Hedging The Decline And Fall Of A Currency

“Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.” – John Maynard Keynes, The Economic Consequences of Peace (1919)

–––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

Hedging the decline and fall of a currency

The baseline case for gold hasn’t changed much in 1700 years

Image courtesy of Visual Capitalist • • • Click to enlarge

(Editor’s note: We first published this review of Jack Whyte’s novel, The Burning Stone, almost two years ago in March 2020. With inflation back at the forefront of investor concerns, we thought it appropriate to reprint it here for our new readers and those who may have missed it. The story is likely to capture your interest. The message Whyte imparts on saving, the value of money and inflation is timeless.)

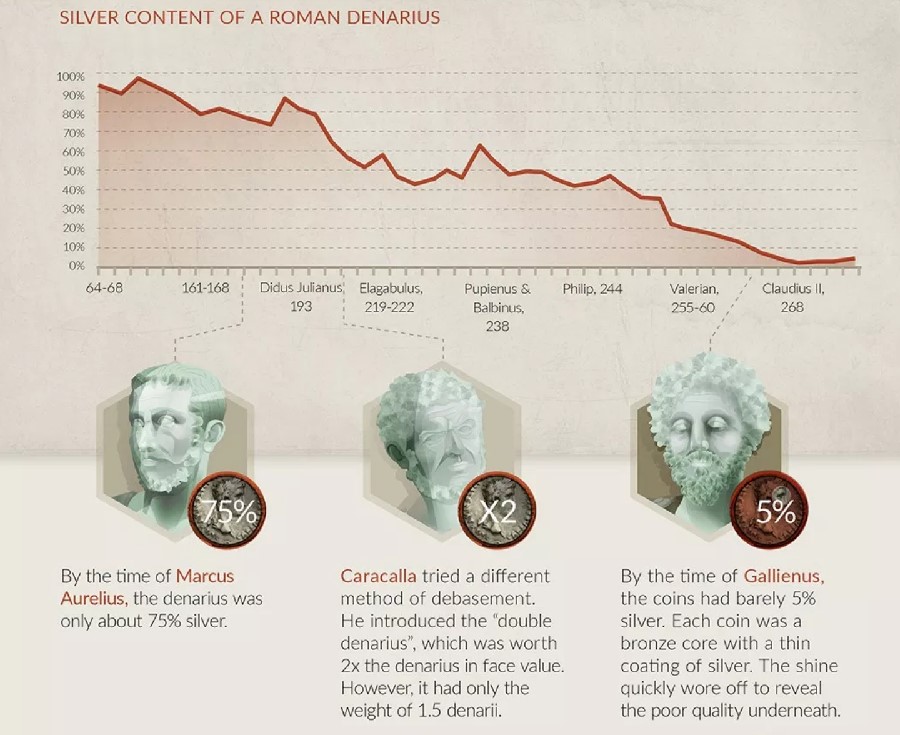

We sometimes forget that inflation is a process rather than an event. One of the better-known examples of that axiom is the nearly two centuries-long debasement of Rome’s silver denarius – an inflationary episode Jack Whyte, a writer of historical fiction, skillfully addresses in his latest novel, The Burning Stone.

Set in Great Britain in the fourth century AD during the Roman occupation, The Burning Stone is a prequel to Whyte’s engaging, seven-book series on King Arthur – The Camulod Chronicles. Throughout the series, Whyte juxtaposes the rise of Arthur’s Camelot against Rome’s decline. This particular story is told through the lens of a young Roman from a wealthy family with banking, political and military interests who flees to Britain after his immediate family is murdered for reasons that remain a mystery for most of the novel.

After a series of fateful events involving his future wife, he becomes a blacksmith forging and fashioning the highest quality swords. Even as he assumes the life of tradesman-entrepreneur, he keeps contact with the Roman military in Britain and goes about the business of reordering his affairs as an expatriate Roman citizen, albeit one who wishes to keep a low profile. Then, one day, the young blacksmith, Quintus Publius Varrus, receives a scroll from his uncle, an admiral in Rome’s navy, advising him to expect an important shipment from the continent in the near future.

This is where Whyte’s tale takes a turn toward monetary economics and an insightful commentary on Rome’s currency debasement as a symptom of, if not a catalyst for, the empire’s ultimate demise. The inflationary process extended over the reigns of several emperors and went on for more than two centuries (See graphic below). The Roman citizen who had the wisdom to hedge that process ended up preserving and building his or her wealth — those who did not suffered the debilitating effects of the resulting inflation.

In Whyte’s telling, Varrus’ grandfather, an advisor to Emperor Diocletian and a member of the ultra-wealthy Seneca banking family through marriage, was among those who chose to accumulate gold coins as a hedge against the ongoing debasement of the silver denarius.* When Varrus opens the shipment from his uncle, he finds it to contain a very large hoard of Roman imperial gold coins and a letter describing his grandfather’s rationale for forming the accumulation.

“His heroes,” the uncle writes, “included giants like Cincinnatus and Cato the Elder, both revered for their unswerving loyalty, integrity, and civic duty. More humorously, and with genuine irony, he distrusted banks and bankers – unsurprisingly, perhaps, given that he wed into the wealthiest banking family in Rome… In keeping with that distrust, he was assiduous in hoarding his money, keeping its whereabouts unknown.”

“There are five thousand aureii in the box,” he goes on, “the oldest of them dating from the time of Octavian, Caesar Augustus, and the newest of them, in the fourth level down, minted during the reign of Marcus Aurelius. After that time the value of the aureus declined from year to year as the intrinsic value was degraded by unscrupulous speculators, so your grandfather refused to deal in anything more recent than the mintings of Marcus Aurelius.”

“The bottom layer of coins, though,” he says concluding his description of the chest’s contents, “contains nothing but golden solidi minted during the lifetime of Diocletian. There can be no deception there. The solidus is minted of pure gold, and though few of them were issued, there can be no doubt of their validity in real terms, and my father valued them highly. That layer contains one thousand Diocletian solidi. There is no more valuable coin in existence, and I know of no one other than yourself, among all the people I know, who can claim to have a thousand genuine Diocletian solidi in their possession. Any one of the other coins in the box could fetch ten times their nominal value from a sharp-eyed trader.”

And so it is, according to Whyte’s tale, that great wealth was transferred at the time of Rome’s decline from one generation to the next………

(Please scroll to Final Thought for concluding section.)

Short & Sweet

FUND GURU JOHN HUSSMAN’ delves into the return of your capital in a market so distorted none of the old verities matter any longer. He says we are in an era of “return-free risk.” He goes on to say in a recent client letter that “By relentlessly depriving investors of risk-free return, the Federal Reserve has spawned an all-asset speculative bubble that we estimate will provide investors little but return-free risk. … In a world where securities are regularly described on CNBC as ‘plays,’ it’s clear is that the financial markets presently have little to do with ‘investment’ – at least not by Benjamin Graham’s definition as ‘an operation that, upon thorough analysis, promises safety of principal and an adequate return.'”

“The difference between genius and stupidity is that genius has its limits.”

Albert Einstein, as quoted by Hussman in that same article

THROUGHOUT THE 1970s, we recall, the federal government blamed inflation on everything but itself: businesses, oil exporters, even farmers. The 1970s Nixon administration went so far as to introduce price controls – a policy that only made things worse and had to be abandoned. The real source of inflation now is the same as it has always been – running large federal deficits and financing them with printing press money. The White House, from our perspective, is doing its best to ignore the continuing pleas of the former Treasury Secretary. Summers says we are moving toward “higher entrenched inflation.” In a recent Bloomberg report, Summer says that “misdiagnosis of the problem around greed or around particular sectors raises the risk that ultimate recession will be necessary. We need to recognize that we’ve got an overheated economy that we are going to need to cool off.”

ONE OF THE MORE INTRIGUING ANALYSES of the gold market to emerge in recent months comes from Myrmikan Research’s John Oliver. He inquires into gold’s rangebound behavior under these extraordinary circumstances and concludes, “what propels gold into the multi-thousands of dollars per ounce—is sharply rising rates that destroy the value of the Fed’s assets and make further federal deficit spending impossible. Without a political reason to buy the dollar, it will seek out its economic value.” It’s all in the math, and more specifically, he says that when looking at gold, investors “are going to have to get used to logarithmic scales.” Last January, Myrmikan projected a gold price of $5000 per ounce at some point down the road to give one-third backing to the Fed’s balance sheet. Now, says Oliver, it would take a gold price in excess of $11,000 to achieve the same backing. Consulting projections on gold’s logarithmic chart, he says, “the first stop of $10,000 is actually not that far away.”

“THE NATURE OF INFLATION is widely misunderstood and misinterpreted,” writes analyst Dave Kranzler in an Investing.com overview, “‘Inflation’ and ‘currency devaluation’ are tautological—they are two phrases that mean the same thing. … Dollar devaluation has been occurring since the early 1970’s. The value of the dollar relative to gold (real money) has declined 98%. In 1971, $40,000 would buy a 4,000 square foot home in a good suburb. Now it takes $700,000 on average to buy that same home. Price inflation is the evidence of currency devaluation. The CPI is not a real measure of price inflation. The CPI is methodically massaged – starting with the Arthur Burns Federal Reserve (it was his idea) to hide the real degree of currency devaluation from all of the money that has been printed since 1971.”

FINANCIAL TIMES’ DELE OLOJEDE Financial Timers recently reviewed Howard French’s new book, Born in Blackness, which chronicles Africa’s central role in the emergence of the modern world. In the fourteenth-century Mali ruler Mansa Musa, who some say was the wealthiest individual in history, traveled to Mecca to pay homage spreading his golden largesse along the way. “Camels and horses,” he writes, “reportedly carried up to 18 tonnes of pure gold, all of which the benevolent ruler dispensed along his route to all and sundry. … On account of this singular voyage, the price of gold reportedly plummeted throughout the region by up to 25 percent over the following decade.” Musa’s journey, says French, “remembered by virtually no one save the historians of medieval Africa, merits consideration as one of the most important moments in the making of the Atlantic world.”

“For those who think gold missed the inflation train, there are several reasons to reconsider. There have only been two other inflationary periods in the last 50 years. The first was in the seventies, the second from 2003 to 2008. In each of these inflationary periods, gold underperformed commodities in the first half and outperformed in the second half. It seems that markets don’t take inflation (or gold) seriously until it proves to be intractable. There are many reasons to believe 2022 will see the beginning of a wage/price spiral.” – Van Eck Funds

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

The six keys to successful gold ownership

This eye-opening, in-depth introduction to precious metals ownership will help you avoid many of the pitfalls that befall first-time investors. Find out who invests in gold, what role gold plays in serious investors’ portfolios, and the when, where, why, and how of adding precious metals to your holdings. To end right, it is critical that you start right, and the six keys to successful gold ownership will point you in the right direction.

––––––––––––––––––––––––––––––––––––––––––––––––

IMAGINE YOURSELF AS PRIVATE CITIZEN ELON MUSK and that three months ago you sold your 3-year old Tesla. In payment, you accepted bitcoin and decided to hold onto the remittance because it looked to have a very bright future. At first, your decision looked to be a very shrewd maneuver as the cryptocurrency rose 10%. But then things began to go in the other direction. By the end of January, the value of your holding had dropped nearly 40%! Not so shrewd after all. You just sold your Tesla for about 60% of its value. To the rest of the world, your plight illustrates why bitcoin can never be mistaken for gold. Had you taken gold in payment, instead, the value of your holding would have risen by about 2%. The truly wise investor will note, at the same time, bitcoin’s trading in sympathy with tech stocks, particularly those priced on shaky foundations.

IN HIS TEN SURPRISES FOR 2022, Byron Wien predicts persistent inflation will become the dominant theme, the 10-year Treasury note will yield 2.75% (it’s 1.72% now), and gold will gain 20% as it “reclaims its title as safe haven for newly minted billionaires.”

ECONOMIST BRUCE YANDLE says that “the monetary chickens have come home to roost.” Recent data, he says in a recent article posted at the Washington Examiner, put to rest “any suggestion that inflation was beginning to wither away. What consumers in grocery stores and filling stations have known for months, politicians must now grudgingly admit: The cost of living is going up and far faster than average wage increases will cover.” Yandle, a professor of economics at George Mason University and former executive director of the Federal Trade Commission, says it took about a year for the pandemic-induced money printing binge to show up in prices. “[W]hen confronted with evidence of rising prices,” he advises, “there was more than just a tendency for political leaders to lay the blame on OPEC, China, or greedy capitalists. Their own culpability with the monetary printing presses didn’t come up much.”

FORMER KANSAS CITY FED CHAIRMAN THOMAS HOENIG recently issued a dire warning about where we are headed with monetary policy. “The historical record,” writes Politico’s Christopher Lewis, “shows that Hoenig was worried primarily that the Fed was taking a risky path that would deepen income inequality, stoke dangerous asset bubbles and enrich the biggest banks over everyone else. He also warned that it would suck the Fed into a money-printing quagmire that the central bank would not be able to escape without destabilizing the entire financial system.” Is this not where we are as 2022 dawns?

BRIDGEWATER SECURITIES RAY DALIO says the old order is giving way to a new. “I believe,” he writes in a recent Linked-in piece, “the current paradigm is a classic one that is characterized by the leading empire (the US) 1) spending a lot more money than it is earning and printing and taxing a lot, 2) having large wealth, values, and political gaps that are leading to significant internal conflict, ad 3) being in decline relative to an emerging great power (China). The last time we saw this confluence of events was in the 1930-45 period, though the 1970-80 period was also analogous financially.” He advises against owning dollar, euro and yen-denominated credit instruments. Over the past several years, Dalio has repeatedly recommended gold ownership for the average investor to hedge the difficulties he sees ahead.

“BULLION COIN SALES,” reports CoinNews, “were the best in over 20 years, almost doubling in total revenue from $2.1 billion in 2020 to $3.8 billion in 2021. Increased demand for bullion products was led by increases of 70.5% and 57.1% in sales of total ounces of American Gold Eagles and American Buffalo Gold coins, respectively. Sales of Silver Eagles increased by 62.4% (again in total ounces sold), while American Platinum Eagle sales rose by 33.9%.” Rangebound pricing, bargain hunting, and the inflation outlook were prime contributors to the U.S. Mint’s outstanding year.

“So silver is relatively cheap right now. In fact, the metal is currently trading well below its July 2020 price of roughly $27 – before the Fed’s printing press really went into overdrive. In other words, it’s trading as if no money-printing has happened. … The next few years could be huge for silver. Now is the time to add some exposure to this unloved metal to your portfolio.” – Laurence Vegys, Rogue Economics, The Commodity That Soars When Inflation Is Rising

DOUG NOLAND RECENTLY SUMMARIZED what others were thinking in his weekly digest, Credit Bubble Bulletin. “Books will be written chronicling 2021,” he says. “I’ll boil an extraordinary year’s developments down to a few simple words: ‘Things Ran Wild’. Covid ran wild. Monetary inflation ran wild. Inflation, in general, ran completely wild. Speculation and asset inflation ran really wild. More insidiously, mal-investment and inequality turned wilder. Extreme weather ran wild. Bucking the trend, confidence in Washington policymaking ran – into a wall. … The year ends ominously. Omicron and Manias. Inflation and ever-widening wealth disparities. Anger, frustration and disillusionment. Irrepressible enthusiasm for stock market and economic prospects – for those fully consumed by the asset markets. A gambling mentality and wanton disregard for risk. Disheartenment for those surviving outside the Bubble, while those on the inside – wallowing in the monetary deluge – bask in the ‘Roaring Twenties.'”

“IN RECENT YEARS,” writes Desmond Lachman in an analysis posted at the American Enterprise Institute website, “accurate economic forecasting has not been the economic profession’s strong suit. In 2008, it spectacularly failed to anticipate the Great Economic Recession despite the advanced signals that the US housing and credit market bubbles were about to burst. In 2021, with very few exceptions, it failed to anticipate that inflation would accelerate to a forty-year high.… 2022 looks like it might be another year in which the economics profession in general gets caught very flatfooted with its forecasts.” Lachman goes on to outline why we should be worried about the financial system’s health in 2022. He says economists now believe that the banks are much better positioned to weather higher rates than they were in 2008, but they are blind to the vulnerability of “unregulated hedge funds, private equity companies, insurance companies, etc.”

ATLAS PLUS’ CHARLIE MORRIS SAYS, “It is time to be bullish on gold. … Just as investors were confused by gold’s weak 2021,” he predicts in his Atlas Plus newsletter, “they will be surprised by its buoyant 2022. Too many have written it off, which is ridiculous when you come to think of it. Hundreds of years of human economic history, yet investors get bored when it takes a short break. … I mean, who would bother owning gold when there’s a boom in growth stocks? The point here is that booms eventually come to an end, and the last time this happened in March 2000, gold enjoyed one hell of a run thereafter.”

THE SILVER INSTITUTE POSTED its forecasted year-end (2021) results for the white metal last week and reports record global demand with investors taking advantage of consistently lower, rangebound pricing. Overall demand, it says, will surge past the one billion ounce mark for the first time since 2015, led by industrial demand at 524 million ounces – a new high. In addition, it forecasts investment demand will end the year 32% higher due to heavy uptake in India and (surprisingly) the United States. “Building on solid gains last year,” says TSI, “US coin and bar demand is expected to surpass [for 2021 year end] 100 million ounces for the first time since 2015. Growth began with the social media buying frenzy before spreading to more traditional silver investors. Indian demand reflects improved sentiment towards the silver price and a recovering economy. Overall, physical investment in India is forecast to surge almost three-fold this year, having collapsed in 2020.”

Final Thought

Conclusion: Hedging the decline and fall of a currency

(Editor’s note – The following is the concluding section of the original special report published March 2o2o. Please see above for introductory section.)

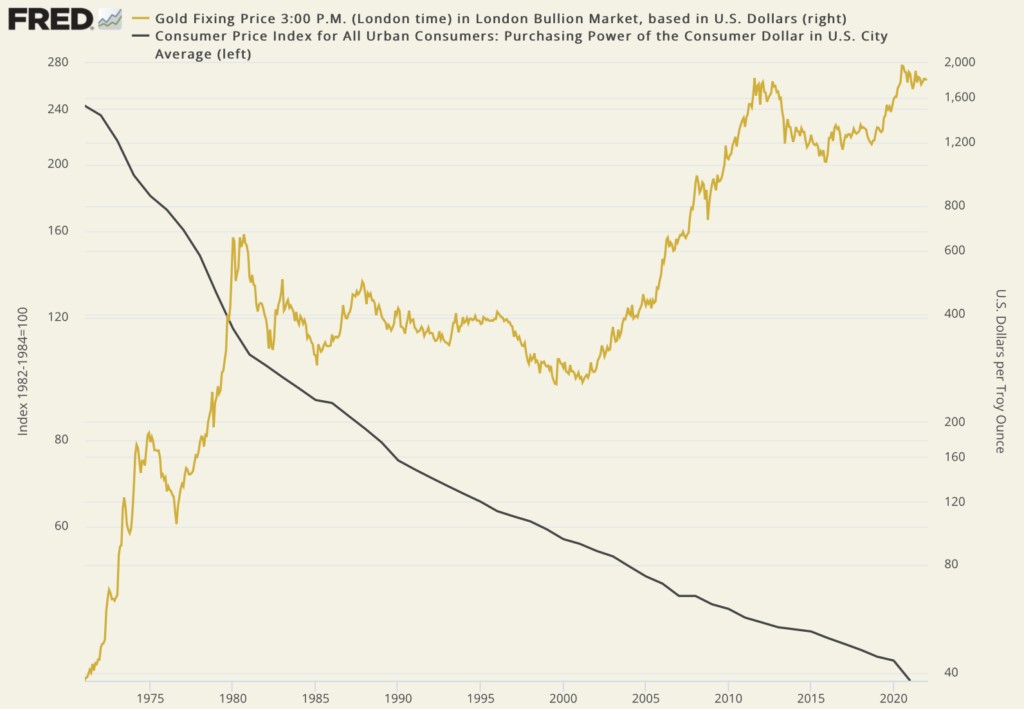

Fast forward 1700 years and we find that not much has changed. Since 1971, when the United States detached the dollar from gold and ushered in a new era of fiat money, the dollar, as shown in the chart below, has lost 84.5% of its purchasing power. The 1971 dollar is now worth 15.5¢. Gold in the meanwhile has risen from $35 per ounce then to nearly $1700 today (with a stop at $1900/oz in 2011.)

Over the long run, gold in the modern era has maintained its purchasing power as it did in Roman times, while the dollar, like the denarius, has been steadily debased. So it is by the circuitous route just taken, you now know how Jack Whyte’s depiction of the Roman inflation in The Burning Stone reinforces the argument for gold ownership today. It also explains why we went to the trouble of presenting a review of this intriguing book in our monthly newsletter.

Sources: St. Louis Federal Reserve, Bureau of Labor Statistics, ICE Benchmark Administration

We should be careful not to drop our guard on the prospects of future inflation because of the lull we have encountered in recent years. In the inflationary process, the line between cause and effect is not always a straight one. History teaches us, though, that when runaway price inflation does arrive, it can come suddenly, without notice, and with a vengeance. Rome’s inflation and currency debasement, as Whyte points out in The Burning Stone, proceeded in fits and starts and unfolded over centuries. When runaway price inflation struck, however, it delivered its ill-effects emphatically during individual lifetimes – sometimes within a few short years. That is why it pays, as shown in the chart, to view gold as a permanent and constantly maintained aspect of the investment portfolio like Quintus Publius Varrus’ grandfather did in Whyte’s novel.

In a recent Daily Reckoning opinion piece, James Ricards argues that investors around the world are now beginning to lose faith in fiat currencies and stockpiling gold as a result. The fact that the metal has achieved all-time highs in a long list of currencies over the past several months supports that conclusion. The incipient demand for gold on a global basis, however, raises a different kind of problem – particularly if we move from crisis watch to crisis reality.

“In the new super-spike,” he warns, “you may not be able to get any gold at all. You’ll be watching the price go up on TV, but unable to buy any for yourself. Gold will be in such short supply that only the central banks, giant hedge funds and billionaires will be able to get their hands on any. The mint and your local dealer will be sold out. That physical scarcity will make the price super-spike even more extreme than in 1980. The time to buy gold is now, before the price spikes and before supplies dry up.”

At the moment, the supply lines in the precious metals business are still functioning smoothly. There could come a time, though, when they are not – a possibility, by the way, that has received scant attention in the context of the coronavirus contagion.

–––

Up-to-the-minute gold market news, opinion, and analysis as it happens.

If you appreciate NEWS & VIEWS, you might also take

an interest in our Daily Top Gold News and Opinion page.

Disclaimer – Opinions expressed on the USAGOLD.com website do not constitute an offer to buy or sell or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. USAGOLD, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such, USAGOLD does not warrant or guarantee the accuracy, timeliness, or completeness of the information found here. The views and opinions expressed at USAGOLD are those of the authors and do not necessarily reflect the official policy or position of USAGOLD. Any content provided by our bloggers or authors is solely their opinion and is not intended to malign any religion, ethnic group, club, organization, company, individual, or anyone or anything.

********