Gravity Grasps Gold

Let's start with a show of hands. Ready? How many of you after reading last Wednesday's Policy Statement as issued by the Federal Open Market Committee basically sensed that all they did was change the date from 28 July to 22 September? Good, good, most of you. What's that? Just as they'd done prior from 16 June to 28 July. Yes, a fine observation there.

Which continues to make the point: lots of between-the-meetings talking without any actual tapering nor tightening. 'Tis always about to happen, but never so does. Indeed to quote Chair Powell from his Wednesday presser: "... I think we could easily move ahead at the next meeting or not..." And the FOMC's unanimity continued as all were "Voting for the monetary policy action..." What action?

'Course within the timeframe of now and the next FOMC meeting (03 November) is what we lovingly dub for the stock market as "Crash Season": that doesn't mean 'twill, but as you well know, we're now in the heart of what historically is the most difficult time of the year for equities. And it remains our take that the Fed's most unspoken fear is it all going south for stocks. However of note thereto, Chair Powell did warn on Wednesday that The Bank shan't be able to shield the markets should the U.S. default on its debt, which in a fundamental sense it rather has been doing for years. Nonetheless (or more so), Congress just again came through in the nick of time to raise the ceiling for more debt. (Are you going to buy some?)

Either way, with respect to a debt default, the folks over at Moody's have calculated were such to occur, 'twould result in the loss of almost six million StateSide jobs. 'Tis quite a complex calculation up with which they've come, however we query: would not a debt default extinguish nearly all (some 160 million) jobs? Don't deny domino theory:

And as we continue to hammer: whether measured by our "live" S&P 500 price/earnings ratio of 50.6x or Bob Shiller's 38.5x, the next p/e "means reversion" means a massive move lower for price, barring earnings more than doubling (which en masse obviously never happens). Remember: the "remarkable Q2" Earnings Season for 2021 recorded an increase over that of 2020's "shut down Q2" of just +35%. Otherwise, year-over-year percentage increases typically are at best single-digits. "Say G'Nite, Dick!"

"But until the Fed actually 'jerks the rug' as you say, mmb, the money is gonna keep on coming, right?"

That's been the unaltered course since the depths of COVID well over a year ago, Squire. And even should tapering start, the flow remains positive until the purchasing stops. Just in time for your next best-seller: "Accounting Credits Killed the Currency", (in bookstores for the holidays).

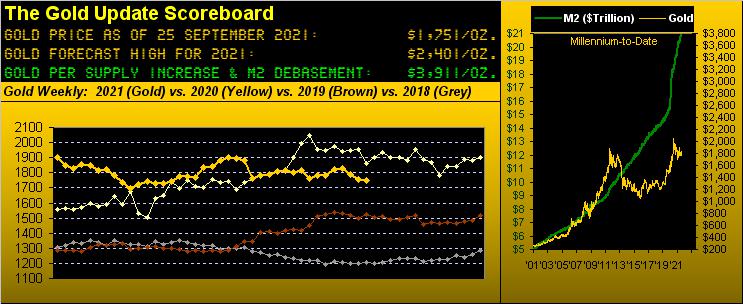

Regardless, such papering-debasing of the currency hasn't budged Gold (net net) for better than 10 years. That covers a lot of rooting without results. Gold's settle yesterday (Friday) at 1751 essentially matches that of 09 August 2011. And yet since that date, the U.S. money supply ("M2") is +121% and the S&P 500 is +280%. Under-owned and out-of-favour remains our Gold, +0%. Reprise: "Goin' Nowhere"--[Chris Isaak, '95].

Still, we on occasion remind ourselves of that stated by the first sole recipient (one JGS) of The Gold Update: "One day we'll wake up and Gold'll be $1,000/oz. higher than it was the day before." 'Twould be nice if that, too, were in store for the holidays, for our 2021 Gold forecast high of 2401 shall have been achieved. But that now lofty goal is really looking lousy.

Lousy in tandem is the present 13-week stint of the yellow metal's parabolic Short trend shown here in the graphic of the weekly bars from a year ago-to-date. As gravity grasps Gold, the pull to this past week's 1738 low was as far down as we've seen price go since six weeks ago. Further for those of you lucky enough to be scoring at home, these current 13 weeks of Short trend tie for 12th in duration since the turn of the millennium; the Short average is 11 weeks. Thus this trend ought well flip to Long before year-end. But in this year of reduced contract trading volume for Gold (see last week's piece) and the expected weekly trading range now 52 points, the nearly 100-point stretch to flip the trend to Long in the ensuing week is by rote remote:

From lousy to loosey-goosey is this perception as published during the week by Dow Jones Newswires that "Fed Officials See 'Transitory' Inflation Lasting Quite a While" thus in the balance there being a "growing eagerness to start raising rates." We didn't actually glean same this past Wednesday from the FOMC nor Chair Powell; however the notion of something transitory as lasting is marvelously oxymoronic.

Specific to the economy, the week's rather brief calendar did highlight housing improvements notably for September's National Association of Home Builders Index and August's level of both New Home Sales and Housing Starts/Permits. And on balance, the tilt of the Economic Barometer is of late rising:

'Course in this new 180° out-of-phase paradigm of bad being good and vice-versa, should the apparent economic enhancement continue, such good then reverts to bad for the S&P -- already struggling as you can above see -- upon the Fed pressing the raise rates key. Fortunately 'tis said that's not supposed to take place until 2023; oh wait, 'twas moved up a year to 2022; oh wait, (uh-oh?) And how about that S&P lower low, (uh-oh!)

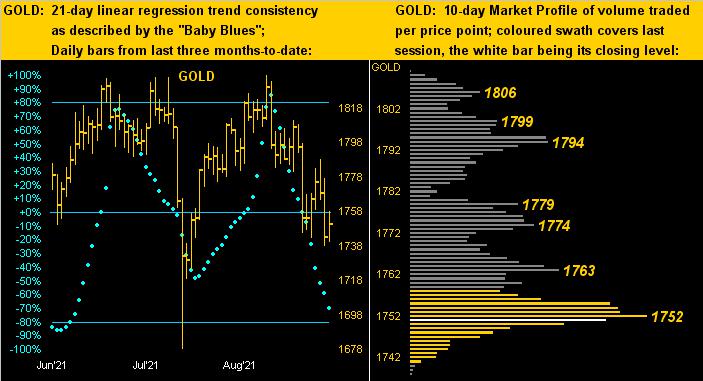

To the yellow metal's technicals we go, the daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. And for both panels, Gold's picture has pretty much been the same these past three weeks: plunging "Baby Blues" with price maintaining a low profile (pun intended):

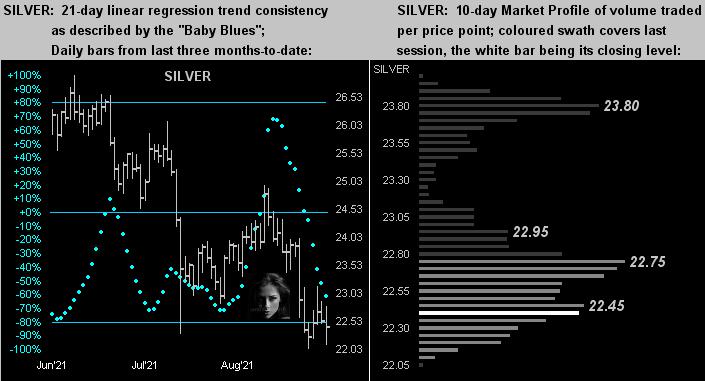

For the white metal, the picture too remains the same: three weeks of nothing, save if you've been Short Sister Silver, something to which she historically does not take kindly...

Next week, kindly or otherwise, brings Q3 to a close. Within the batch of 13 incoming metrics for the Econ Baro comes (on Friday, 01 October) the Fed's favourite read of inflation: the monthly change in Core Personal Consumption Expenditures. We thus again ask: Transitory, Perma-Story or Stagflatory?

Let's close, again with a show of hands: Now be honest. How many of you one week ago at this time had heard of something called Eveready, (or is it Everclear)?

"Actually, mmb, one makes batteries and the other one is ethanol. You're thinking of Evergrande..."

Yes, that's the one, Squire, thank you. Anyone? Evergrande? Just a couple of you. We appreciate your honesty. Come last Monday, it seemed anybody and everybody was talking about Evergrande as a long-standing household name. Clearly, 'twas the "in-thing" about which to know, but we'd never heard of it. So we looked it up and found it to be a PRC-based reality group with a global ranking of 112. That's why we'd never heard of it. Thus all of those phinancial phonies showing off their intimate knowledge of Evergrande clearly were full of Everclear, (which apparently you can both drink and use to power your car -- not advisable in any combination).

Indeed, (gravity's present grasp notwithstanding), a far most suitable and lasting combination is Gold and Silver. We'll drink to that!

www.deMeadville.com

www.TheGoldUpdate.com

*********

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.