Gold-Stock Reversion Due

The gold miners’ stocks are still languishing deeply out of favor, largely left for dead. Their low prices are collateral damage from this past summer’s anomalous pair of extreme gold-futures-selling episodes on Fed-tightening fears. But this bombed-out sector is due for a major mean reversion higher. Gold stocks’ technicals, sentiment, and fundamentals are all aligned to fuel a strong resumption of their interrupted upleg.

The leading gold-stock benchmark, the GDX VanEck Gold Miners ETF, was set up for a good summer. Between early March to mid-May, it powered 28.4% higher in a solid young upleg. With its four previous uplegs during this secular gold bull averaging massive 99.2% absolute gains over 7.6 months each, the gold stocks had great upside potential. But their mounting fifth upleg was torpedoed in a surprise attack.

In mid-June the Fed’s Federal Open Market Committee met, as it does eight times per year. The FOMC didn’t do anything that day, neither slowing its colossal quantitative-easing money printing nor hiking its federal-funds rate off the zero-lower-bound. The Fed didn’t even hint at any coming QE tapering or a new rate-hike cycle. Yet unofficial distant-future rate projections by top Fed officials came in slightly-hawkish.

Just a third of those guys expected to maybe see two quarter-point rate hikes way out into year-end 2023, about 2.5 years into the future! That somehow freaked out hyper-leveraged gold-futures speculators, who fled in a torrent of long selling. That hammered gold sharply lower, which the gold stocks leveraged like usual really damaging sentiment. Normally GDX amplifies gold’s significant price moves by 2x to 3x.

Gold soon resumed grinding higher on balance out of that Fed-tightening-fears anomaly, and gold stocks eventually followed. Then unbelievably in early August another extreme episode of gold-futures selling erupted! A modest upside surprise in monthly US jobs ignited a US-dollar rally as traders expected the Fed to start slowing its QE money printing sooner. Some large trader seized that for a manipulation op.

In super-illiquid Sunday-evening trading, they slammed gold by short selling an enormous amount of gold futures all at once. Brazen manipulation is the only explanation for such a huge slug of shorting unloaded instantly at such an odd low-volume time. That rare gold-futures shorting attack was an attempt to run long-side stops, unleashing cascading selling. It wasn’t too successful, but still hit gold and its miners’ stocks hard.

When the dust settled on that reporting week, speculators’ gold-futures shorting had skyrocketed near an all-time record! With gold anomalously bludgeoned for a second time in just 7 weeks, gold-stock sentiment continued to deteriorate. Bearishness exploded, which soon climaxed in heavy capitulation washout selling in mid-August. The gold stocks were wholesale abandoned, with contrarian traders fleeing in droves.

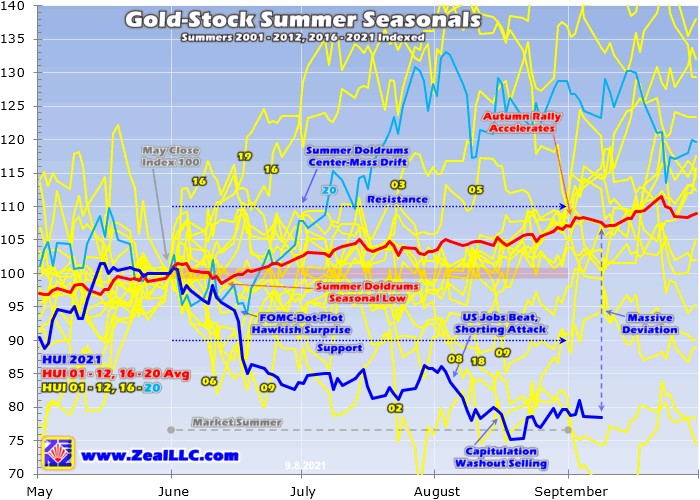

The technical damage in this sector was severe, as seen in gold stocks’ summer seasonals. This chart is updated from my summer-doldrums research thread. It looks at sector performance during all modern gold-bull years during market summers. The older HUI gold-stock index is used since GDX’s history is insufficient for this longer study. All summers are individually-indexed in perfectly-comparable percentage terms.

May’s final close is set at 100, then gold-stock price action is recast off that common baseline. Incredibly those two anomalous bouts of extreme gold-futures selling pounded gold stocks into one of their worst summers ever! That implies this sector is way oversold, and due to mean revert much higher back into more-normal territory. There’s a massive deviation from where gold stocks are and where they ought to be.

The gold stocks were consolidating high in early June before that FOMC-dot-plot hawkish surprise ignited the first round of extreme gold-futures selling. That crushed this sector well under the lower support of its normal summer trading range, which runs +/-10% from May’s final close. Gold stocks finally started to recover soon before early August’s US-jobs upside surprise provided cover for that gold-futures shorting attack.

That stoked bearishness to such irrational extremes that heavy capitulation selling flared violently a couple weeks later, even though gold prices were stable. As a result, the gold stocks plunged to an indexed level of just 75.2! They had lost a quarter of their value summer-to-date, their worst performance ever at that point in all 18 modern gold-bull years. On average their seasonal low is just 98.6 back in mid-June.

There were only two other summers where the gold stocks carved some lower lows, 2002 and 2009. In the former year, this sector collapsed as low as 67.2 indexed in late July. The culprit was again extreme gold-futures selling battering gold lower. But gold stocks soon mean-reverted sharply higher out of those deep summer lows. By early September this sector had soared 45.3% to regain 97.6 in indexed terms!

In the latter year, the gold stocks collapsed to 78.6 indexed in early July. That was more righteous then, as that older HUI index had just skyrocketed 162.7% higher in only 7.2 months out of October 2008’s brutal stock panic! So a correction was necessary to rebalance sentiment, and it happened during that summer. Yet out of that anomalous summer low, the gold stocks still soon mean reverted sharply higher.

By mid-September 2009, this sector had blasted 42.1% back higher to achieve 111.8 indexed! The principle here is clear. After extreme selling episodes hammer gold stocks to deep anomalous lows over summers, they tend to soon mean revert sharply higher. There’s a massive deviation between where the gold stocks were this week at 78.5 indexed and where they normally are now way up at 108.3 on average.

Gold stocks’ powerful autumn rally driven by gold’s own parallel one normally gets underway earlier in summers before gathering momentum later in summers. That August-and-September timeframe has long proven one of the seasonally-strongest spans for gold miners. So technically they have vast ground to make up after getting pummeled so low in mid-August. And that mean reversion is increasingly likely.

Markets abhor sentiment extremes, which are always necessary to force technical extremes. When gold stocks are trading at deeply-oversold lows, fear and despair are overpowering. That forces weak-handed traders to flee in droves, giving up at exactly the wrong time to sell out near major durable lows. But that heavy capitulation selling soon burns itself out, as everyone susceptible to being scared into selling low is gone.

That redistributing flushing leaves only buyers, hardened contrarian traders tough enough to fight the herd and buy low. These guys have spent many years studying the markets, coming to understand the endless flowing and ebbing of gold-stock cycles. They have multiplied their wealth many times in those massive-gold-stock-upleg doublings. Their buying is tentative at first, but soon accelerates as gold stocks rally.

The more contrarians buy in low, the faster gold stocks bounce out of extreme lows. The stronger that inevitable mean-reversion rebound grows, the more additional capital this sector attracts. This powerful virtuous circle of buying begetting buying is what fueled gold stocks’ big-and-fast 45% and 42% rebounds out of those anomalous lows in the summers of 2002 and 2009. That magnitude of mean reversion fits today.

To claw all the way back up to September’s average modern-gold-bull-year high of 111.5 indexed, the HUI would have to rocket up 48.2% from mid-August’s deep low! That is right in line with past summers’ mean-reversion precedent from anomalous extreme selling. This last summer’s GDX closing low on August 20th was $30.83, down 21.8% summer-to-date. A 40% rally would carry GDX back above $43.

This technical and sentimental case for a massive gold-stock mean reversion higher is bullish enough to stand on its own. If this were the entire story, this left-for-dead sector would be a screaming buy right now. But interestingly the fundamental case for regaining much-higher gold-stock prices is actually even stronger. The gold miners also happen to be deeply undervalued relative to today’s prevailing gold prices!

Stock prices ultimately have to normalize to reflect some reasonable multiple of underlying corporate earnings. The economics of this industry are simple, average gold prices less average production costs drive profitability. The gold miners earned hefty profits in their recently-reported Q2’21 results, which I analyzed and wrote about in a mid-August essay. They are earning money hand over fist at these gold levels!

That was readily apparent in trailing-twelve-month price-to-earnings-ratio terms, with many of the GDX gold miners trading at cheap multiples in the teens and even single-digits! In my decades studying and actively trading gold stocks, they are as cheap fundamentally as I’ve ever seen. Gold-stock prices need to power way higher to reasonably reflect their fat earnings driven by today’s still-high prevailing gold prices.

A great proxy for sector earnings is calculated by subtracting GDX gold miners’ average all-in sustaining costs in a quarter from its average gold prices. Those numbers ran $1,037 AISCs and $1,814 gold in Q2’21, working out to huge unit profits of $778 per ounce. That proved the third-highest on record for the gold miners! And remember mid-June within Q2 is when that first extreme gold-futures selling hit post-FOMC.

Despite early August’s crazy gold-futures shorting attack, gold is still averaging an impressive $1,797 quarter-to-date in Q3. That is running a trivial 0.9% under Q2’s lofty levels. On top of that, many of the GDX gold miners are forecasting higher production in Q3 and Q4 as ore grades improve and expansions ramp up. Better production lowers unit costs proportionally, so this current quarter’s AISCs should retreat.

So the gold miners’ latest earnings in Q3 should either hold near Q2’s great heights or even improve! If gold itself mean reverts higher as it ought to through the rest of this quarter, gold-miner profits will grow even larger. So with gold stocks trading at dirt-cheap prices relative to gold, their fundamental outlook remains strong. That really amplifies their mean-reversion upside potential as their interrupted upleg resumes.

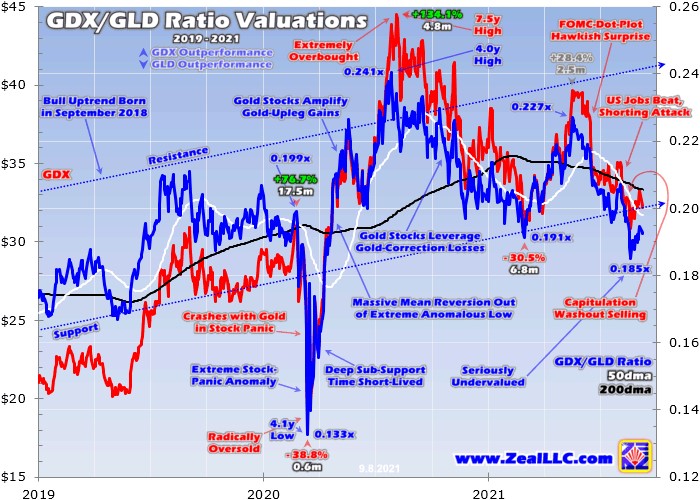

Gold-stock earnings and thus valuations are overwhelmingly driven by gold’s fortunes. So considering gold-stock price levels relative to gold’s own offers insights on whether gold stocks are undervalued or overvalued. One ratio distilling out this core fundamental relationship looks at GDX’s prices divided by those of the leading and dominant GLD SPDR Gold Shares gold ETF. This quantifies mean-reversion upside.

As secular gold bulls gradually march higher, traders increasingly believe those uptrends are sustainable. So they deploy more capital in gold stocks, slowly pushing up their valuations. This uptrend is readily evident in this GDX/GLD Ratio or GGR in recent years. While gold-stock cycles are volatile with massive uplegs and corrections, on balance miners are regaining ground relative to gold. This uptrend context is key.

But gold-stock valuations can greatly deviate from this GGR uptrend at times. They get way overbought after major uplegs, leaving the miners overvalued compared to their metal. And they get deeply oversold after major corrections, which pummel gold stocks down to super-undervalued levels. But those valuation extremes never last for long, they soon peak and give way to major mean-reversion reversals in opposite directions.

March 2020’s pandemic-lockdown stock panic slammed gold stocks so mercilessly the GGR plummeted way down to 0.133x! That deep sub-support time was short-lived though, as a massive new upleg soon erupted. As usual the gold stocks way outperformed gold’s own upleg, with GDX skyrocketing 134.1% in just 4.8 months! That pushed the GGR well above its uptrend’s resistance to a 4.0-year high of 0.241x.

That gold-stock overboughtness and overvaluation fueled by extreme greed soon yielded to a downside mean reversion in a major correction. Whenever the GGR is pushed or pulled well out of its uptrend, a big reversal swing in the opposite direction soon gets underway. That’s another reason why gold stocks look so darned bullish today. In late August the GGR collapsed way down to 0.185x, well under uptrend support!

Such seriously-undervalued levels relative to gold imply another major mean reversion higher is imminent in this battered sector. Gold stocks should outperform enough during gold’s resumed upleg to drive this GDX/GLD Ratio back up to upper resistance which is running over 0.24x. Run the numbers on that, and it portends big coming upside based on gold miners’ fundamentals. Gold stocks are due for a major upleg.

As usual that will be driven by gold’s own upleg, which will also be the fifth in this secular bull. The first four averaged big 33.3% gains. Unlike gold stocks, this past summer’s couple of extreme-gold-futures-selling episodes didn’t force gold to a deeper correction low. The yellow metal decisively bottomed at $1,681 back in early March. Another average 33.3% upleg from there would ultimately propel gold to $2,241.

There are plenty of strong arguments that this bull’s fifth upleg should grow much larger. One is the Fed’s epic money printing. Since that March-2020 stock panic, the Fed’s balance sheet has ballooned by an astounding 93.6% or $4,037b! Nearly doubling the US-dollar supply in just a year-and-half leaves wildly more money to compete for and bid up gold. Its aboveground supply only grows 1%ish per year from mining.

The raging price inflation that radically-unprecedented deluge of new money has spawned isn’t going away unless the Fed unwinds its colossal bond buying through quantitative tightening. But that would kill these lofty stock markets levitated by trillions of dollars of QE. Gold investment demand can only grow as that flood of money keeps forcing prices higher. Investment buying easily overwhelms gold-futures selling.

But to be conservative, even a mere 20% gold upleg would push this metal back up to $2,017. That is still under its last upleg’s peak of $2,062 in early August. Translated into GLD terms, that yields a gold-ETF share price around $189. Apply that GGR-uptrend-resistance valuation ratio of 0.24x to that GLD level, and it implies a GDX target of $45.36. That lowballed outlook is still 40.9% above this week’s GDX prices!

Plug in numbers for a larger gold upleg, the rising GGR resistance line, and an overbought overshoot as gold stocks’ next major upleg peaks, and the GDX upside targets are way higher. As last year’s mighty post-stock-panic specimen proved, gold-stock uplegs born out of anomalous valuation lows tend to grow massive before giving up their ghosts. Another mean reversion upleg is due today, and is likely to get big.

So despite the vast majority of traders either hating or ignoring gold stocks now, they should be pouring capital into this battered sector. Incredible bargains abound with gold stocks’ technicals, sentiment, and fundamentals all strongly supporting resuming this sector’s extreme-gold-futures-selling-interrupted upleg. While it is never easy to fight the herd and buy in low, those great entry prices lead to much-larger gains.

Thanks to gold-futures speculators freaking out about both distant-future Fed rate hikes and QE tapering slowing money printing’s pace, it’s been a rough summer in gold stocks. We suffered stoppings in some of our newsletter trades on those anomalous selloffs. But with gold and gold-stock outlooks remaining so bullish, we redeployed in fundamentally-superior mid-tier and junior gold miners to keep our trading books full.

At Zeal we walk the contrarian walk, buying low when few others are willing before later selling high when few others can. We overcome popular greed and fear by diligently studying market cycles. We trade on time-tested indicators derived from technical, sentimental, and fundamental research. That has already led to realized gains in this current young upleg as high as +51.5% on our recent newsletter stock trades!

To multiply your wealth trading high-potential gold stocks, you need to stay informed about what’s going on in this sector. Staying subscribed to our popular and affordable weekly and monthly newsletters is a great way. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today while this gold-stock upleg remains young! Our recently-reformatted newsletters have expanded individual-stock analysis.

The bottom line is gold stocks are due for massive mean reversions after this past summer’s anomalous extreme gold-futures-selling episodes. That bashed gold stocks to deeply-oversold levels technically, which spawned super-bearish sentiment. And with gold miners’ earnings so strong, their valuations were also crushed to dirt-cheap levels. These excesses aren’t sustainable, portending another major upleg coming.

Market extremes are soon followed by sharp reversals in the opposite direction to normalize relationships. Both gold’s and gold stocks’ parallel uplegs interrupted by mid-summer distant-future-Fed-rate-hike fears are set to resume powering higher. That means beaten-down gold stocks should see major upside during coming months. As always the biggest gains will be won by the contrarian traders buying in early and low.

Adam Hamilton, CPA

********