Negative Real Rates Puts Shine On Getchell's Gold

A number of factors influence gold prices (mainly the US dollar, gold ETF inflows/ outflows, inflation rate, bond yields, safe haven demand, physical gold demand, gold supply) but none is more reliable than real interest rates.

The demand for gold moves inversely to interest rates - the higher the rate of interest, the lower the demand for gold, the lower the rate of interest the higher the demand for gold.

The reason for this is simple, when real interest rates (interest rate minus inflation) are low, at, or below zero, cash and bonds fall out of favor because the real return is lower than inflation - if you’re earning 1.6% on your money from a government bond, but inflation is running 2.7%, the real rate you are earning is negative 1.1% - an investor is actually losing purchasing power. Gold is the most proven investment to offer a return greater than inflation, by its rising price, or at least not a loss of purchasing power.

The gold price is tied to low or negative real interest rates which are essentially the by-product of inflation - central banks drop interest rates when the economy is running too hot, demonstrated by an increase in the consumer price index. In the US, this means inflation greater than 2%.

Bond market and gold market observers keep a close eye on US Treasury yields, particular the yield on the benchmark 10-year note.

When real bond yields are low, the price of gold can and will rise; on the flip side, when real rates are rising, gold can fall very quickly.

There’s a saying that “6% interest can draw gold from the moon,” undoubtedly true, but rates below 2% also draw investors to gold, because that means the real interest rate, if inflation is trending about 2%, is approaching 0%, the point where bond investors lose their purchasing power and start looking around for an investment that will protect it, ie., gold.

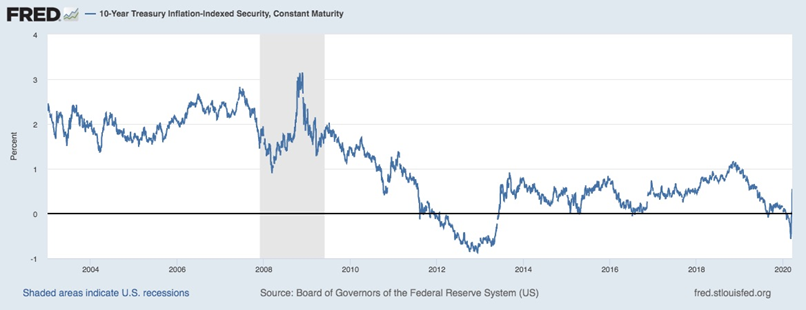

Historically we can see the inverse relationship between real interest rates and gold, by comparing two charts, the gold price over the last 20 years, and the yields on 10-year Treasury Inflation-Indexed Securities (TIPS), which analysts use as a proxy for real interest rates, charted over the same period.

Notice that the TIPS blue line dips under the 0% baseline between 2012 and 2014, nearing -1%. Gold represented by the yellow line rises gradually from 2002 then climbs sharply after 2010, reaching its all-time high of $1,917/oz in 2011. In 2015, we see gold falling in anticipation of the US Federal Reserve hiking interest rates, and the resultant rise in the US dollar at the same time as real interest rates, ie. the TIPS blue line, are rising.

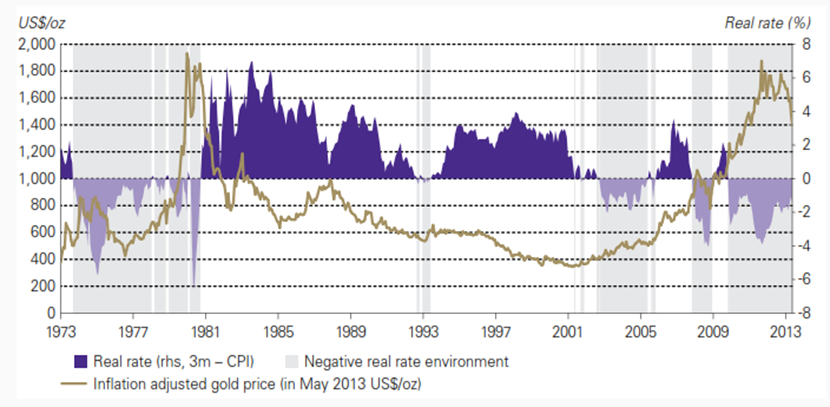

In an article titled ‘The Golden Dilemma’, authors Claude Erb and Campbell found a near-perfect negative correlation of -0.82 (-1 being a perfect negative correlation) between real interest rates and gold prices between 1997 and 2012. Going back further in history, when real interest rates turned negative during the second half of the 1970s, gold moved as high as $1,900 an ounce, as real rates plummeted as low as -6%. When Paul Volcker, Fed Chair under President Carter and Reagan, hiked short-term nominal interest rates, real rates returned to positive, ending gold’s run. In fact the gold price continued to drift downward, reaching a 30-year low under $400 an ounce in 2001. The gold bull market of 2010 to 2013 is easily seen in juxtaposition with negative real interest rates which bottomed out at around -4% during that same period.

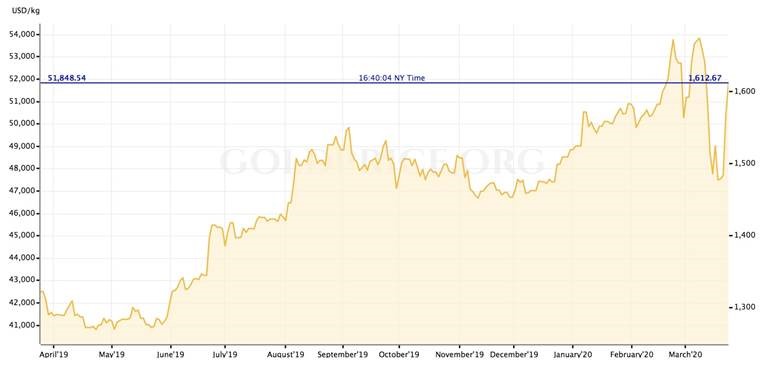

Fasting forward to 2019-20, it’s clear that negative real rates played a big part in gold’s run during the second half of 2019. Inflation, reflected by core CPI, increased 2.4% in August, the high for the year. Meanwhile the 10-year Treasury note halved from 3% to 1.6%, setting up a period of negative real yields for the benchmark 10-year.

As a contributor to Kitco’s gold commentary wrote, These falling real yields were rocket fuel for gold, and this was in spite of the USD’s bull market against the euro and yen. The price of gold increased by double digits [its 2019 gain was 18%] even though the Dollar Index has also increased by nearly 5% in the last 12 months.

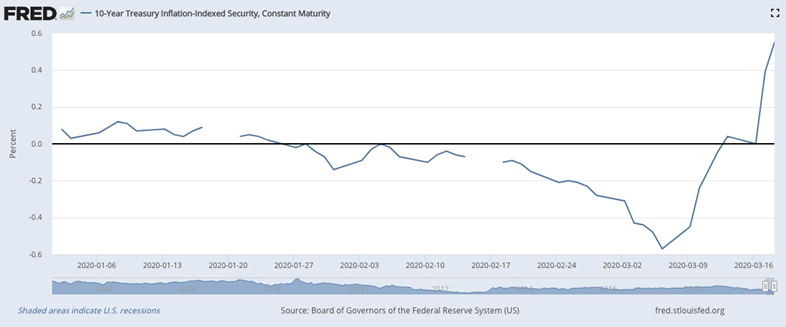

As for 2020, looking at a year-to-date 10-year Treasury Inflation-Indexed Securities (TIPS) chart, we see interest rates start to go negative again at the end of January, then they really drop sharply in February when the coronavirus outbreak begins - falling to a record low of -0.57 on March 6, the same day the 10-year hit a record low yield of -0.7%.

During this time the relationship between gold and negative real yields is fairly tight. The correlation however gets compromised by some major gold volatility, with the spot price climbing to a high of $1,674 on March 9, then losing almost $200 within a week. We see the yield on the 10-year TIPS head upward between March 6 and March 13, when it breaks above zero, lapses for a day, then shoots all the way to 0.55% on March 18. This was due to bond traders selling long-term bonds, in anticipation of a deluge of future debt supply - resulting from a fresh round of Treasury note auctions presumed necessary to pay for a potential $1 trillion stimulus package being discussed to combat the coronavirus.

Currently real yields are negative, which should be good for gold prices going forward. (the current 10-year yield of 0.85% minus the inflation rate of 2.3% = a -1.45% real rate).

Flight to bonds

Indeed the tremendous fear and uncertainty surrounding the coronavirus is forcing investors into safe havens like the US$, US government bonds and gold/ silver, even though Treasury yields are abysmal.

The dramatic bond rally we are currently seeing, is driving down yields across the world (bond prices and yields move in opposite directions). On March 8 the US 10-year Treasury note reached an all-time low of -0.38%; two days earlier the German “bund”, whose yields have been negative for awhile, fell to a record -0.74%.

Investors are piling into sovereign debt based on expectations of monetary stimulus (see below) similar to financial crisis-era easing programs that pushed down interest rates to zero and sparked a multi-year rally in stocks.

The longest economic expansion in US history lasted 11 years- 126 straight months of economic growth. The stock market bull everyone hoped would keep going has finally died, the coup de grace delivered with stunning efficiency by the coronavirus. Despite a huge rally on Wednesday – it was the best day for the Dow in almost 90 years – global stocks this month have seen a drop of at least 25%.

Extraordinary stimulus measures

Early Wednesday morning, White House and Senate leaders struck a deal on a colossal $2 trillion emergency aid package – the largest in US history - to help absorb the economic hit from covid-19.

Among the measures are a $1,200 direct payment to every American, $500 billion in loans for distressed businesses including $50 billion for airlines, and $350 billion in loans for small businesses.

The Canadian government also passed a coronavirus aid package Wednesday. It includes CAD$52 billion in direct financial support for individuals and businesses, polus $55 billion in tax deferrals.

As the crisis deepens, with the number of cases around the world topping 463,000 and nearing 21,000 deaths, as of this writing, leaders and health officials are discouraging travel, telling people to restrict gatherings, stay at home and practice social distancing.

A third of the world right now is under some form of lockdown, including Italy, Britain and India.

In North America, many businesses have been forced to close by ordinance, or due to a severe drop in clientele. Most can no longer count on routine business to keep cash flows intact.

Among the industries hardest hit by covid-19 restrictions are hospitality - including hotels, restaurants, cafes and bars - travel (airlines and cruises), the auto sector and the oil patch.

Last week, among efforts to contain the pandemic, Canada shut its borders to foreigners including its southern border with the United States - an unprecedented move that restricts all non-essential crossings. Trade flows and seasonal workers are exempted.

Most Canadian provinces and major cities, including Toronto, Vancouver and Montreal, have declared states of emergency, including a health order that bans large public gatherings, closes gyms and casinos, and allows the prosecution of people who fail to comply.

This week Ontario and Quebec, which have the most cases, asked all non-essential businesses to close. The Canadian government hasn't yet declared a state of emergency but Prime Minister Justin Trudeau is pleading for people to stay home, to avoid spreading the virus further.

In the United States which has over 20 times as many coronavirus cases, there are even tighter restrictions around movement.

As more states lock down, including California, Maryland, Ilinois and Washington, one in three Americans are under orders to stay home.

Most business venues such as indoor malls are closed, as are dine-in restaurants, bars, nightclubs, gyms and fitness studios. Convention centers and public events are also out of bounds. Only businesses providing essential services have remained open. These include grocery stores, food banks, convenience stores, banks, doctor’s offices and pharmacies.

Last week, Goldman Sachs came out with a shocking unemployment prediction, that a record 2.25 million Americans could enter claims for unemployment benefits; half a million Canadians have already signed up for EI.

Goldman warns that US GDP will shrink 29% by the end of the second quarter, and unemployment could hit at least 9%.

James Bullard, the President of the St. Louis Federal Reserve Bank, said he sees unemployment reaching 30% in coming months - worse than the Depression and three times as bad as the 2007-09 recession.

A recession is defined as two consecutive quarters of GDP contraction.

As the coronavirus continues to spread across the United States, confidence among consumers is dropping like a stone. The consumer sentiment index fell from 100 to 95.9 during the first 11 days of March.

The next Arab Spring?

One of the most alarming effects of the pandemic, likely visible to every single shopper who has been to the grocery store in recent days, is the prospect of a complete break in the grocery supply chain, resulting in a food shortage.

Assurances from grocery giants like Loblaws, that supplies will flow unimpeded (we already know that isn’t true, otherwise why so many empty shelves?) haven’t stopped widespread hoarding, as residents confront the reality of being confined to their homes for weeks, through government-imposed “shelter in place” orders.

As more businesses close down daily, it's not outside the realm of possibility to imagine grocery stores operating at reduced hours, with limited shipments coming in, especially as more workers, including truck drivers and warehouse personnel, fall victim to covid-19. In the worst-case-scenario, there could even by wartime-type rationing.

It’s not just grocery shoppers who are hoarding pantry staples. Some governments are moving to secure domestic food supplies during the conoravirus pandemic.

Kazakhstan, one of the world’s biggest shippers of wheat flour, banned exports of that product along with others, including carrots, sugar and potatoes. Vietnam temporarily suspended new rice export contracts. Serbia has stopped the flow of its sunflower oil and other goods, while Russia is leaving the door open to shipment bans and said it’s assessing the situation weekly.

Could a supply pipeline that has run uninterrupted for, well forever, something we North Americans absolutely take for granted, be broken by covid-19?

It doesn’t take a leap of logic to see what could happen next. With fruit, vegetables and meat either too expensive or simply unavailable, due to shipments being canceled or delayed, there could be long line-ups to get into grocery stores when they open.

Those lucky enough to get their meat, veggies, pasta and toilet paper will be okay until the next shipment. What happens to the unlucky ones? The prospect of food riots is not hard to imagine.

Remember, the Arab Spring started over a shortage of bread.

Just as bad is the prospect of pharmacies running out of medicine, and medical supply stores getting shorted on shipments of critical medical equipment like surgical masks.

An article by F. William Engdahl states that 80% of medicines consumed in the United States are made in China. Among them are most antibiotics, birth control pills, blood pressure medicines such as valsartan, blood thinners such as heparin, and various cancer drugs. The list also includes medications to treat HIV, Alzheimer’s disease, bipolar disorder, schizophrenia, depression and epilepsy,

Even over-the-counter remedies like Vitamin C have been outsourced to China, able to produce them much cheaper than in the West.

Imagine what could happen if factory closures or limited operations start restricting drug shipments, leading to shortages in the pharmacies of Europe and North America?

The breakdown in supply lines, supposedly made more efficient by globalization, is becoming in some places a matter of life and death.

In Seattle, hospital workers ran out of surgical masks and have been fashioning protective gear from office supplies.

Star athletes, Hollywood elites, politicians, the rich, all can get tested for coronavirus before the rest of us (and get back tests in a very timely manner). We working-class peasants get sent home, no test done, told to ‘self isolate.’ President Trump, when asked about this said: ‘That’s life.’ Well he’s right, it is.

“On March 11, the state of Oklahoma used 60% of its testing capacity on NBA players and team staff after a member of the Utah Jazz tested positive, allowing them to bypass the long waits endured by ordinary citizens waiting for tests.”

China makes most of the world’s pharmaceuticals, along with the majority of its medical equipment. Front-line health workers are having to re-use masks, or wrap scarves around their necks to protect themselves against sick patients.

That’s because the Chinese government bought up the country’s entire supply of masks from local manufacturers, causing a supply crunch in other countries in need, including the United States. US mask suppliers have been going full tilt for months, trying to fill the need, but their 1.2 billion masks will not come anywhere close to the anticipated demand of between 1.5 and 3 billion. And remember, covid-19 is just getting started in the United States and Canada. There will be a lot more cases before we are able to “flatten the curve” of rising infections, in WHO jargon.

During a White House briefing, President Trump said he will invoke the 1950 Defense Production Act to address potential medical supply shortages, and deploy two hospital ships to New York which has been heavily impacted by the coronavirus.

The act, established in 1950 during the Korean War, is described by FEMA as “the primary source of presidential authorities to expedite and expand the supply of resources from the US industrial base to support military, energy, space and homeland security programs.”

It’s my considered opinion that Trump could, and probably will, use his expanded powers to cancel the November election, one that, imho, he is no longer a shoe-in to win, given all the criticism against him regarding his handling of the coronavirus crisis, and the fact that Joe Biden, a moderate Democrat many Republicans could see themselves voting for, has overtaken Bernie Sanders in the Democratic primaries.

Trump, of course, has only himself to blame for dismissing the coronavirus out of hand, and delaying rolling out measures that could have started containing the virus weeks before the first actions were taken. Trump, in my opinion, was no doubt thinking about how closing hotels and gold courses would affect his real estate empire, as usual putting his own interests above those of the American people, many of whom could die for his self-serving lack of empathy.

If this isn’t the perfect environment for buying gold, I don’t know what is.

Gold juniors

Historically, and especially so today, for all the reasons to like gold, the greatest leverage to rising precious metals prices has been owning the shares of junior resource companies focused on acquiring, discovering and developing precious metals deposits.

Importantly, juniors are a cost-effective answer to the problem of gold reserves depletion. Because gold reserves are being used up faster than they are being replenished, it behooves the industry to come up with a strategy for reversing this trend – one that doesn't involve high-grading the best ore, which diminishes the value of the deposit - and M&A. Do you want to own the cheapest gold and silver you can find to reap the maximum coming rewards? If you do, buy it while it’s still in the ground.

Juniors, not majors, own the world's future mines and juniors are the companies most adept at finding these mines. They already own, and endeavor to find more of, what the world’s larger mining companies need, to replace reserves and grow their asset bases.

As smart resource investors, we recognize downtrodden sectors, and companies, and pounce on them when they go on sale. On the advice of the 18th century British banker, Baron Rothschild, “The time to buy is when there’s blood in the streets, even if it is your own.”

The markets are experiencing record volatility, and nobody knows where they are going next. Admittedly, making investment decisions now is tricky. Many are staying on the sidelines and waiting it out. But it’s not too early to at least be thinking ahead of the herd. Picking the right pure-play gold explorers who own the most attractive gold that can be bought at historically low valuations would seem to me a very prudent investing strategy.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified. AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice. AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

AOTH/Richard Mills is not a registered broker/financial advisor and does not hold any licenses. These are solely personal thoughts and opinions about finance and/or investments – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor. You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments but does suggest consulting your own registered broker/financial advisor with regards to any such transactions.

*********