Gold Mid-Tiers' Q4'21 Fundamentals

share

share

share

share

share

share

share

share

share

share

The mid-tier and junior gold miners in their sector’s sweet spot for upside potential have powered higher in recent months. Amplifying gold’s young upleg, they have already surged to major breakouts. And the smaller gold miners’ gains are likely to grow much larger. Their recently-reported Q4’21 earnings season revealed ongoing strong fundamentals. Those along with inflation-driven higher gold prices will fuel big buying.

With Q1’22 already winding down, looking at the prior quarter’s operational and financial reports seems dated. But because most companies run on calendar years, the Q4 reporting deadlines are extended. In the US companies don’t have to report full-year 10-K results until 60 days after quarter-ends, compared to 40 days for 10-Q quarterlies. In Canada, the epicenter of the gold-mining universe, year-ends extend to 90 days!

So late March is about the earliest that enough mid-tier and junior gold miners have reported their full Q4 results to analyze them. Right after each quarterly earnings season, I dig into the latest reports from the top-25 component companies of the excellent GDXJ VanEck Junior Gold Miners ETF. With $5.1b in net assets midweek, this is the second-largest gold-stock ETF after its big-brother GDX major-gold-miners one.

Gold-stock tiers are defined by their production rates. Small juniors mine less than 300k ounces of gold annually, medium mid-tiers have outputs running from 300k to 1,000k, large majors yield over 1,000k, and huge super-majors operate at vast scales exceeding 2,000k. The mid-tiers offer a unique mix of sizable diversified production, good output-growth potential, and smaller market capitalizations ideal for outsized gains.

Mid-tiers are much-less-risky than juniors, and amplify gold’s uplegs much more than majors. Despite its name, GDXJ is overwhelmingly a mid-tier gold miners ETF. While it started out as a true junior one, that market alone proved too small to absorb the big capital inflows GDXJ attracted. I analyzed that evolution in depth in previous essays in this deep-research thread, which has been running for 23 quarters in a row now.

Speculator and investor interest in these smaller gold miners is mounting after GDXJ’s big 30.8% surge between late January to early March. But that only amplified gold’s parallel upleg in that span by 2.1x, which is weak for these high-potential stocks. Mid-tiers and juniors need herd sentiment to shift to bullish on gold, which only happens after it has rallied high enough for long enough. That key inflection point is nearing.

Much to its managers’ credit, GDXJ continues to improve. Unlike GDX, GDXJ isn’t saddled with the huge dead-weight super-majors unable to grow their production. GDXJ is far-better-diversified too, with its top-25 holdings only accounting for 61.4% of its total weightings mid-week compared to 88.5% in GDX. While handpicked fundamentally-superior individual stocks will easily best any ETF, GDXJ is the cream of the crop.

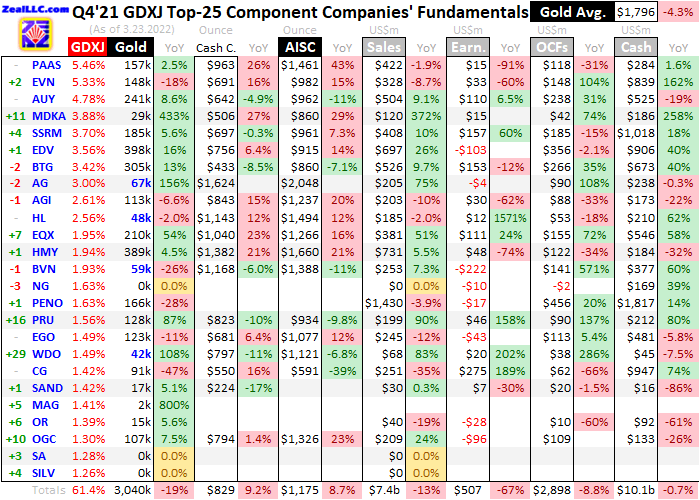

This table summarizes the operational and financial highlights from the GDXJ top 25 in Q4’21. These gold miners’ stock symbols aren’t all US listings, and are preceded by their rankings changes within GDXJ over this past year. The shuffling in their ETF weightings reflects shifting market caps, which reveal both outperformers and underperformers since Q4’20. Those symbols are followed by their current GDXJ weightings.

Next comes these gold miners’ Q4’21 production in ounces, along with their year-over-year changes from the comparable Q4’20. Output is the lifeblood of this industry, with investors generally prizing production growth above everything else. After are the costs of wresting that gold from the bowels of the earth in per-ounce terms, both cash costs and all-in sustaining costs. The latter help illuminate miners’ profitability.

That’s followed by a bunch of hard accounting data reported to securities regulators, quarterly revenues, earnings, operating cash flows, and resulting cash treasuries. Blank data fields mean companies hadn’t reported that particular data as of the middle of this week. The annual changes aren’t included if they would be misleading, like comparing negative numbers or data shifting from positive to negative or vice versa.

The elite mid-tier and junior gold miners filling GDXJ’s upper ranks generally reported good results last quarter, despite lower average gold prices. Fundamentally these smaller gold miners well-outperformed the major-dominated GDX stocks in Q4’21, a bullish omen. The entire gold-stock sector is set up for far-greater gains as gold powers higher on this raging inflation unleashed by the Fed’s epic money printing.

Like most exchange-traded funds, GDXJ is essentially market-capitalization-weighted. That’s the most-logical way to construct ETFs, reflecting relative capital amounts traders have deployed in component stocks. But shifting market caps continually alter ETF-component weightings and rankings, mixing up the bottom end of the GDXJ-top-25 stocks. This past year’s striking changes really affected data comparability.

Since Q4’20, two explorers have charged up into these rarefied ranks. Seabridge Gold has an incredible monster gold deposit, but may never build a mine after long decades of milking investors to pay corporate salaries. SilverCrest Metals also has no production, but is successfully making the rare transition from explorer to producer. It is constructing a nice new silver-and-gold mine scheduled to come online in Q2’22.

Traders bidding up these explorers’ market caps knocked out actual gold miners IAMGOLD and Fortuna Silver Mines from the GDXJ-top-25 ranks since Q4’20. Another mid-tier gold miner, the British Centamin, was displaced by the ascent of the tiny gold streamer Osisko Gold Royalties. These big composition changes in the GDXJ top 25 leave its aggregate Q4’21 data much-less-comparable to Q4’20’s totals than usual.

After decades of intensely studying and actively trading gold stocks, I’ve never understood the obsession with royalty and streamer companies. Their stocks are radically-overvalued, with high market caps way out of line with their meager underlying gold outputs, revenues, and earnings. Fundamentally nearly all the royalty and streamer plays are wildly-overpriced, way inferior to actual gold miners generating big profits.

In addition to these market-cap-driven component changes, GDXJ’s managers also made a big and very-welcome one. For years one of this “Junior Gold Miners” ETF’s largest components was Gold Fields, a South African super-major miner. In Q4’21 alone it produced a staggering 631k ounces of gold! A year ago in Q4’20 it mined 593k. Such a colossal gold miner belongs in GDX alone, it never should’ve been in GDXJ.

Gold Fields was finally booted out of GDXJ over this past year. But its massive production, sales, profits, operating cash flows, and cash hoard greatly boosted Q4’20’s GDXJ-top-25 totals. So it really needs to be excluded from that comparable quarter to get a clearer fundamental picture of how mid-tier and junior gold miners are faring. Thus adjusted Q4’20 means without Gold Fields, IAMGOLD, Fortuna Silver, and Centamin.

Last quarter these GDXJ-top-25 gold miners collectively produced 3,040k ounces of gold, which plunged 18.6% year-over-year. But that was heavily skewed by those four companies being included in Q4’20 but not Q4’21. Excluding them, these elite mid-tier and junior gold miners actually grew their total output an impressive 5.6% YoY! That crushed the GDX majors’ 6.2%-YoY shrinkage to 8,352k ounces of Q4’21 production.

Yet GDXJ and GDX actually have large overlap in their holdings. These GDXJ-top-25 stocks were mostly clustered between the 13th-to-35th-largest rankings in GDX. GDXJ effectively lops off the dozen biggest GDX stocks dominated by super-majors, then greatly expands the weightings of the rest. These GDXJ-top-25 stocks accounting for 61.4% of this ETF also currently comprise 18.6% of GDX’s total weightings.

I just analyzed the GDX-top-25 stocks’ Q4’21 resultsin last week’s essay if you want to compare their holdings or performances. Fully 12 of these GDXJ-top-25 stocks are also GDX-top-25 ones! I’ve long argued GDX and GDXJ holdings should be mutually-exclusive, leaving more-distinctive gold-stock ETFs that would better serve traders. But the gold-stock universe is likely too small to make that work for GDXJ.

Whether mid-tiers or true juniors producing less than 75k ounces per quarter, fully 3/5ths of the GDXJ top 25 reported higher production in Q4’21. The handful of actual junior primary gold miners have production highlighted in blue. With more exposure to smaller mid-tier and junior gold miners, GDXJ’s usefulness for traders continues to improve. It has way more upside potential during gold uplegs than major-dominated GDX.

Unlike the majors simply too big to grow fast regardless of how well they are managed, the mid-tier and junior gold miners are coming from much-smaller bases. These sweet-spot-for-upside-potential mid-tiers usually have a few mines or less, so expansions and new mine builds really boost their outputs. And the mid-tiers also have way-smaller market caps, making their stock prices far-more-responsive to capital inflows.

When mid-tiers’ lower production and market caps are combined with leveraged profits growth from higher gold prices, their upside potential during big gold uplegs trounces that of the majors. So the mid-tiers are easily the best gold stocks to own as this secular gold bull continues marching higher over coming years. Their future gold-production growth will far exceed the majors’, and their earnings aren’t done soaring.

Long-term gold-stock price levels ultimately depend on miners’ profitability, which is directly driven by the difference between prevailing gold prices and gold-mining costs. In per-ounce terms these are generally inversely proportional to gold production. That’s because gold mines’ operating costs are largely fixed during planning stages. Their designed throughputs limit the amounts of gold-bearing ore they can process.

That doesn’t change quarter to quarter, and requires about the same levels of infrastructure, equipment, and employees. The only real variable is the ore grades run through the fixed-capacity mills. Richer ores yield more gold ounces to spread the big fixed costs of mining across, lowering unit costs which boosts profitability. With adjusted production surging, the GDXJ top 25 should’ve reported lower unit costs in Q4’21.

Cash costs are the classic measure of gold-mining costs, including all cash expenses necessary to mine each ounce of gold. But they are misleading as a true cost measure, excluding the big capital needed to explore for gold deposits and build mines. So cash costs are best viewed as survivability acid-test levels for the mid-tier gold miners. They illuminate the minimum gold prices necessary to keep the mines running.

These elite mid-tiers’ and juniors’ average cash costs actually surged 9.2% YoY to $829 per ounce last quarter. While worse than expected, that is still better than the GDX top 25’s crazy 21.8% catapulting to an even-higher $853! Most of the GDXJ-top-25 gold miners were operating at much-lower cash costs than that $829 average implies. That was skewed way higher by extreme outlying costs from a couple stocks.

For years the major silver miners have been increasingly diversifying into gold, as it simply has far-better mining economics. Last year First Majestic Silver acquired its first pure gold mine to add to its stable of silver ones, but that has been plagued with super-high costs. Harmony Gold Mining’s old and very-deep South African mines are ever-more-expensive to run. Excluding these, GDXJ-top-25 cash costs averaged $750.

All-in sustaining costs are far superior than cash costs, and were introduced by the World Gold Council in June 2013. They add on to cash costs everything else that is necessary to maintain and replenish gold-mining operations at current output tempos. AISCs give a much-better understanding of what it really costs to run gold mines as ongoing concerns, and reveal mid-tier gold miners’ true operating profitability.

The GDXJ-top-25’s AISCs also surged a similar 8.7% YoY in Q4’21 to $1,175 per ounce, the highest on record! Again the smaller gold miners outperformed the bigger ones, with GDX-top-25 AISCs coming in up a hotter 14.5% YoY to a slightly-higher $1,188. Also again the GDXJ-top-25 AISCs look better if those super-high-cost operations of First Majestic and Harmony are excluded, averaging a much-milder $1,090.

But mining costs naturally creep higher during secular gold bulls, where rising prices make less-economic gold deposits mineable. Q4’21 was the 15th consecutive quarter where GDXJ-top-25 AISCs climbed on a year-over-year basis! The preceding four quarters saw them surge 11.5%, 11.2%, 12.8%, and 14.9% YoY, so Q4’21’s 8.7% jump was actually a moderation. Even $1,175 remains far below prevailing gold prices.

Those averaged $1,796 last quarter, slumping 4.3% YoY. The difference between quarterly gold prices and gold-mining AISCs offers a great proxy for mid-tier and junior profitability. That implies these GDXJ-top-25 gold miners earned $622 per ounce in Q4’21. Although that did fall 21.9% YoY, it was still better than the GDX-top-25 majors’ $608 that dropped 27.5% YoY. And unit earnings still remain high absolutely.

Q4’21’s $622-per-ounce sector mining profits are the seventh-highest on record after the preceding six quarters’. Those averaged $741, a stark contrast to the mere $413 average in the dozen quarters before those. Despite higher costs and lower gold prices, the mid-tier and junior gold miners continue to earn money hand-over-fist. And their earnings are poised to surge back higher in this current almost-done Q1’22.

Gold’s $1,873 average price so far this quarter is 4.2% better than Q4’21’s. It is already the third-highest ever witnessed, and should still be able to usurp Q4’20’s $1,876 to take second! And mid-tier AISCs are expected to flatten from here. Fully 17 of these GDXJ-top-25 miners gave full-year-2022 AISC guidance that averaged $1,165 per ounce. Q1’22’s $1,873 average gold less $1,165 AISCs would yield fat $708 profits!

Gold stocks amplify material gold upside so effectively because their earnings greatly leverage higher prevailing gold prices. If the GDXJ-top-25 gold miners pull in $708 per ounce this quarter, that would rank as their fourth-highest quarterly unit earnings ever. The last time this metric came in over $700 was back in Q4’20, when mid-tier and junior gold stocks and GDXJ itself were trading way up at much-higher prices.

Gold itself will almost certainly power way higher too. The reason even lowballed headline-CPI inflation is soaring 7.9% YoY is extreme Fed money printing. In just 24.6 months since March 2020’s pandemic-lockdown stock panic, the Fed ballooned its balance sheet by an absurd 115.3% or $4,796b! Effectively more than doubling the US money supply conjured up far more dollars to compete for and bid up price levels.

During the last similar inflation super-spikesin the 1970s, gold prices nearly tripled during the first then more than quadrupled in the second! The gold miners’ stocks shot stratospheric on that, generating life-changing wealth for contrarians deployed in them. Gold has always been the ultimate inflation hedge, as its supply growth is hard-limited by geology unlike fiat-money supplies. Gold-stock earnings amplify gold gains.

On the hard-accounting front, the GDXJ-top-25 gold miners’ total revenues fell 13.0% YoY to $7,435b. But when adjusted for those four producers included in Q4’20 but now replaced with non-mining explorers and royalty companies, overall sales actually grew 6.6% YoY. That’s again much better than the 5.7%-YoY revenues decline reported by the GDX top 25. The mid-tiers and juniors are fundamentally-superior.

Yet in Q4’21 their bottom-line accounting earnings under Generally Accepted Accounting Principles or other countries’ equivalents looked ugly. They plummeted 67.2% YoY to $507m, or 59.2% against that adjusted Q4’20 total! But this was heavily distorted by unusual items, one-off things flushed through income statements like mine impairments and impairment reversals. I always look for any larger ones.

Last quarter saw plenty of big unusual items, which netted out to offsetting another $446m of net income! That slashes the YoY decline in GDXJ-top-25 operating profits to 38.4% absolutely or 23.3% adjusted for those four companies. Q1’22 earnings should look much better, as managements often dump things like mine-impairment charges into Q4 results. Those are forgotten by the time year-end bonuses are calculated.

With weaker accounting profits, mid-tier and junior gold-stock valuations in classic trailing-twelve-month price-to-earnings-ratio terms shot up to 62.5x. That was an anomaly mostly driven by two outliers with extreme P/Es though, another explorer transforming into a miner MAG Silver and Hecla Mining. Without their 100x+ P/Es, the rest of the GDXJ top 25 averaged just 27.7x. Gold miners are generally undervalued.

With way-fewer estimates distorting operating cash flows than earnings, the former often provide a clearer picture of how gold miners’ businesses are actually doing. The $2,898b total OCFs reported by these elite mid-tier and junior gold stocks fell 8.8% YoY absolutely, but climbed 11.3% when Q4’20 is adjusted. Those fed fat cash treasuries totaling $10.1b, tying a record high for the GDXJ top 25 despite composition changes.

That slumped 0.7% YoY absolutely, but soared 27.7% when those four companies are removed from the comparable Q4’20. The mid-tier and junior gold miners will use those big cash hoards to grow their future production. They will continue expanding existing mines to boost their outputs, developing new mines, and buying other mines and sometimes entire companies. Such projects are underway at many of the GDXJ top 25.

The smaller gold miners are also prime acquisition targets for the majors, since those perpetually struggle to offset ongoing depletion from their large-scale operations. Building occasional new mines isn’t enough either, so most of majors’ growth comes from buying out entire mid-tier and junior gold companies. Those offers usually come at nice premiums, offering more upside for contrarians deploying capital in these stocks.

If you regularly enjoy my essays, please support our hard work! For decades we’ve published popular weeklyand monthlynewsletters focused on contrarian speculation and investment. These essays wouldn’t exist without that revenue. Our newsletters draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks.

That holistic integrated contrarian approach has proven very successful. All 1,280 newsletter stock trades realized since 2001 averaged outstanding +20.7% annualized gains! Today our trading books are full of great fundamentally-superior mid-tier and junior gold and silver miners to ride their uplegs. These stocks have surged with gold breaking out, but still have massive room to run. Subscribe todayand get smarter and richer!

The bottom line is the mid-tier and junior gold miners in the sweet spot for stock-price upside potential just reported another strong quarter. Their adjusted production growth surged, far outperforming the majors’ drop. And these smaller gold miners still earned fat profits, despite rising mining costs and lower average gold prices. Those earnings will soar back higher in this current quarter on better gold levels and stabilizing costs.

The mid-tier and junior gold stocks still have lots of catch-up rallying left to do, both to reflect their superior fundamentals and this mounting gold upleg. That is destined to grow far larger too, as gold prices nearly tripled and more than quadrupled during the last similar inflation super-spikes in the 1970s. That naturally launched gold miners’ earnings and stock prices stratospheric, generating fortunes for contrarian traders.

Adam Hamilton, CPA

Copyright 2000 - 2022 Zeal LLC (www.ZealLLC.com)

*********

share

share

share

share

share

More from Gold-Eagle