May Is History!

The eagerly awaited end of the month of May has arrived and is becoming history. It is too early to say whether the Comex end of month developments measure up to expectations that have been repeatedly raised since the aborted attempt to effect a silver squeeze at the end of January. Nevertheless, neither of the February, March or April month ends triggered such a spike in the price of silver as the first attempt in January. That came as a surprise as the market reacted to the REDDIT Apes and their hype about a squeeze, riding on their GameSpot success. Then came May.

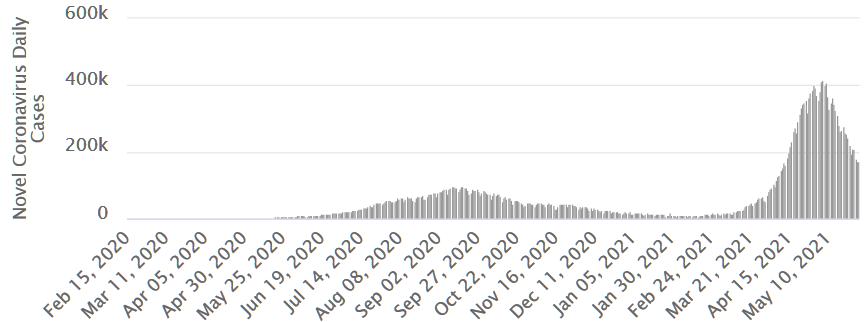

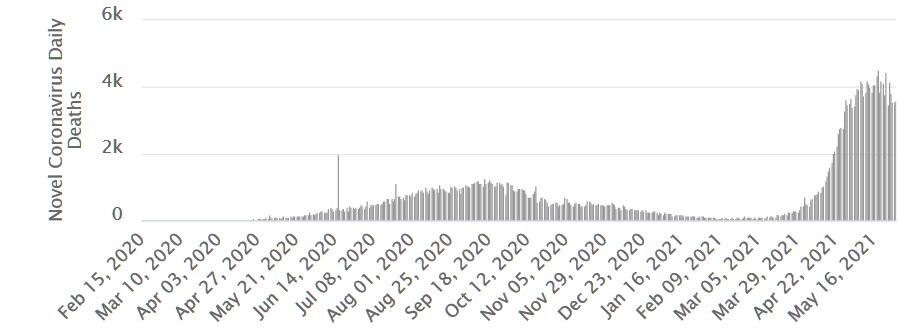

On the COVID front, India had been in the spotlight for some weeks, with the virus spreading widely during the time, hospitals swamped with sick people and cremation fires burning round the clock. The two charts below of the daily number of cases and deaths show the steep rise of the spread of apparently a new variant of the virus and the usual time lag of deaths compared to new infections.

Uttar Pradesh, the most populous state in India, experimented with the natural drug Ivermectin as prophylactic and treatment for COVID more than a year ago and had very good results, both to prevent infection and as a cure. It has recently been used more widely and must contribute to the decline in the number of infections and deaths that is being observed.

Ivermectin is an anti-parasitic and anti-viral drug discovered in Japan in the 1970s and is so safe and so successful that the two developers received the Nobel Prize for medicine in 2015. In Western countries the use of cheap and effective Ivermectin is not being promoted, but discouraged. Big Pharma’s influence stretches wide and far!

Early to midway through May it was clear that the gold and silver prices were still being suppressed and more so as the month progressed and the prices crept higher; $1900 and $28 would be defended. Later in the month it became evident that the suppression was only slowing down the upward trend in the prices and also that it would be touch and go whether the prices would challenge the obvious limits.

As the time for OPEX etc neared, with the prices still increasing gradually despite the daily attacks, the OI of gold in particular started declining quite rapidly. My guess as to the reason for this is that many of the more speculative longs decided to grab what profit they had in the bag before the month end progressed as had always happened in the past – with sustained attacks that took prices below key levels to ensure as many options and contracts as possible expired with no value as could be managed.

It turned out the month of May did not follow the usual pattern. Both prices were kept contained quite close to the $1900 and $28 limits, with only brief and limited breaks higher, which all failed. Available charts of the spot prices are not precise enough to know which options and contracts made it to expiry in the money, but it is clear that it was quite touch and go for derivatives that were borderline priced.

Later, gold sneaked above $1900, but silver was more sedate. With the month of May not being a big silver month, its price did not test the $28 level as keenly as the gold price challenged $1900. Silver held a little below the $28 level, rising some more to get within touching distance of that ceiling at the close on Friday. Monday is FND; as the Comex preliminary report shows, 334 silver contracts and 9479 gold contracts will be standing for delivery. No great shakes for the silver squeeze, but a good number for gold, representing about 30 tons.

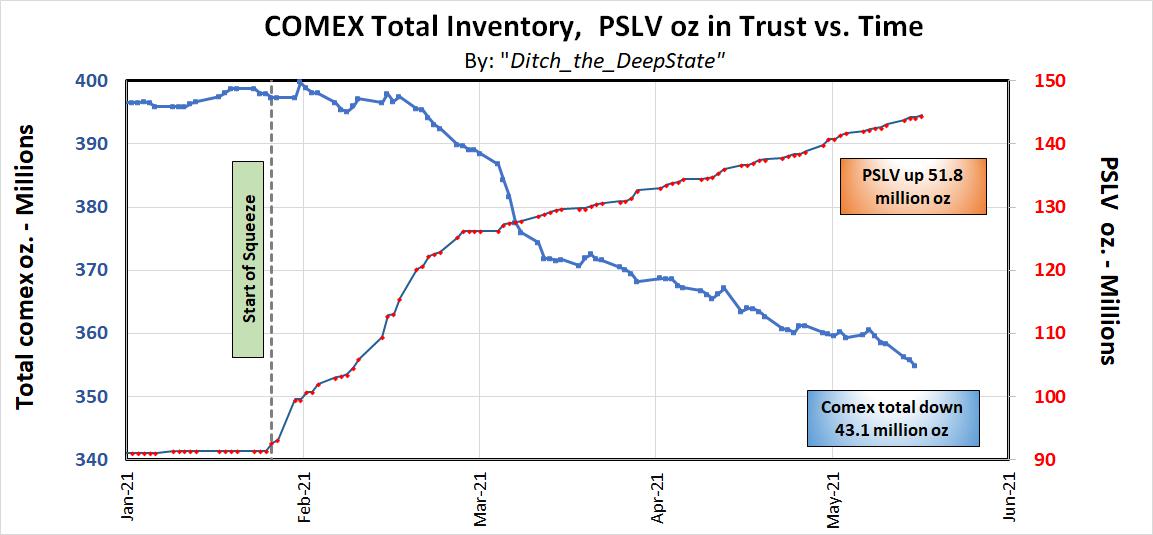

Correlations can be deceptive when they are happenstance and not due to a specific cause effect relationship. The chart below from a REDDIT report by an Ape activist, does show a good inverse correspondence between the Comex silver inventory and the number of ounces of silver in the PSLV vaults.

The timing of the divergence shows the PSLV holding of silver reacted immediately when the Apes launched their campaign and started to have effect on Comex a month later, presumably with an increased number of deliveries. The initial steep decline in the inventories became shallower as the increase in PSLV silver also increased at a more shallow rate. Perhaps the Apes have committed most of their budgets for silver, while recruitment of outsiders to join the squeeze proceeds at a slower pace? It can be assumed that the relatively smaller capitalised Apes have to employ PSLV for the squeeze, while the silver bulls on Comex have to do their bit by taking delivery.

Perhaps the most telling sign that silver supply is being depleted – with assistance from the Apes, as above – is the fact as reported in a recent Midas that the US Mint is suspending the minting of silver dollars because of lack of supply. The Mint is legally mandated to meet demand. One would therefore expect that rather than interrupt the minting, the Mint would have to pay whatever it takes to obtain silver, but apparently they baulk at the high premiums; or is it that higher authority prevents the Mint from paying up too far beyond the ‘official’ price and depleting limited reserves?

The above chart shows that the net short OI of the Commercials has widened, before holding steady near 72 250, close to the maximum net short position since mid 2018. Given the falling trend in the silver price this year until late March and then the rising trend that followed, the majority of their its positions must have been initially opened at much lower than the ruling price. That number represents an awful lot of silver, even when the average price is $26.50, or $1.50 below the current price.

The sum of the above is that we are closing in on a time when silver will be scarce and command higher premiums, with users of silver where it is critical for their operations being compelled to pay the higher prices or having to close down their operations – as the US Mint has done. Crunch time cannot be too far in the future, which is perhaps why there was no sustained attack on the metal prices at the end of May. The Banks do not want to risk selling more contracts at lower prices.

Meantime, warning calls about a Wall Street implosion and dollar collapse, possibly into a state of hyperinflation, are increasing and becoming more strident. Many such are simply marketing efforts, trying to scare people into paying for how to react when – not if - the crises erupt. Yet there are also well-considered professional analyses that point to severe problems for the markets and the currency. Few are as explicit with their timing as John Williams in his interview with Greg Hunter. Williams believes that dollar hyperinflation will begin to kick in during 2022, perhaps during its first half.

The dollar, much like Wall Street, manages to get resurrected whenever weakness begins to set in, while the yield on the 10 year Treasury note and the price of crude oil also have ceilings – like gold and silver – where any advance soon gets reversed. Wall Street, with the average PE of the Dow 30 a fraction below 30 and that of the S&P500 shares a little above that number, according to CNN, manages to hold close to its all time high. The limited reaction of these prices to news, good or bad, describes markets that are either distant from reality, or subject to external control.

As we are now expecting with justification for the suppression of the silver price soon to end, the same should apply to these other markets.

Euro–Dollar

Euro–dollar, last = $1.2189 (www.investing.com)

The euro is now in a two ticks upward and one tick back mode, largely because the dollar index dips below 90 and then gets levitated back to above that key number – the euro being on the other end of the whipsawing going on. If John Williams is to prove on target with his expectations for the dollar, the rising trend for the euro ought to become more consistent in the not too distant future – irrespective of the fact that the EU is also ‘enjoying’ a somewhat loose monetary policy.

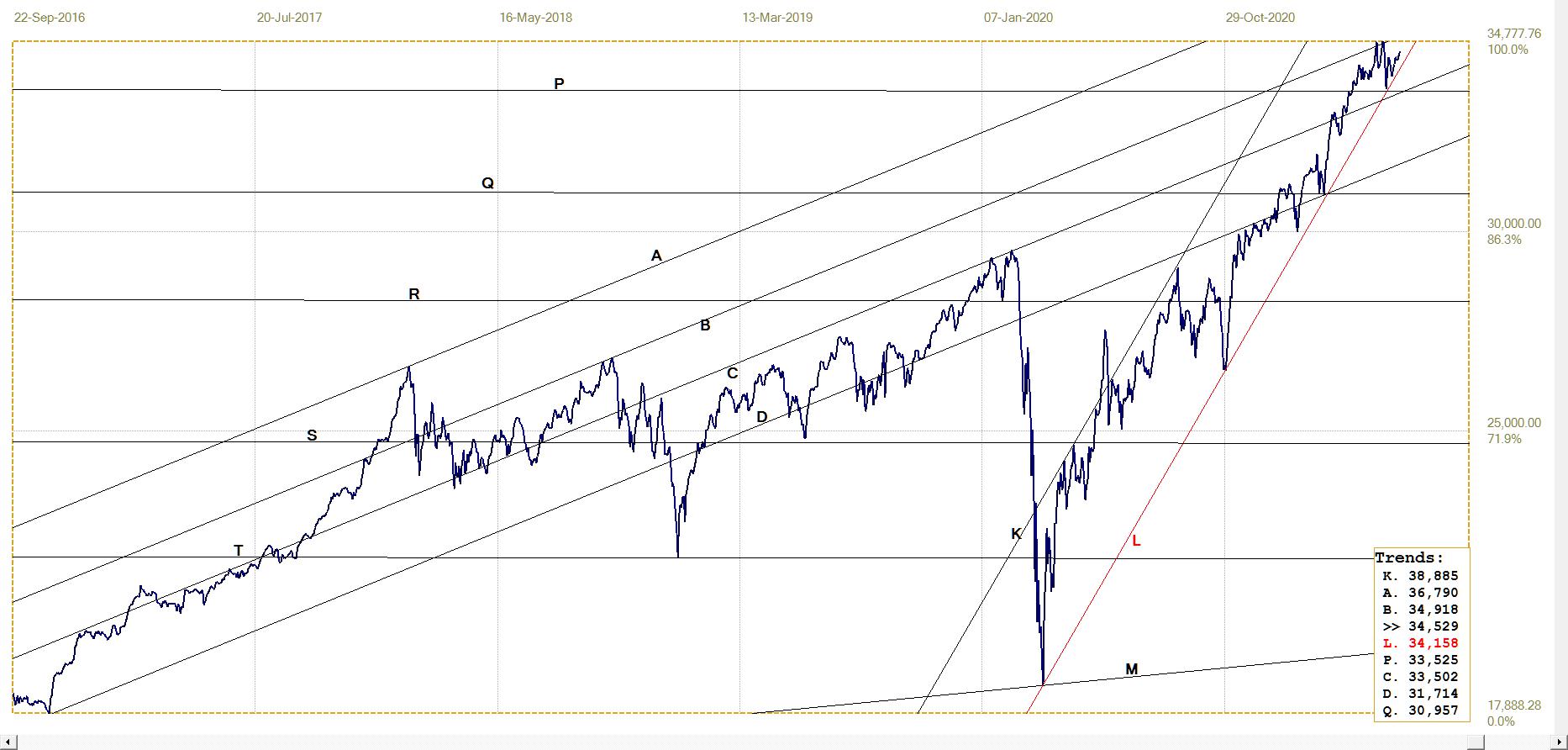

DJIA daily close

The DJIA continues to display admirable resilience by holding in steep bull channel KL while holding clear of support along line P. The rally has to keep going higher in order to buy time before a break from the bull channel is forced. A test of support at line L does seem likely before the end of June, so time could be running out.

DJIA. last = 34529.45 (money.cnn.com)

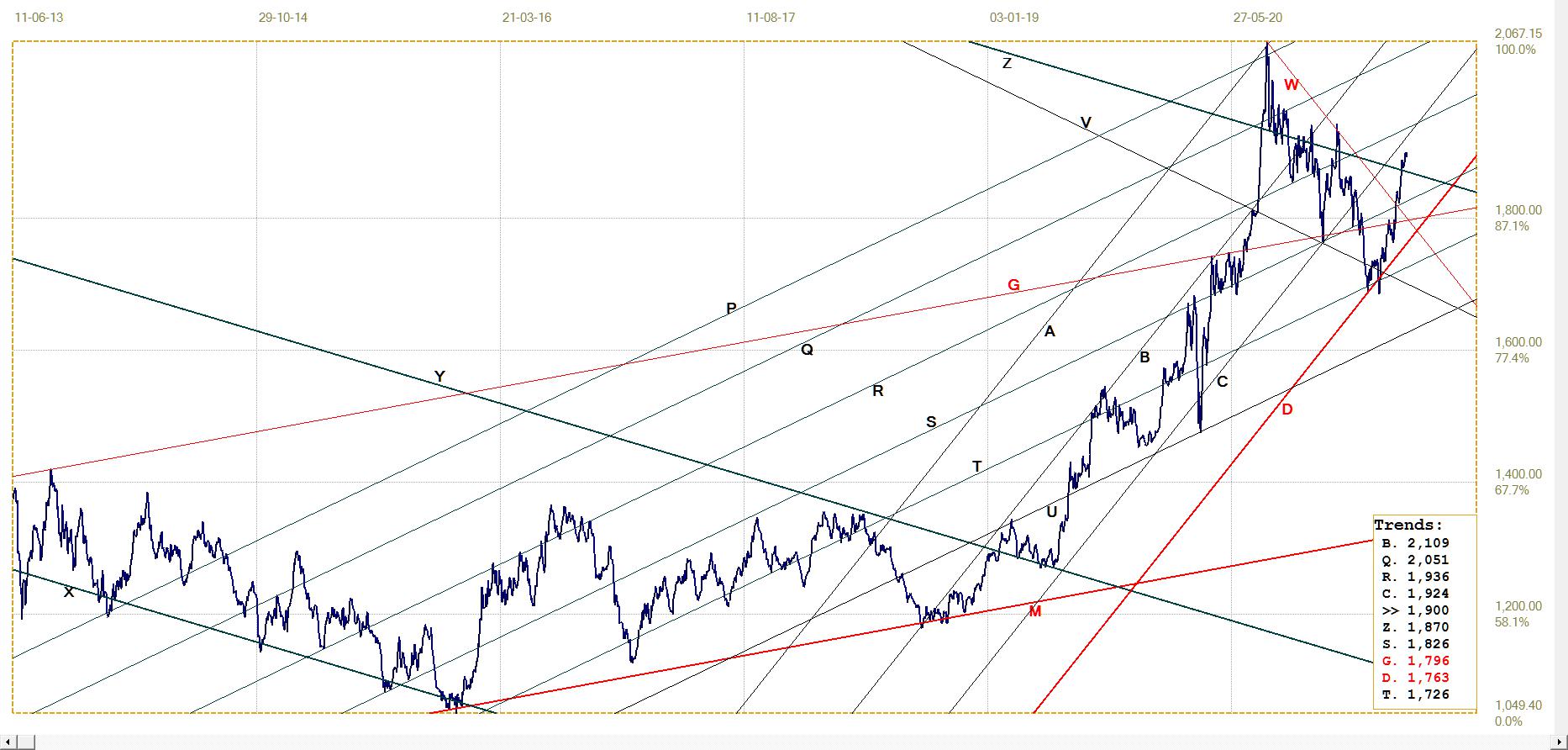

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1899.95 (www.kitco.com)

The rally in the price of gold after the sell-off in early April is also proceeding in fits and starts – under the influence of the vacillating dollar and the frequent if relatively mild attacks as the price suppression continues. The marginal break above channel YZ 10 days ago, followed by the pull back to line Z, managed last week to hold the break in the advance to test $1900.

Now that the end of May is past, with no major fireworks either way, we could expect the price to hold the break and continue higher – with perhaps only the routine early Monday morning attack in Asian trading time. In the past, these attacks have been quite vicious; it will be interesting to see if that repeats under current circumstances.

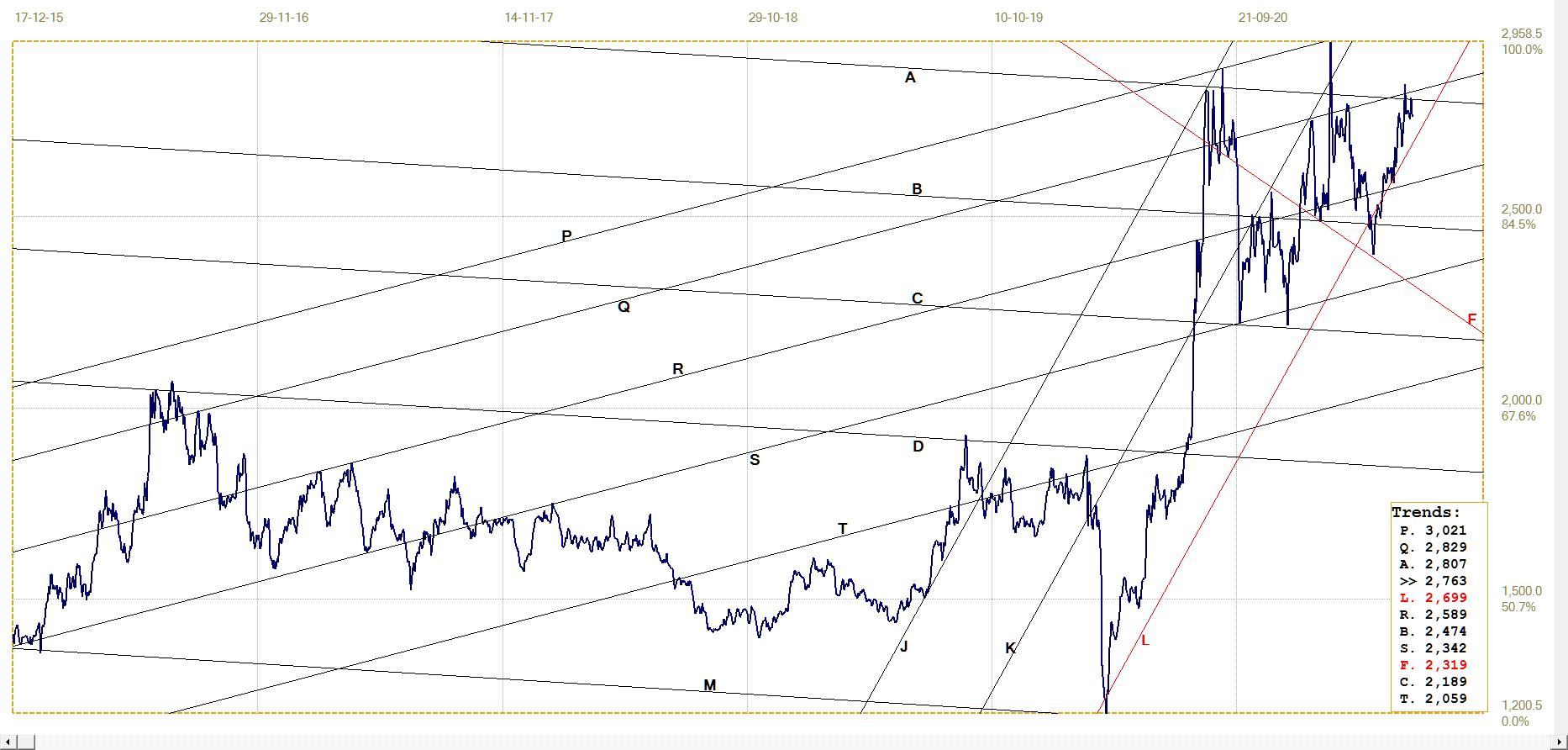

Euro–gold PM fix

The rally in the euro price of gold initially struggled to hold close to the support along the bottom boundary of bull channel KL. Since breaking above resistance at lines X and G, the price has moved away from the critical area close to line L; it is testing the resistance at line D with a marginal break higher on the London PM fix on Friday; just 5 cents below $1900.

This now steeper gradient for the euro is a sign this improvement in the euro price must be due to improving strength of gold itself, since the euro has been firm against the dollar. Doing so reduces the price of gold in euro – as can be seen by comparing the gradients of the recent rallies in the dollar and euro prices of gold. The difference in these two sustained rallies is due to the intrinsic strength of gold being greater than the strength of the euro against the dollar.

Euro gold price – PM fix in Euro. Last = €1561.76 (www.kitco.com)

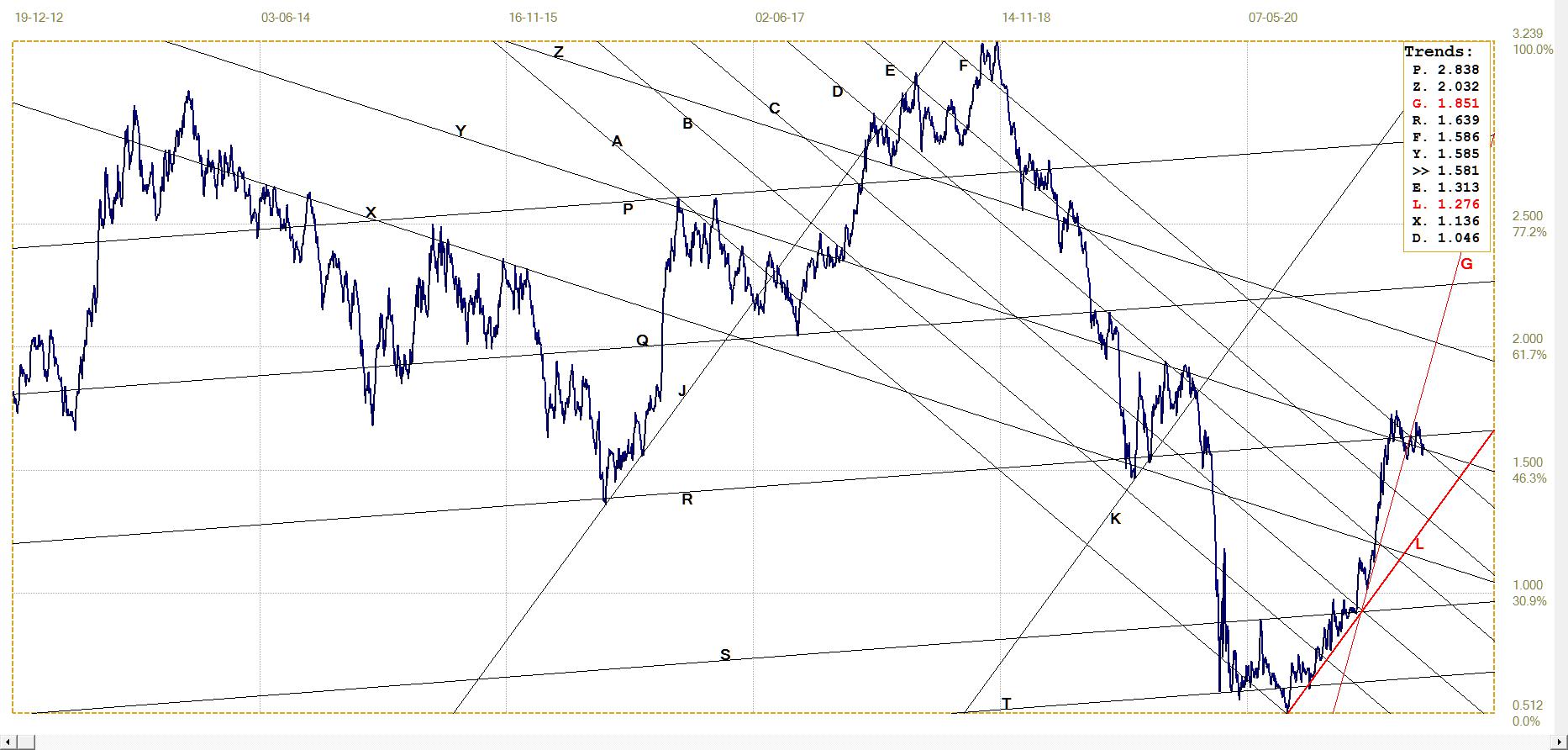

Silver Daily London Fix

Silver daily London fix, last = $27.63 (www.kitco.com)

Unlike what the gold price managed to do, the price of silver failed to hold the recent break above resistance along lines A and Q. The break happened on 18 May when the London silver fix was $28.475, a break above $28 that had called for immediate action to put silver back in its place. On Wednesday, when OPEX would happen later, the fix in London at $28.12 again broached the $28 level.

This would not do. Then many more options would end in the money. Again there was the required selling to make certain OPEX would be favourable for the option writers. No surprises and no mention of manipulation, as usual.

U.S. 10–year Treasury Note

This is getting monotonous. Signs from different markets that inflation is rife – as often happens, particularly so in food and energy, which two sectors have been excluded from the headline CPI since the 1970s.

Even the ‘adjusted’ CPI came in with a shock at 4.2%, but luckily the higher trend in other prices is ‘transitory’ – by the second half of 2021 the CPI will be back to the usual 2-3%, or even less. It is therefore quite safe to hold the yield on the 10-year Treasuries near the 1.5% mark to which investors have become used.

U.S. 10–year Treasury note, last = 1.581% (www.investing.com )

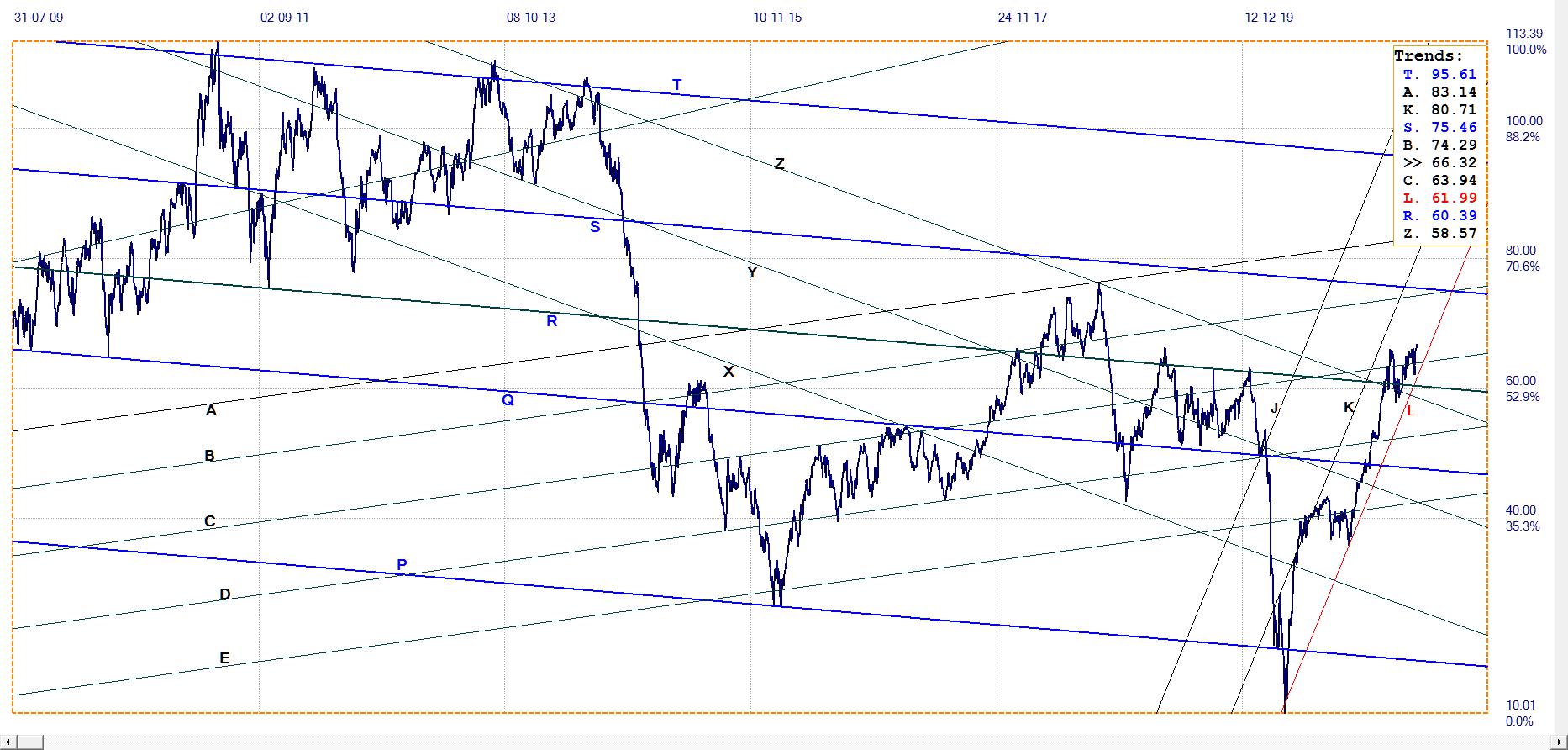

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $66.32 (www.investing.com )

There can be no crisis in the market for crude oil – or, by inference, for gasoline – since the oil price has been so stable these past few weeks. The queues that had developed at filling stations are proving to have been ‘transitory,’ similar to what is expected of inflation. While many people may have believed the problem is all due to those pesky Russians that hacked Colonial’s systems in control of their pipeline, or perhaps those sneaky Chinese, the BBC reported it was the DarkSide cyber-criminal gang that claimed responsibility

They apparently tried to apply ‘ransomware’ blackmail on Colonial. "Our goal is to make money and not creating problems for society,” DarkSide wrote on its website. As an aside, what an interesting fact about our technocratic society. Imagine the likes of Al Capone, or the Mafia, spreading the news about their activities.

A strange world we live in, indeed.

*******