Market Turning Points

Current position of the market

SPX: Long-term trend – In 1932 and 1974, the 40-yr cycle was responsible for protracted market weakness. The current phase is due this year but where is the weakness? Has man (Federal Reserve) finally achieved dominance over universal rhythms or has it simply delayed the inevitable?

Intermediate trend – We are looking for the move from 1905 to end, after which a much more serious correction should start. (It has probably started!)

Analysis of the short-term trend is done on a daily basis with the help of hourly charts. It is an important adjunct to the analysis of daily and weekly charts which discusses the course of longer market trends.

ODDS FAVOR MORE WEAKNESS AHEAD!

Market Overview

After a 9-day correction which spanned nearly 100 SPX points, the short-term, oversold condition assisted by Friday’s good employment report triggered a sharp rally which retraced nearly half of the entire decline in one day! Is the decline over (for now)? We’ll find out next week! While SPX retraced nearly 50% of its decline, it was the exception rather than the rule. A number of indices only bounced .382 or less, capped by the Global Dow which only retraced 14%. If the decline is over, the least we can do is to re-test last week’s low. Of particular concern is the Global Dow, the weakest of the lot, which we will discuss a little later. Let’s analyze some key points.

Momentum: The weekly and daily MACDs both made a new low last week. The daily also went negative for the first time since the beginning of the decline. The weekly is still positive, but it did break below the August low while the daily is still slightly above. Last Friday’s rally prevented it from making a new low (for how long?). In spite of the strong rally, the hourly could only get up to neutral. Let’s see what happens when it turns down again.

Breadth: The McClellan Oscillator remained negative at Friday’s close, even with the strong rally. Surely, this cannot be a good sign for the bulls. Strong rallies normally begin with a strong breadth thrust. As a result the McClellan Summation Index made another low.

VIX: Surpassed its August high by a fraction but the strong rally caused it to reverse sharply. Nevertheless it managed to stop well above its 200-DMA, which is a bullish sign (bearish for the market).

Structure: The belief that primary wave III had ended and that primary wave IV had started increased sharply as a result of last week’s action, although this still cannot be objectively confirmed. It would take a decisive break below 1905 to say for sure. By that definition, we would have to say that IWM and MID already have and that NYA just barely failed to do so (assuming they have a similar structure).

Accumulation/distribution: The first phase of the SPX decline (the minimum decline projection) stopped at a P&F/Fib projection combo. Practically the same thing can be said of Friday’s rally which has either reached a completed phase or nearly so. If we break below 1905 it will trigger much lower projections.

Cycles: It is very possible that the low point of the long-term Kress cycles were simply delayed by the Fed’s easy money policy. In that case, it will be a little more difficult to pin-point their lows and we should let the market do it for us.

Chart Analysis

I want to start by comparing one of the strongest indexes (DJIA) to two of the weakest (GDOW and IWM). These are weekly charts (courtesy of QCharts.com).

The DJIA (left) shows that its 2007 high was around 14200 -- much lower than the level attained in 2014. The IWM (Russell 2000 ETF -- right) shows that its 2007 high was around 86, also much lower than its 2014 high. However, the 2014 high of the GDOW (Global DOW) was significantly lower than its 2007 high making it the weakest of the three indices on a long-term basis. For 2014, at one time the Russell 2000 was one of the strongest indexes, but it made an initial high in March (red V), essentially double topped in June, and made a much lower high in October. That makes it one of the weakest indices since early 2014.

Of the early August lows made by all three indices, we can see that only the DJIA managed to stay above it and by a fairly substantial margin. The two others have broken below it decisively.

Another way to assess the comparative relative strength of the three indices is to look at where they are priced relative to their 30-wk MA. Until it was broken, this MA did a pretty good job of containing the rising trend. Now, just last week, the two weakest ones have broken and closed well below it. This is important because it suggests that the downtrend may only be getting started.

One final way of comparing the relative strength of these indices (and others) is to see how far they bounced after last week’s weakness, measuring from their 2014 highs. While the DOW retraced 50% of its decline, the other two stayed below 20%.

What can we deduce from the above? First, that the US stock market may be entering a correction the likes of which has not been seen for a while. If we have indeed started primary wave IV, it would not be unreasonable to expect something of the magnitude of wave II, which was 250 points. Of course, if the decline stops (or has stopped) on a dime and we start up again, then all bets are off! The Russell 2000 is telling us that this is unlikely. It has patiently waited for the other indices to finish their exuberant uptrend, and it now appears ready to lead them lower. Already, the NYA and the MID have joined it at a level comparable to below the SPX 1905.

But the GDOW is telling us an even more negative story by 1) by staying well below its 2007 top, and 2) by quickly and decisively reversing its 2014 uptrend. This is what could be called a double negative for the market. For those who are not familiar with the Global Dow: it is made up of 150 blue chip corporations from around the world, including the 30 Dow industrials as well as some stocks taken from the Dow transportation and utilities indexes. While the New York Stock Exchange Index, which is comprised of more stocks than just about any other, has already signaled an intermediate downtrend which could be forecasting some unpleasant economic news about the US, the Global Dow is saying it even more emphatically, and this is bound to have additional repercussions on our own economy.

We’ll now look at the daily SPX chart (courtesy of QCharts.com) to see what it tells us.

Earlier, I mentioned that the decline reversed when we reached a projection level determined by both P&F and Fib. That level also marked the low of a correction made in June, which coincided with the parallel to a line drawn across the tops. Note that a deceleration channel has formed and this nearly always marks the advent of trend correction. Although the decline penetrated the trend line from 1343 by a wide margin, and even closed below it for two consecutive days, the next day’s rally took it right back inside by just as wide a margin. For a conclusive break of this important trend line, the SPX would have to close below it again, and follow that with a new low.

The SPX, like the DJIA, has retraced about 50% of its 2-wk decline all in one swoop. We know that (although we are not yet in a bear market) bear-market type rallies can be very sharp, but they have no staying power and prices come back down very quickly. We had an example of this on 9/24 when a 20-point rally was followed by a much larger decline the next day. Is this what lies ahead? Whatever it may be, we’d better be prepared.

In spite of two consecutive days of strong rally, none of the daily indicators have given bullish readings. Even the A/D oscillator (bottom) failed to make it into positive territory. The only way that we could get some bullish indication out of Friday, would be with a strong follow-through on the upside.

The hourly chart (also courtesy of QChart.com) has the same parallels and longer term trend lines drawn on the daily. In addition, channels which encompass the downtrend are drawn. On Friday, the rally stopped at an area of overhead resistance marked by several trend lines and parallels. If it goes a little higher on Monday, it will run into even thicker resistance as well as the 200-hr MA. That should provide too much for prices to go through all at once, even in a strong uptrend, and a pull-back – which could become much more – should take place.

Note that the oscillators are overbought and are beginning to curl down. The MACD is still in a strong uptrend, but it has only reached the zero line, and the histogram is also turning down. All this is indicative of at least a pause in this area, and perhaps more.

Breadth

The McClellan Oscillator and the Summation Index appear below (courtesy of StockCharts.com).

If there ever were two indicators which exemplified the internal weakness of the market, these two do.

First, think of the kind of rally that we had over the past two days. Now compare the last three times that the McClellan Oscillator dropped to the green line or below and how it rallied from it, to the current anemic upward move.

As for the Summation Index, it is still probing for a bottom at minus 300 and it is now challenging the August 2013 lows!

Sentiment Indicators

The SentimenTrader (courtesy of same) long term indicator has dropped to a neutral 50. It too seems to be waiting for the market to decide in which direction to go next

VIX (NYSE Volatility Index) - Leads and confirms market reversals.

VIX made another attempt at breaking out of its corrective channel, but did not quite make it. It did achieve a fractional new high above its last short-term top (the equivalent of 1905 SPX) but pulled back immediately leaving the break-out question unresolved and put off until next week.

IWM (iShares Russell 2000) - Historically a market leader.

To say that IWM is at a critical technical juncture would be an understatement! By breaking below its August low, it has confirmed a short-term downtrend, and if it closes decisively below the January low, it will have confirmed an intermediate downtrend. Certainly the entire formation from January looks like an important (double) top. This index remains one of the weakest, if not the weakest of the lot. Holding this level is critical to what the market will do over the next week or so. If it has a substantial extension of its downtrend, it should confirm that an intermediate market correction has started.

TLT (20+yr Treasury Bond Fund) – Normally runs contrary to the equities market.

TLT has shot back up inside its uptrend channel, but it is not certain that it can immediately proceed to making a new high, although it looks capable of extending its move to 122. If it did so immediately, it would be because the market is continuing to decline.

GLD (ETF for gold) – runs contrary to the dollar index

As long as the dollar remains in a strong uptrend, GLD should continue to decline. Presently, it looks like it’s making a bee line for its 25-wk cycle low (green arrow), though it may have a chance to hold on to 115 a little longer.

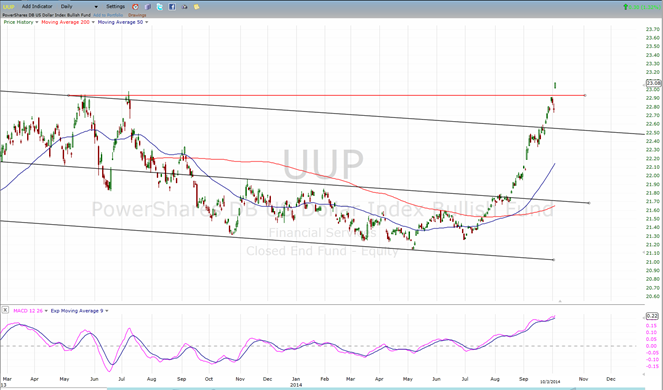

UUP (dollar ETF)

Can the dollar continue to surge without pausing for a consolidation? It’s unlikely and the former tops, even though they have been penetrated, could provide an opportunity for a well-deserved rest.

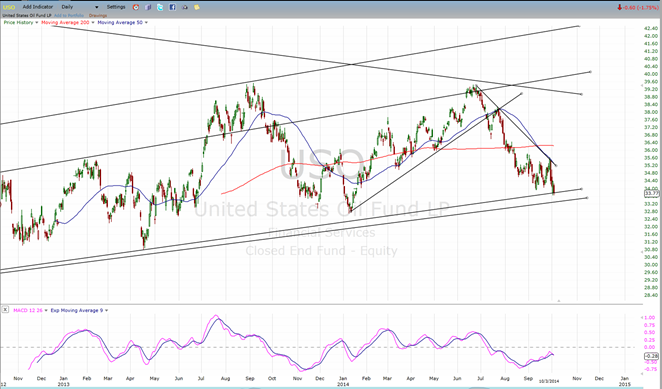

USO (US Oil Fund) (following chart courtesy of QCharts.com)

Like GLD, USO is pretty much at the mercy of the dollar. In addition, a developing oil glut is affecting its fundmentals. That does not provide any reassurance that USO will be able to hold above its long-term trend lines.

Summary

Friday’s rally in the strongest indices has created a cloud of uncertainty as to whether or not the SPX has started an intermediate decline. However, the strong rally was not shared by the weaker indices, some of which even failed to retrace .382 of their recent decline.

In the past couple of weeks, I mentioned that there was a developing tug-o-war between strong and weak indices and that we should wait to see who wins the contest before making a final forecast. What we can say is that since then, the strongest and the weakest have both become weaker. Friday’s rally could be a last-ditch-stand by the strong indices to put off the inevitable for another day.

A final judgment could come as early as next week.

********

FREE TRIAL SUBSCRIPTON

Market Turning Points is an uncommonly dependable, reasonably priced service providing intra-day market updates, a daily Market Summary, and detailed weekend reports. It is ideally suited to traders, but it can also be valuable to investors since highly accurate longer-term price projections are provided using Point & Figure analysis and Fibonacci projections. Best-time reversal estimates are obtained from cycle analysis. An increasing use of EWT for structural analysis and the recent addition of CIT (Change In Trend) time slots has greatly improved the exact timing of reversals.

For a FREE 4-week trial, send an email to: [email protected]

For further subscription options, payment plans, weekly newsletters, and for general information, I encourage you to visit my website at www.marketurningpoints.com. By clicking on “Free Newsletter” you can get a preview of the latest newsletter which is normally posted on Sunday afternoon (unless it happens to be a 3-day weekend in which case it could be posted on Monday).

The above comments and those made in the daily updates and the Market Summary about the financial markets are based purely on what I consider to be sound technical analysis principles. They represent my own opinion and are not meant to be construed as trading or investment advice, but are offered as an analytical point of view which might be of interest to those who follow stock market cycles and technical analysis.

When Andre Gratian was a stock broker years ago, a friend introduced him to technical analysis of the market. Consequently, it is not an exaggeration to say that Andre fell in love with this approach! Ever since then, it has become an increasingly important part of his professional life. Gratian has studied the works of Wyckoff, Edwards & Magee, Edward J. Dewey (cycles) and many others. However, one of my most profitable undertaking has probably been to study Point & Figure charting, which he finds invaluable in analyzing stocks and indices. If he were restricted to one methodology, this is the one that he would choose. This well-rounded background has given him what he feels to be a special insight into the stock market, facilitating the recognition of meaningful patterns and the ‘turning points’ in all trends, whether they be short or long term. Andre feels very comfortable discussing the stock market and passing on meaningful information to others. His subscribers include individuals and money managers throughout the world. Moreover, his Newsletters are currently published on several financial sites, here and abroad.