May CPI Ratchets Up Pressure on Fed to Return to Inflation

The May CPI report is ratcheting up pressure on Jerome Powell and the Federal Reserve to cut interest rates.

In other words, the perception that the inflation problem is solved is raising the specter of more inflation.

In a social media post on Wednesday, Vice President JD Vance joined President Trump in publicly calling for the central bank to cut interest rates.

“The president has been saying this for a while, but it’s even more clear: the refusal by the Fed to cut rates is monetary malpractice.”

Trump has been badgering Powell about rate cuts for months. After the jobs report last week, Trump urged the Fed, “Go for a full point, Rocket Fuel!”

Trump, Vance, and others recognize the stimulative impact of artificially low interest rates. They understand that the debt-riddled economy is laboring under even the modestly higher rate environment today. Trump alluded to this in a follow-up post on Truth Social, posting, “If ‘Too Late’ at the Fed would CUT, we would greatly reduce interest rates, long and short, on debt that is coming due.”

But Trump, Vance, and other advocates of rate cuts are ignoring the inflationary impact of looser monetary policy. In the same post, Trump insisted, “There is virtually no inflation anymore.”

The May CPI report supports Trump’s claim.

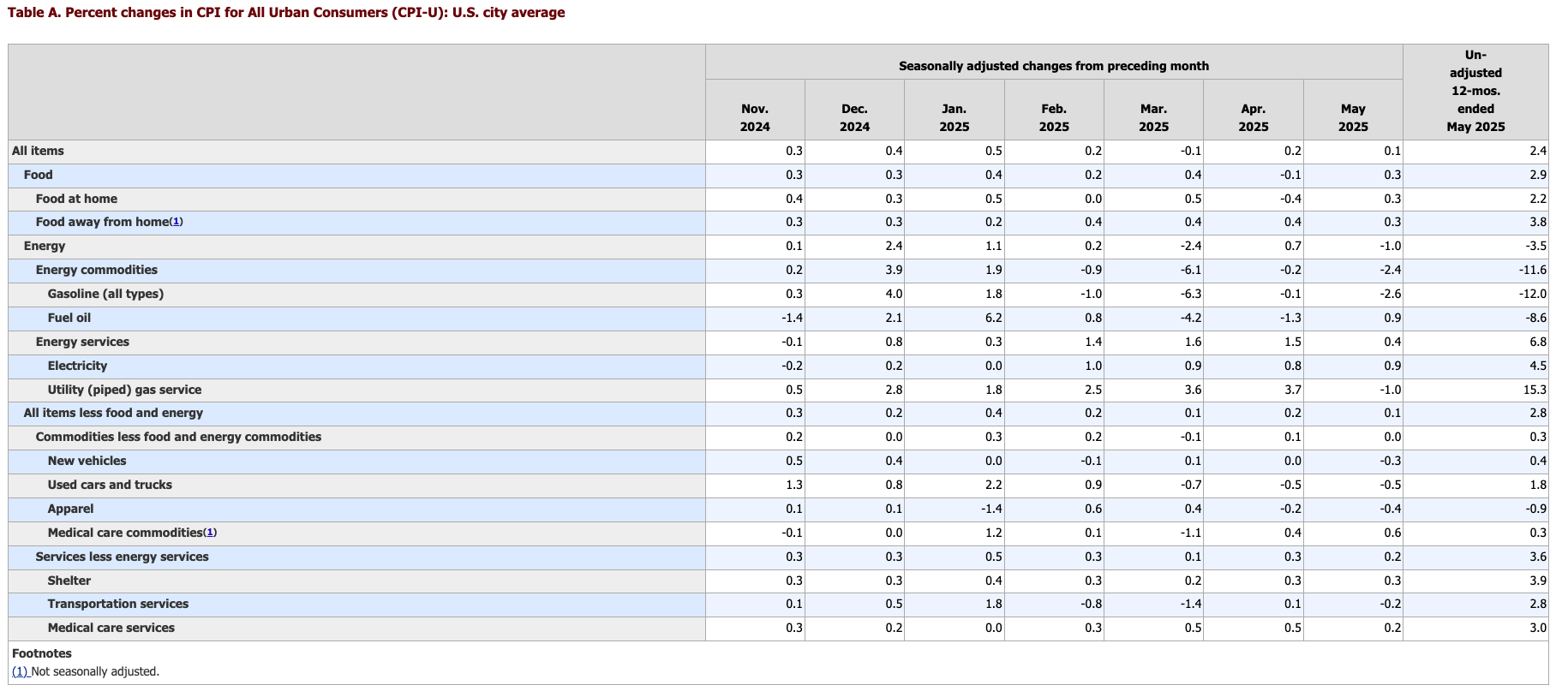

May CPI By the Numbers

The headline annual CPI number rose from 2.3 percent in April (revised down from 2.4 percent) to 2.4 percent last month, according to the latest data from the BLS. Still, everybody fixated on the modest 0.1 percent monthly rise in prices. The forecast was for a 0.2 percent monthly gain.

Stripping out more volatile food and energy prices, core CPI also rose by a modest 0.1 percent month-on-month. On an annual basis, core CPI remained at 2.8 percent. Both numbers were better than expectations. The forecast was for a 0.3 percent month-on-month rise and a 2.9 percent annual core CPI reading.

April was the first time core CPI had dropped below 3 percent since March 2021.

As you parse the data, keep in mind that the CPI doesn’t tell the entire story of inflation. The government revised the CPI formula in the 1990s so that it understated the actual rise in prices. Based on the formula used in the 1970s, CPI is closer to double the official numbers. So, if the BLS used the old formula, we’d be looking at CPI closer to 6 percent. And using an honest formula, it would probably be worse than that.

However, this is the formula the government uses, and it drives decision-making.

It is also important to note that a federal government hiring freeze has reportedly stretched the BLS thin, and the agency recently reduced data collection and expanded a process known as “imputation,” which uses modeling to fill in incomplete data. In April, the BLS announced it was “reducing sample in areas across the country” and suspended data collection in Lincoln, Nebraska; Provo, Utah; and Buffalo, New York.

Looking deeper into the May BLS data, falling energy prices continued to pull the overall CPI lower. The energy index dropped a full 1 percent, with gasoline prices falling 2.6 percent.

This helped balance out a 0.3 percent increase in food prices and a 0.2 percent monthly jump in services.

While the CPI boosted optimism at the White House and among investors desperate for their easy money drug, many analysts remained wary of tariff-related price increases still in the pipeline.

Principal Asset Management chief global strategist Seema Shah told CNBC that the CPI report was “reassuring, but only to an extent.”

“Tariff-driven price increases may not feed through to the CPI data for a few more months yet, so it is far too premature to assume that the price shock will not materialize.”

Meanwhile, Fed watchers assign close to a zero percent chance that the central bank will cut rates at the June meeting next week.

They Are Calling for More Inflation

It’s important to emphasize that Trump and others are calling for more inflation. I’ve been harping on this point for months – beating inflation is losing. Falling price inflation greenlights a return to the inflationary policies that got us in this position to begin with.

This is all possible because of a wildly successful campaign to redefine inflation. Americans generally only understand half the inflation story. They think that inflation means rising prices. But price inflation is a symptom of monetary inflation (an expansion in the supply of money and credit). In the 70s, that’s what people meant when they used the term inflation.

Lots of things can cause some prices to rise (tariffs, for example). Only one thing causes the general price level to rise – monetary inflation.

In other words, a rise in the general price level isn’t inflation. It is caused by inflation.

Henry Hazlitt is best known for his brilliant book Economics in One Lesson. In another essay titled “Inflation in One Page,” he explained why using a more precise definition of inflation is crucial.

“Inflation is an increase in the quantity of money and credit. Its chief consequence is soaring prices.

“Therefore inflation—if we misuse the term to mean the rising prices themselves—is caused solely by printing more money. For this, the government’s monetary policies are entirely responsible.” (Emphasis added)

These confused definitions allow Trump, Vance, and others to claim that there is virtually no inflation when inflation is on the rise, and to push for even more inflationary monetary policy from the Fed.

Again, it’s important to emphasize that rate cuts are inherently inflationary.

Lower rates encourage borrowing. In turn, this boosts the money supply. This is, by definition, inflation. One of the symptoms of this monetary inflation is price inflation. In other words, any victory over price inflation opens the door for the Fed to resume the very policy that gave us higher price inflation to begin with.

We’re already seeing this inflationary pressure manifest after the first round of rate cuts and the slowdown of balance sheet reduction.

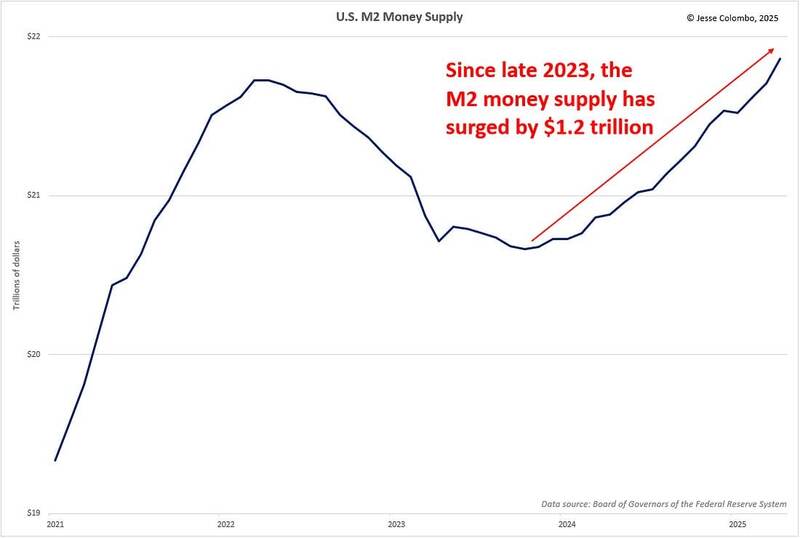

During the pandemic, the M2 money supply surged by roughly $6 trillion as the Federal Reserve unleashed massive monetary stimulus. That led to the bout of price inflation we suffered through in 2022.

During the Fed’s inflation fight, the M2 money supply contracted. This is exactly what needs to happen to wring out inflation from the economy. The money supply bottomed a little over a year ago at $20.60 trillion.

Since then, it has crept upward.

As of April, it was at $21.86 trillion. That’s the highest level since June 2022 and approaching the all-time high of $21.72 trillion hit in the spring of that year.

The Chicago Fed National Financial Conditions Index also reflects this increasingly inflationary environment. As of the week ending June 6, the NFCI stood at -0.51. A negative number reflects historically loose financial conditions.

And Trump et al want even more looseness!

The fact is, they’ve already gotten it.

Here’s the rub: they aren’t wrong. A higher interest rate environment will eventually crack the debt-riddled economy and pop the bubbles. The economy needs its easy money drug. However, a few good CPI reports notwithstanding, inflation is far from dead.

So, the central bank needs to simultaneously keep rates higher for longer and cut rates. That’s quite a Catch-22.

********

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.