Gold: The Never Normal

share

share

share

share

share

share

share

share

share

share

Alternate facts or reality have become part of our daily lives such that there is an indistinguishable blurring between the two worlds. In the fantasy world of the metaverse, people or their avatars are spending ever greater portions of their lives on online communities where people can work, learn, play and even shop. Reality to some has become so stifling that a seamless virtual make-believe universe is more appealing. Another reality exists in the fake news/misinformation /disinformation which is causing a deterioration in democracy in the world. The metaverse is somewhat different, more like an artificial digitized state of human activity but rather than reality, the user can choose a virtual reality which has its roots in the evolution of radio to movies. Often real money changes hands with games, NFTs, work and stocks in a virtual boom, all unregulated and sometimes untethered from reality. Gaming revenues today are bigger than global box office receipts.

Typically the big tech giants like Meta (formerly Facebook) and Microsoft have jumped on board providing the digital bricks needed to enable the virtual world. The numbers are sobering. Microsoft is buying video gamemaker Activision Blizzard in a whopping $75 billion deal. Metaverse hardware from headsets to smart glasses is produced by Apple or Sony capitalizing on the newest thing. Japanese and Korean companies are in the forefront using gaming, headsets, and entertainment as a way to open up the metaverse. Today, the internet is populated with virtual traders, or bots and platforms feasting on the booms and busts. Some investors no longer wanting to face the highs, lows and potential losses of the stock market or Bitcoin (a money alternative), have satisfied their gambling instincts in the more comfortable cyberworld of the metaverse. Virtual reality has become genuine reality for some, and alternate facts, alternate reality.

The Never Normal

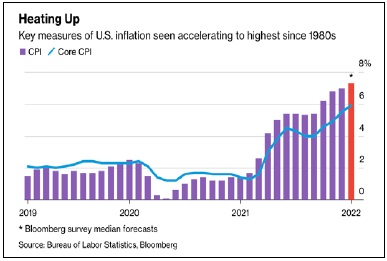

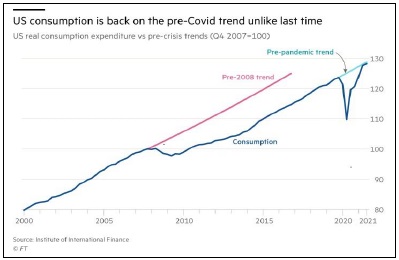

While the stock market last year made daily highs owing to widespread stimulus measures, the alternate reality is different. Two years into the pandemic, we are still coping with Covid-19 and its variances and in the United States, 60 million or a quarter of the population has been infected with its variants and a death toll approaching 1,000,000, according to Johns Hopkins University. Omicron is spreading like wildfire, faster than climate change with its wildfires, heatwaves and floods. Despite trillions spent on vaccines, ppe, medical innovations and that most countries are close to full vaccination, Covid-19 cases continue to surge. And inflation, the worst in forty years, threatens to go higher. Nonetheless it is far from certain that governments have a creative plan to tackle these problems as fiscal and monetary policy continues easing. Amid the Covid-19 disaster, there is a schizophrenic US with a foreign policy dominated by the Afghanistan retreat and locked in escalating tensions with China and Russia. Domestically Mr. Biden is at odds with his own party, failing to get his Build Back Better bill or filibuster bill passed. What happened to government’s commitment to order and good governance? What happened to Biden’s FDR moment? Mr. Biden’s approval has sunk to a dismal 33%. Mr. Biden is making the GOP great again. He might want a different reality.

In fact, Biden’s economic and regulatory agenda is partly to blame for accelerating inflation and fall in the polls. His voting rights bill is stalled in the Senate. His signature climate change and social policy Build Back Better plan would have raised taxes and fed a growing deficit at a time when both the pandemic and inflation are felt by every American. Surging Omicron cases are only a small part of the equation. And still, the world’s most powerful central bank is flooding the economy with money even though economic growth and inflation is much higher.

In fact, Biden’s economic and regulatory agenda is partly to blame for accelerating inflation and fall in the polls. His voting rights bill is stalled in the Senate. His signature climate change and social policy Build Back Better plan would have raised taxes and fed a growing deficit at a time when both the pandemic and inflation are felt by every American. Surging Omicron cases are only a small part of the equation. And still, the world’s most powerful central bank is flooding the economy with money even though economic growth and inflation is much higher.

The US Federal Reserve’s spending increased 54%, reminiscent of the 1970s when inflation took off as easy money led to increased leverage and inflated stock prices. Policymakers then as now believed the upsurge was temporary. President Gerald Ford too blamed Wall Street, issued WIN (Whip Inflation Now) buttons and imposed draconian price controls. Mr. Biden also believes that inflation is temporary but persists in stoking the inflationary fires, spending unprecedented sums to keep the economy from free-falling during Covid. The parallels do not stop there. Like the seventies, energy prices have skyrocketed but not because of OPEC but because of Mr. Biden’s regulatory heavy hand which has blocked exploration, development and even the construction of pipelines, which resulted in shortages, elevated demand and much higher energy prices. Some things stay the same. As before Mr. Biden blamed everyone including OPEC, corporate America, the food cartels and even Big Oil. Oil prices now seem headed for US 100 bbl. And yet Mr. Biden’s solution is to spend more money to end inflation. The consequence of all this is higher debt than before, higher prices, and bigger government.

High Cost of Climate Change

Also feeding persistent inflation areMr. Biden’s environmental policies which blames dirty coal for global warming and despite adopting much stricter government regulations, local state politics and culture helped boost US coal production by 17% in 2021, putting the US further off course in meeting its zero emission goals. Meantime “greener” natural gas production fell 3% causing prices to skyrocket, sending electricity prices to near records. Although the greening of America has led to big spending, renewables only make up about 20% of US electricity needs, insufficient to satisfy their voracious energy appetite. Thus there still will be the need for fossil fuels, nuclear energy combined with a stable energy supply during the decarbonisation transition, so costs will keep heading higher. Moreover, the building of more electric vehicles (EVs) domestically will push demand for already scarce critical metals of which the US must import from China and others. After all this, CO2 emissions last year climbed 7% to a record high, despite trillions being spent. The reality is that government’s environmental policies can’t suck and blow at the same time.

Shortages and high energy prices will persist making inflation worse this time as climate obsession and the winds blow through global capital markets driving lending and investment out of fossil fuels and into renewables in the effort to wean the world from fossil fuels. True, fossil fuel is a factor in global warming but not the factor or only factor. Investment in fossil fuels as a result has fallen sharply but consumer demand hasn’t. Consequently, energy prices are skyhigh as renewables have been found to be unreliable. Natural gas prices are up 850%. Consumers are bearing the brunt, paying higher energy bills and higher taxes. Government policies to incentivize electric vehicles (EVs) also boosted demand for critical supplies of lithium, copper, and nickel needed to make the batteries, putting energy transition at risk. Inflation also hit the general car industry which has become like fossil fuels, the lightning rod for climate change. In addition, resilient consumer demand and chip shortages caused used car prices to jump a whopping 45% last year. While billions of subsidies and incentives are spent, it does not match the reality that transportation only makes up 11% of global emissions. The reality today is that despite billions spent on subsidies and new technology, electric vehicles make up a paltry 8.6% of the new car market. So much money, too few results.

Shortages and high energy prices will persist making inflation worse this time as climate obsession and the winds blow through global capital markets driving lending and investment out of fossil fuels and into renewables in the effort to wean the world from fossil fuels. True, fossil fuel is a factor in global warming but not the factor or only factor. Investment in fossil fuels as a result has fallen sharply but consumer demand hasn’t. Consequently, energy prices are skyhigh as renewables have been found to be unreliable. Natural gas prices are up 850%. Consumers are bearing the brunt, paying higher energy bills and higher taxes. Government policies to incentivize electric vehicles (EVs) also boosted demand for critical supplies of lithium, copper, and nickel needed to make the batteries, putting energy transition at risk. Inflation also hit the general car industry which has become like fossil fuels, the lightning rod for climate change. In addition, resilient consumer demand and chip shortages caused used car prices to jump a whopping 45% last year. While billions of subsidies and incentives are spent, it does not match the reality that transportation only makes up 11% of global emissions. The reality today is that despite billions spent on subsidies and new technology, electric vehicles make up a paltry 8.6% of the new car market. So much money, too few results.

America at War, with Itself

And a full year later, Trump and the Republicans continue the Big Lie, an alternate reality that the election, the core of democracy was stolen, and the January Capital riot was simply a “legitimate political discourse” or a patriotic demonstration of their rights. And worrisome is that despite the Capital riot was backed by heavily armed citizens, polls show it was supported by some 20-30 million Americans. The attack hasn’t really ended. Ahead of the upcoming 2024 election, Mr. Trump and his acolytes have placed “friendlies” in state legislatures, governorships, news organizations and even the courts because who counts the votes matters more than the actual votes. The untruths go beyond one self-absorbed man. At one time the size of government and conservative principles were the base of Republicans but today it consists of an alternate reality of the Big Lie, conspiracy theories, and false claims like President Obama’s birth certificate. Ominously the last election was just a dress rehearsal for what is to come. Mr. Trump this time, will be more organized, more determined and more dangerous. That is not an alternate reality.

A Washington Post – University of Maryland poll showed 70% of Republicans believe that the Capital siege was “justified”, which is in sharp contrast to only 23% among Democrats. Fully 70% of Republican voters believe the election was stolen. Meantime, Mr. Trump seems to live in a reality of his own making, from the fake world of reality television to the fact that he believes he is still president. In fact, Mr. Trump and his acolytes have become permanent features of the American scene and despite a history marked by three presidential assassinations, a civil war, endless battles and now a messy retreat from Afghanistan, America is a country at war with itself. What is clear is that there are deep divisions among the American people. A year ago, Mr. Biden promised to restore unity and civility and today democracy itself is at risk. The mistrust, however is not limited to Mr. Biden, but all leaders, and rather than stick to the facts, an alternate reality of cheap rhetorical excesses and hyperpartisan has become the rule of the day. The threat to democracy is real, not an alternate reality.

What Is The Reality?

With 70% of Republicans believing the last election was a fraud, Mr. Biden can do little to sway the American voter making the November midterms problematic. At home, he is politically fragile. Overseas he has taken on Russia and China and only months after retreating from Afghanistan, the market fears that he might send troops into Ukraine, or Taiwan. To be sure the upcoming election in 2024 will be waged under the shadow of Mr. Trump. If the Republicans win, Democrats can counter that they too suffered injustices and will dispute the outcome. If the Democrats win, we get a replay of 2020. That is the future of American politics. Moreover, at a time of deep divisions, battle lines have hardened between the two parties and there seems no middle ground. Wearing a mask has become a political statement. With deep divisions, part of the problem is that bipartisanship is part of the past. But what are those divisions about? Immigration is a big factor among Republicans, economic insecurity is another. Covid real or not is another. Among progressive Democrats, who were on the sidelines for so long, political revolution is an issue. Since these issues were around the last election, alienation has exacerbated the agenda. Then there are changes in the electoral process as numerous states used their powers to change voting rights whilst Mr. Biden’s voting rights bill is stalled in Congress. Today, a major part of the American population feels frustrated and disenfranchised. With the polarisation affecting every democratic institution, distrusted and under siege by some segment of American society, election integrity will be paramount. As the Capital riot showed, violence is often a last resort. A similar frustration, alienation and polarisation is not confined to the United States. In Canada, the Canadian truckers’ “Freedom Convoy” protest against Covid measures has spread nationally and globally to other national capitals and still occupies the nation’s capital in a standoff. Prime Minister Trudeau’s dismissive response was that the protests undermine democracy and the police responded by issuing hundreds of traffic tickets.Who knew that Canada’s truckers would show up the ineffectiveness of government when it is time to take action on reopening the economy. That is a reality.

The Fed Is Part of The Problem

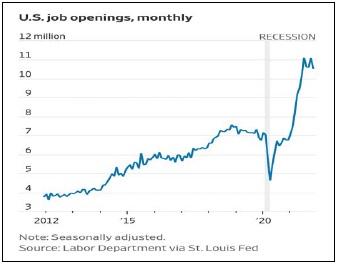

The government has pumped massive amounts of money into the economy to combat the pandemic recession. At the same time the Fed also pledged to keep monetary policy expansionary until full unemployment was reached. What is full unemployment? Labour markets are tight. Employers added almost 500,000 jobs, despite millions out sick. A host of data shows that labour markets are already behaving in late-cycle fashion with sharp drops in unemployment and a huge number of unfilled jobs. Besides, millions aren’t working either to care for someone or are sick themselves. Also with high quit rates and as much as 20% of American income coming from government benefits (ZIRP, PPP, CTC), subsidised workers stayed home. A decline in immigrants, legal or otherwise compounded the problem. Of concern is that at 4% we are at or near what was once considered full unemployment, a level reached in the Great Inflation period of the late 1960s and 1970s. The Fed’s inaction is noteworthy allowing Mr. Biden to pile on the stimulus, encouraging consumers to spend more on imported goods while exports lag, resulting in a trillion-dollar trade deficit for the first time ever. Why this matters is that to finance the deficit, the Fed’s balance sheet has grown 10 times larger than the 2008 financial crisis and much of America’s debt to pay for that surge in consumer spending is owed to foreigners. The only thing transitory is the Fed’s usage of that word.

The government has pumped massive amounts of money into the economy to combat the pandemic recession. At the same time the Fed also pledged to keep monetary policy expansionary until full unemployment was reached. What is full unemployment? Labour markets are tight. Employers added almost 500,000 jobs, despite millions out sick. A host of data shows that labour markets are already behaving in late-cycle fashion with sharp drops in unemployment and a huge number of unfilled jobs. Besides, millions aren’t working either to care for someone or are sick themselves. Also with high quit rates and as much as 20% of American income coming from government benefits (ZIRP, PPP, CTC), subsidised workers stayed home. A decline in immigrants, legal or otherwise compounded the problem. Of concern is that at 4% we are at or near what was once considered full unemployment, a level reached in the Great Inflation period of the late 1960s and 1970s. The Fed’s inaction is noteworthy allowing Mr. Biden to pile on the stimulus, encouraging consumers to spend more on imported goods while exports lag, resulting in a trillion-dollar trade deficit for the first time ever. Why this matters is that to finance the deficit, the Fed’s balance sheet has grown 10 times larger than the 2008 financial crisis and much of America’s debt to pay for that surge in consumer spending is owed to foreigners. The only thing transitory is the Fed’s usage of that word.

In addition, the rip-roaring bull market fueled by the Fed’s money printing has created more rich multi-billionaires and trillion-dollar corporations (Apple’s market cap is $3 trillion) than ever. Government today is bigger not smaller. Booming asset prices has benefited the rich who now occupy government. It does not help that some of the most powerful lawmakers on Capitol Hill recently resigned over possible conflicts of interest, trading while in possession of material non-public information, despite their conflicted position. As for the so-called independent Fed, a trading scandal had three of its senior officials resign, tarnishing the Fed’s independent reputation, resulting in an overdue review of trading – but after the horse left the barn.

Self-Inflicted Vulnerabilities

The new reality is that both parties blame globalisation for America's problems. However in the last two decades, globalisation helped the world economy prosper as different players in different countries took advantage of their own strengths and niches. China went from the workshop of the world to its capital provider. Russia is an energy powerhouse, becoming Europe’s biggest supplier of energy. Economic inter-independence helped build the global supply chains which became value changers over the two-decade period. Tariffs were reduced and leveled the playing field. Consumers were the prime beneficiary of lower prices. In fact, the pandemic is a good example of how globalisation worked with the American, German and British vaccine makers spreading their goods and vaccines globally to the benefit of all. Importantly no tariffs were added to these vaccines in the worst pandemic in a century. The tragedy is that the benefits of globalisation were poorly understated and that under Trump and now Mr. Biden, America has turned inward leaving others to fill the vacuum.

So, buffeted at home and with a divided Congress, President Biden has set his sights on foreign policy. After leaving a vacuum in the Middle East which allowed his cold war opponents to outflank America by filling the vacuum, Joe Biden has escalated tensions with Russia while the cold war with China festers. Within days of a messy withdrawal from Afghanistan, the opportunistic Chinese signed deals with the Afghanistan government to secure critical commodities ironically also needed in the greening of America. And then while attention was on Ukraine, Russia outflanked America using its gas resources as an energy weapon exposing Europe’s heavy dependence on Russian gas. The Russian threat to weaponize energy has forced the West to scour the globe looking for surplus gas supplies. Yet when the sabre-rattling hit American consumer gas prices, he was the first to ask Moscow and the Saudis for help, which of course was refused.

The new world order sees Russia and China demanding a central role based on distinct spheres of influence. The Saudis, Russia, and Europeans are lining up visiting Beijing, offering goods, services, and even drones. China is one of Russia’s largest natural gas buyers as the Ukraine crisis tightens the Moscow-Beijing bond. In addition to commodities, the Chinese are using its markets as political tools, upending the market once driven by basic supply/demand. Putin’s success in Kazakhstan and Belarus has kept those countries within Russia’s orbit without a shot being fired and is a major step towards Putin’s end goal of re-establishing the Soviet Union and Moscow’s sphere of influence.

The pickup in geopolitical tensions, climate change and the self-inflicted energy vulnerability of the West has undermined America’s hegemony. Moreover Biden’s retreat from globalisation has resulted in spiralling energy prices, hurting American consumers in the pocketbook. Similarly, Europe too is vulnerable and because of their heavy reliance on Russian natural gas, face much higher gas prices on top of soaring bills particularly if Russia squeezes supplies in response to Western sanctions. The run-up in energy prices helped make Russia the largest gas producer in the world. The approval of the recently completed $11 billion Nord 2 Stream gas pipeline is an ideal bargaining chip since Europe relies on Russia for 40% of their gas imports. Then there is Germany which ironically shutdown their nuclear reactors, making them more reliant on Russian gas, potentially splitting the Western alliance’s unity. While nuclear has a 25% share in the US, there is no uranium production currently in the US and thus they are dependant on uranium imported from the former Soviet Union, including Russia and Kazakhstan.

The Forever Pandemic

Two years ago, few had heard of Covid-19 or thought that not one but a number of different vaccines would work. Now the coronavirus and its fourth or fifth variant have already killed more people than those who died in World War II. But unlike the war, it has not gone away. In a country where the Covid-19 death toll has already surpassed the number of fatalities than the 1918 flu, life is considered back to normal. Yet the economic toll keeps mounting. Although much time and money was devoted to vaccines with huge success in shortening the interval from “lab to jab”, the creation of mRNA platforms is a modern-day accomplishment raising questions as to why more should be spent on therapeutics (treatment), particularly given America’s low vaccination rate and dysfunctional public health institutions. Or, after the epic shock, why haven’t we more vaccines or, a national programme for the next virus or, a plan for recovery?

Of concern is that the pandemic is now in its fourth wave, exacerbated by a large contingent of anti-vaxxers, and anti-maskers. A look back at two of the most important global pandemics, the Black Death in the 14th century and Spanish Flu in 1918 gives clues as to what is to come. The Black Death killed about half of Europe’s population or 75 million people. In 1918, HINI flu virus infected nearly one third of the world’s population and killed 50 million. And yet the virus is still with us today (in the US 35,000 people die every year from this variant). Importantly both led to huge socio-economic changes, wealth distribution and political change. And, because the death rates were so high, a good percentage of the population was lost, such that labour became tight so wages went up. Also, governments borrowed to cushion their economies from the shock and, like wars the pathogen fight caused countries to go deeply into debt. Savings too increased and interest rates stayed low for decades. After the Spanish Flu, then, as now there was relief and celebrations paving the way for the Roaring Twenties and the hangover, the Great Depression which took generations to recover. We may have been done with Covid-19, but Covid-19 is not done with us.

Today we too are fighting a long war against inflation and Covid-19. It might take generations to recover. As with other pandemics, the world is learning to live with Covid-19, just as we learned to live with the flu or HIV. Vaccines will help, but we will be dealing with Covid-19’s aftermath for years, maybe decades. This never normal will likely see more boosters, more vaccines and treatments. However all will cost money. In fact, none of this will generate new money. As before, today governments borrowed trillions to combat Covid-19 and worrisome has become more than a health crisis, it is a debt crisis, a debt pandemic.

Debt Pandemic

Moreover there is the alternate reality of the Federal Reserve, rather than a steward of money became a creator of money, aiding and abetting government’s spendthrift ways. Fed Chair Powell earlier said the surge in CPI inflation at 7.5%, the largest jump in 40 years was transitory and not of the Fed’s doing, but more of a supply/demand mismatch caused by the pandemic. Mr. Powell now believes differently, showing naïve ignorance in the consequences of the Fed’s unprecedented programme of reducing rates to near zero and monthly purchases of $120 billion of government debt would lead to higher inflation. The good news is that the Fed finally recognizes the inflation problem.

The bad news is that Fed policy is still stimulative and on track to remain so, while the supply of government bonds keeps expanding to fund the mountain of debt. US money supply rose 8% in January. The Fed is part of the inflation problem. We believe years of quantitative easing and MMT was the major factor in causing inflation to run at the fastest pace since the seventies, exacerbated by the pandemic stimulus. Ultra-cheap money encouraged homeowners to buy big homes with big mortgages, businesses to buy each other at inflated prices and a global stock market boom. The reality though is that America’s financial prolificacy which has led to a mountain of debt, makes America more dependent on others like China. America’s push for self-sufficiency is illusory, a policy by pretension. There is no alternate reality here.

History shows that when debt gets unmanageable, governments try to inflate their way out of debt as the most expedient method to pay down that debt. However the cost outweighs the benefits. Turkey is a good example. Today stocks are in the biggest bubble ever and inflation is deep rooted. Stocks are more leveraged, concentrated and risk is skyhigh. With liquidity at new records and investors buying the dips, a melt-up rather than a meltdown is likely. However the Fed is using “hawkish” threats but is “running” out of tools and reluctant to trigger a recession to stop inflation. Inflation is dynamic and WIN buttons or “tough” rhetoric did not work in the seventies when they lost control as inflation jumped to double digits. Then former Fed Chair Paul Volcker was forced to hike interest rates to double digit levels that curbed spending and led to two recessions just to get inflation under control. If Mr. Powell continues this path, hyperinflation is in the offing.

With the economy on the mend the Fed believes there is still the need for monetary medicine to be administered. However, the cupboard is empty. America’s debt today tops $30 trillion or 130% of GDP. The federal budget deficit at $2.8 trillion is equal to 12.4% of GDP, up from 4.7% last year. And there is little room to maneuver, particularly since the Fed’s balance sheet is at all-time highs representing almost 40% of America’s GDP and M2 money supply. Households and businesses too are already heavily in debt. Given the history of past discase models and lessons from pandemic pasts, of concern is that governments today have declared victory before the war is done. And the dysfunction that hampers America’s dealings with the world comes just when the central bank threatens to take the punch bowl away.

What damages trust in the US, damages the whole world. The US has a serious problem with its large deficits, accumulated debt and overvalued dollar. The 20-year war in Afghanistan alone cost $4 trillion. Also, their economy has a wide gap between the haves and have-nots, creating an increase in inequality with the pandemic accelerating the trend. Returns of capital soared but returns on labour have declined. Globalisation too was a factor as America “contracted out” its manufacturing in exchange for providing capital, but this too has come to an end as America turned inward. America instead has become an importer of capital rather than provider. As we learned in 1971, America’s huge debt load and growing twin deficits caused the US to abandon the dollar’s convertibility to gold resulting in a drastic reordering of the global financial system, changing finance forever. Today the United States is the world’s biggest debtor owing over $30 trillion in debt. Their trillion-dollar trade deficit pushes America’s debt higher making America more beholden to offshore investors who fund a good part of that debt.

With the likelihood of at least three interest rate increases this year, the interest cost on the Fed’s debt will weaken the market value of the Fed’s assets used to protect the power of the dollar. Of concern is that we believe the consequent dollar weakness would put into question the dollar’s role as a reserve currency. America faces other challenges but given its heavy dependence on foreign capital to finance its large and growing deficits, any reduction would cause Treasury securities to lose a significant amount of value, causing a debt spiral.

Already becoming the primary buyer by default of US debt, the Fed would then find itself having to support the dollar in their role as buyer of the last resort. Noteworthy is that the dollar has been steadily losing its purchasing power such that investors have migrated into hard assets or cybercurrencies, commercial real estate, art collectibles and even fine wines. Today awash in liquidity, the diversification into other assets is a reflection of the deterioration of the dollar’s role as a storehouse of value. To be sure with the prospect of change in America's monetary orthodoxy and given the stock market’s high risk, change is coming. It is to be the never normal.

The Swamp Is Draining

Financial history is littered with lessons. The implosion of the Teslas, Meta and the NASDAQ market is the beginning of the air being let out of the bubble, usually a late cycle sign of an aging bull market. The roller coaster ride because of the Reddit type investor strategy of “buying the dip” and volatile stock prices have gone hand in hand with rising bond prices, suggesting the resumption of a rotation of assets, another late cycle sign. Netflix lost $150 billion in market value. Meta lost $200 billion overnight. The once hot NASDAQ is down at least 40% from last year’s highs. And there is the $10 trillion of negative yielding debt which investors must pay just to hold the debt and guarantees a loss if held to maturity. Then there is Bitcoin losing half its value since last November as part of the $1 trillion crypto losses. Simply the swamp is draining and we are beginning to see the ugly frogs.

Still trusting the Fed, the stock market has ignored that the Fed is repeating many of the same mistakes of the 1970s. And now the jump in yields and expectations of rate increases has removed a key driver, causing the worst ever start for the stock market. Gold in turn has picked up as a barometer of investment uncertainties and a defense against inflation. Investors might like an alternate reality. Gold is that new reality.

Both China and Russia have ramped up their foreign exchange reserves to reduce their reliance on the global financial system by building monetary fortresses to protect themselves against threats of sanctions or the weaponization of Belgium-based SWIFT (The Society for Worldwide Interbank Telecommunication), the global payment network countries use for payment between themselves. While diplomats shuttle back and forth for security talks over Ukraine, America has threatened to block Russian access to SWIFT causing the rouble to weaken over fears of a capital outflow. As a result, Russia has looked for alternatives. China too has already built its own financial payment system (SPFS) and the Europeans have begun preparations on a domestic system. At the Beijing Winter Olympics, China introduced its yuan digital currency for usage. All this gradually impairs America’s monetary sovereignty by displacing usage of the dollar, undermining America’s hegemony.

We believe that China’s $3.2 trillion of reserves makes decoupling from the dollar more of a reality that would end America's monetary hegemony. China has become the sixth largest gold holder in the world. Swiss figures show gold shipments topped 275 tonnes, up from 30.5 tonnes in 2020 hitting multi-year highs. Russia too has purchased gold as part of a de-dollarization move and is the fifth largest holder with more than 20% of its reserves in gold. Meantime foreigners have slowed their purchases of US debt leaving the Fed to fill the financing gap. Markets are wary of the state of America’s finances. We believe the biggest driver will be the collapse of the US dollar. The US has a serious problem with its deficits and overvalued dollar. Although the Fed remains the world’s largest holder of gold, Russia and China already own half of what US owns. America is the world’s largest debtor while China is the world’s largest creditor. Gold is an alternative investment to the dollar for central banks. The dollar is not forever.

Gold briefly broke out of its trading range amid the escalating tensions with both Russia and China but retreated on Powell’s “hawkish” turn. There was a time when gold was money because of its permanence and longevity. In today’s uncertain world with the ongoing pandemic and geopolitical tensions deepening a worldwide inflation problem, gold is back in fashion. Part of the allure is its role as a store of value at a time of persistently high inflation and when everything else seems too risky.

Gold’s bull market is only just beginning.

Recommendations

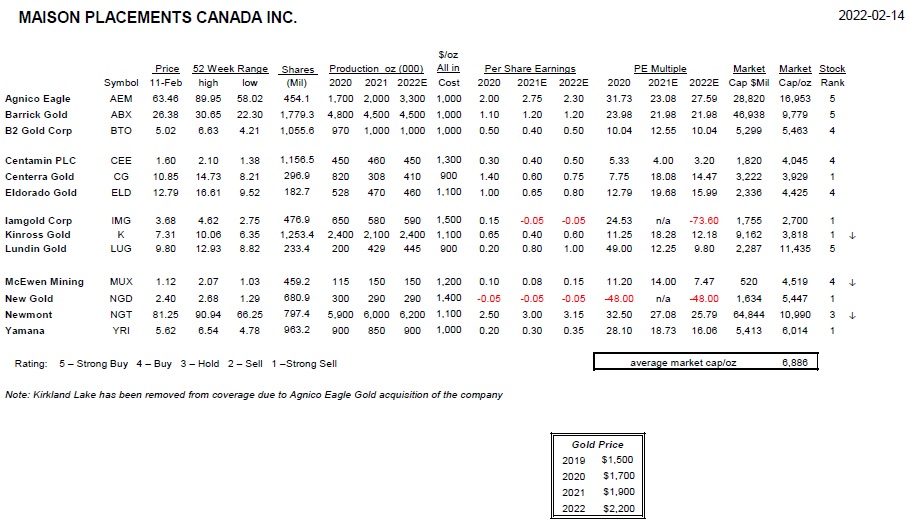

The gold mining industry’s M&A activity continues as the gold price firms up. With the completion of the $10 billion mega-merger of Agnico Eagle and Kirkland Lake Gold, investors are asking who is next. The beat goes on, Kinross made a whopping $1.8 billion acquisition of Great Bear’s Dixie Project, a project that shows promise but there is not yet a NI 43-101 report. Worrisome is that gold miners believing in the number crunchers sometimes go on misguided acquisitions such as IAMGOLD's acquisition of Côté Lake or Argonaut Gold’s acquisition of Magino whose price tag has escalated over $800 million, costing the CEO's job. IAMGOLD dumped its CEO over cost overruns at Côté. Kinross should heed past mistakes. On the other hand, Agnico Eagle and Kirkland Lake merged in Canada’s biggest takeover with the combination complementary in that it combines some of the best mining camps. Fundamentally, the reason for the rash of deals is the industry’s problem of declining reserves as a consequence of a lack of exploration and discoveries. Gold miners, flush with cash are instead looking to replace reserves on Bay Street because it is cheaper and less time consuming than to explore. Earlier Kirkland Lake bought Detour Lake for that very reason. The problem however is this game of musical chairs has few chairs empty. Consequently, the mining industry is looking at tuck-in projects rather than the mega project.

We continue to recommend a barbell approach with a heavy emphasis on the senior producers on one end like Agnico Eagle and Barrick with the developers like B2Gold, Lundin, Dundee and McEwen Gold on the other end. We like the exploration stocks in between but to date there have been few discoveries. M&A activity will continue and the single mine entities are probably prime acquisition targets. Underperforming IAMGOLD, New Gold and Eldorado are probably in the next round of takeovers.

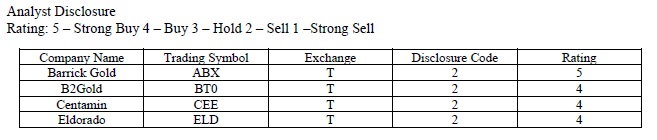

Barrick Gold Corp.

Barrick Gold has the largest number of high-quality Tier 1 assets among the gold producers. Fourth quarter production was the strongest quarter due to major contributions from joint venture Nevada Gold Mines (NGM), and contribution from Bulyanhulu in Tanzania which was once on the selling block. In addition, higher copper prices contributed to free cash flow. At one time Barrick also considered selling Lumwana but now would likely want to increase their copper exposure because of tight markets and copper’s healthy contribution to cash flow. Barrick’s copper cash costs are low and the recent acquisition of new mining equipment and stripping helped Lumwana’s margins. Barrick Gold is the world's second-largest producer with an array of top-quality assets, healthy margins and strong cash flow. The company boosted reserves this year to 69 million ounces at 1.7g/t. Barrick is a strong believer in shareholder return so buybacks and a boost in dividends are likely. Buy.

B2Gold Corp.

B2Gold received the Menankoto exploration permit located about 7 km from the flagship Fekola mine (Tier 1 asset) that consolidates the Bantako North permit lands. The granting of the permit for three years is also renewable for two additional three-year periods which allows B2Gold to begin its drill program to upgrade the resource. Meantime contributions from Cardinal will boost Fekola output. B2Gold’s operations in Mali and Burkina Faso were unaffected by changing governments. B2Gold is a low-cost producer generating strong cash flow with a strong balance sheet. We like the shares.

Centamin PLC

Centamin had a strong quarter at its Sukari Gold Mine in Egypt and is building up cash. The company produced 407,000 ounces last year in line with guidance and expects a strong year this year. The underground mine’s tonnage was up 36% from a year ago. With gold recoveries of 89%, this year the company should produce 450,000 ounces at an all-in cost of $1,300/oz. Centamin has ended underground contract mining, using its own people which will save $19 million next year as part of a new 12-year LOM schedule. Centamin recently boosted underground reserves by 200% extending Sukari’s mine life. We continue to like the shares here particularly because the company is also a potential acquisition target with reserves of 12.1 million ounces. Centamin has almost $260 million of cash and no debt or hedges. Buy.

Centerra Gold Inc.

Centerra Gold is in negotiations to offload the Kumtor mine in Kyrgyzstan. Centerra is in arbitration after Kumtor was crudely nationalized by the government, so Centerra is trying to make the best of a bad situation. Although the Kyrgyz government killed the Golden Goose, the company's future is dependent upon Mt. Milligan in BC and Oksut Turkey. Centerra expects to produce between 400,000 to 450,000 ounces from both mines and as consolation, Centerra has a cash heavy balance sheet. Nonetheless near-term prospects are clouded by protracted negotiations. Sell, because the shares are dead money.

Eldorado Gold Corp.

Mid-tier Eldorado had a strong quarter with contributions from Lamaque in the quarter. Eldorado is a mid-tier producer with mines in Canada, Turkey and Greece. Higher grades were achieved at Lamaque and the decline that will connect the Triangle deposit to Sigma will be completed this year. Kisladag in Turkey had a weaker quarter offset by Olympias in Greece. Eldorado will produce between 430,000-460,000 ounces at AISC of $1,100/oz. Eldorado has 15.3 million in reserves. Eldorado’s Kassandra assets (Skouries and Perama Hill) in Greece are a hidden asset so the shares are a hold.

IAMGOLD Corp.

IAMGOLD continues to go from crisis to crisis. Gordon Stothart resigned as CEO and President after it was disclosed that joint-venture Côté Lake once again is over-budget and will cost more to complete. Under siege from an activist investor, long standing Chair Don Charter also resigned and a new Board was named. IAMGOLD’s flagship Rosebel in Suriname recently had a new life-of-mine plan that boosted capex but reserves were reduced by 20%. Rosebel is losing money and the life of mine plan increased costs with a need for more than $1.2 billion for the remaining 12-year life. No surprise production has declined and likely Rosebel will be put up for sale. At Côté Lake, the company must spend at least an additional $700+ million dollars in order to complete the project sometime in 2023. Côté is a huge project with over 13 million ounces but the project is only 40% complete and there is the need for more money to be spent. We have always been sceptical about this big money project, believing there is fewer reserves, inconsistent grades, and the project at best is a high-risk low-reward gamble. Historically IAMGOLD has difficulty in execution. Finally at the problem-prone Westwood, the project is also to be sold. That leaves flagship Essakane with a 6-year mine life to support two failing mines which must generate sufficient cash to build Côté. We don’t think that is possible, notwithstanding the appointment of Daniella Dimitrov, known to mining and Bay Street who has bravely taken over the top job. Sell.

Kinross Gold Corp.

Kinross shares came under pressure as the Street gave thumbs down to Great Bear’s expensive (shares and cash) $1.8 billion acquisition. Great Bear’s Dixie project, southeast of Red Lake will cost more than a billion dollars to build the mine, assuming a positive feasibility. Surprisingly the project does not yet have a NI 43-101 resource so Kinross is betting the farm on making it work. Kinross could have acquired Victoria Gold’s Eagle mine in central Yukon at less cost and risk. However, Kinross does not have a good acquisition record with Tasiast still underperforming. Meantime the increase in tensions in Ukraine focused attention on Kinross’ healthy exposure in Russia where its three mines make up 25% of the company assets. Sell.

Lundin Gold Inc.

Lundin finished a strong year producing 429,000 ounces in the year from Fruta del Norte (FDN) in Ecuador. The company will produce 455,000 ounces this year at an all-in cost of $900/oz.We expect strong free cash flow will enable the company to pay down debt. Lundin will spend $14 million on regional exploration with a focus at Puente Princesa only 7 km from FDN. The South Ventilation Raise (SVR) will be completed in the next quarter. We like the shares and continue to view the shares favourably here.

New Gold Inc.

Canadian producer New Gold produced only 287,000 ounces of gold as copper production slipped 15% hurting overall costs. New Afton’s update guideline was also lowered. Cost pressures continue. Lower throughput at Rainy River in Northwestern Ontario hurt this low grade mine and all-in cost is a whopping $1,400/oz. New Afton also had a poor quarter at an all-in cost of $1,300/oz but is developing the C Zone. New Gold struggles to produce gold at a profit. At yearend the sale of a stream on Blackwater to Wheaton for $300 million helped its balance sheet. Sell.

Newmont Corp.

The world’s largest gold producer, Newmont is to acquire Buenaventura's (BVN) 43.65% interest in the Yanacocha mine in Northern Peru for $300 million plus contingent payments of up to $100 million. Newmont consolidates its interest and allows the go ahead funding of the Yanacocha huge sulphides project that will extend mine life for multiple decades. Yanacocha was a cash cow, but the open pit reserves are depleted and plans to go underground to mine the sulphides. The project already has half a billion dollars invested and there is a need for $2 billion to build the mine, including an autoclave. The first phase is to produce 500,000 gold equivalent ounces annually at AISC between $700-$800 an ounce in first five years. Newmont generates $1.7 billion of cash flow so financing is not a problem. Newmont has reserves of 94 million ounces and a stable but flat near-term production profile of 6 million ounces or so plus 1.4 million ounces of by-product credits. We prefer Barrick for their superior pipeline and array of quality assets.

John. R. Ing

[email protected]

Please refer to the Legal Section of our website (https://maisonplacements.com/legal/) for our Research Disclosures for an explanation of our rating structure at https://maisonplacements.com/research-reports/.

Disclosure Key: 1 = At the end of the month preceding the date of issuance of the report or the end of the second most recent month if the issue date is less than 10 calendar days after the end of the most recent month, Maison Placements Canada Inc and its affiliates collectively beneficially own 1% or more of any class of the issuer’s equity securities. 2= Analyst or any associate of the analyst or any individuals directly involved in the preparation of this report hold or are short any of the issuer’s securities directly or through derivatives. 3=Any partner, director or officer of Maison Placements Canada Inc or any analyst involved in the preparation of the report during the preceding 12 months provided services to the issuer for remuneration other than normal course investment advisory or trade execution services. 4=Maison Placements Canada Inc has provided investment banking services for the issuer during the 12 months preceding the research report. 5=(employee name) who is a partner, director, officer employee or agent of Maison Placements Canada Inc is an officer, director or employee of the issuer, or serves in an advisory capacity to the issuer. 6=Maison Placements Canada Inc is making a market in an equity or equity related security of the issuer. 7=In the previous 12 months the analyst received compensation based on Maison Placements Canada Inc’s investment banking revenues. 8=Analyst has paid a visit to review material operations of the issuer with the past 12 months. 9=Analyst has received payment or reimbursement by the issuer for the analyst’s travel expenses within the past 12 months. T-Toronto; V-TSX Venture; NQ-NASDAQ; NY-New York Stock Exchange.

Disclosures

Rating Structure: Number Rating: Our number rating system is a range from 1 to 5. (1=Strong Sell; 2=Sell; 3=Hold; 4=Buy; 5=Strong Buy) With 5 considered among the best performers among its peers and “1” is the worst performing stock lagging its peer group. A “3” would be market perform in line with the TSX market. UR is “under review” and is given to companies dealing with either a new issue or is waiting to clear. NR =we do not have an opinion.

Analyst’s Certification: As to each company covered in this report, each analyst certifies that the views expressed accurately reflect the analyst’s personal views about the subject securities or issuers. Each analyst has not, and will not receive, directly or indirectly compensation in exchange for expressing specific recommendations in this report.

Analyst’s Compensation: The compensation of the analyst who prepared this research report is based upon in part; the overall revenues and profitability of Maison Placements Canada Inc. Analysts are compensated on a salary and bonus system. Some factors affecting compensation include the productivity and quality of research, support to institutional, investment bankers, net revenues to the equity and investment banking revenue as well as compensation levels for analysts at competing brokerage dealers.

Analyst Stock Holdings: Equity research analysts and members of their households are permitted to invest in securities covered by them. No Maison analyst, or employee is permitted to effect a trade in the security of an issuer whereby there is an outstanding recommendation for a period of thirty calendar days before and five calendar days after the issuance of the research report.

Dissemination of Research: Research is distributed via an email marketing service in pdf form. Electronic formats are available upon request.

General Disclosures: This report is approved by Maison Placements Canada Inc. (“Maison”) a Canadian investment dealer and a participating organization of the Toronto Stock Exchange and TSX Venture Exchange. Maison is a member and shareholder of Neo Exchange. Maison is a member of and is regulated by, the Investment Industry Regulatory Organization of Canada (IIROC). Maison is also a member of the Canadian Investor Protection Fund (CIPF).

The information contained in this report has been compiled by Maison from sources believed to be reliable, but no representation or warranty, express or implied, is made by Maison, its affiliates or any other person as to its accuracy, completeness or correctness. All estimates, opinions and other information contained in this report constitute Maison’s judgment as of the date of this report, are subject to change without notice and are provided in good faith but without legal responsibility or liability.

Maison and its affiliates may have an investment banking or other relationship with the company that is the subject of this report and may trade in any of the securities mentioned herein either for their own account or the accounts of their customers. Accordingly, Maison or their affiliates may at any time have a long or short position in any such securities, related securities or in options, futures, or other derivative instruments based thereon.

This report is provided for informational purposes only and does not constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdiction where such offer or solicitation would be prohibited. As a result, the securities discussed in this report may not be eligible for sale in some jurisdictions. This report is not, and under no circumstances should be construed as, a solicitation to act as a securities broker or dealer in any jurisdiction by any person or company that is not legally permitted to carry on the business of a securities broker or dealer in that jurisdiction.

This material is prepared for general circulation to clients and does not have regard to the investment objective, financial situation or particular needs of any particular person. Investors should obtain advice on their own individual circumstances before making an investment decision. To the fullest extent permitted by law, neither Maison, its affiliates nor any other person accepts any liability whatsoever for any direct or consequential loss arising from any use of the information contained in this report.

For more information, please visit our website: www.maisonplacements.com to access the legal page for our Research Disclosures.

For further information please see IIROC Rule 3608 Research report disclosure of potential conflicts of interest.

********

share

share

share

share

share