Gold SWOT: Goldman reiterated its “buy” rating on Sibanye Stillwater

Strengths

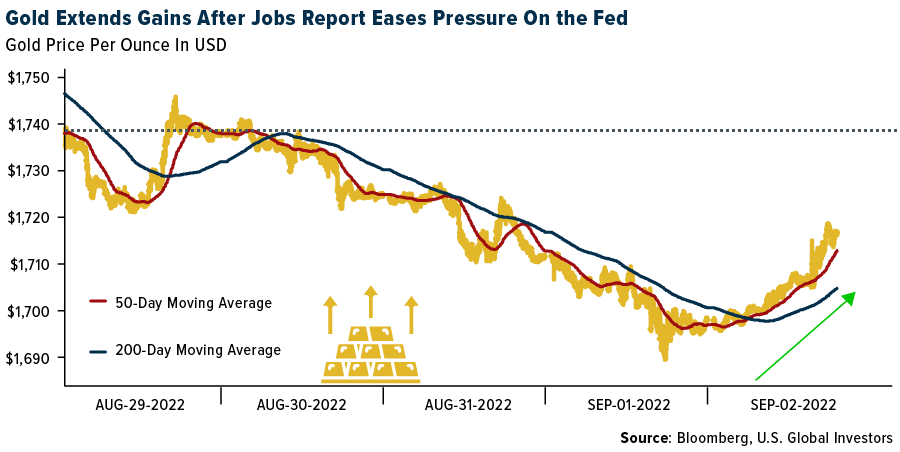

- The best performing precious metal for the week was gold, still down slightly 1.63%. Gold showed some strength as we closed out the week on a jobs report showing that more Americans are coming back to the labor market. The report reduces the risk that the Federal Reserve will hike faster-than-expected, according to Edward Gardner of Capital Economics.

- Revival Gold’s share price moved up 20% this week as the company announced it will extend the earn-in agreement to acquire 100% of the Beartrack property from Meridian Gold, a wholly owned subsidiary of Yamana Gold, for an additional two years. Revival Gold also made the final option payment of $250,000 to acquire 100% of the Barnett claims, which expands the flexibility of the Beartrack property and adds exciting exploration potential, noted Hugh Agro, President and CEO of Revival.

- Steppe Gold provided an update on progress of its Phase 2 Sulphide Expansion for the ATO Gold Mine located in Mongolia. Progress has been made on two key milestones, the grid power connection, and the new fixed crusher construction. Approval has been granted by the Mongolian government agencies to provide power to the ATO Phase 2 Expansion. This will materially decrease operating costs (by more than $100 per ounce) through significantly decreased power costs.

Weaknesses

- The worst performing precious metal for the week was palladium, down 5.28%, on little specific news other than a potentially weakening industrial pace ahead. Investor interest in gold continues to wane due to a hawkish Federal Reserve, with Chair Jerome Powell signaling higher-for-longer rates in his speech at Jackson Hole. Global holdings in bullion-backed ETFs have shrunk for 11 straight weeks, the longest stretch since September 2018. Moreover, the latest outflows have been dominated by those who established positions only within the past two years, suggesting that recent buyers have been less committed compared to traditional ETF investors, said Suki Cooper, a precious metals analyst at Standard Chartered Plc.

- Endeavour Mining reported that unidentified gunmen killed six people and wounded two others in an attack on a convoy from the Boungou gold mine in eastern Burkina Faso. Boungou accounts for 9% of the company’s asset value.

- Harmony Gold reported a swing to a net loss for fiscal year 2022, citing higher production costs and impairment charges. Gold production of 1.49 million ounces was achieved, coming in lower than the 1.54 million ounces in the prior year. Harmony’s share price slid more than 20% over the week.

Opportunities

- Maverix Metals said it has acquired a portfolio of 22 royalties from Barrick Gold Corp for an upfront cash consideration of $50 million, reports Proactive Investors, and up to $10 million in contingent consideration depending on certain events occurring. The portfolio includes royalties on development, advanced exploration and exploration stage projects located predominantly in Canada, the United States, and Australia.

- Goldman reiterated its “buy” rating on Sibanye Stillwater. The bank sees appealing valuation coupled with strategic focus on acquiring green metal assets in developed markets and unique exposure to gold within its coverage.

- “ Sad” is how Dirk Treasure, CEO of Chrysos Corp., described the share price of his company after its IPO three months ago. With the price down more than 50%, largely on the overall negative tone since gold peaked earlier in the year, Chrysos has a revolutionary, game changing technology for rapidly analyzing drilled rock core for its metals content. The company uses high-powered X-rays to travel through the rock core, activate the atoms of gold and other metals, and then measure their concentration levels. This process should ultimately disrupt the historic process of splitting the core and sending it off to a lab for fire assays and then waiting weeks to months to find out where in the exploration program you’re at. Chrysos just reported maiden results with revenue up 215% to $14.2 million, ahead of the forecast $13.6, and has $92 million on hand to help fund its manufacturing pipeline.

Threats

- Northam expects cost inflation just under 10% on a unit cost basis but sees the current environment as one of “elevated business risk.” Diesel, which has doubled in price, remains a key uncertainty and is the primary energy input at Booysendal. Northam expects the diesel price to moderate alongside oil.

- UBS cut its medium-term earnings and cash generation forecasts for Northam following a disappointing fiscal year 2022 operational performance and deteriorating medium-term management outlook. UBS subsequently reduced its PT by 7% to R140 per share and reiterates its “sell” rating as the group is increasingly concerned by Northam's unit cost and capex inflation, and questions when/if this trend will reverse through greater economies of scale and declining growth capex.

- De Beers reported sequentially "flat” rough diamond sales for its seventh sale of the year, indicating a continued strong uptake for its unprocessed diamonds amid uncertainty around the supply of rough stones out of Russia. Interestingly, this dynamic is different to polished diamond markets that had started to show signs of a souring consumer sentiment amid softening prices. It remains to be seen how long the price performance disparity persists between rough and polished markets.

********

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].