms of other currencies as gold in euros is up 15% from a year ago. Similarly in pounds, gold has increased 14% from a year ago and gold /yen is up a whopping 22%. Even in dollar terms, gold has been effective, but volatile. When Russia invaded Ukraine, gold hit a peak at $2,000/oz in March. In the past quarter, gold averaged $1,800/oz. In July, gold hit a low of $1,700/oz but rallied to $1,800/oz in August. Longer term in dollars, gold has gone up 470% over the past 20 years. Consequently, we believe gold’s pullback is timely having successfully tested $1,700/oz again. We continue to target $2,200/oz. This bull market has only just begun.

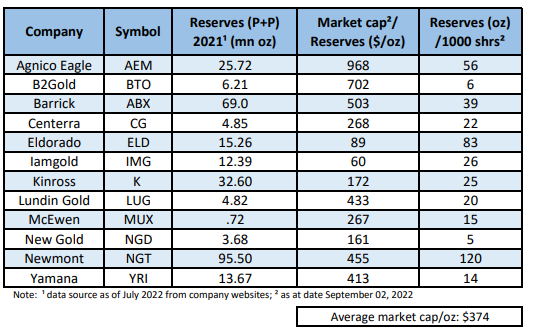

The mining industry’s profits were hit with higher costs despite gold averaging $1,872/oz in the second quarter. Newmont, New Gold, Eldorado and Centerra were particularly hard-hit. Lundin, Agnico Eagle and Barrick bucked the trend and showed good cost control. Unlike the popular meme stocks, gold companies have a firmer base in fundamentals. Today gold shares are under-owned and neglected despite producers throwing off huge cash flows. Most have been able to contain costs, keeping margins wide. Barrick and Centerra have built up huge cash hoards. The industry reserves are declining so M&A activity is expected to continue. South African miner Gold Fields’ premier bid for Yamana is a reflection of the need for reserves. It is cheaper to buy reserves on Bay Street than to explore with the market cap per ounce of reserves under $400 an ounce – cheap today, ensuring continued M&A activity. We believe the fundamentals for the industry are positive as geopolitical uncertainty, soaring inflation and a dysfunctional US will spur investment into gold, a barometer of investor anxiety. Among the stocks we like Barrick, Agnico Eagle as well as developers B2Gold, McEwen Gold for their growth potential. We also like Lundin Gold and would include potential M&A tidbits like Eldorado, Dundee and Centamin in portfolios.

Agnico Eagle Mines Ltd.

Agnico Eagle is a large-cap Canadian producer with production in Canada, Finland, Australia and Mexico. Agnico reported a stronger quarter maintaining guidance, producing almost 900,000 ounces at AISC of $1,026/oz due to better grades and cost control. A new mine plan at Detour Lake added 5.4 million ounces to reserves and extended mine life to 2042. Agnico also reduced debt by $125 million. Gold production was better than expected due to contributions from Amaruq, Detour Lake and Macassa which performed better. Gold reserves at Detour stands at 20.4 million ounces which will increase further with recent exploration drilling showing an extension with positive results. At joint venture Canadian Malartic, Agnico Eagle has about 20 drills turning at Odyssey to delineate that deposit. And Agnico has a disciplined management team with strong execution capabilities which allowed them to efficiently digest Kirkland Lake Gold. As a result, Agnico has a strong balance sheet with $2.2 billion of available liquidity. We like the shares here.

Barrick Gold Corp.

Despite higher costs, Barrick Gold had a strong quarter maintaining guidance that allowed it to outperform its peer, Newmont. Barrick’s array of Tier I mines generate huge cash flow that allows them to establish long-term assets like Reko Diq in Pakistan. Definitive agreements at Reko Diq with the government are being finalized as Barrick updates the feasibility study with a targeted 2028 start. Reko Diq is one of the world's largest undeveloped copper/gold deposits with about 3 billion tons grading 0.48 copper and 0.26 g/t gold and a 40-year mine life. Barrick noted that construction on the Pueblo Viejo (PV) plant in the Dominican Republic is 56 percent complete and the project costs at $1.4 billion remains unchanged, despite the new Tailings Facility. Pueblo Viejo commissioning is expected in the first quarter of next year and the additional capacity will allow average annual production of 800,000 ounces, extending the mine’s life to 2040. And at Bulyanhulu in Tanzania, Barrick has turned around the once trouble-prone Tanzanian mines elevating those mines to Tier 1 status and is negotiating an agreement with the government to extend mine life as well. We like the shares here for Barrick’s both near and long-term prospects.

B2Gold Corp.

B2Gold had a solid quarter producing 224,000 ounces at an all-in cost of $1,100/oz. Guidance was maintained at low-cost Fekola in Namibia which is a cash machine. B2Gold generated $134 million in operating cash flow. Disappointing was B2Gold and joint venture partner AngloGold decision to scrap the Gramalote open pit project in Columbia because of a higher up-front capital cost despite a second look. Meantime B2Gold has 4 licenses and will process satellite deposits like Cardinal using Fekola’s infrastructure. B2Gold has a great balance sheet with $587 million and $600 million undrawn facility compared with $382 million last year. Management continues to be looking for M&A candidates, but to date it’s slim pickings. We like the shares here.

Centerra Gold Inc.

Centerra had a negative quarter after scrambling to replace production following the brutal nationalization of flagship Kumtor in the Kyrgyz Republic. Making matters worse was the shutdown of Öksüt in Turkey resulting in the stockpiling of ore and mining was curtailed with no indication as to when it will restart. Also Öksüt’s permits are at risk, following the mercury leak at the ADR plant leaving only the Mount Milligan mine in BC to support Centerra's operations which is not enough. Mount Milligan produced almost 43,000 ounces of gold in the quarter and 17 million pounds of copper while guidance is maintained at 190,000 to 210,000 ounces, Centerra has about $723 million on hand but few prospects. Scott Perry is to be replaced as CEO. We think there are better opportunities elsewhere.

Centamin PLC

Centamin had a great quarter and produced 111,000 ounces from Sukari, the largest mine in Egypt. The company spent $67 million on infrastructure including a paste fill plant and a 36 M-W off-grid solar plant and 7.5 MW battery facility which will come on in the third quarter. Centamin has no debt, no hedges and cash of $176 million. The company should produce about 445,000 ounces this year at an all-in cost of $1300/oz. Centamin’s underground grade has improved due in part to the switchover to owner operated mining from contract in the underground section. Of note is that the company has begun to spend money on exploration on their vast 3000 km2 license of highly prospective lands. We like the shares here and believe Centamin is a perfect takeover tidbit for one of the global players.

Eldorado Gold Corp.

Eldorado is a mid-tier player and had a disappointing quarter as costs at Lamaque and Olympias in Greece increased. The company reported negative cash flow of $63 million after spending $83 million, largely on Kisladaq in Turkey. Eldorado has about $370 million of cash and equivalents but will require more than a billion dollar to build out Skouries in Greece. As such, the company is looking for a joint venture partner or alternatives to finance Skouries. Eldorado has maintained guidance with Efemçukuru in Turkey having a strong quarter producing almost 23,000 ounces at a cash cost of $706/oz, in line with expectation. Lamaque in Quebec produced almost 47,000 ounces at a cash cost of $657 an ounce as drilling on Ormaque deposit will boost reserves, now that decline at Lamaque is complete. Eldorado’s Greek operations are a hidden asset but the company has yet to capitalize. As such, the shares are a hold.

IAMGOLD Corp.

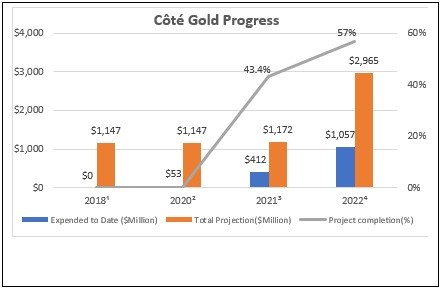

Data source: www.iamgold.com

¹2018 feasibility study projection. ²construction commenced in September 2020

³ Projection using upper projection scale. ⁴as at date May 1, 2022

IAMGOLD had a disappointing quarter but not surprisingly the cost of Côté Lake increased again with the price tag jumping to $1.3 billion, representing a more than 12 percent increase. Of concern is that the company is only now drilling at a tighter 10 x 10 spacing sharing our concern that the deposit was not properly drilled off. While Côté Lake is 57 percent complete, the heavy lifting is still ahead leaving a financing gap. IAMGOLD will need additional funds or outside financing to complete the project as the project’s cost has tripled since inception. Production hasn’t increased making the project a sink hole and company destroyer. Côté’s economics remain poor with an after-tax return of only 13.5% and yet still the company throws good money after bad. On a positive note, Essakane had a strong quarter and there was some improvement at Rosebel. IAMGOLD will likely have to sell Rosebel which is a drain on cash. Westwood, another drain only produced 14,000 ounces in the quarter. While IAMGOLD’s joint venture partner, Sumitomo has dilution rights, there is no indication whether Sumitomo will pay for its share or dilute, leaving IAMGOLD a bigger nut to finance. Given the cost escalation, Sumitomo might take a pass or, alternatively, wait for IAMGOLD to fail, picking up the balance for peanuts. Sell.

Kinross Gold Corp.

Kinross had a miss in the quarter due to problems with the mill ramp up at La Coipa in Chile. Also Kinross’ Round Mountain, Bald Mountain and Fort Knox are mature operations which did not do well. Tasiast had a better quarter with mill throughput at 21,000 tpd which accounted for the improvement despite lower grades. Kinross also shed light on Great Bear project in Red Lake Ontario where it is betting the farm and noted that production is targeted in 2029. Kinross is planning a 200,000 m drill program at a cost of $60 million to more properly drill off the deposit (needed in our opinion), a reflection that Great Bear is an early-stage exploration project. We believe Kinross jumped the gun in spending $1.8 billion without a formal reserve report which will only follow after this drill program. Kinross will need to spend at least $1 billion on Great Bear and won’t see a return until the next decade. In jumping the gun, Kinross may well have bit off more than they can chew. Kinross hopes that Great Bear will replace it's Russian assets which were given away for a paltry $340 million to Highland Gold in Russia and not $680 million as earlier reported. The Russian assets represented about 25 percent of Kinross’ cash flow, but Great Bear will not replace those assets. As such, we would sell the shares because there is little near term on the horizon.

Lundin Gold Inc.

The world’s richest gold mine, Lundin Gold had a strong quarter beating street guidance raising its production guidance and lowered costs at Fruta del Norte in Ecuador. Cash costs came in at $700/oz and AISC at $860/oz reflecting higher grades. Lundin generated positive free cash flow of $47 million with cash on hand at $300 million. The South Ventilation Raise (SVR) will be completed in the last quarter. Lundin will report the results from nearby exploration two priority targets at Barbasco and Puente-Princesa. We like the shares on a total return basis. Lundin declared a dividend of $0.20 semi-annually, returning capital to shareholders and an annual yield of 3%-4%. Buy.

McEwen Mining Inc.

McEwen Mining shares have been a disappointment due to problems at Gold Bar in Nevada and the Fox complex in Ontario. The processing problems appear resolved but carbonaceous ore at Gold Bar adversely affected output. However the second quarter results showed improvement as both operations made contributions along with San José in Argentina. McEwen produced 27,600/oz of gold and 704,600/oz of silver for a total gold equivalence of 36,000/oz. All-in costs went down in the quarter but remain high however. At the Fox complex, the company is spending $10 million on exploration on its vast lands. McEwen Copper, a subsidiary to be spun off has completed its $80 million financing with an investment by Rio Tinto and a team in place to put Los Azules into production on a phased basis. Los Azules is one of the top ten undeveloped copper projects in the world and a hidden asset in McEwen Mining. To keep its US listing, McEwen rolled back their shares on a 10 for 1 basis. We like the shares for McEwen’s development potential.

New Gold Inc.

New Gold had a disastrous quarter due to too much rain at Rainy River as well as lower grades from its stockpiles and increased costs at New Afton. Flooding at Rainy River resulted in the processing of lower grade material hurting cash flow with production off 33%. Consequently New Gold's production guidance was lowered as the company faces continuing challenges and increased costs. New Gold continues its losing streak, losing money mining on every ounce it produces. Sell.

Newmont Corp.

Newmont also had a disastrous quarter due to a dramatic increase in costs resulting in the lowering of guidance to 6 million ounces. Newmont produced 1.5 million ounces at AISC of $1200/oz. The restructuring of Goldcorp’s assets continues with the Pamour pit to be dewatered, Peñasquito labour costs have increased, and Cerro Negro remains challenging with $300 million of development costs. Continuing problems at Ahafo and open pit CC&V in Nevada also hurt results. Noteworthy is that the company reported $1 billion in operating cash flow and $514 million free cash flow. However Newmont also has hefty capital spending requirements at the Tanami expansion, Ahafo North as well as the huge Yanacocha sulfides project. The Yanacocha Sulfides will take three years to build at a capital cost of $2.5 billion. Newmont has 12 operating mines and two joint ventures and a base of 6 million ounces annual production. However in the near term, there is little upside so we prefer Barrick here.

Yamana Gold Inc.

Yamana produced 261,000 gold equivalent ounces in line with estimates of a stronger quarter from Jacobina. Free cash flow was disappointing at $58 million due to higher capex and taxes. At Wasamac, drilling and more work will be needed to update the feasibility study where capex is almost half a billion. El Peñón had a solid quarter but with output declining, Yamana has excess plant capacity and despite exploration, they have not been able to fill the gap. Desperate for reserves, South African miner Gold Fields bid a rich premium for a mature business promising to increase dividends to sway their own shareholders to okay the bid. However, Gold Fields will need a hefty 75% approval. We believe the deal will likely fail largely because Yamana's mines are mostly in harvesting mode except for Agnico Eagle’s Canadian Malartic joint venture. Ironically that acquisition weighed heavily on Yamana’s balance sheet, resulting in a capital constrained Yamana needing Gold Fields’ cash to develop its longer term projects. Sell. Take the money and run.

John R. Ing

********