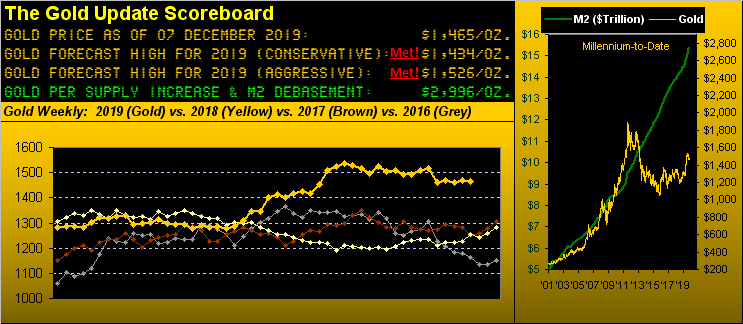

Gold Takes A Whack, Its Support Shelf Intact

Following Gold's fall from the 1500s back on 05 November, our missives these past several weeks have found us fairly bulled-up throughout. Trusting the 1454-1434 "support shelf" as a pricing base has thus far been Gold's saving grace. So much so that a week ago we queried "Shall Santa Gift Gold at 1500?" St. Nick's great global ride is still better than two weeks away, and given Gold having settled yesterday (Friday) at 1465 combined with an "expected weekly trading range" of 38 points, 1500 is certainly not out of range whatsoever. But per the above Gold Scoreboard in looking at Gold's weekly settles across the past five weeks, 'twould appear rather that the patient is almost flatlining on life support. In fact, Gold's net weekly change has been less than ten points now for each of four straight weeks "...beep...beep...beep...beep..."

Indeed as we turn to Gold's percentage track across the past 21 trading days (one month), its correlation to the stampeding S&P 500 clearly continues as negative, but 'tis not the perfect mirror image that we had been seeing through the prior like period. Our sense is the 1454-1434 "support shelf" has become sufficiently visible to the Gold trading community such that price is stubbornly refusing to cave in kind to the S&P's rising frame of mind. To wit per this time frame, the S&P is +1.9%, however Gold is off just -0.8%, (notwithstanding a week ago some seven points of premium help in the roll from the December contact to that for February):

Now obviously, yesterday's stellar StateSide November jobs creation report was a win for the S&P and a whack for Gold; however as we oft quip: "change is an illusion whereas price is the truth." And through it all, Gold's price has maintained buoyancy vis-à-vis the 1454-1434 "support shelf" as we next see here in the chart of Gold's weekly bars from one year ago-to-date. Moreover, this past week's high of 1489 (noting that Gold's "expected daily trading range" is now 14 points) came within 11 points of regaining the gift of 1500. Further, the red-dotted parabolic Short trend continues to descend without price really following such bend:

In the broad view from Gold's All-Time Closing High of 1900 we next contextually see price's pullback from this year's high of 1566, a rather controlled decline without the sharp down-streaks of years past. As an active trader of Gold equities just reminded us: "You can't sell 'em on the way up if you first didn't buy 'em on the way down." Common sense is a beautiful thing:

What's regaining some degree of beauty, (barring it being a one-time straight-up spasm) is the current spike of the Economic Barometer. As we've preached ad nauseam over the years, 'tis the S&P 500 (red line) that ultimately moves to the graphed level of the Econ Baro (blue line). At present, seems 'tis the opposite. In addition to the Bureau of Labor Statistics citing a pickup in November payrolls of 266,000 -- a 71% increase over that from October and completely contra to ADP's calculated jobs decline of -45% to just 67,000 -- came increases in Vehicle Sales, but the month's Institute for Supply Management manufacturing reading again ran in contractual mode. And despite a pullback in October's Construction Spending, that month's Factory Orders increased, the Trade Deficit was reduced, and Consumer Credit (albeit a bit scary) doubled from $9.6 billion to $18.9 billion ... "Got credit cards?" Everybody must be happy as the University of Michigan's initial Sentiment read for December hit a six-month high. Here's the Baro:

'Course "It's all good" is a matter of perspective when living off of other entities' monies: the mighty U.S. corporates' total level of debt has now risen to some 47% the size of the entire economy: everybody expecting their $10 trillion back? "What?" Meanwhile any phase of an on-again-off-again trade deal with China seems was on-again but now is off-again; Japan is cranking up its stimulus machine; Canadian job growth is morphing into job loss; and reform of the French pension has fueled a record storm of strike tension. Just as along as we're happy with the "live" price/earnings of the S&P at 36.4x, "It's all good", right?

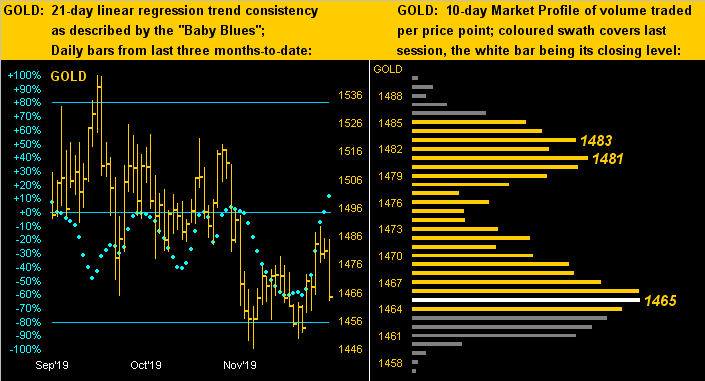

What is looking right -- notwithstanding Gold having yesterday put in its worst intra-day high-to-low blow (-22 points) since 07 November (-32 points) -- is the track of the yellow metal's "Baby Blues" that we next see below left across the last three months of daily bars. The blue dots pace up through their 0% axis confirms the 21-day linear regression trend as having turned positive. But Gold need regain grippity to maintain such stance, indeed not fall afoul of the 1465 trading support area where price sits in the 10-day Market Profile below right, (under which, 'natch, lies the 1454-1434 "support shelf"):

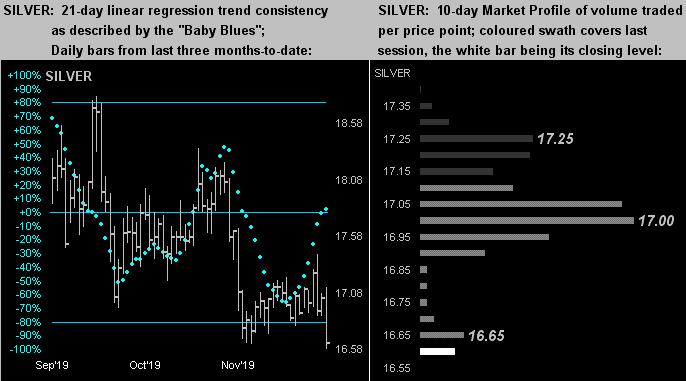

Silver's "Baby Blues" (lower left), too, are rising, but now just barely so. The white metal's Friday demise by pricing structure was far worse than Gold's fallout, the 12 November low (16.615) being taken out (16.575). So low did Silver go that (as noted in the data of the Gold weekly bars graphic) the Gold/Silver ratio now stands at 88.1x, an off-the-charts reading to be sure, but then again, the high end of "the norm" across the past year. And thus hardly for the first time, we find Sister Silver buried at the base of her Profile (lower right):

Thus as the economic good-times roll, we have to say Gold is playing a fairly stalwart role. Indeed, price took a significant whack in closing out an "It's all good" week for the S&P and the economy, yet Gold's critical 1454-1434 "support shelf" remains intact. To be sure, the S&P is flying high, its lack of earnings suggesting otherwise. So let you be the wise: for in due course Gold has so far to rise! Just ask Helvetia.

www.deMeadville.com

www.TheGoldUpdate.com

********

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.