Gold Miners Are In Trouble…Is There A Way Out?

It is said that gold miners are in a “sunset industry,” as they fight for their very survival. Is there any hope left? I would reason that it is possibly the “darkest before the dawn,” there is light and these are the reasons why.

My last articles focused on physical gold and its role in our economy. I have strongly advocated that the best way to protect oneself against the ravages of inflation and the potential stock market loss through a correction, is to hold some physical gold as your “insurance.”

Furthermore, I indicated that between 5 and 10% of one’s portfolio should be invested in gold, of which the majority should be in Krugerrands, and that only the assertive investor should place a small portion of his assets in gold shares (the gold mines with their gold resources are still in the ground).

The definition of a “sunset industry” is, “An older industry that continues to be important to an economy but is losing favour with investors due to its steadily falling employment generation capacity and profits, and comparatively higher environmental costs.” This describes the gold mining industry perfectly.

Let’s then attempt to go underground and see how we can find out more about the gold mining industry. In particular, the gold that still needs to be discovered (exploration), proven by geologists, and then to build a mine on how best to access the ore body and deliver it for its pouring.

Why should one have avoided investing in South African gold mine companies?

-

The gold miners sector has had a notorious track record of underperforming the rest of the stock market.

-

South African mines future has been unclear up to now, due to the delayed revision of the much needed Mining Charter for clarity.

-

This month the new Mining Charter was published. Regarding ownership of the mine it was previously 26% of the mine that needed to be owned by BEE candidates - “Previously disadvantaged people.” The percentage for new mining licences has increase to 30%.

-

The High court was approached for clarity on the matter of “once empowered always empowered,” should owners sell their shares. The Court ruled that there must always be “a recognition of previous transactions.”

-

Labour strikes hold the miners to ransom demanding higher wages and benefits.

-

In the event of a mining accident, government shuts down the mine until a full investigation has been made. These delays lead to further financial loses.

What are the positive attributes of investing in the gold mines?

-

In the 1970’s gold mining made up 25% of South Africa’s GDP, its profits made a meaningful contribution to the coffers of the country, it benefitted all concerned.

-

Gold miners have been traditionally a big employer and therefore helped alleviate the unemployment problem.

-

South Africa is known to have the best gold resources in the world. Unfortunately they are very deep and therefore not feasible to mine at the present low prices.

-

If the gold price were to rise significantly, then South Africa is well positioned to benefit from this opportunity.

-

There is a leveraging effect when the gold price increases. That means that the basic costs to mine gold remain the same, but as the gold price increases, so the profit margin escalates significantly, which translates into a far higher share price.

What does the Industry say about itself?

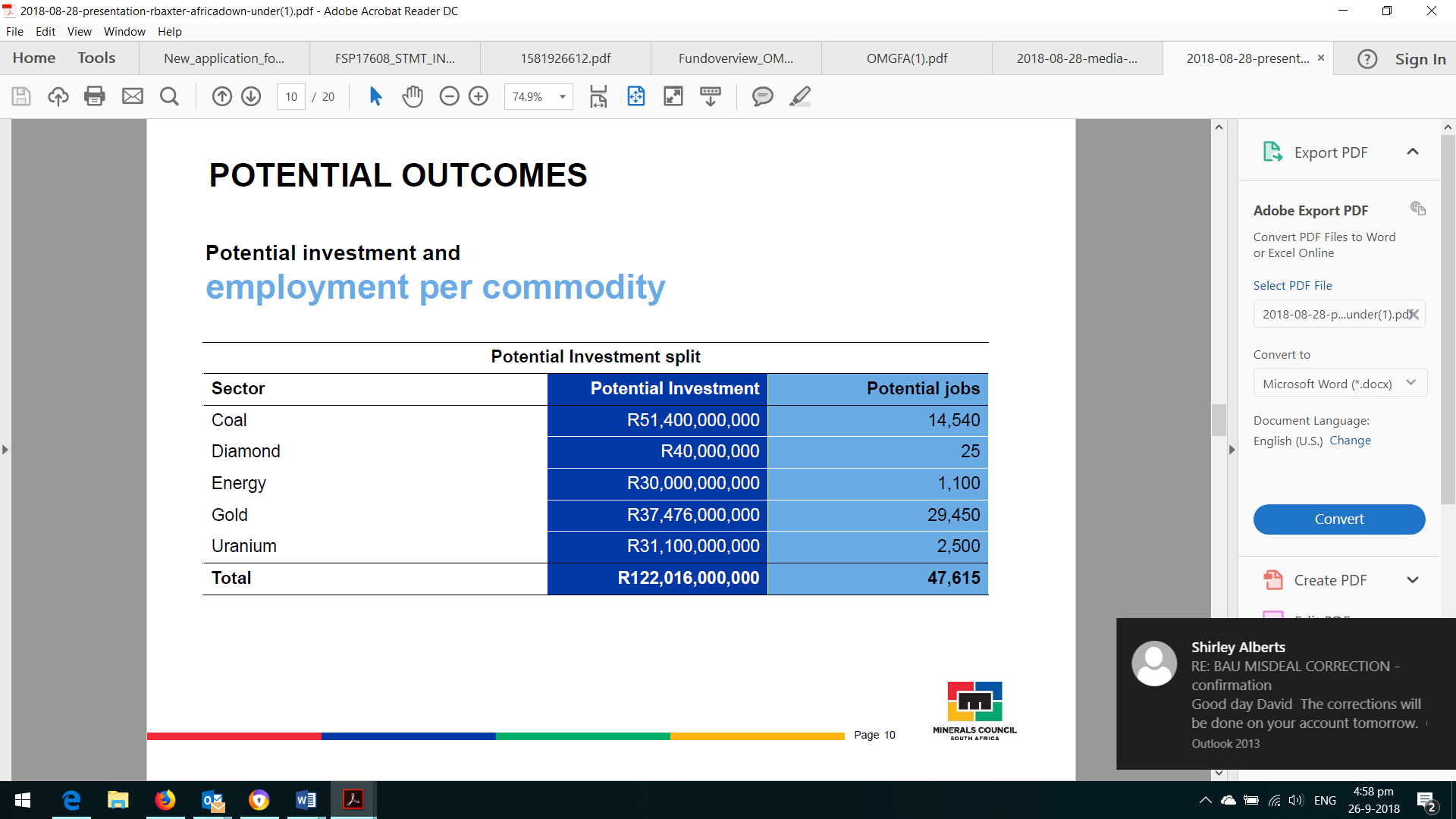

Roger Baxter, the Minerals Council CEO, recently presented at the Africa Down Under conference in Perth, Australia. (By the way the long standing Chamber of Mines has rebranded itself as the Mineral Council South Africa).

Baxter stated: “South Africa’s mining potential is huge. Even in the absence of a Greenfields exploration boom in South Africa, mining investment could almost double in the next four years if the country was to return to the top 25% of the most attractive mining investment destinations worldwide.”

He went on to say, “This would result in another 200,000 jobs being created in the economy with 50,000 direct jobs created in mining alone … the mining industry would be in a better position to increase its contribution towards infrastructure development and social projects in mining-affected communities. Given the industry’s commitment to real transformation, this would also materially advance the entire country’s transformation agenda.”

From his slide presentation one is able to deduce that the gold miners will benefit the most. They will add 29 000 jobs directly, this is more than double the next best, the coal miners will employ, and their investment capital expenditure requirement is 40% less.

Why is the Mineral Council so upbeat?

They have constructively engaged with all stakeholders. They see the strategy which is necessary in order to enable the South African mining industry to realize their potential. Roger Baxter outlined the key requirements:-

-

A shared Vision of the future of the mining industry;

-

Ethical leadership and good governance;

-

Policy and regulatory certainty and competitiveness;

-

Infrastructure that is available, efficient, cost competitive and reliable;

-

Improving productivity and competitiveness; and

-

Creating a “greenfields exploration boom.”

What grounds are there for hope at the country level?

Baxter points out that under President Ramaphosa’s last six months of rule there have been a number of reforms and changes to address State Capture, rooting out of corruption and getting the economy back on track.

The appointment of key cabinet ministers such as respected Gwede Mantashe as the minister of Minerals, and trusted ministers: Pravin Gordhan and Tito Mboweni the ministers of economics and finance respectively.

There are still thorns amongst the green shoots

The President does need to spell out clearly his understanding and policy of his proposed Land expropriation without compensation.

The Revised Mining Charter has long been under review and was published last month in the government gazette. This now gives a much needed consensus on the way forward. The revisions are positive. It appears to be a win for all concerned. It will thus advance transformation of the industry and also facilitate growth and development.

Who are the South African gold miners?

In the 1970’s when gold was booming in South Africa, there were over 50 gold companies listed on The Johannesburg Stock Exchange, today they are a mere six actively traded companies.

In order of size, they are AngloGold Ashanti (43%), Goldfields (25%), Sibanye Gold (16%) and Harmony Gold (11%). The two small companies are Pan African Resources (3%) and DRD Gold (2%).

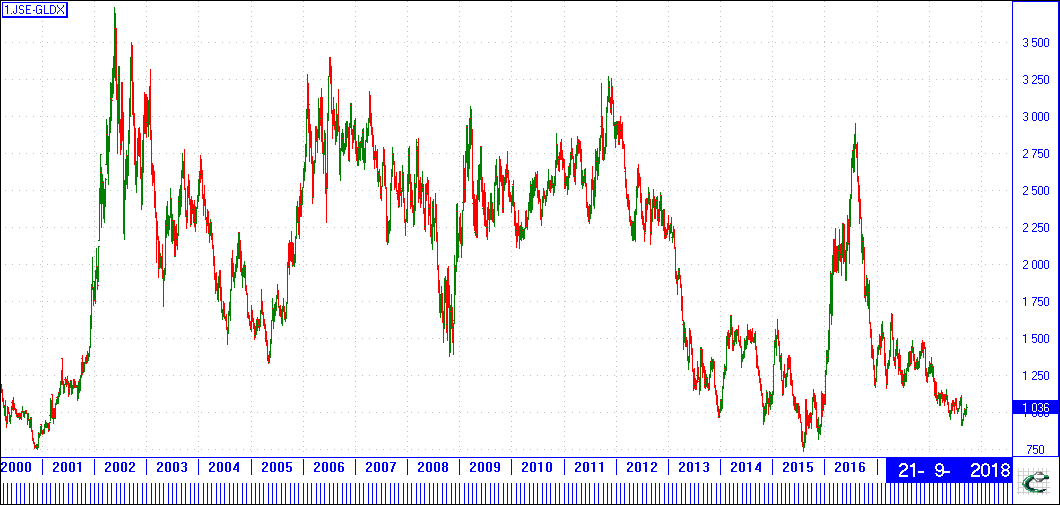

The chart of the Gold Miners below represents their performance. The net effect is that the index is back to where it was when it started some 18 years ago, at the turn of the millennium.

While there have been some favourable times, one has only made money if you traded the portfolio. A “buy and hold strategy” has been very painful.

The chart shows that the gold index has been as high as 3 600 points, today it is merely keeping its head above 1 000 points. That is 70% off its high.

Were there better times for miners?

Yes there were indeed. My first encounter with gold shares as a young boy was in the 1970’s. I remember excitedly catching the train during the school holidays to visit a large departmental store, Garlicks, in the city of Cape Town, for lunch. It was a lavish lunch sponsored by our great aunt. We made this family outing at least twice a year. Her father had left her a portfolio of gold shares, these paid handsome dividends. We were the willing recipients of these windfalls.

In 1967, the Mint Refinery and the Reserve Bank of South Africa teamed up to launch the production and sale of the one ounce Krugerrands. It was an extremely successful endeavour and as a result some 60 million plus Krugerrands circle the globe today. Many countries have followed suit.

At the pinnacle of the gold era in 1980, gold reached its high of $850 an ounce. At that stage the Rand was at parity to the dollar, or even a little stronger. That made gold then R850 an ounce too.

Today gold is barely up at $1230. That is up a mere $380, or 45% over the marathon time frame of 38 years. Fortunately the rand has substantially weakened and it is now R14 to the dollar. That translates into around R 17 000 an ounce of gold, or 20 times more than what it was then. That is significant growth. Yet despite this and allowing for inflation, South African gold miners are battling to make a profit.

What caused the gold price to decline?

I am not exactly sure, but I do know of three key factors that would have played a major role. Firstly, the US hiked interest rates to a record 19% per annum to entice investors to part with their gold. It was too good an offer to refuse. Enough investors surrendered their gold and elected for the cash in the bank. This put pressure on the gold price as demand weakened.

As a direct result of falling gold prices in the 1990’s, many gold miners made use of hedging. This meant they sold their gold forward, they received the cash upfront at a predetermined price and delivered the gold later. It had the benefit of securing that the mine could operate and remain in business, they could fund all their ventures and keep their staff compliment. The downside was that they arranged their own demise as the price was controlled and systematically forced downwards.

Another factor was the fact that Central Banks for at least ten years were net sellers of their gold held on their balance sheets. Consequently supply was greater than demand and the gold price fell to its all-time low of $250 in Dec. 2001. The United Kingdom was the big seller here, as they disposed of half of their assets at rock bottom prices.

In this difficult period South Africa largely stopped exploring and developing new mines. Their focus moved to outside of South Africa. They went from the world’s leading producer up until 2006, to now only rank as the eighth biggest producer.

In their peak production in the 1970’s they produced more than 1 000 tons per annum, now they barely produce 140 tons. But this could change very quickly, if the issues can be resolved and the doors to growth are flung wide open again for investors.

Will the gold price ever rerate again?

It would appear that we may be in a sunset industry. Yet there are early signs of recovery. Oil is known as the “black gold.” It has rallied from its low of $30 to over $80 a barrel. Could this be a leading indicator of recovery in the resource sector?

Because of the low price of gold there has been very little investment spent on exploration. We were involved with the first gold mine to be built in South Africa in 30 years, Gold One.

It was a very profitable gold mine because its assets were shallow, only 500 meters deep. In addition it was easy to mine. Costs were amazingly low, around $500 an ounce. It was not long before the Chinese first acquired a strategic stake and then ultimately made an offer to buy out all the other investors.

It may just be that when the gold price does run there will not be sufficient supply because of the lack of new mines being built. This of course may cause the price to run a lot quicker and higher as a result of short supply.

We need to see the gold price rise significantly for a new era of gold to be heralded in.

There are a few writers forecasting that the world’s monetary system has not been fixed since the Financial Crash of 2008, if anything it is broken. If this should transpire to be correct, it could cause a rapid hike in the gold price. There are some credible analyst forecasting a gold price as high as $ 10 000. One of them is Jim Rickards, a highly respected gold analyst.

How best to buy the gold miners?

As can be gleaned from the long term chart above the gold miners have all been beaten up, there are no exceptions. There are a variety of gold mines all with different aspirations. Considerations would need to made by weighing up where one sees gold being best mined, familiarizing oneself with the management team overseeing it, as well as establishing their strategy on going forward.

AngloGold Ashanti, the biggest miner, has the majority of its assets overseas and has chosen to be very well diversified in different continents.

Goldfields split its company into two parts, electing to hold most of its assets offshore, except for South Deep in South Africa, which has the second biggest known resources in the world.

All its other South African assets were hived off into the new gold company, Sibanye Gold, and later Sibanye-Stillwater. Sibanye Gold performed well initially, but lately it has given a lot of its profits back largely due to huge offshore acquisitions in a United States company called Stillwater. It is a palladium and platinum producer. In addition, they have acquired more platinum assets in South Africa. The mining group is well managed by Neal Froneman; he pioneered Gold One, and he has a proven track record of running a mine successfully.

Harmony Gold’s mines are exclusively in South Africa, although they are busy with a long term development project in Pappa New Guinea. As a result, they perform best when the rand weakens.

Pan African Resources is one of the two junior miners, they are re-mining the old mines in Mpumalanga towns, such as Barberton, where the early finds of gold were made. Methods of extracting gold from the ore body are very much more enhanced since then.

Lastly, there is DRD Gold, it focuses on reworking all the mine dumps. Much of the gold was not well extracted in the early days, so these are value hills that are reworked. The processing cost is much cheaper than mining gold. They together with Harmony will also outperform the other mines if the rand were to weaken.

What about the Old Mutual Gold Fund?

As to be expected the Old Mutual Gold Fund has bitterly disappointed. Over 10 years it has performed at -5% per annum return. It holds the top five South African gold miners (70%) as well as six global gold miners (30%) in its holdings.

Up until recent times it held a big exposure to platinum, and would therefore have best been described as a Precious metals fund. With the platinum price falling significantly from $2 300 an ounce to the present price of barely above $800, it suffered far more than the gold mining sector. Fortunately they are out of their platinum exposure and are now fully gold focused.

Their biggest foreign gold miner is Randgold Resources. There is a $6 billion, all-share merger between Barrick Gold and Randgold Resources that has received shareholders’ approval. This will create a global gold giant that will dominate the African gold industry.

Meryl Pick, has managed the Old Mutual Gold fund for the last three years. She is fully invested in gold shares and does not hold the Gold ETF. She remains optimistic about the gold price, as she rightly believes there is a high correlation between the gold price and the dollar: “We should see the gold price strengthen on the back of the weakening dollar,” she says, “… that may not happen straight away, but we are getting closer.”

The fund is known as the highest risk sector because it is so specialized. The fund fact sheet recommends that your investment time horizon should not be less than five years.

If the gold mining sector is about to come out of its slumber, then maybe it is a good time to invest while its share price is still desperately low. Those long term holders of the fund may yet be handsomely rewarded for their patience in not giving up.

The Old Mutual Gold Fund chart above illustrates that the price is rising towards the 200 day moving average (red line) – it will need to break through this barrier to be convincing.

What happened to the gold miners in the Great Depression years?

Lastly, let’s briefly examine a “worst case scenario” – the terrible crash of 1929 – that led to the Great Depression. The Dow Jones (the top 30 US Industrial companies) fell almost 90%. The Index went roughly from 400 to 40. It was the most devastating collapse ever. It took a mammoth 25 years to recover.

At the time there was a gold mining company known as Homestake Mining. It was the first listed mining company on the New York Stock Exchange (and it also became the longest listed company on the Exchange in its history).

Its share price did the exact opposite of the Dow Jones. If one had had 10% exposure in it, one would have made up your losses. This illustrates the value of having at least 5 – 10% of one’s investable portfolio in gold exposure. Gold is countercyclical in its nature.

The US stock markets continue their longest term ever of a Bull trend (10 years). There are dangers and investors would be well advised to protect themselves by purchasing some “insurance” through gold exposure.

The long term trend (30 years) of gold in Rand terms is intact.

In conclusion, if the gold mining sector in South Africa is finally poised to turn around because of a favourable Mining Charter that helps all stakeholders benefit from the rich resources in the ground, as it paves the way for development and growth, then maybe now is a good time to start investing into South African gold mines again.

We see that gold shares are extremely cheap, their prices are back where they were in 2001/2. The evaluations are excellent and relative to other assets such as stocks and the Bond market, the gold miners are offering superb value. This has got to be one of the best buying opportunities in many years.

A prudent investment portfolio may look something like this in the present times: 60% in equities, 30% in cash, and 10% in gold.

Suggestion: The best advice is to discuss your personal needs and your appetite for risk with a good investment advisor before investing.

David Melvill ~ FSP No 17608

+27 23 614 1215 - +27 83 284 2202

Brandy Hall 45 Long Street, Montagu, South Africa 6720

*********