Gold: A Lump Of Coal?

Source: WSJ

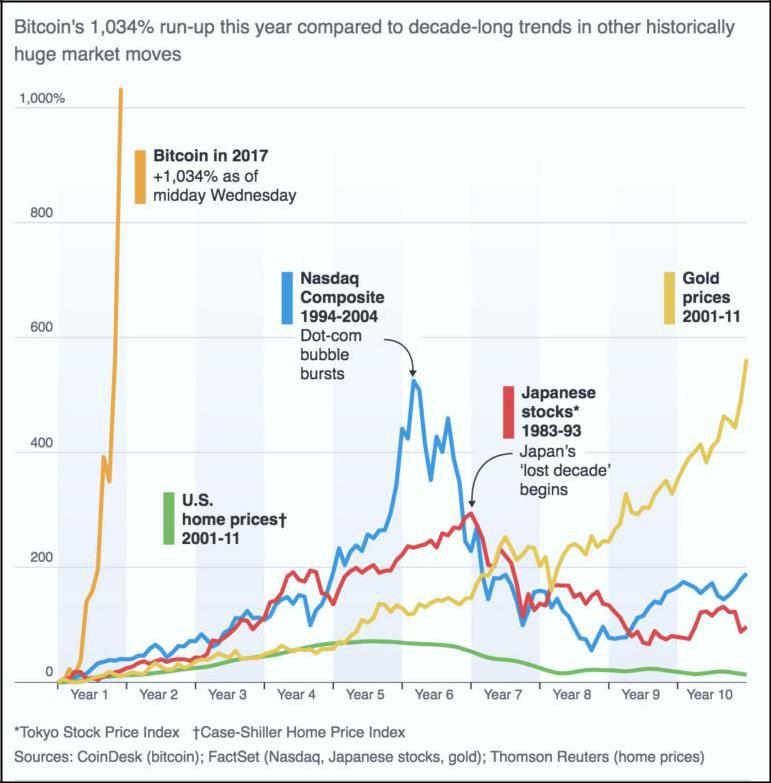

After a decade of monetary laxity, money and even bitcoins, fiat currencies have become a market commodity like tulips during the 1687 Dutch mania. Bitcoin has become an investment mania, made for the times and the craze has dwarfed the tech bubble. Who can trust the value today? Bitcoin or digital currencies are a man-made product created in minutes with a click. Like fiat money, there are no limits to production, no guarantor and consequently, of little lasting value. Ironically, undeterred by warnings that this electronic currency is a bubble waiting to be burst, bitcoin is a currency without a country. When investors can borrow to hedge bitcoins or when Wall Street creates the newest digital cyber-currency derivative, only then will we discover bitcoin’s intrinsic worth.

Debt, Deficits And The Dollar

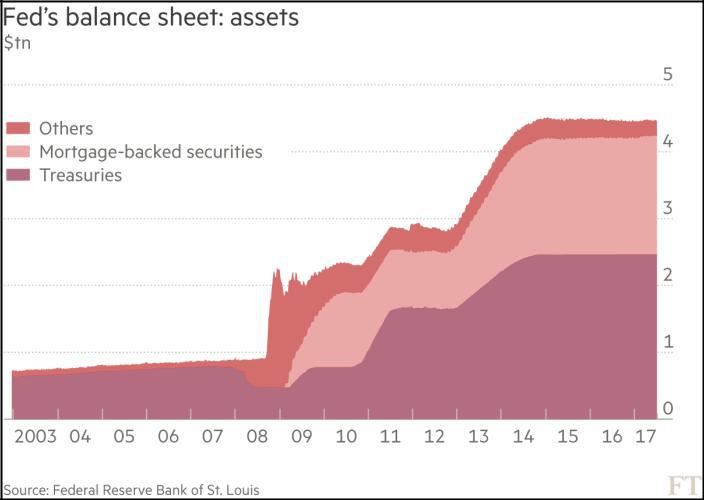

For almost a decade, central banks monetised their budget deficits to finance the government of which they are a part. Their monetary laxity financed the large part of America’s growing deficits via the expansion of their balance sheets through massive purchases of government securities. Rates remained at rock bottom as quantitative easing distorted market rates of interest. Since 2007, even the Fed’s own balance sheet increased four times to a whopping $4.5 trillion. After three

Rounds of quantitative easing, America has created the biggest bubbles in history, the largest being the debt bubble. Worrisome is that in becoming the largest debtor nation in modern history, any downturn in corporate profitability could be a disaster since the corporate world also is over-leveraged.

To date, the US benefited from this arrangement because they consumed more than they produce. For the rest of the world, they are now awash in dollars. The manufactured $10 trillion of central bank liquidity, born in the depths of the 2008 financial crisis has been the key driver pushing up asset prices to manic levels from bonds’ bull run to the subsequent record breaking stock market rally. Not a problem, until foreign investors and creditor nations decide to go on strike because they have too many dollars or,

Insulted by a tweet or gaffe, a Mueller charge, or the scrapping of another agreement, decides to retaliate and unload those dollars.

Debt is like cocaine. Today investors have become addicted. The Federal Reserve, responsible for credit creation has become the dominant player in the global financial system. Global growth and a decade of money printing has fueled a progression of mania or bubbles and demand for liquid dollar assets, from stock markets, da Vinci paintings, real estate to bitcoins, the bubbles have expanded in scope and risk. Some of the funds sloshed over to the corporate sector, funding buybacks, instead of investments or capex. Ironically, the tax reform bill will do little to repatriate the billions of oversea funds or stimulate capital spendings – instead there will be much more red ink despite pay-as-you-go rules. Debt cannot be solved with more debt.

Is It Different This Time?

Worrisome then is that in a world where everything looks expensive, investors’ search for yield has them taking on increased risk and leverage in order to boost returns. Central bank asset purchases also crowded out investors leaving them with riskier assets, distorting traditional valuation metrics. However, while record-breaking stock markets trumped fundamentals for investor attention, junk bond prices have collapsed and the sovereign debt market has swooned after Venezuela’s default inthe biggest sovereign default in history. As the central banks’ so-called “normalization” unfolds, we believe the first crack will surface in the debt market. Of concern, is that the present time is reminiscent of the months before the 2008 crisis. Housing is again in a bubble, Wall Street is caught up in its own rational exuberance and Americans do not save. It is not so different this time.

Central banks’ recent guidance to rein back on the monetary reins discloses an addiction to ultralow interest rates such that a backlash has them only gradually ending these programs.

Incoming Fed Chairman Powell has cautiously spoke of halving the Fed’s balance sheet and a “steady as she goes” approach. However, pulling the punch bowl away in the form of tapering or even unwinding the large scale purchases of financial debt, will in our opinion leave an impact on the economies’ liquidity and of course, higher rates and a reaction from of those addictive to liquidity.

A year after his election, President Trump remains controversial as ever. Much was made of the implications of America’s controversial choice, yet the stock market has given a resounding thumbs up with the S&P Index up 20 percent on hopes that Mr. Trump would be a good thing for the US economy. True that the economy is growing, albeit at the same pace under Obama. However, since his election, the market volatility index (VIX) has fallen to an all time low of 0.51 percent, the lowest since the early sixties. The lack of volatility could imply a bullish view that the economic recovery is growing amidst a global upturn. On the other hand, a low volatility index preceded the biggest financial correction in 2008, as investors believed then like now, that the benign conditions would prevail indefinitely in a “Minsky Moment”.

What Could Go Wrong?

Investors have taken for granted that whatever damage Mr. Trump’s unpredictable behaviour caused, the American system of checks and balances could overcome it. To date, they have been proven correct. However, Democrat successes in the November election and the overhaul of the tax code debacle has raised questions about this risky bet. US fiscal policy is the chief focus for most markets. High yield bond funds recently suffered the third largest outflow on record. The Treasury yield curve is the flattest in a decade, a condition that has inverted ahead of every US recession since the Second World War. Investors must decide whether these concerns are transitory or a warning of turmoil to come. And overlooked is what ballasts the US monetary system is debt. One of the biggest threats to an “America First” financial stability is the reckless build-up of debt. The delay of the tax cut is only the first of many disappointments. As a consequence, we expect a rethink about the US dollar, economy and of course gold, particularly when the debt ceiling comes up for discussion again as the government’s current funding expires in December.

So while the Trump “reflation” trade exists, we believe it is hanging by a thread. Amid the bluster, tweets and interventions, the greenback has weakened. We believe the recent sell-off in the US dollar reflects a growing uneasiness in the market with credit risk. And, as America turns inwards, the geopolitical climate and risk has become murkier from the Middle East (MbS’ Saudi Arabia) to Europe (Spain, Brexit,

a Merkel-less Germany) to Latin America (bankrupt Venezuela). Most worrisome is that the leadership vacuum has already changed the world order. Russia and China are attempting to fill the void left by America’s retreat. China’s Xi Jinping has elevated himself to rival only Mao as China’s greatest leader. From Europe to Asia to the Middle East, other countries have focused on

their priorities without US influence to limit their ambitions. The Saudi Arabia purge reflected 32-year-old Saudi Prince Mohammed bin Salman’s (MbS) move to consolidate his power, which could destabilize the Middle East. In addition, Trump’s brand of populism has spread from Austria to Italy to Turkey and worrisome is that Italian elections are looming next year. Even Berlusconi is staging a comeback.

Gold, The End Of Fiat Money

Gold is an alternate investment to the dollar for central banks. It is the rational solution to an excessive accumulation of dollars. The rise in the gold price can be seen as a devaluation of the dollar. The world is awash in dollars. The Fed ironically is the world’s biggest holder of gold, and while supplies of the metal are shrinking, America’s creditors are loading up on gold. If gold is a finite currency, its value against fiat currencies

like the dollar, euro, and even sterling must rise. Gold is thus an index of currency fears. In the last 50 odd years, more and more people have unsuccessfully looked for alternative stores of values and payment methods. Under fiat currencies, we have had a series of economic upheavals from the 2007–2009 crash, the Asian crisis, the Nifty Fifty collapse, the internet bubble and of course various European crises. It goes on with regularity. Without confidence in the dollar, there is no valid reserve currency.

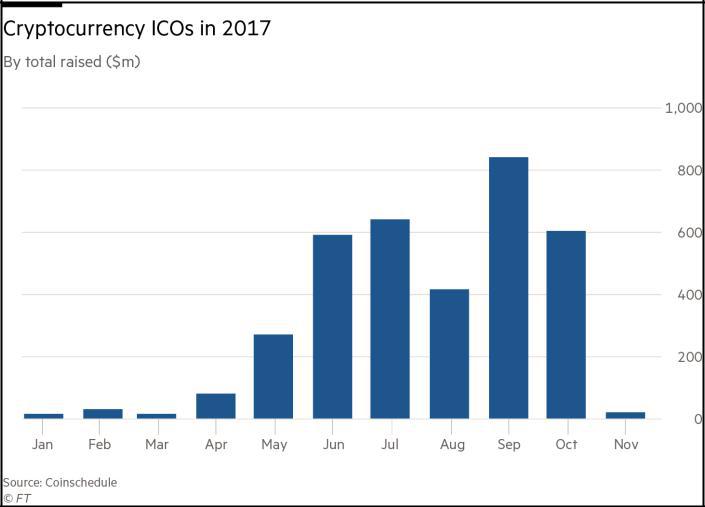

On the other hand, gold is a product that is thousands of years old, made by Mother Nature, and is both finite and inherently valuable. There was a time when gold was money. In today’s uncertain world, the cryptocurrency craze is a reflection of a market top in a mania-fueled world where bitcoin investment is matched only by the tulip bubble craze of 1600s. Gold is the real deal in an overvalued world. We believe the yellow metal will soon be back in fashion. Part of the allure is its traditional status as a safe haven against a world where there is quite a list of uncertainties and concerns. It is the ultimate store of value when everything seems risky.

Recommendations

Total above ground gold stocks in the world are small, at only 180,000 tonnes or less than one ounce per person in the world. Despite demand, gold remains extremely scarce. The largest share is held in jewelry form but the second largest is held by central banks. Global supplies have been squeezed with a decline in output from China, the largest producer in the world. China’s mines are expected to run out of reserves in the next few years, raising the possibility of a supply crunch particularly as Chinese demand grows even faster. China has become more open in its challenge to American financial hegemony, purchasing gold to become the fifth largest holder in the world. Russia too has made monthly purchases becoming the sixth largest holder in the world, declaring recently that any escalation of sanctions, which would freeze foreign accounts of the Central Bank of Russia, would be regarded as a “declaration of financial war”.

We believe it is the relationship between the dollar and the reaction of the world’s central banks of whom many are creditors to the US that is important. Gold’s biggest driver is a depreciating US dollar. The combined debt of governments, corporate and households are now 300 percent of global GDP. Many are still accumulating dollars that they do not want. Over the last decade, the Fed has created a risk of a sharp rise in American inflation and a precipitous collapse in the dollar.

Gold miners are facing an identity crisis. Some have written off billions of dollars and are still repairing their balance sheets. Others have made expensive acquisitions hoping that the increase in reserves would give them a growth multiple and a market following. Others however, have expanded their exploration budgets with hopes that acorns can grow into trees. However, it can take two to seven years to fully commission a gold mine from discovery to first gold pour, so that bet is for the very lucky and very patient. Moreover, the cost of extraction keeps on rising. To be sure, the lack of exploration and declining production suggests that gold supply is a major problem.

Technically, the group has been in a base building more for almost three years and recent activity suggests a breakout from a triangle formation. Fundamentally, cash costs have declined 20 percent from $1200 to under $1,000 an ounce, suggesting that the industry is at long last profitable. Of note is that the gold miners’ in-situ reserves are at the cheapest ever, trading under $300 an ounce on a market cap per ounce basis. We believe that in the near term, gold is headed for resistance at $1,375 an ounce which will support higher gold miner prices. We continue to believe gold will reach $2,200 an ounce within 18 months.

As such, we would emphasize Barrick for its 85 million ounces of reserves, Agnico Eagle for its growth profile and organic pipeline. We also like mid-tier B2Gold for its growth profile now that Fekola is in production. Among the juniors, we continue to recommend McEwen Mining as it brings Gold Bar in Nevada into production and down the road, exploit a fourth leg in Timmins through the acquisition of the Black Fox mine. We also think it’s time and thus financed some exploration vehicles like Aurania, Keith Barron’s newest company as he tries to discover another Fruta del Norte in Ecuador.

Agnico Eagle Ltd.

Agnico had a record quarter producing over 450,000 ounces at a total cash cost of $546 an ounce allowing the company to raise its dividend by 10 percent. Agnico also raised its production guidance for this year to exceed 1.6 million ounces. Of note, Agnico’s operating margins widened with record production from flagship LaRonde, mining below 3.1 km underground. Importantly the discovery of Whale Tail and Amaruq deposits extend the life of Meadowbank in Nunavut. We continue to recommend the shares here

B2Gold Corp.

B2Gold had a strong quarter with contributions from the Otjikoto mine in Namibia and Masbate mine in the Philippines. The improvement offset lower output from its Nicaraguan mines. Importantly, B2Gold commissioned Fekola in Mali ahead of schedule which will contribute 400,000 ounces next year at an all in sustaining cost (AISC) of around $600 an ounce. Fekola only took two years to build and will contribute to B2Gold’s 975,000 ounce estimated production next year from five mines pushing all in costs down below $800 an ounce. B2Gold has one of the best growth profiles among the gold companies growing from zero output to almost one million ounces in only 10 years. With the ramp up at Fekola complete, the company has boosted its exploration budget. We like the shares here

Barrick Corp.

Barrick had lower output due to the cessation of mining activity at 64 percent owned Acacia in Tanzania. Barrick generated free cash flow of $225 million in the quarter. Barrick’s core projects,

Lagunas Norte, Turquoise Ridge, Goldrush and Cortez Hills Deep South are expected to contribute more than 1 million ounces beginning in 2020. Barrick boasts the largest gold reserves in the world at 85 million ounces and does not have to explore for more ounces since its core development plans alone will replace reserves. Barrick has also begun a prefeasibility study for the underground development at Pascua Lama, under a deal with Chinese Shandong Gold. Barrick also reduced debt and the annualized savings on debt since 2015 are more than $300 million per annum. Barrick has a much-improved balance sheet sitting with $2 billion in cash and a $4 billion credit facility.

Barrick's focus on cash generation will allow it to finance the pipeline of core projects including Cortez Hills lower zone, which is 44 percent complete. In Tanzania, the company and the government have agreed to a framework agreement, handing over 16 percent of its mines for a 50/50 split and the payout of $300 million. The agreement hopefully ends an almost 9 month standoff with the government that stalled gold exports, but is dependent upon the granting of go-ahead permits allowing production, exports etc. Barrick also sold 25 percent of Cerro Casale to Goldcorp in a 50/50 joint venture. The huge project shifts a large part of the financial risk to Goldcorp allowing Barrick to extract some near term value for a long life asset that investors gave little value. We like this deal. We continue to recommend Barrick for one of the best quality collection of assets and having one of the best managements in the gold mining business. Buy.

Detour Gold Corp.

Detour’s mining rates improved in the quarter, with mill throughput at 61,500 tonnes per day, a record. However, production was lower due to lower grades. Total cash costs was $668 per ounce and all in cost at $1,032 per ounce mainly due to lower milling costs. Detour Gold is a low-grade open pit operation and thus grade is particularly important. Detour Gold expects to be mining higher-grade ore from the Campbell pit, which will boost results. We prefer Agnico Eagle here.

Eldorado Gold

Eldorado Gold shares plunged to 15-year lows on disappointment over the recoveries at flagship Kisladag in Turkey, which shocked investors. Because Kisladag is coming to the end of its oxide mine life, recoveries have declined sharply. Eldorado is contemplating high grade high-pressure grinding and conducting metallurgical tests to improve recoveries but have not yet completed work to recover output. Noteworthy, comparable milling facilities could cost $300 to $400 million so the heavy lifting has just begun. Meantime in Greece, the company received final permits at Olympias’ Phase 2 however, Skouries’ permits are overdue resulting in a construction hiatus. Skouries’ construction is 35 percent complete and the plant is at 54 percent completion but the halt will mean more delays. Consequently, Eldorado has again put the project on hold not wanting to spend more money until the government grants the permits.

In Canada, Eldorado is working on a prefeasibility study (PFS) at Integra’s Lamaque project in Québec as Eldorado seeks to diversify from its heavy exposure to Greece and Turkey where the outlook has dimmed. At Integra, underground development continues and the project could produce some 120,000 odd ounces annually over 10 years. While Eldorado has a strong balance sheet with liquidity of more than half billion dollars, the acquisition of Integra Gold is an expensive price to pay for a safe jurisdiction. To be sure, the exploitation of the Integra acquisition will stretch Eldorado's balance sheet. With the uncertainties of the Greek government permitting issues and Kisladag’s recovery problems, the shares have limited upside. However, longer term we think Eldorado shares have adequately discounted many of the problems and as a result is an attractive option on higher gold prices.

Goldcorp Inc.

Goldcorp had strong results producing 630,000 ounces at an all in cost of $827 per ounce. During the quarter, former flagship mine Penasquito in Mexico and newly commissioned Eleanore in Quebec improved. Goldcorp boasts proven reserves at 53.5 million ounces bumped up from newly acquired Cerro Casales joint venture with Barrick. Importantly however, the recent reserve additions reflect an expensive acquisition price and Goldcorp, still has to spend billions to exploit its reserve position. Meantime, at flagship Red Lake, Goldcorp is trying to extend its life. Also, the company is still working on a prefeasibility study at Century where continuity is a problem. While Goldcorp has a pipeline of projects which could bring 3 to 4 million ounces on stream, huge capex and sustaining capital for Coffee (cost $526 million), bringing on Dome – Century (Borden cost $526 million) and Cerro Casales (cost $1 billion) are in the billions. Until the dust settles, we prefer Barrick.

Iamgold Corporation

Iamgold Gold reported better results due in part to production from Essakane in Mali, which contributed about 93,000 ounces towards the 217,000 ounces, produced in the third quarter at an all in sustaining cost of $969 an ounce. Iamgold’s production guidance remains at 845,000 ounces to 885,000 ounces for 2017. Iamgold’s flagship Rosebel produced 75,000 ounces in the third quarter at an all in cost of $900 per ounce and hopes to extend its life with nearby discovery Saramacca which contains one million ounces at higher grades at 2.2 grams of gold per tonne. Iamgold was fortunate to salvage a joint venture with Sumitomo for Côté Gold whose original price tag was a whopping $600 million. A feasibility study is to be completed by the first half of 2019. Delineation drilling has already started which in our opinion is needed since our belief that the deposit was not drilled properly. However, the mine won’t be in production until 2021 at the earliest. We prefer B2Gold here.

Kinross Gold Corporation

Kinross had an excellent quarter due to improved output from Tasiast in Mauritania and from its Nevada mines, which generated about $320 million of adjusted operating cash flow. Also a strong performance from Kupol in Russia contributed to the results. Kinross’ balance sheet is strong at $1 billion of cash with totally liquidity of $2.5 billion, required for the proposed buildout of Tasiast Phase 2, and Round Mountain Phase W. Kinross produced 654,000 gold equivalent ounces in the third quarter. Importantly, at Paracatu, sufficient rainfall in late October allowed the resumption of operations and the reprocessing of tailings, which contributed 47,000 ounces in the quarter. Under normal rainfall conditions, one of the largest mines in Brazil could produce some 500,000 ounces, so water management is a key here. In Russia, the mine produced 146,000 ounces at a cash cost of $524 per ounce due to higher grades.

McEwen Mining Inc.

McEwen Mining had mixed results due to a mechanical failure at the El Gallo Mine in Mexico. Also in Argentina, poor weather and lower grades contributed to San José’s lower results. McEwen closed their $30 million strategic acquisition of the Black Fox mine, which brought in facilities, a mine and $150 million of tax pools which allows McEwen to exploit subsidiary Lexam’s reserves. McEwen completed a detailed PEA at Los Azules in Argentina, which is a long life copper project. During the first 13 years of production, average output is projected 415 million pounds of copper at an average production cost of $1.14 a pound. However, Azules requires a healthy $2.4 billion so the big project will likely require partners. Nonetheless, we believe Los Azules is not reflected in McEwen's stock price. Meantime at flagship El Gallo in Mexico, mining is taking place in the

deeper portion with better grades. McEwen will bring on Gold Bar in Nevada to replace declining oxide output from Mexico. Progress is substantially advanced and engineering is more or less completed. At Black Fox, McEwen is processing low-grade stockpiles but the intention is to exploit Lexam’s Timmins properties and ship to the 2,400 tpd mill, making it McEwen’s fourth mine. We like the shares here for its growing profile and debt-free balance sheet. Maison recently participated in the last underwriting.

New Gold Inc.

New Gold is an intermediate player, producing 82,000 ounces from New Afton, Peak and Cerro San Pedro. However, Peak Gold in Australia was recently sold for $58 million. Trouble prone Rainy River was finally commissioned and the Ontario mine is more or less complete. However the balance sheet has been stretched by the build-out, cost overruns and delays. While New Gold only has about $200 million in cash, some $73 million is left on their credit facilities, the sale of Peak will help Rainy River until it is in full production. Cash costs at Rainy River is high but as production increases next year, the cost should come down. Blackwater (100 percent owned) is New Gold's next big project, but the inevitable start-up problems at Rainy River and capex must be addressed before Blackwater could be considered. We remain on the sidelines here.

Newmont Mining

Newmont had a good quarter with production from newly commissioned Merian and Long Canyon offsetting mature operations like giant Yanacocha whose oxide life is winding down. However, Newmont generated nearly $500 million in free cash flow, double the previous year. The performance reflects the harvesting of some of its assets allowing Newmont to retire $575 million of convertible notes, further improving its stellar balance sheet. Newmont has total liquidity of nearly $6 billion and net debt to EBITA at only 0.4 times. Of interest is that 70 percent of Newmont's production comes from the United States and Australia. While, Merian and Long Canyon were small contributors, Newmont ambitiously hopes to add 1.7 million ounces annually from nine projects over the next few years financed internally and with cash flow. Barrick with more reserves is a better buy here.

Yamana Gold Inc.

Yamana had a strong quarter producing 257,000 ounces of gold and 1.4 million ounces of silver from six mines. Yamana increased the guidance for silver and for copper. Yamana’s results were assisted by contributions from Chapada and Jacobina. Nonetheless, debt reduction was a key factor since the company is saddled with a whopping $1.6 billion of debt from acquiring its half of Canadian Malartic. Yamana also hedged putting in gold and copper collars. We would avoid this debt-loaded player.

John R. Ing