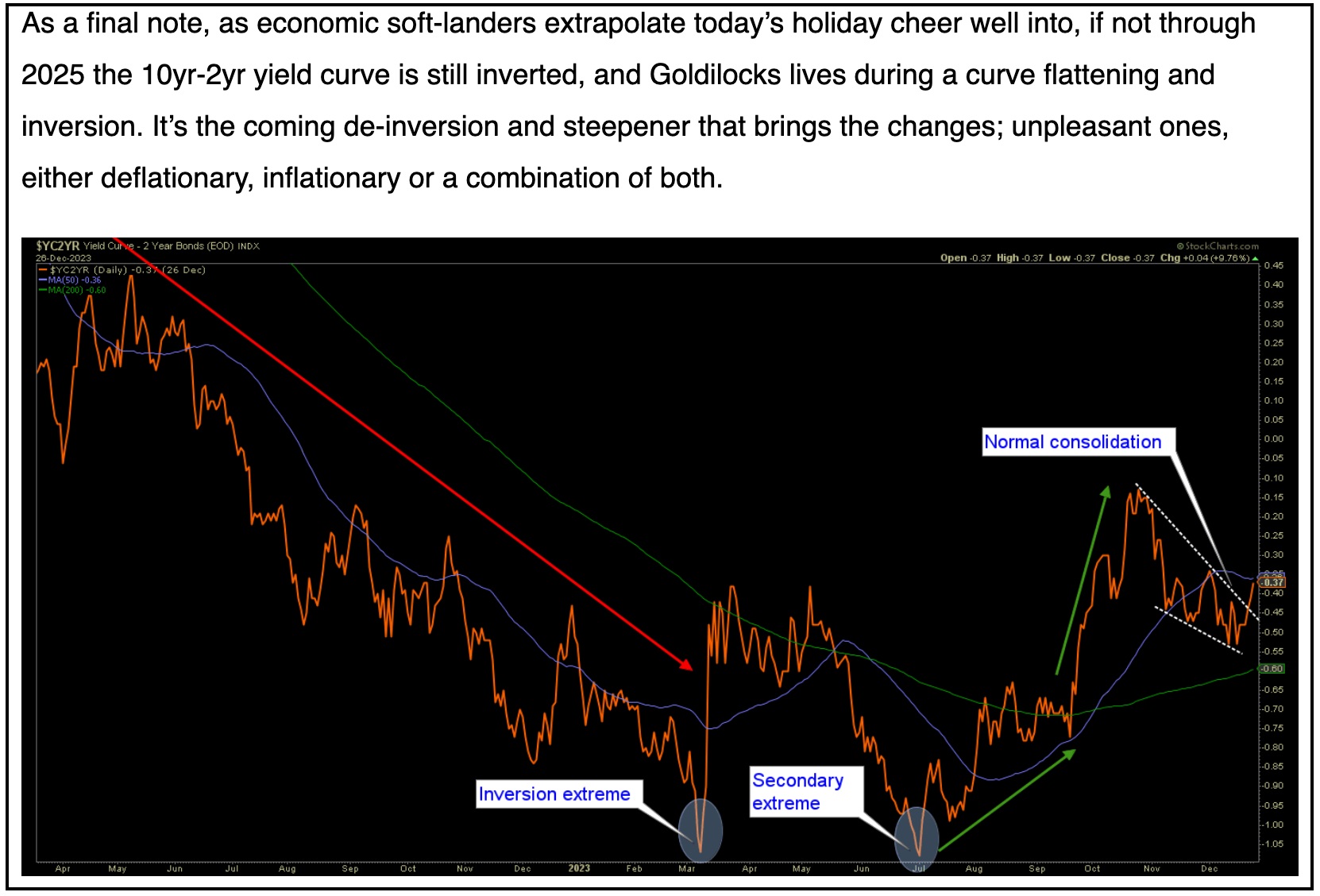

Inflationary Yield Curve Steepening?

After a gentle disinflationary easing (Goldilocks), the bond market is hinting at an inflationary steepening of the 10yr-2yr yield curve

A yield curve can steepen under inflationary or deflationary pressure.

Inflationary: Generally, long-term yields rise in relation to short-term yields as both rise nominally, or more importantly long-term yields rise nominally.

Deflationary: Short-term yields decline in relation to long-term yields, as both decline nominally.

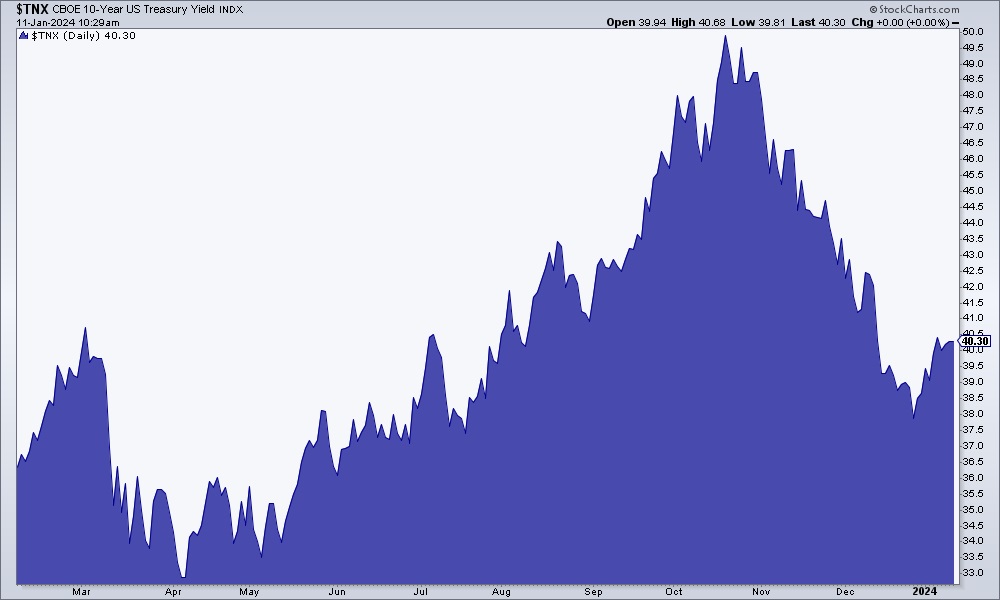

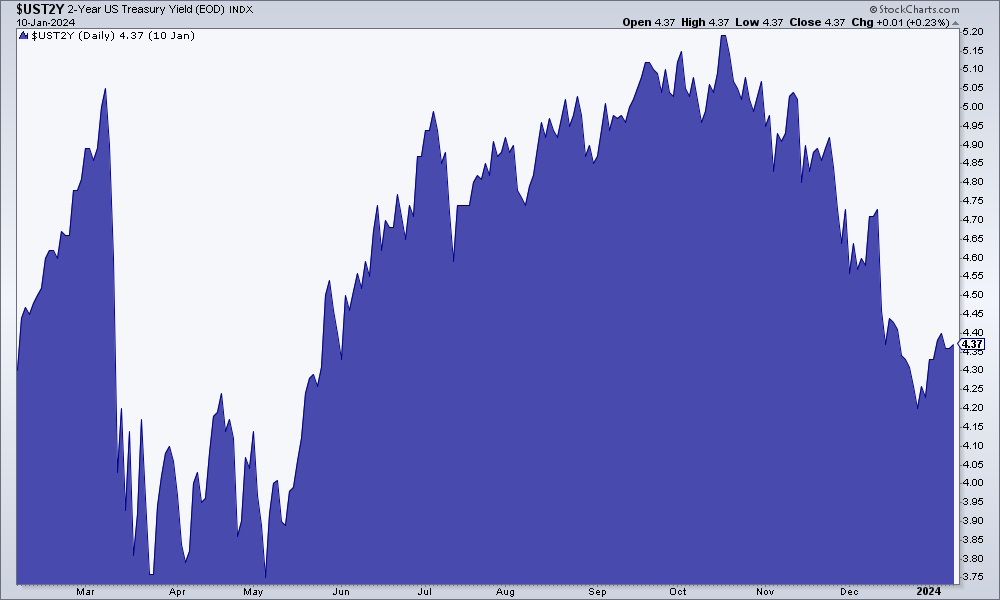

Thus far during the Goldilocks phase from the stock market lows in October, the signal has been disinflationary relief as the 10 year Treasury bond yield dropped from near 5% to 3.8%.

The 2 year Treasury bond yield has also dropped from the October high.

The yield curve, which is the product of the two yields above, shows the steepener still in progress after we noted in last week’s public article that the recent Goldilocks-friendly easing in the curve was merely a consolidation on the way to further steepening.

Today the break from consolidation is furthered and the steepening continues. It continues with the nominal yields shown above rising. Hence, a little inflationary hint that will obviously need follow through in order to play out.

cnbc.com (my markups)

The decline in yields from October to December represented the best Goldilocks had to offer in 2023 as our original thesis of pleasant disinflation played out, Goldilocks style, at various times in 2023. It was a perfect accelerant for the anticipated seasonal (Q4) party atmosphere, built on relief from a hawkish Fed as inflation signals faded from the macro.

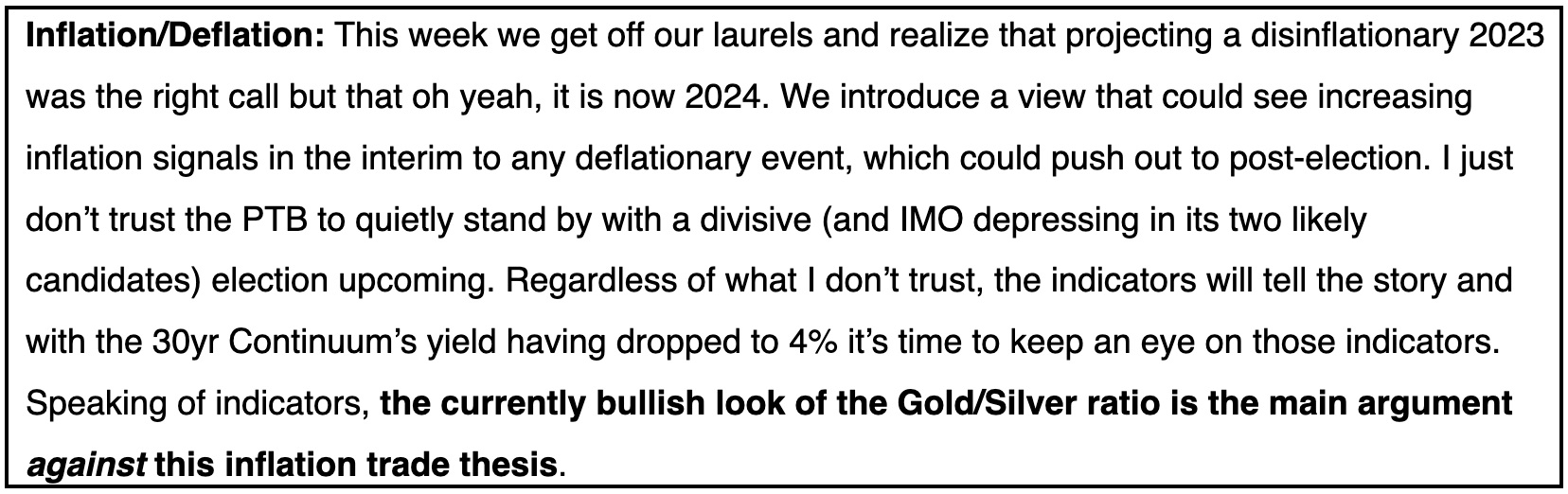

Last weekend in NFTRH 791, we began a very preliminary theme whereby the writer did not want to get caught in a self-congratulatory feedback loop, due to the correct disinflationary/Goldilocks call a year ago. With the caveats of a still-bouncing US dollar and a bull-poised Gold/Silver ratio, the following was noted in the report’s opening Summary segment:

As always, there is much more to be factored than one public article can illustrate. But 2023 was disinflationary, on cue, and today’s soft-landers and Goldilocks adherents were the inflation-phobes of a year ago. You see? Some aspects are coming into play for an unexpected – if interim to a real deflation phase – inflationary phase. I am sure fiscal authorities will stand ready in support to try to boost the incumbent party in power, and the only trick in their book is and has been, fiscally stimulated inflation. With the Fed sitting soft on the sidelines, that in itself would also be a tailwind. A hard deflation could be pushed out until post-election.

The strategy? We will manage that weekly in NFTRH reports and during the week in NFTRH+ updates. But consider this; what are commonly referred to as the “inflation trades” in commodity and resources related speculations, have already been hammered, much like the 2020 disinflation stuff like ARK funds and Cloud/SaaS got croaked prior to Goldilocks, which re-lifted those boats. If the macro flips inflationary – even if only for a phase – the nearly sunken ‘inflation trade’ boats could sail again… for a phase, at least.

It is still very preliminary analysis. But my spidey sense says ‘Gary, don’t over-stay your disinflationary view’. Now let’s see if the indicators back that notion up. If the yield curve resumes its steepening as expected and if that steepening is inflationary, as has been the little hint since mid-December, those confident about a Goldilocks style soft landing will be disappointed and maybe even those willing to deploy trades in the opposite direction of 2023’s disinflationary backdrop may find success.

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. Subscribe by Credit Card or PayPal using a link on the right sidebar (if using a mobile device you may need to scroll down) or see all options and more info. Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter@NFTRHgt.

********