Inflation Should Be A Four Letter Word

Wikipedia, the encyclopedia of the man on the street, describes the practice by central banks of “inflation targeting” as Monetary policy - “Inflation targeting is a monetary policy where a central bank follows an explicit target for the inflation rate for the medium-term and announces this inflation target to the public. The assumption is that the best that monetary policy can do to support long-term growth of the economy is to maintain price stability, and price stability is achieved by controlling inflation. The central bank uses interest rates, its main short-term monetary instrument.” Wikipedia

From “The Balance”: Inflation targeting can be a key factor in boosting the economy.

By Kimberly Amadeo. Inflation targeting is a monetary policy where the central bank sets a specific inflation rate as its goal. The central bank does this to make you believe prices will continue rising. It spurs the economy by making you buy things now before they cost more.

In a perfect world, prices are set freely by the seller and buyer, whether this happens by barter or through a monetary intermediary of which the supply is fixed. Bartering is influenced by the cost of production on the seller’s side and by the perception of value on the side of the buyer. Prices also vary as supply and demand change, because of circumstances and time. In such a world there effectively will be no systemic inflation due to any extrinsic factor or factors.

In winter, because of scarcity, vegetables will be relatively more expensive than what they had been in summer. But as spring comes and turns into summer once more, they will become relatively cheaper again. Similar changes happen to many goods and services that are in demand. That is considered typical of a normal economy and it is one that works well over time.

Now consider a people who viewed large brown grasshoppers as such a delicacy that in due course and as these became more scarce, they came to be used as money, either fresh or dried. After school all but the youngest kids were sent out into the veld and the bush with nets mounted on sticks to hunt for large brown grasshoppers. It was a system that worked well for generations, but then a disaster happened. Freaky weather conditions caused the large brown grasshoppers to swarm.

Suddenly, everyone in that economy was a millionaire. People who had wished for a long time to have some minor luxuries which they could not really afford, rushed out to purchase these. Latecomers soon discovered that prices had increased to levels they again could not afford; that is, if supply had not by then been exhausted.

A crude example, but it gets the message across. Prices remain relatively stable while the balance between the money supply and the goods and services in demand are close to balanced. When the supply of money suddenly increases substantially so that real demand grows more rapidly than it can be satisfied by a much slower increase in production, prices will rise. Initially, while demand can be easily met, the increases will be relatively slow. Then, as demand reacts to more easy money, prices rise at a steeper rate and gain momentum as the lag in the supply chain and availability of goods and services begin to have effect.

This process is bad enough when demand is predominantly for the more luxury items that previously were unaffordable, but it goes critical when the necessities for survival become scarce and expensive. When absolute necessities of life begin to get scarce – and therefore more expensive – while the supply of money keeps on growing, it is too late to turn back the clock. Inflation is on a roll and continues to get much worse.

Because of COVID, the initial money printing was necessary to enable households that were suddenly with no income and too few reserves to cope with the new normal to survive. Then more money was printed in an effort to kick-start the economy; which accelerated as 2021 took hold. It would become a political disaster if the White House and new administration failed to extend the economic recovery that had begun in Q3 of 2020 and lasted into Q4, as claimed by politicians and the media.

Going into H2 of 2021, the US has at least two major handicaps in the effort to get the economy going while keeping inflation under control. The first is the drought in the western states, California in particular. This event is having a significant effect on the prices of food, which is essential and has to be purchased even when supply is low and prices are increasing steeply. Even if it did start raining soon, this problem cannot be resolved over-night; prices will keep on rising. Dams used for irrigation are close to being empty, and crops of all kinds take time to grow until they can be harvested.

The second factor other than a reduced supply of food is scarce consumer goods. It so happens that ever since the Clinton administration ‘opened gates to let US factories out’, to settle in other countries, the USA developed a ‘drought’ in its manufacturing capability. This fact, combined with efforts to reduce dependence on China, surely must reduce the flow of consumer goods onto the shelves in the malls – or onto the web pages of the internet retailers. A lack of local manufacturing capacity also means fewer well paying jobs, a slower economic recovery and few new jobs being created to make households self-supporting

With this as background, the probability that the jump in the CPI will turn out to be only a spike – a transitory event – has to be rather small. Inflation tends to nurture on itself; ask ex-Fed Chairman Volcker how difficult it was in the late 1970s to force the inflation genie back into the bottle; having to raise interest rates well into two digits to do so – a solution that is impossible to employ in 2021.

The effects of high inflation on the economy are not good, but these are much worse for households where reserves are minimal and wages and salaries do not keep pace with increases in prices. The elderly who are existing on pensions and Social Security are guaranteed to fall below the bread line, with dire consequences for them. the older folks.

We should note that the current gloomy situation is not a result of the pandemic. Not that COVID is not contributing to the problems and is helping to precipitate the state of crisis that is developing rather rapidly. The US was set on the path to where it is today when during the Clinton administration the official CPI was ‘adjusted’ to satisfy academic concerns and interpretations, then continued to be used as a CoL index to determine wage and salary increases.

Clinton was scared that if the economy did not recover fast enough from the recession in the early 1990s that cost the senior Bush a second term, the same would happen to him. Having ‘low’ inflation suited his other measures to be re-elected; requirements to purchase a home were relaxed to boost the property market, as were regulations over the financial industry; trade agreements were modified to enable more importation of cheaper consumer goods and then also the export of manufacturing capacity.

The first indication that the new path was leading to trouble came in 2007/8. The new crisis was patched up with plentiful dollars and nothing changed. Great concerns later about the widening gulf between the wealthy and the rest were much discussed and then new memes took over, with Trump’s presidency, COVID and a strange election among them – all of which triggered a deluge of fresh dollars entering the economy.

These recent events only hastened what John Williams of Shadowstats believes will be hyperinflation by 2022; the causes of what seems set to happen soon lie more than 25 years ago in history. Tough times are closing in fast, likely to be made worse by a developing food crisis and probably constraints on energy as well. E.B. Tucker views the Fed as addicted to inflation as if it were cocaine, a drug that is the scourge of the rich. Inflation similarly deserves to be described by a four letter word for the economic damage and financial pain for most households that it causes.

On 28 May the gold OI was 497 102 and that of silver 181 373. Last Friday, the gold OI was lower, little changed from two weeks before at 493 196, but the silver OI is now 198 791 – an increase of 17 418 or 9.6%. Often after a month end, the metals’ OIs decrease by a substantial amount as contracts stand for delivery while many of the expiring contracts are not rolled over into later months.

After two weeks into the new month of June, the gold OI has already recovered near to what it had been close to the end of May; the silver OI has increased substantially and could increase even further by the end of June as the battle for $28 continues. July is a silver month, but on Friday the July OI decreased by 6400, while the OI for September increased 9700 – perhaps an indication that the ‘Squeeze silver’ campaign is being rescheduled two months later in order to build more momentum.

That would give PSLV and buyers of the metal itself more time to sweep the shelves retailers and other reserves clean of any excess silver – to compel the official price of the metal much closer to what is currently being asked and paid on the open market.

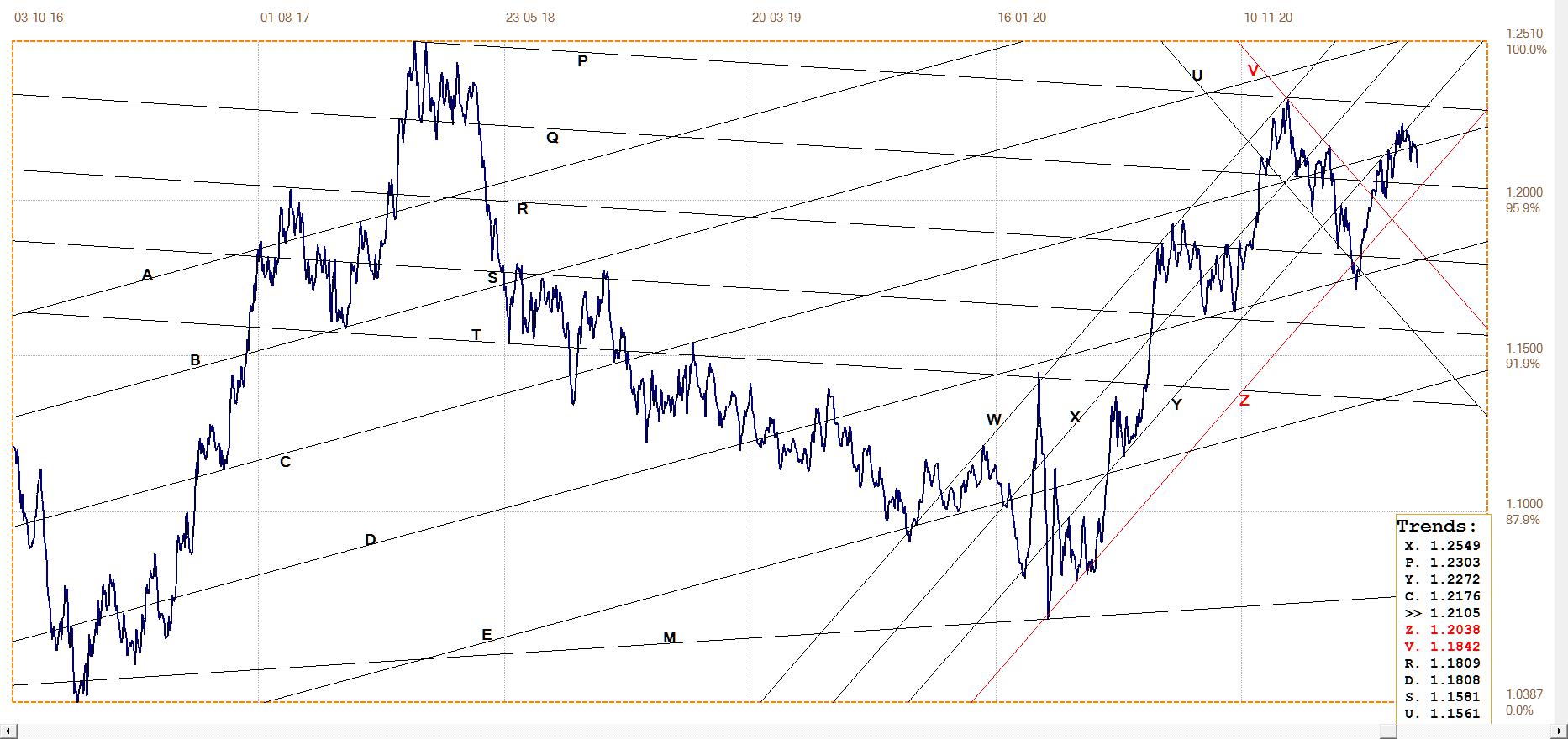

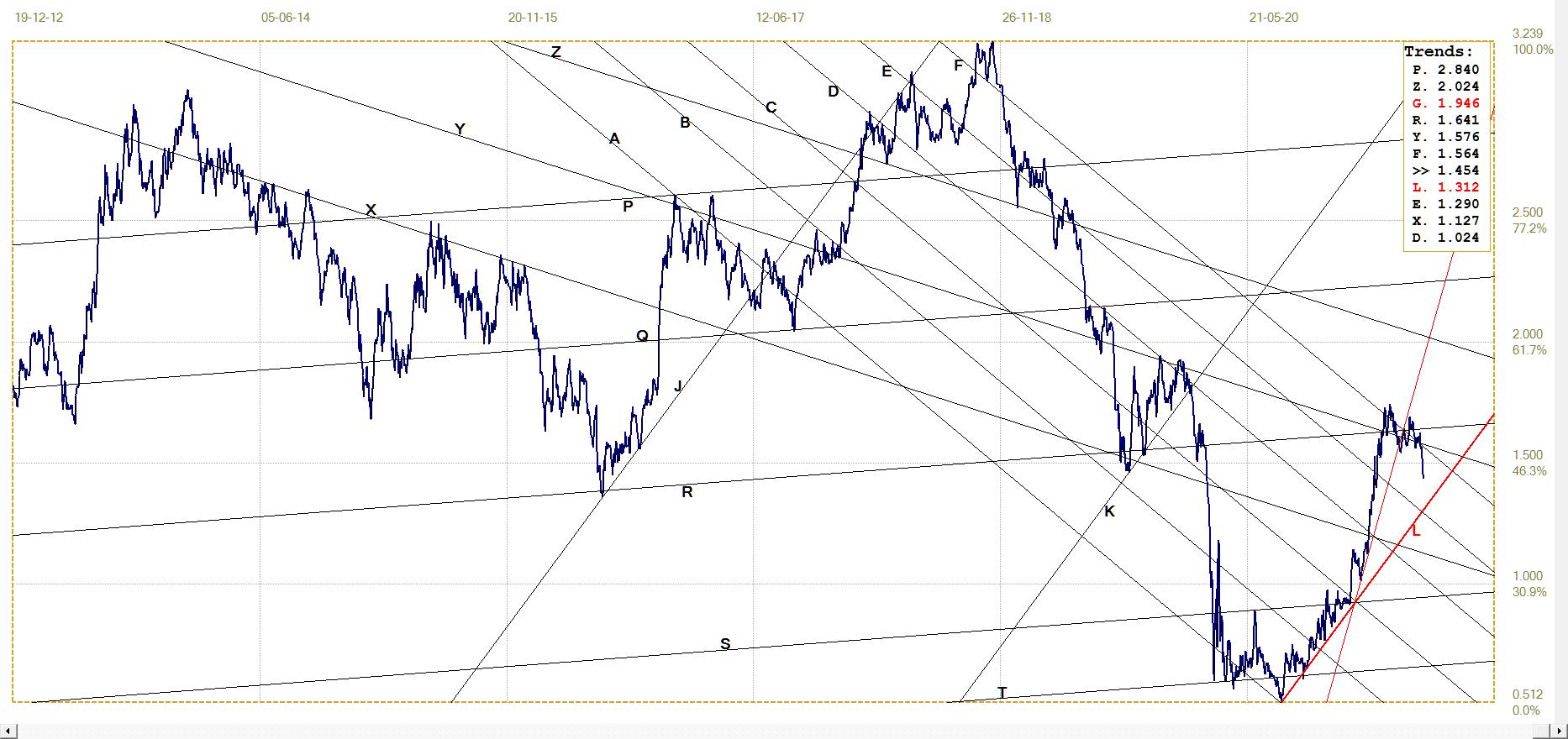

Euro–Dollar

Euro–dollar, last = $1.2105 (www.investing.com)

Last week saw the dollar reversing its on-off medium term weaker trend, which then had the effect of dragging the euro back below line C, after it had failed to hold onto a marginal break into bull channel XY. At the rate at which the dollar is being printed – with a $3 trillion deficit on the budget after only 8 months, apart from the exploding Fed balance sheet – one would expect the euro to break higher again. That is, except if the Euro community decides it can print an even greater volume of euros.

The currencies’ race to the bottom is such there can be no winner when the race ends – perhaps only a survivor or two.

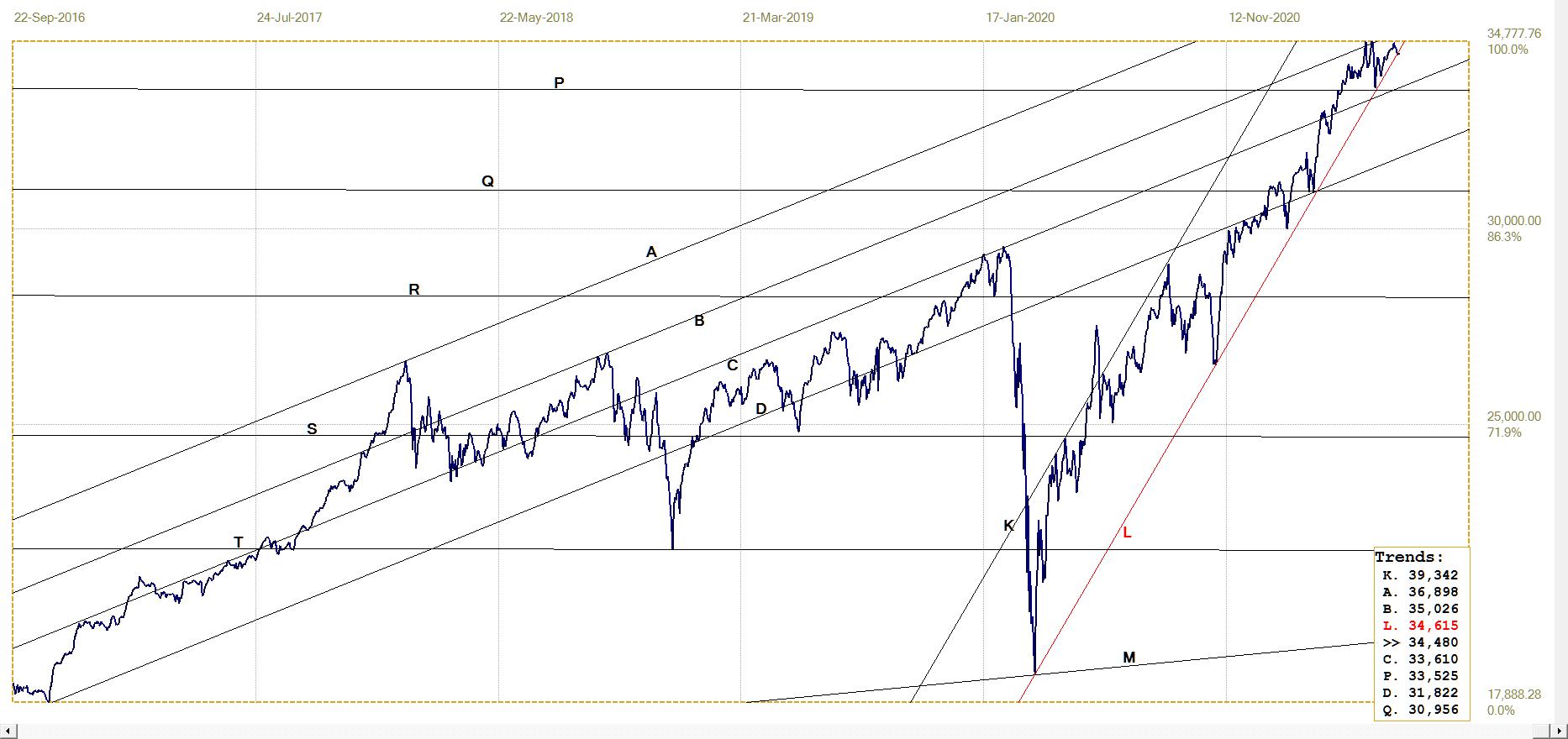

DJIA daily close

The DJIA is trying hard to set another new all time high. There is as yet no sign of any panic selling – volumes remain on the low side - but neither is there much determined buying to bring a new all time high within reach.

US households – the common man – are said to be more invested in equities than at any previous time. My guess is this fact will prove to be a contrarian indicator; one that will come into effect as soon as the flow of shiny new dollars dries up. When this happens, equities will be sold by many households to pay for food and energy.

DJIA. last = 34479.60 (money.cnn.com)

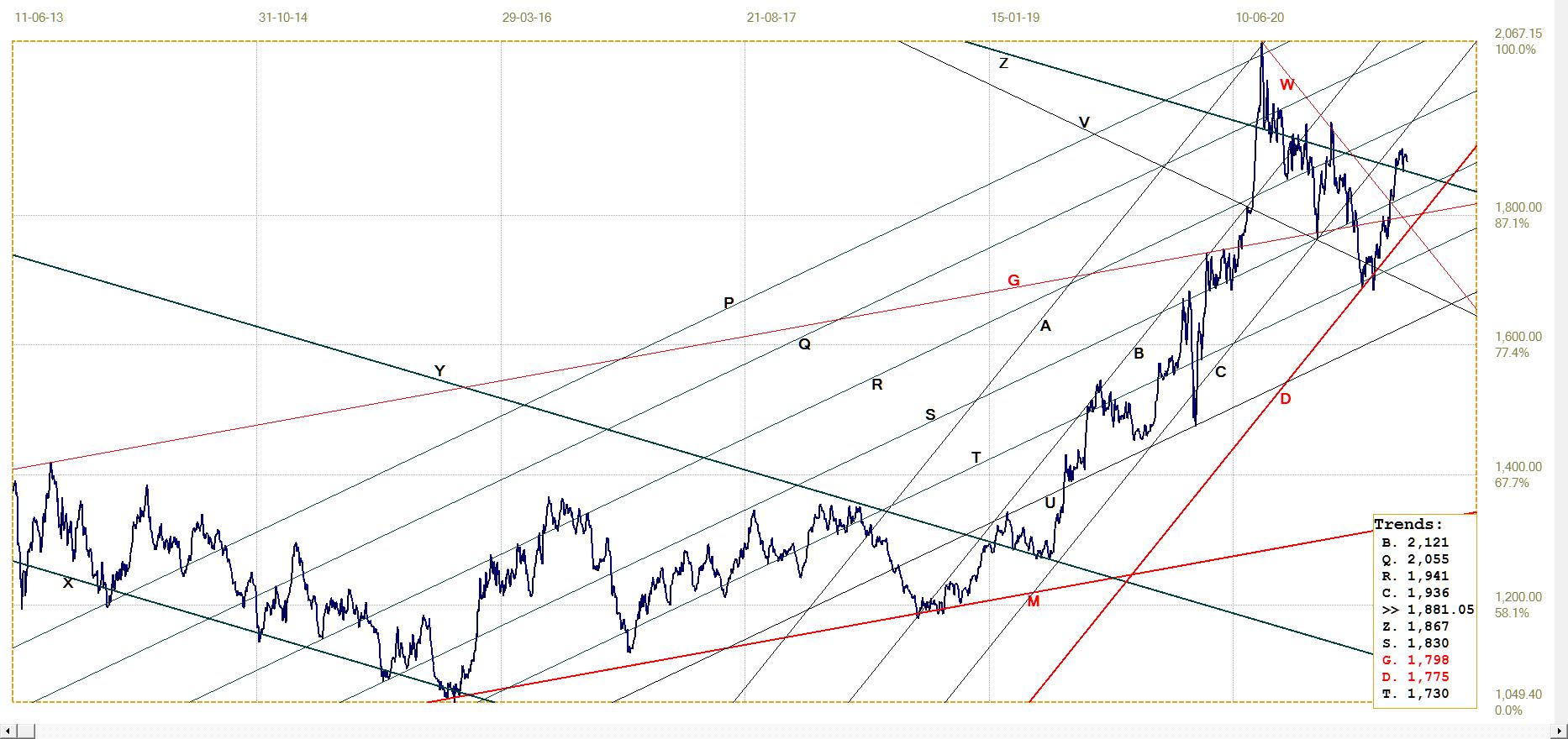

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1881.05 (www.kitco.com)

The break above resistance at line Z has held so far, despite a lacklustre performance by the price of gold under a firmer dollar, which acts as cover for a more determined cap that is being placed on the rally. Even so, as mentioned earlier, the Comex gold OI is nearly back at the level reached late in May, despite the loss of June contracts that did not end in the money. The focus of the Apes is on silver, but gold is not being completely neglected by the gold bulls, many of whom are waiting for the rally to break free of resistance at $1900 before stocking up further.

Euro–gold PM fix

The rally in the euro price of gold reached and then held a little below resistance at line D, which is seen as a breather after the sustained rally off lines L and X. There is some room for a sideways move, while gold is penned below $1900 and the dollar is trying to sustain its new and so far limited rally. Channel KL is not under pressure as yet and the future still looks good for the euro gold price.

Euro gold price – PM fix in Euro. Last = €1551.30 (www.kitco.com)

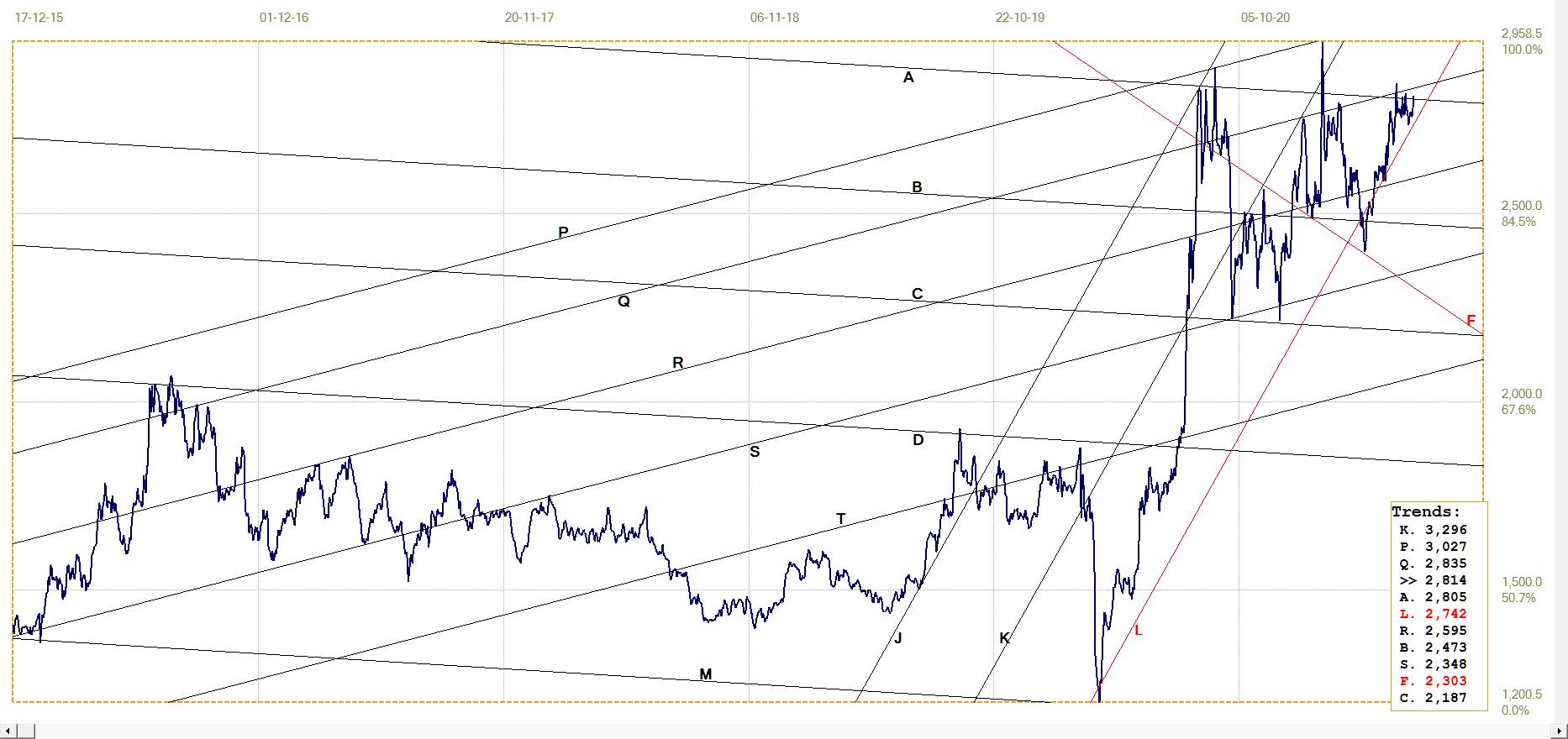

Silver Daily London Fix

The chart clearly shows how silver has repeatedly been trying to again break above the price ceiling at $28, which it had briefly done on four occasions now, the last being the London silver fix on Friday. None of the breaks higher were allowed to last longer than only one day – if that were to happen, silver bulls might be motivated to keep on buying and that is not something the Big Banks will allow to happen. However, the increasing silver OI may well force their hand during the next two weeks.

Silver daily London fix, last = $28.14 (www.kitco.com)

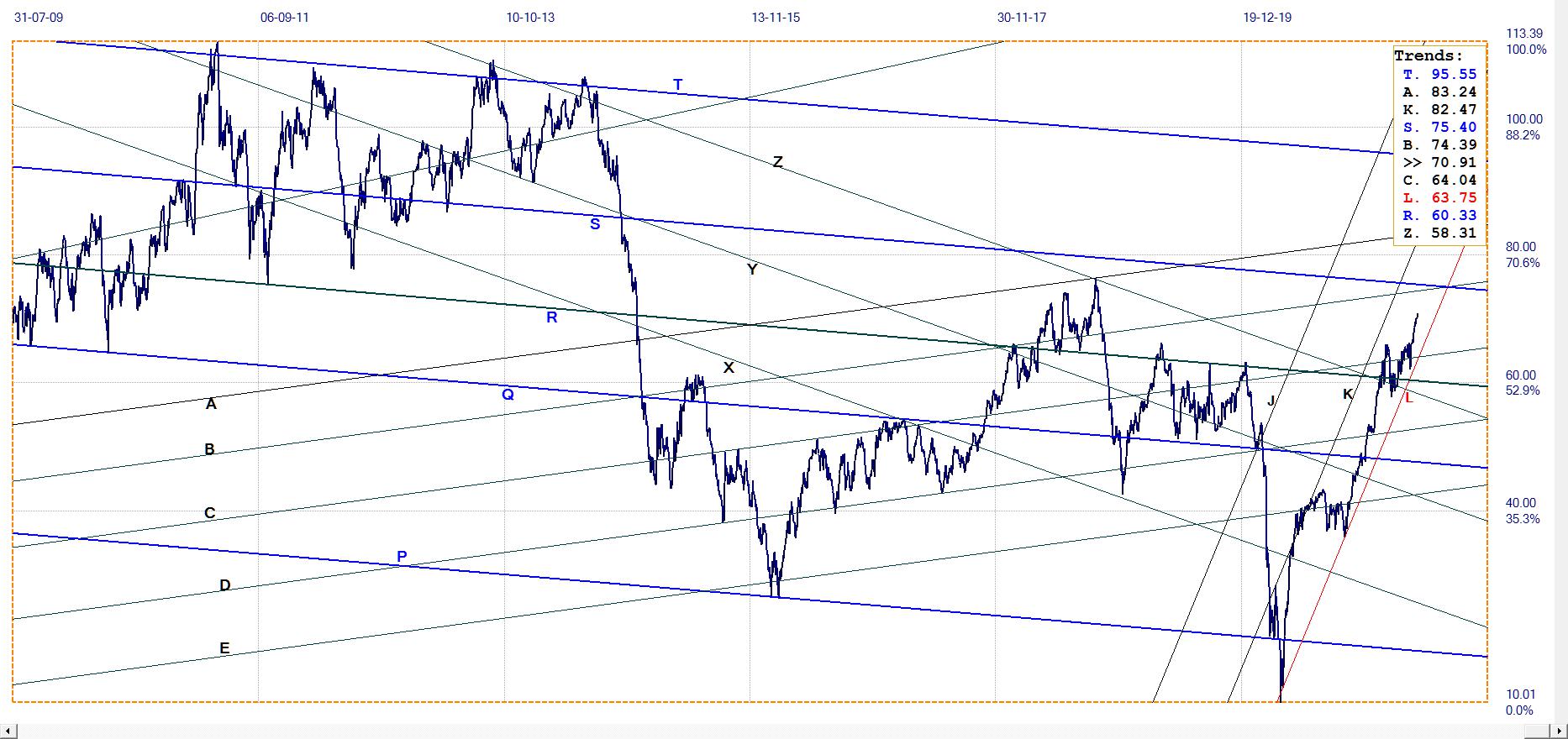

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 1.454% (www.investing.com )

Surprise, surprise! Old established economic principles are being overturned one after another. If it is not the de facto UBI (Universal Basic Income) that has been sneaked in under the radar, or an apparent allegiance to the MMT dogma that has taken over, then it is the apparent belief that higher inflation is bullish for bonds. Of course, that is unless the clout of Powell and Yellen is such that investors are preparing for the new bond rally that will happen when the transitory spike in the CPI is over soon.

As described earlier, this author, among many others, thinks we are back into the mid 1970s and that there will be a need for a reincarnation of Volcker to get the inflation under control again.

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $70.91 (www.investing.com )

Is the sudden jump in the price of crude only a transitory inflationary spike or does it warn that systemic problems are developing in the energy sector? The energy policy of the still new administration – or should it be their interim energy policies that are liable to change at short notice – does not seem to have a single well-defined umbrella objective. The term, ‘Climate change’, is frequently heard when energy is discussed, but the gist of the references implies that fossil energy is bad for the US and the rest of the world – but excluding Europe where the Nordstrom pipeline is a good thing for them and for Russia.

The cost of energy is such a pervading factor for the overall economy that this new spike in the price, should it not be transitory, is going to make it more difficult to ‘contain’ the CPI when it gets calculated next month.

********

More from Gold-Eagle