The Gold Price Driver

There continue to be all sorts of purported analysts out there who insist that the price of gold is determined through physical supply and demand. These folks cling to the arcane notion that somehow fundamental factors are the key determinant of the daily price.

Nothing could be further from the truth.

Whether it's organizations like the World Gold Council, sell-side bullion bank scribes or internet prognosticators, the vast majority of these "analysts" believe that the primary driver of the gold price is physical supply and demand. They cite global mine supply, GLD flows and sovereign demand as their primary sources for this analysis.

But since 2014, we've argued that the primary driver of price on a daily basis is instead the HFT reaction to changes in the single forex pair USDJPY. Below is one of the original charts we posted back in November of 2014. Note that prior to The Great Financial Crisis of 2008, there was no clear correlation between the yen and gold. However, since then, and with the now-present central bank management of nearly every "market", the correlation is obvious.

If we bring this chart up-to-date and look at just the past four years, we see the result below. Note that the inverse of the USDJPY is in candlesticks, and the continuous COMEX gold contract is displayed as a blue line.

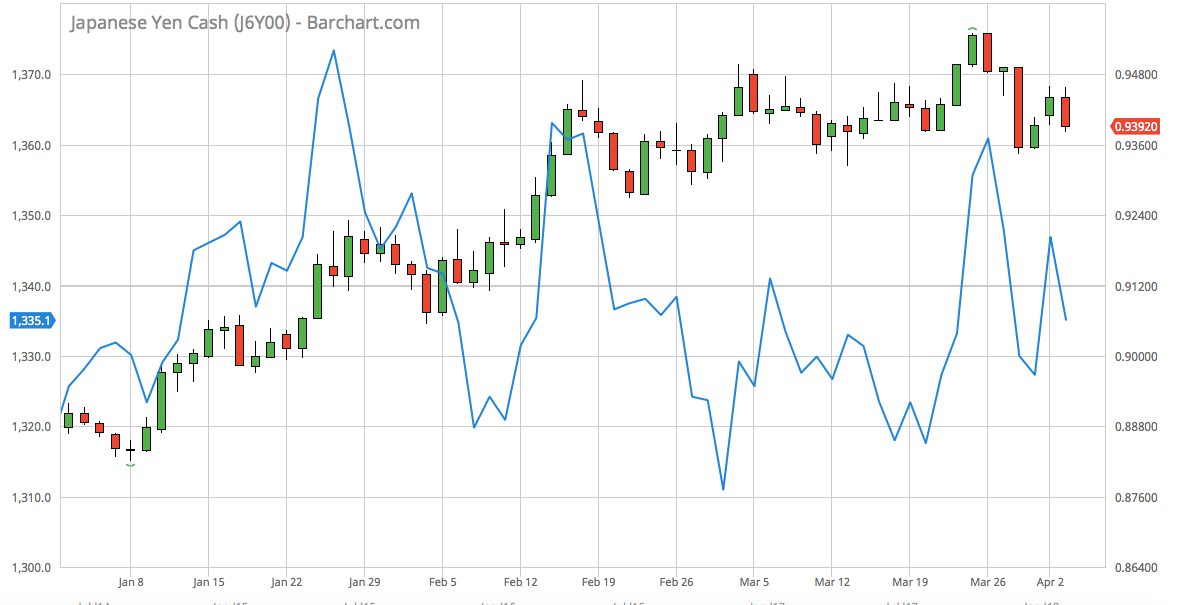

Upon closer inspection, however, it appears that a major shift has occurred in 2018. Since late January, there has been a significant divergence in the yen-gold correlation. While the yen has steadily appreciated against the dollar, the price of COMEX gold has been flat and has not kept up. See below:

And it is as if the Bank and/or Spec HFT computers have been reprogrammed. Where the yen-gold correlation had been tight on a nearly tick-for-tick basis, the price of COMEX gold now closely correlates with the dollar index, or perhaps more specifically the euro, instead. The chart below shows the euro in candlesticks and the continuous COMEX gold contract as a blue line.

IF a change has truly taken place, and IF the dominant algos have now pegged the price of COMEX gold to the dollar index or euro, then the single most important driver of the COMEX gold price in 2018 will not be mine supply, sovereign demand or ETF flows.

Instead, the single most important factor will be the general trend in the dollar. If the dollar recovers and rallies, the HFTs will sell COMEX gold exposure and price will fall. If the dollar continues to slide, the HFTs will continue to seek COMEX gold exposure and price will rally.

Back in early January, we laid out our thesis for dollar weakness in 2018, and we urge you to read it now if you missed it back then: https://www.sprottmoney.com/Blog/the-three-major-t...

In the end, it is vitally important that you understand that "the markets" in 2018 are not the same as they were in 2008 or 1998. Instead, "markets" are primarily controlled by High Frequency Trading computers whose algorithmically-based programs swap positions at the speed of light.

As this pertains to the precious metals, it's clear that fundamental factors such as physical supply and demand have little to no impact on price. Only a recognition of this basic fact gives you an understanding of what drives price on a daily or weekly basis.

Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.

Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.