Inflation And Gold In The 1970s Vs. Today's Situation

History does not repeat itself, many people say. However, the lessons from the past should be learned. The prices of precious metals have recently fallen after the last Fed’s meeting. Briefly, investors are worried the Fed will hike the interest rates twice in 2023 due to the inflationary pressures. Here I will explain how inflation can get out of control by comparing the current situation to the 1970s Great Inflation in the US.

1970s inflation

Some of the 1970s inflation pressure was due to the fact President Nixon canceled the 1944 Bretton Woods system that tied the US dollar to gold. So, the gold prices were fixed and the inflation rate was highly moderate. In 1971 President Nixon decided to abandon the gold standard. This in turn allowed the country to expand the monetary policy or, in plain terms, raise the money supply.

But the story is not that simple.

To start with, during the Great Depression in the 1930s the US suffered enormously. One of the most catastrophic social and macroeconomic problems was extremely high unemployment. After World War II it became the government's priority to create full employment. One of the most notable laws that emerged, as a result, was the Employment Act of 1946. According to the act, it became a responsibility of the federal government “to promote maximum employment, production, and purchasing power” and provide for greater coordination between fiscal and monetary policies. In other words, fighting unemployment got the government's top priority. The post-war period was a time of rapid expansion and macroeconomic growth. Now experts say that the current post-Covid-19 economic growth is similar to the post-war economic expansion.

The economic philosophy behind this was Keynesian, named after John Maynard Keynes, a British economist, that supported the view that governments should use countercyclical policies in hard times. According to him, it is acceptable to run deficits in recessions and depressions.

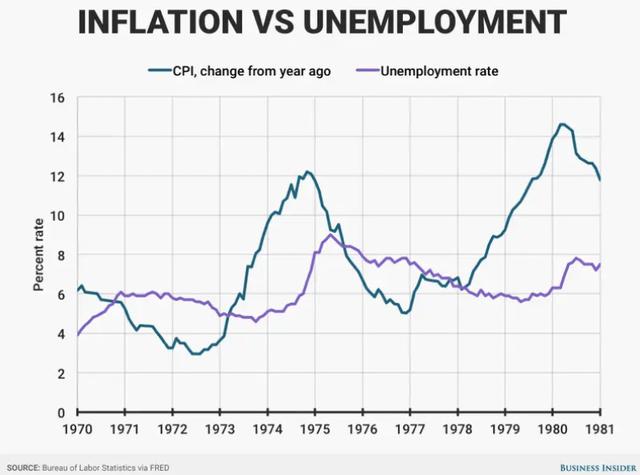

As I have mentioned before, the USD was backed by gold. So, there was a limit to monetary expansion since the global supply of gold is limited. So, in 1964 inflation was only 1% and unemployment was 5%. It took only 10 years for the macroeconomic picture to change dramatically. A lion's share of the changes has happened after 1971. The inflation rate exceeded 12%, whereas unemployment was more than 7%. By the summer of 1980, inflation was about 14.5%, whilst the unemployment rate was over 7.5%.

Source: Business Insider

However, facilitating economic expansion was not the sole motive of this reform. The US suffered from significant budget deficits, caused by the Vietnam War. The debt soared, whilst before 1971 it was impossible to significantly devalue the dollar due to its link with gold.

However, when the Bretton Woods system was over, the dollar got devalued and the money supply soared. This was also facilitated by a significant reduction in interest rates.

The inflation rate soared significantly. The graph above shows the consumer price index minus the volatile goods, namely the food and energy costs. By the mid-1970s it reached around 12%. However, in the 1970s there was an oil supply crunch that made the overall inflation level soar even further.

By the late 1970s, the public began to expect that inflation would be here to stay, whereas the Fed would continue doing nothing about it. Obviously, they were getting increasingly unhappy with inflation. Survey after survey signaled deteriorating public confidence over the macroeconomic outlook and monetary policy in the latter half of the 1970s. Inflation was identified as a special evil. During this time, business investment slowed, productivity faltered, and the nation’s trade balance with the rest of the world worsened. What is more, inflation was accompanied by high unemployment. The interest rates spiked sharply higher as the 1970s came to a close and inflation was universally viewed as either a significant contributing factor to the economic unease or its primary cause.

So, in 1978 the Full Employment and Balanced Growth Act, more commonly known as the Humphrey-Hawkins Act, was adopted. Humphrey-Hawkins obliged the Federal Reserve to aim for both full employment and price stability. The act also required that the central bank establish targets for the growth of various monetary aggregates, and also present a semiannual Monetary Policy Report to Congress.

Now the goal was to reduce both the unemployment rate and inflation. In early 1980, Volcker said, “[M]y basic philosophy is over time we have no choice but to deal with the inflationary situation because over time inflation and the unemployment rate go together.… Isn’t that the lesson of the 1970s?” (Meltzer 2009, 1034).

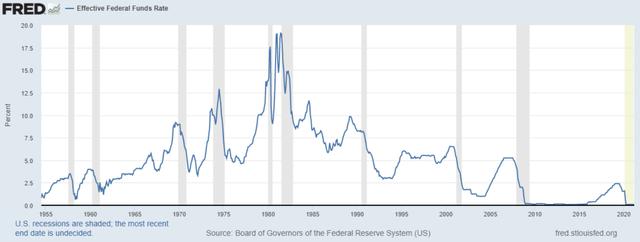

In October 1979, the FOMC announced its plan to target its balance sheet rather than the fed funds rate as its policy instrument. In other words, the Fed decided to significantly curb its money-printing activities. The inflation rate slowed significantly not just because of the tighter money supply but because of the dramatic interest rate hike in 1980. Credit controls were introduced as well. This had its own consequences. Lending activity fell, the unemployment rate surged, whilst the economy entered a brief recession between January and July. Inflation fell but was still high even as the economy recovered in the second half of 1980. Despite this, the Fed, led by Volcker, pressurized inflation with higher interest rates and slower reserve growth.

The economy entered recession again in July 1981, and this turned out to be much longer, which continued until November 1982. Unemployment totaled almost 11%, but inflation kept falling and by the recession’s end, year-over-year inflation was below 5%. As the Fed’s commitment to low inflation gained the general public's trust, the period of Great Inflation was over.

The key here seems to be the public's trust the Fed is committed to low inflation. So, it's not just the actual CPI figure that matters in combatting inflation but there are also general inflation expectations that play the role.

Even more interesting is the history of gold pricing and inflation. In the 1970s there was quite a strong correlation between gold and the CPI index. In the 1970s gold served as a true hedge against inflation. The main reason was mainly the public's expectations of much higher inflation and the destruction of the dollar's value. The interest in gold was due to a fall in public confidence.

Source: Investing.com

Although high-interest rates are normally considered to be a hurdle to higher gold prices, this clearly was not the case for the 1970s. As can be seen from the graph above, it took the gold price just a couple of years to jump from around $40 per ounce to $200 per ounce despite the reasonably high interest rates.

Source: FRED

The main reason for such a surge was the rising money supply.

What is happening today?

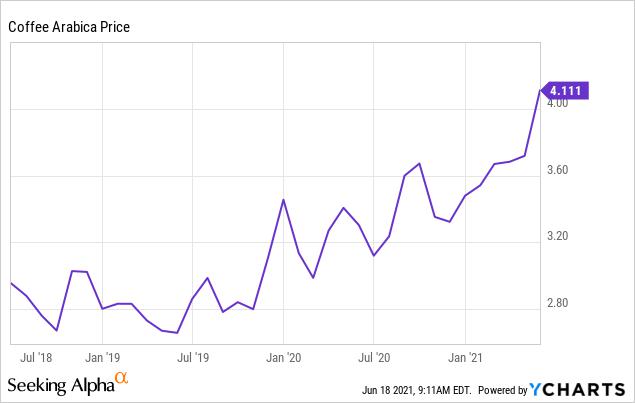

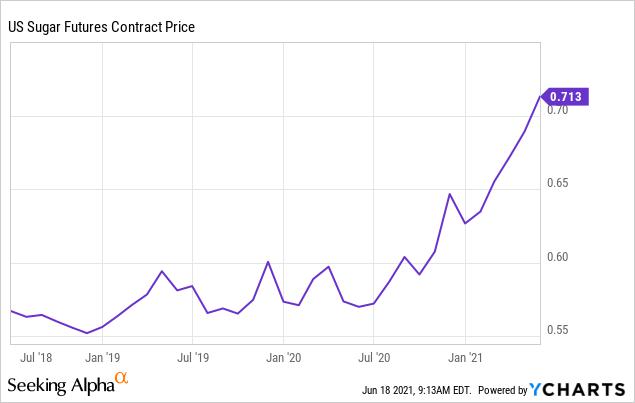

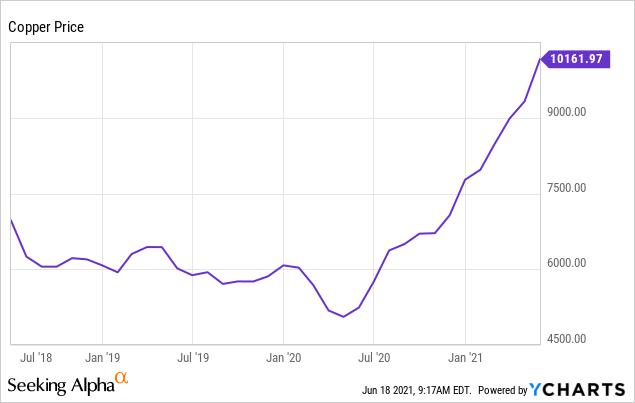

The recently reported annual inflation rate for the United States totaled 5.0% for the 12 months ended May 2021. This is the highest indicator since 2008. At the same time, the prices for many commodities and raw materials have risen even more. This surge has been true of products like coffee, sugar, iron ore, copper, and lumber. In recent days, the prices have cooled somewhat due to the Fed's higher inflation expectations and the forecasted hikes in 2023 but the post-pandemic surge still looks impressive. Many commodities have surged by 30% and 50% since the spring 2020 collapse.

Data by YCharts

Data by YCharts

Data by YCharts

The prices of copper and other metals have almost doubled.

That is highly similar to the situation we faced in the 1970s when there was cost-push inflation, mainly caused by soaring oil prices. There was an extreme oil shortage due to the Arabic embargo and the Iranian revolution.

Another problem that looks quite similar to the 1970s crisis is the Fed's priority of the labor market over the inflation rate. Although the Fed's Jerome Powell said the labor market generally improved since the start of the pandemic, he still pointed out that there is still progress to be made. At the same time, in the Fed's view inflation is "transitory".

The investors have recently assumed that the Fed would hike the interest rates in 2023 due to the dot plot. But this sounds like an eternity to me since a lot can change over this time period. Even Jerome Powell admitted the central bank members' predictions should be taken with a "grain of salt".

What is more, there is a problem with the excessive money supply. This problem was in the 1970s and it is present now. Right now just like in the 1970s the Fed is in no rush to cut the money supply. At the same time, we are also suffering from stagflation when the labor market is weak, whereas the inflation rate is high. So, as many experts say, "the Fed is trapped". Whatever it does, its actions will be disapproved by the general public. If it tightens the monetary policy, it will lead to massive market selloffs, surging unemployment, and overall economic inactivity. If it does not tighten its monetary policy, the inflation rate will get totally out of control.

Not only do the Fed's actions matter here. Its willingness to act is also important here. In the 1970s there was a crisis of confidence, a panic. This also made inflation get out of control. Many experts nowadays also fear the inflation rate will get out of control. The fear the USD will quickly lose its value may make the demand for precious metals soar again the way it did in the 1970s.

Conclusion

The world changes fast. The very same situation might not completely repeat itself. However, we can clearly see the parallels between the 1970s and today. Inflation is rising fast, whereas the unemployment rate is still quite high. It seems to be the Fed's priority to stimulate the labor markets, whereas inflation is seen as transitory. There are fears the overall price level will get totally out of control. There was cost-push inflation just like there is today. At the same time, there was a crisis of public confidence, which may also happen nowadays. That is why the gold prices soared back then and they might rise substantially in the near future.

*********

Anna Sokolidou, a graduate of the University of Edinburgh, is a research analyst and a freelance writer with a strong interest in commodities. She has several years of investing experience and working as an in-house analyst. She is particularly enthusiastic about researching precious metals and conducting macroeconomic analysis. Her work has appeared on a number of investing websites but she now mostly publishes her work on Seeking Alpha.

Anna Sokolidou, a graduate of the University of Edinburgh, is a research analyst and a freelance writer with a strong interest in commodities. She has several years of investing experience and working as an in-house analyst. She is particularly enthusiastic about researching precious metals and conducting macroeconomic analysis. Her work has appeared on a number of investing websites but she now mostly publishes her work on Seeking Alpha.