Monetary Failure Is Becoming Inevitable

share

share

share

share

share

share

share

share

share

share

This article posits that there is an unpleasant conjunction of events beginning to undermine government finances in advanced nations. They combine the arrival of a long-term trend of rising welfare commitments with an increasing certainty of a global-scale credit crisis, in turn the outcome of a combination of the peak of the credit cycle and increasing trade protectionism. We see the latter already undermining the global economy, catching both governments and investors unexpectedly.

Few observers seem aware that an economic and systemic crisis will occur at a time when government finances are already precarious. However, the consequences are unthinkable for the authorities, and for this reason it is certain such a downturn will lead to a substantial increase in monetary inflation. The scale of the problem needs to be grasped in order to assess how destructive it will be for government finances and ultimately state-issued currencies.

Introduction

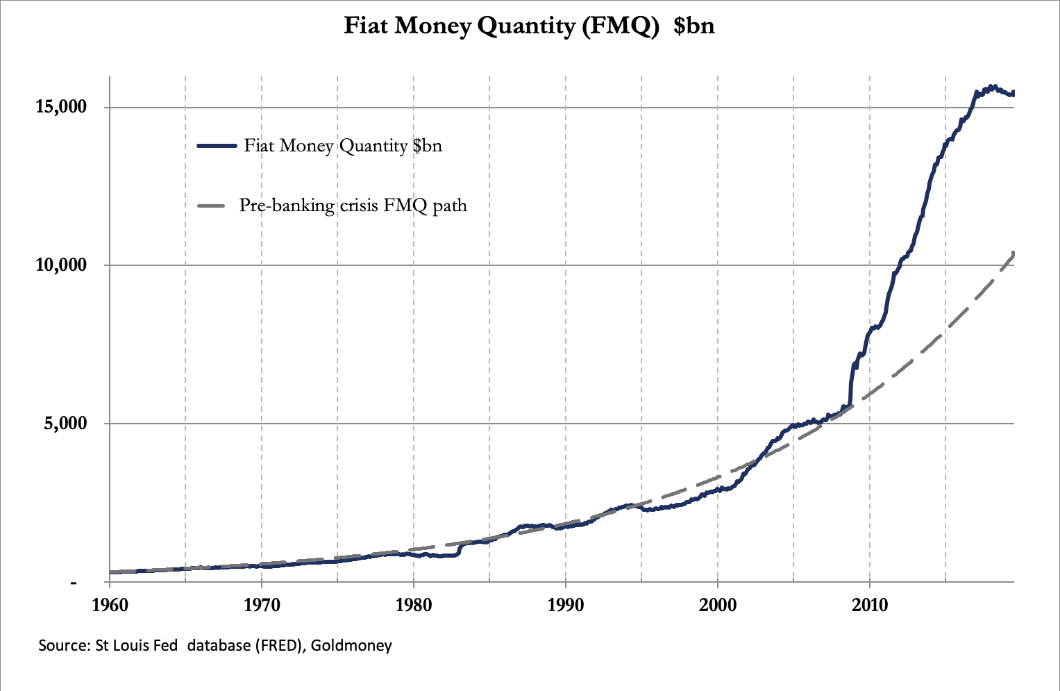

Listening to recent commentaries about the repo failures in New York leads one to suppose there is insufficient money in the system. This is not the real issue, as the chart below of the fiat money quantity for the dollar clearly shows.

The fiat money quantity is the amount of fiat money (in this case US dollars) both in circulation and held in reserve on the central bank’s balance sheet. Before the Lehman crisis, it grew at a fairly constant compound growth rate of 5.86%. Since the Lehman crisis, it has grown at an average of 9.45%, even after the slowdown in its rate of growth that started in January 2017. FMQ is still $5 trillion above where it would have been today if the massive monetary expansion in the wake of the Lehman crisis had not happened. If there is a shortage of money, it is because the process of debt creation to fund current expenditure is spiralling out of control.

It is not just the US. If we take similar (but less detailed) figures for FMQ in other major nations by adding together broad money M3 and central bank balance sheets, we find that it has increased at varying rates for the most important economies. In China, the compound annual growth rate has been 12%, though the growth in Japan at 5.2% and in the Eurozone at 4.9%. has been more subdued, reflecting stagnant levels of bank credit. When for the lack of any other measure statisticians use a GDP money total as a substitute for defining economic progress, we should not be surprised to see that the economies with the greatest rate of monetary growth are reckoned to be the best performing.

Just as GDP tells us nothing about human progress and its benefits to society, other uses of money as a control mechanism for economic management are equally misleading. Much of the monetary expansion has been to fund unproductive government spending. Most of the balance after the government’s cut has fuelled speculation in the financial sector and has funded consumer credit for those whose savings have been tapped out. Not revealed by the acceleration of money supply growth is the wealth transfer effect which impoverishes every productive individual for the benefit of governments, the banking system and the bank’s favoured customers, who are in the main large corporates and directly or indirectly the hedge funds.

Decades of impoverishment by monetary inflation, which has quickened since Lehman, is a very serious matter and is behind the fragility of economic systems dominated by government spending deficits. The reason there appears to be not enough money is because the acceleration of government liabilities in nominal currency terms is catching up with them. Laurence Kotlikoff’s famous 2012 estimate of the US Government’s future commitments of a net present value of over $222bn is very much alive on arrival.

It would be more accurate to say the figure for the US is trending towards infinity. It is already infinity in Japan and the Eurozone, where negative interest rates and bond yields offer the basis for the net present value calculation. As in most things financial, the public is blissfully unaware of the true implications of low and negative interest rates and ultra-low bond yields. They take the view that very low interest rates permit their government to borrow as much as it likes to provide the public with new hospitals, schools and the like. It is a case of fools of politicians and central bankers having turned everyone else into fools, and the few who realise it have no idea how to reverse the process. What they do not see is the government cannot now fund public healthcare and pensions, which make up the bulk of future obligations in a welfare state, without accelerating monetary debasement even more.

No one can know what the true figure is for future government liabilities, of which welfare is an increasing component. Politicians, who claim that a week in politics is the long term, fail to see any problem. The few governments which have raised retirement ages have done so to deal with escalating current welfare liabilities, not addressing those of the future that will lead ultimately to the destruction of what as Westerners we generally agree is civilised democratic society. That is their successors’ problem.

If history and reasoned economic theory is any guide, the demands for credit by the state will terminate in the destruction of government currencies. For the truth of the matter is inflation of money and credit has created the illusion we can all live beyond our income, our income being what we produce.

Nothing, with the sole exceptions of a central bank and its commercial charges can make money without having to advertise for it: the seigniorage is simply taken without public consent. Without questioning how it arises, the extra money allows us to indulge in all our flights of fancy until at some time reality strikes. Rather like Monty Python’s glutton, Mr Creosote, can we force in a little more inflation before we all explode?

The credit cycle is now on the turn

The complaint that the current precarious position faced by major economies is due to a shortage of money is untrue. The problem is one of escalating expenditures, and anyway, the response to any shortage, as we saw recently with problems in the US repo market, is simply to issue more money. But it is no solution, only making the eventual crisis worse.

It is easy to increase the quantity of money, but virtually impossible to increase the quantity of goods to accompany it. For this reason, increases in the quantity of money disadvantage ordinary people, the everyday producers of goods and services in small and medium sized enterprises. And with more money in circulation but the same quantity of goods, the pressure mounts for prices to rise. For a time, consumers can escape price rises by substituting cheaper goods from abroad. This reduces the impact of price rises in the domestic market. Savers are also beneficial for price stability, because they defer their purchases to a future date. But in the absence of savers taking the steam out of inflation-fuelled demand, and contemporary American tariffs on Chinese imports designed to limit them by erasing the price advantage handed to China by America’s monetary inflation, the effect is bound to raise the general level of prices.

Consequently, legacy businesses in America have hoped for a bonanza through not being forced to compete with China. For too long, they have seen the costs of production rise, driven by rising input costs, government regulations, their own expanding bureaucracies, and the natural tendency for expenditure to rise towards the income available. Having been bound hand and foot by red tape they hope that tariffs will protect them from foreign competitors who are not. They maintain their higher uncompetitive prices only to find that consumers, who have not had the benefit of the new free money, are not prepared to pay them or are unable to afford them. Sales volumes suffer and losses begin to accumulate. An international problem provoked by trade protectionism becomes a domestic setback, which is the transition currently hitting the US economy.

We already see the evidence of a developing slump as well in other countries, not directly involved in the trade spat between China and America, but also dependent on the world’s two largest nations measured by trade engaged in their trade war. The member states of the Eurozone are all reporting disappointing internal trade conditions, as are virtually all other nations which report them. The solution, the inflationists say, is more money.

It is a call that has even evolved into a demand that borrowers should be paid to borrow through negative interest rates, killing off the few savers left in the advanced economies. The source for the investment in production deemed necessary to keep the world’s economy from crashing is no longer backed by genuine savings, but by increasing quantities of money conjured out of thin air directly or indirectly by the banking system.

Those that benefit from inflation by expansion of bank credit are those who do not need it, because they are creditworthy and can always raise funds in the market. The problem lies with those who are not creditworthy. No amount of monetary inflation will rescue them, because the banks, in America for instance, have already loaned almost all of the equivalent of their own capital to non-financial borrowers who are deemed to be less than investment grade, in other words junk, both directly and through collateralised loan obligations. In the coming months, or it might even be just a matter of weeks, the banks will protect themselves by turning from providers of liquidity to withdrawing it. Inevitably, a volte-face on credit by the banks will bring on the slump. A systemic crisis will then ensue, and central banks will be forced to ride to the rescue by printing yet more money.

As we saw following the Lehman crisis, the money will be printed to bolster banks’ reserves in return for government debt accumulating at the central bank, so most of that newly printed money ends up covering the government’s deficit through the purchase of government bonds by the central bank.

A credit cycle will have completed: the post-Lehman stabilisation, followed by an uncertain recovery, then a return to normality. Normality matures into complacency, with bank credit being expanded in favour of increasingly risky borrowers. The post-credit expansion crash, mirroring Lehman, is now in the making.

It is a repetitive cycle, the consequence of earlier monetary interventions by the central banks. They have been unable to stop themselves. The decision to pull the plug on Lehman, only a second-rank investment bank, nearly brought down the entire global financial system. No central bank can take that risk again. We can be certain the solution to the next credit crisis will be a further acceleration of the production of money and credit with no one in the financial system being allowed to fail. And the expansion of base money directed at bolstering the banks’ balances will predominantly favour the one borrower class left with any financial standing, the governments.

But what we see is two forces joining together to accelerate the demise of state-issued currencies, which at the end of the day are only backed by the faith and credit the public holds in their governments’ finances. The upcoming credit crunch will occur against a background of a rapidly increasing burden of welfare liabilities, so dramatically identified by Laurence Kotlikoff seven years ago, and likely to have increased markedly from his alarming estimate.

Inevitably, the prolonged suppression of government bond yields will begin to end, and irrespective of central bank interest rate policies, they will rise as investors realise that adjusted for a more realistic estimate of price inflation than that provided by government statisticians, they are a costly safe haven. Then, government finances will become so visibly out of control that even modern monetary theorists will return to their textbooks to see which bit they failed to understand.

The dawning of monetary inflation on the general public

Today, the public is blissfully unaware of the inexorable trend of monetary debasement while enjoying the continuing benefits of government welfare. Government economists tell them that moderately rising prices, the consequence and justification for expanding the quantity of money and credit, are good for them. And who are they to question the experts?

Fortunately, people pursuing their daily lives usually adapt to the circumstances forced upon them by governments. A targeted two per cent inflation rate of prices is not overtly disruptive, and government statisticians have become skilled at goal-seeking price inflation figures. Everyone’s experience of price inflation is different, so government figures become believable by default. But for some considerable time, increases in peoples’ wages have badly lagged the price rises of their normal purchases, which bear little relation to the composition of governments’ consumer price statistics. Coupled with the financial freedom afforded to them to borrow, they have made up the difference between income and expenditure just like any modern government: by borrowing with little or no intention of repaying.

The cause of the problem people face is the continual destruction of their personal wealth by monetary inflation. It has led to a fundamental difference between the credit cycle today and those earlier described in the textbooks of the Austrian School of economists. Before Keynesianism took hold, investment in production was funded by savings. Those savings have been substantially destroyed. Instead of savings being a cushion against uncertainty, for practical purposes they no longer exist.

There are two consequences that concern us here. The first is that the burden of investment and its continuity now falls entirely on the state and its licenced banks, whose only recourse is yet more monetary expansion. The second is the almost total reliance today’s wage earners place on receiving their monthly salary to survive, with a reported 78% of US workers living pay-check to pay-check. British workers are similarly strapped. They have no means of surviving a credit crisis and the economic consequences that follow. That will be another cost that falls to the government and its central bank to add to already escalating welfare commitments.

It is becoming easy to envision the day that the majority of government spending is financed by inflation and inflationary borrowing, through a combination of falling tax revenues and escalating spending commitments. There is also an imbalance between taxpayers, with a mobile wealthy class bearing the bulk of national tax burdens who can up sticks at any time. The question then arises as to how financial markets will react when the triple conjunction of a credit crisis, sharply increased government deficits, and the long-term escalation of welfare costs, materialise in the public consciousness all at the same time.

Ahead of the next credit crisis, the knowledge that things are not quite right has so far led to a flight to perceived safety: in some countries, investors are even paying to own their government’s debt. In the US, the yield on the 10-year US Treasury bond has declined from 3.2% a year ago to 1.4% today.

As the next credit crisis materialises, perceptions of investment risk are bound to change radically. The imperative to print money at an even faster rate will accompany the trend towards deeper negative interest rates, penalising bank deposits, eliminating residual savers from the system. Consequently, if the Fed makes the mistake of even considering negative interest rates, it will put the whole commodity complex firmly into backwardation from the money side because all commodities are priced in dollars.

We can take anticipation of lower and more widespread negative rates as guaranteed when the credit cycle enters its crisis stage. Last time, everyone was so relieved that life after Lehman’s death continued that they still regarded government debt as the risk-free yardstick for financial investment. It would be foolish for a central bank to think this trick could be pulled a second time. Just imagine how high the fiat money quantity in our introductory chart would be above that long-term pre-Lehman trend line. And just think of the damage to the purchasing power of the dollar and the other major fiat currencies from interest rate policies that are bound to drive deposits towards widespread encashment.

This time, the coincidence of a credit crisis and rapidly escalating short- and long-term welfare commitments adds a new dimension to the inflation story. Far from rescuing the global economy, the spreading of zero and negative interest rates can be expected to expose the true worth of fiat currencies. Next time is different in another respect: there is a new generation of educated men and women who through cryptocurrencies have learned of the fiat currency fallacy ahead of the event. In the past, nearly everyone learned of it too late. Now, around the world, particularly in America and China millennials could accelerate the ending of fiat money by triggering an early shift out of fiat into cryptos. Bitcoin at a million dollars becomes no longer pure fancy, only don’t forget that a million dollars might not buy you much.

It is not an expected outcome, except by the very few who understand what is happening to money and the built-in escalation of its quantity. These will include growing numbers in the cryptocurrency community and the few who have studied the subject away from the influence of macroeconomists. Hopefully, they will now include readers of this article.

Anticipating a crack-up boom

As the credit crisis drives monetary expansion into overdrive or leads into a hyperinflationary slump, people are bound to begin to discard their national currencies in favour of any goods they think they might need in future. Minimal cash liquidity becomes the desired position. It can rapidly lead into the final short-lived boom that marks the death of an unbacked fiat currency, when it dawns on the general public that their government’s currency might be worthless. As the conviction of it grows, the pace at which it is dumped for anything of use that they can get their hands on increases exponentially. In Germany, it lasted from about May 1923 until the following November when the mark finally expired.

It has long been a theme of survivalist libertarians that this will occur.

So long as the alternative of owning physical gold and silver exists, it is not necessary to stockpile necessities, unless, that is, disruptions to supplies are anticipated. In a slump, the prices of goods will decline measured in sound money. This, after all, was firmly impressed upon Keynesian inflationists by the experience of the early 1930s, when measured in gold substitutes prices of nearly everything fell heavily. When gold and silver became more desirable relative to owning goods, their purchasing power increases while that of fiat currencies declines.

Putting supply considerations to one side, if in the wake of the next credit crisis the economic conditions of the 1930s return, those that use gold and silver as money will see the prices of their consumer staples fall, so there should be no hurry to hoard them.

Alasdair Macleod

HEAD OF RESEARCH• GOLDMONEY

Twitter: @MacleodFinance

MOBILE: +44 7790 419403

Goldmoney

The Most Trusted Name in Precious Metals tm

NEW YORK | ST. HELIER | TORONTO

Publicly Traded Symbols: CA: XAU | US: XAUMF

© 2017 GOLDMONEY INC. ALL RIGHTS RESERVED. THIS MESSAGE MAY CONTAIN CONFIDENTIAL OR PRIVILEGED INFORMATION. IF YOU ARE NOT THE INTENDED RECIPIENT, PLEASE ADVISE US IMMEDIATELY. THIS MESSAGE IS FOR GENERAL INFORMATION ONLY AND SHOULD NOT BE CONSTRUED AS AN OFFER OR SOLICITATION OF AN OFFER TO BUY SECURITIES OR ANY OTHER FINANCIAL INSTRUMENTS. WE DO NOT PROVIDE TAX, ACCOUNTING, OR LEGAL ADVICE, AND RECOMMEND THAT YOU SEEK INDEPENDENT PROFESSIONAL ADVICE IF NECESSARY. WE CONSIDER INFORMATION IN THIS MESSAGE RELIABLE BUT WE DO NOT REPRESENT THAT IT IS ACCURATE, COMPLETE, AND/OR UP TO DATE AND IT SHOULD NOT BE RELIED ON AS SUCH. OPINIONS EXPRESSED ARE OUR CURRENT OPINIONS AS OF THE DATE APPEARING ON THIS MESSAGE ONLY AND ONLY REPRESENT THE VIEWS OF THE AUTHOR AND NOT THOSE OF GOLDMONEY INC OR ITS SUBSIDIARIES UNLESS OTHERWISE EXPRESSLY NOTED.

Notice: This email may contain confidential or privileged information. If you received this email in error or believe you are not the intended recipient, please notify the sender immediately and delete this email without forwarding or opening any attachments. Thank you for your cooperation and attention

*********

share

share

share

share

share