Interest Rates Rise Again as Treasury Auction Comes Up Short

The US government is on track to borrow more than two trillion dollars this year, but that’s going to require a lot of new loans from investors, and it’s looking like there is limited investor appetite for ever larger amounts of federal Treasurys. On Wednesday, the auction of 20-year Treasury bonds was so weak that the 20-year yield climbed to over five percent, and long-dated debt yields hit levels not seen since November 2023.

It’s likely no surprise that this tepid demand for new US Treasurys coincides with recent news that Donald Trump’s so-called “big, beautiful” spending bill does nothing to cut overall spending and will only add to the federal deficit—at least $3 trillion more—in coming years.

(Bond yields move opposite bond prices, so rising yields indicate falling demand (and falling prices) for Treasurys.)

Barron’s provides some historical context on Wednesday’s auction:

The Treasury Department sold $16 billion of newly issued 20-year bonds at 1 p.m. Eastern. It’s routine for the Treasury Department to borrow to fund the government. This auction, however, saw heightened interest as investors worried that increased uncertainty about the U.S. economic policies would lead to less demand for the Treasuries. Their fears were spot on.

The auction saw investors accept a yield of 5.047% on the 20-year note, compared with the past six auctions’ average of 4.613%. It was also 0.011 percentage points higher than the yield seen before the bidding deadline. This was the first time the Treasury sold a 20-year note with a rate over 5% since October 2023. Back in the pandemic, it could sell its 20-year debt at 1.22%. Higher rates signal that demand is weak, as the Treasury has to entice investors with higher yields to buy U.S. debt.

Since the auction results, the 20-year Treasury’s yield jumped to its highest levels for the year at 5.103% on Wednesday....The 30-year yield was also trading at its highest point for the year at 5.071%.

This should be very worrying for the federal government since today’s auction suggests that there are indeed limits to just how much new debt investors are willing to absorb at the “usual” low-low interest rates. Rather, as it becomes increasingly clear that the Trump administration has no interest in cutting spending to slow the rising tide of federal debt, investors expect the federal government to only increase the amount of new Treasury bonds it dumps into the market. As markets see a rising supply of debt, there’s good reason to expect the price to drop—and thus drive yields higher.

This seems to be exactly what happened at Wednesday’s auction. Moreover, a lack of demand meant the Federal Reserve had to step in to buy up nearly $2.2 billion of the $16 billion bond issue.

Not that buying up Treasurys is unusual for the central bank. The Fed routinely engages in bond purchases for a variety of reasons, including efforts to increase liquidity and add monetary stimulus. The Fed also buys bonds for purposes of managing Treasury yields, however. In the current context, the need to prevent yields from getting out of hand is almost certainly among the motivating factors behind the Fed’s bond purchases on Wednesday. After all, Wednesday’s bond purchase comes after the Fed, last week, bought up more than $40 billion in Treasurys. Marketwatch reports:

The U.S. Federal Reserve just pulled off something stealthy — over four days last week, without fanfare, the Fed vacuumed up $43.6 billion in U.S. Treasurys. That’s $8.8 billion in long-dated 30-year bonds on May 8 alone, plus another $34.8 billion earlier in the week. Not exactly small change.

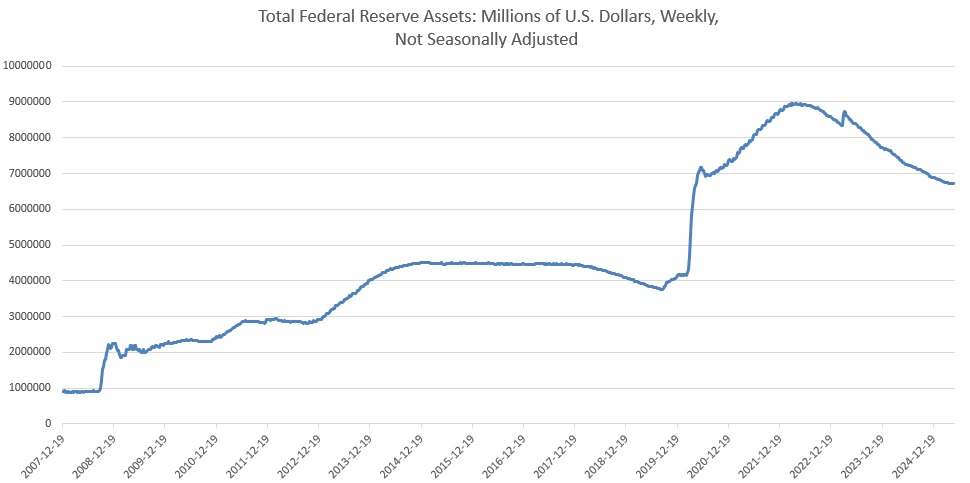

Some observers might argue that this is nothing special, and it’s all part of the Fed’s management of its enormous, $6.7-trillion balance sheet.

Recall that since mid-2022, the Fed has slowly been allowing its assets to roll off the Fed’s balance sheet, which in 2022 had peaked at $8.9 trillion. After the 2008 financial crisis, and again during the Covid Panic, the central bank bought up trillions of dollars’ worth of mortgage backed securities and US treasuries. This was done to drive up asset prices in real estate, and also to prevent rising yields in Treasurys as the federal government was recklessly piling on trillions in new deficit spending in a matter of several months. Since then, the pressure of price-inflation has pushed the Fed to slowly reduce its assets, which has a deflationary effect similar to that of allowing interest rates to rise.

So, are the Fed’s recent bond purchases all just part of the usual orderly portfolio management? Not really. The claim that this is all business as usual would be more convincing were it not for the fact that the Fed has greatly reduced its reductions in total Treasury holdings on the Fed’s balance sheet.

In March, for example,

the FOMC announced that the Committee would further slow the pace of decline of its securities holdings, consistent with its Plans for Reducing the Size of the Federal Reserve’s Balance Sheet. Beginning on April 1, 2025, the Committee reduced the monthly redemption cap on Treasury securities from $25 billion to $5 billion, further slowing the pace of runoff after reducing the cap from $60 billion to $25 billion in June 2024.

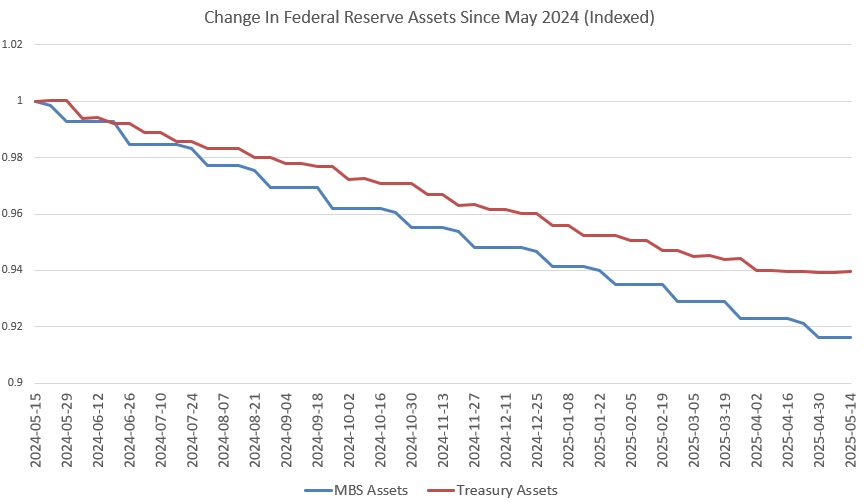

Note that the Fed has repeatedly adjusted its policy over the past year so the reductions in the balance sheet are overwhelmingly focused on mortgages while the Fed finds new ways to hold on to Treasurys, thus minimizing a negative impact on Treasury prices. One could certainly read this as an indication that the Fed is primarily worried about avoiding any fast reductions in Treasury prices.

Indeed, if we look at total Treasury holdings at the Fed in recent months, the Fed’s Treasury holdings have all but stopped getting smaller while mortgage-backed securities continue to fall:

It is not surprising at all, however, that the Fed would choose to prioritize manipulating Treasury prices and yields through its balance sheet holdings. It has long been understood (unofficially) that the Fed will intervene to push down the cost of US Treasuries to the US government by forcing down yields through bond purchases. This was clearly the policy during the Second World War, and was a policy implemented with a wink and nod during the Cold War as well. As total debt mounts, the central bank is expected to step in and ensure that Treasury yields don’t get out of hand. A key tool in this is Fed purchases of Treasurys.

This is great for the US government since a partnership with the Fed to suppress Treasury yields reduces borrowing costs for the US government. After all, as yields go up, the US government must spend more and more of its revenues just to keep up with interest payments. The US Treasury needs the Fed to reduce the impact of interest payments since rising interest forces Congress to divert spending from popular political programs. (There is also the risk of a sovereign debt crisis in extreme cases.)

If history is any indicator, the Fed will happily oblige. Unfortunately, there is a downside for regular people. The Fed generally purchases bonds with newly created money, so an ongoing policy of adding Treasurys to the Fed’s portfolio will put upward pressure on price inflation. This was a significant factor in the price inflation that reached 40-year highs during 2022.

It looks like Donld Trump’s spending policies will drive enormous amounts of ongoing deficit spending, and this will probably hit $4 trillion per year within the next four years. This will require the US government to dump enormous amounts of new Treasurys into the market in coming years. Will there be enough demand from investors to prevent a sizable increase in yields (and, therefore, a sizable increase in interest costs)? If Wednesday’s auction is any indication, there is good reason for the Fed and the federal government to be worried.

Courtesy of Mises.org

********