New Trends Confirmed

In the previous US Markets it was anticipated that it would be a telling week – one that would either confirm that major trend changes are happening, or enable those who work so hard to maintain the status quo to continue their nefarious meddling with the markets. It is of course with much relief that this week it can be confirmed that some key trends have in fact reversed, doing so with vim and vigour for some and with a peek into despair for others. While the power and intent of the meddlers should not be underestimated, nor that this will still be employed, there is real good hope that their successes now will be limited.

Both precious metals have performed well, with gold doing better than silver on the technical development. The euro price of gold has also surprised with a break above its long term continuation pattern. The DJIA broke below key support, while the 10-year Treasury note may have reached a final low, and reversed just higher to make a bond market top. WTI crude had a bad week, but it may have bounced higher off key support to bottom off at least intermediate support.

A number of very long-term charts – to be presented in another report – show that major long-term trends are in the process of changing, supporting the views from the daily charts used in this report. It is still early times, but the provisional outlook is that gold, silver and the euro have turned bullish and then should remain so for an extended period of time. The US dollar has just started to follow the DJIA lower and could soon also be established into a bear trend. The 10-year T-note may have had its final rally to reach a market top for the current move and might turn bearish as well, or sideways if the flight to traditional safety persists. Crude dipped lower to reach support, but could bottom fish near the lows for quite some time still.

Most markets have been in overall bull trends for much longer than a decade and a few even much longer. Bear markets start off steeply; the damage to investors and the economy by the market collapse results in long drawn out weak performance by stock markets, typically ending with a new steep decline. The bear problems for a few markets will last a long time; new bull markets not be only a flash in the pan

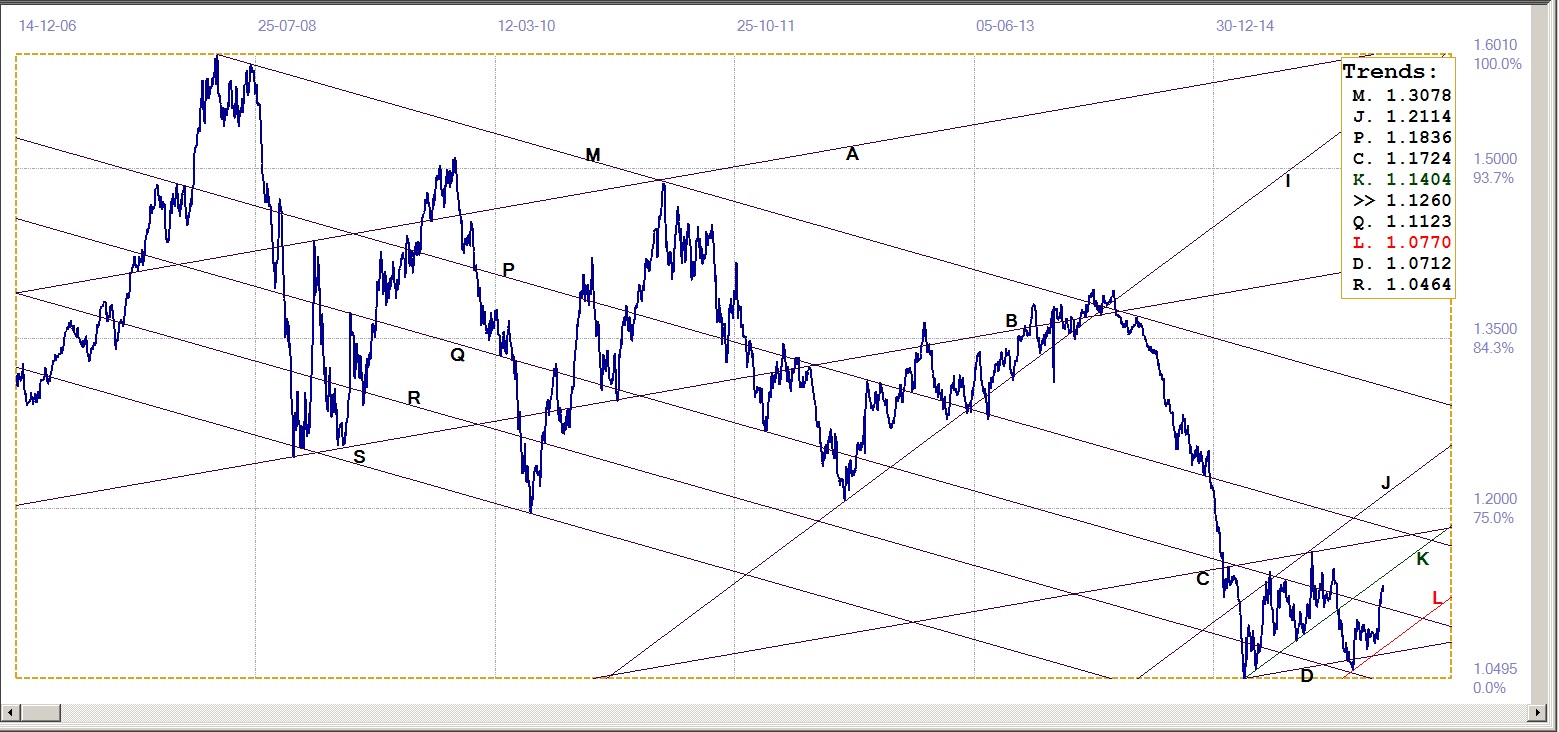

Euro-Dollar Chart

The euro spent some weeks in a narrow if volatile sideways trend; not really going anywhere while the strong dollar held a tight rein on most currencies. Now that the dollar has started to weaken, the euro rallied, breaking above a long unchallenged resistance at line Q ($1.1123) in one unbroken steep rise. There was little change on Friday before the US long weekend; this week will show whether the rally was over-done; or is it dollar weakness that is over-done and the US currency will rally again, to show other currencies their proper place in the greater scheme of things. It may well be that given a true bear trend for the US dollar, any corrections in the euro rally will be brief and contained.

Euro-dollar, last = $1.1260 (www.investing.com)

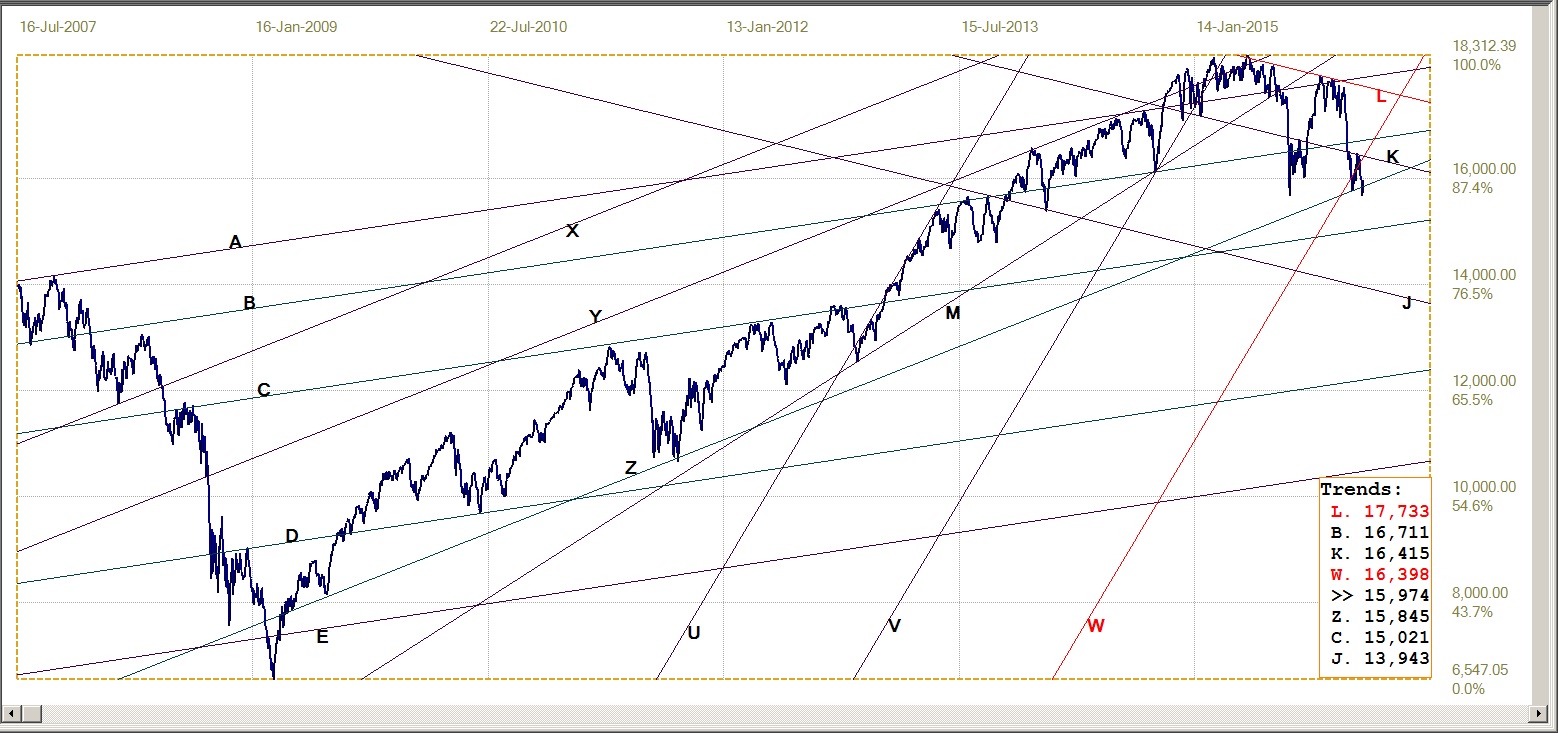

Dow Jones Industrial Average (DJIA)

Dow Jones Industrial Index, last = 15974 (money.cnn.com)

The second break below steep support from bull channel VW (16398) failed to hold at the support of line Z (15845) as it did on the first break below the steep support. This time it broke below line Z and then reversed direction to break marginally back above the new resistance of line Z; but not enough to recover into bull channel VW.

By doing so, what happens this week is in the lap of the gods; the new move higher on Friday could be a goodbye kiss on line Z that became a bit too exuberant; or is it a start on a move higher that will break clear in the bull channel? At least for now - and until a definite break back into bull channel VW – it has to be assumed that the break below the bull channel is intended to continue the longer-term bear trend.

Gold PM fix - Dollars

The persistent waterfall attacks still continue, but with a difference that they longer have the effect they used to do. On most occasions, the price recovers immediately and often shoot above the level prior to the waterfall.

Gold price – London PM fix, last = $1239.75 (www.kitco.com)

After previously having great trouble in holding above the steep support along line L ($1141), the bottom of the long term bull channel, the price has now managed to move well clear of its support to open a good cushion.

Rather than continually focusing on support, the next resistance at lines C ($1269) and Q ($1310) becomes interesting. It would not surprise to see a strong attack on gold – and silver – quite soon; the mass of new short positions from the effort to contain the rising trend can become a major liability if there is no opportunity soon to reduce that exposure. This can only realistically be done by scaring hedge fund players who have gone long into closing long position and perhaps selling shorts.

Any such event should however be temporary and even limited in extent. However, it would present an opportunity to enter the market or to add to long positions.

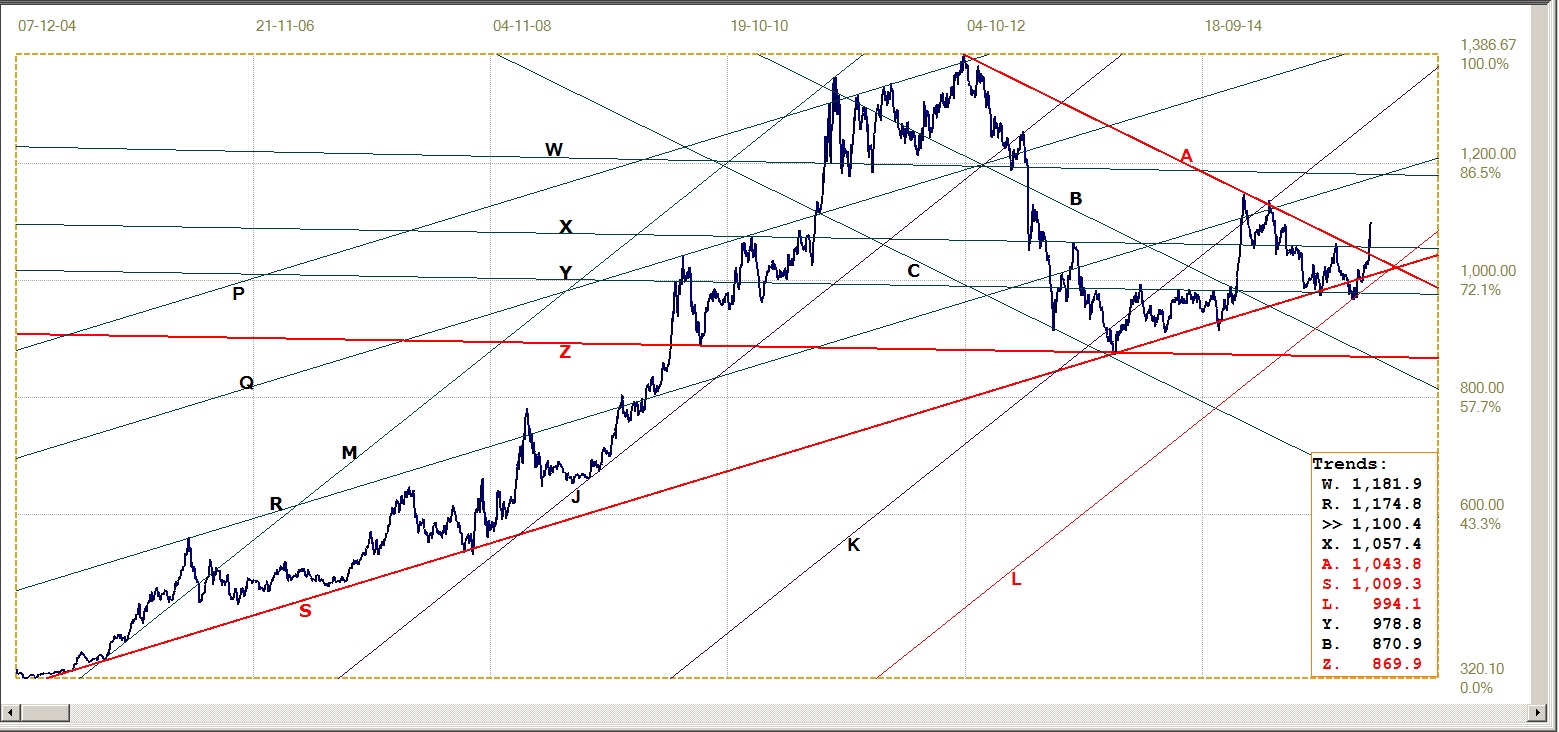

Gold PM fix - Euro

Euro gold price – PM fix in Euro, last = €1100. (www.kitco.com)

The euro price of gold has been in a sideways band between the resistance at line X (€1057) and support at line Y €979) since mid 2015. The volatility has been quite high, yet without really breaking from the band. For some time now, early strength in gold was balanced by a stronger euro, but last week the gold price rocketed far steeper than the euro. As a result, the euro price of gold has broken clear above the resistance at lines A (€1044) and X (€1057).

The break above line A, confirmed by the break above line X, is significant; it is a break higher from triangle AS at the end of leg 5 of the chart pattern. In general, such breaks lead into a long term bull market, which of course implies gold will continue to outperform the euro.

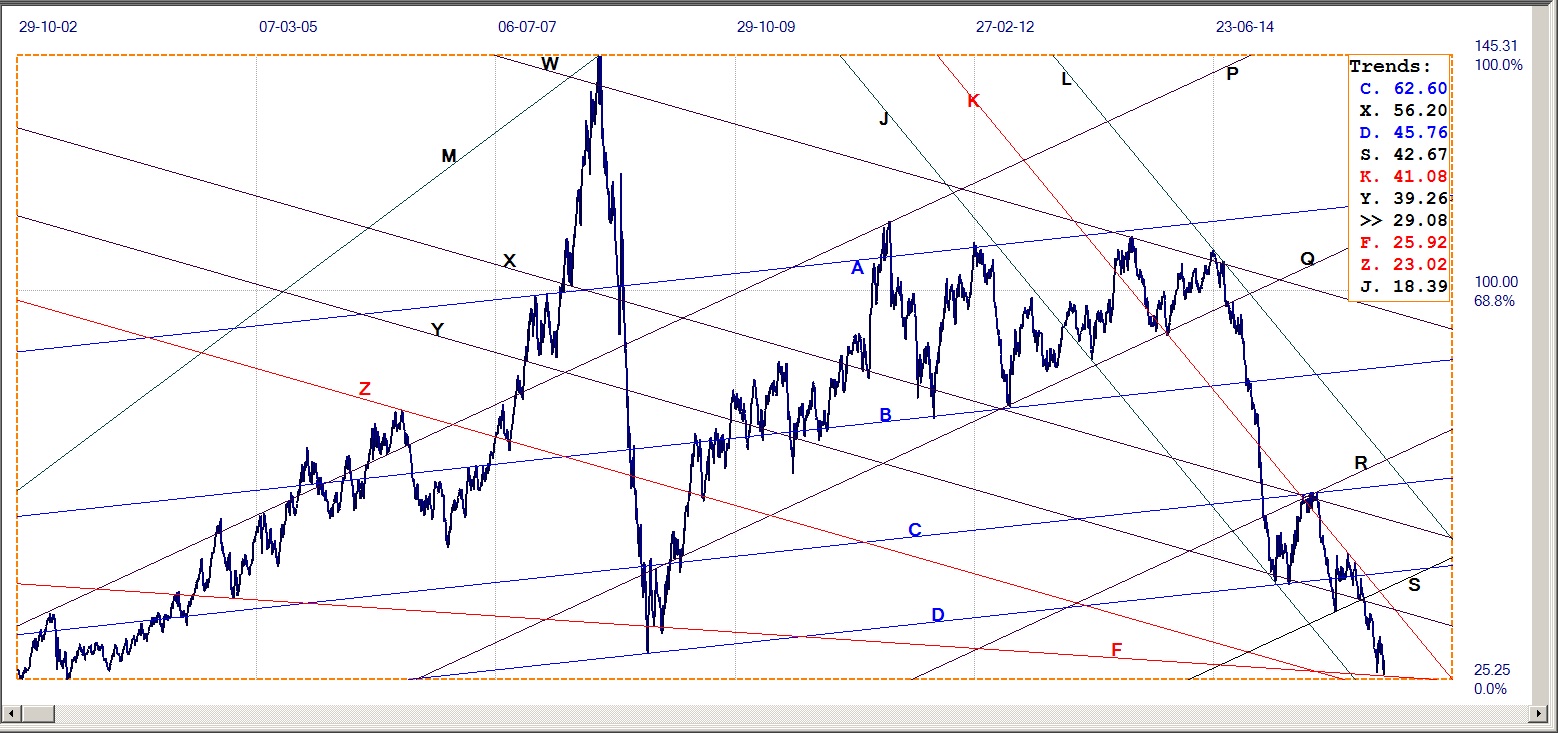

Silver Daily Fix Chart

Visually, silver does not appear to do nearly as well as gold. Perceptions however can be deceptive. The best way to illustrate firstly that silver is doing well, but also that silver has much greater potential than gold, is to compare by how much their price have to increase to equal the high at the top of the chart: gold will do so if the price increase another 50%; the silver price has to increase three times to do so.

This relationship supports a view I have for so long expressed, that silver has been the greater danger to the powers that be, more so than gold. Its price suffered more pressure than gold and was hit harder and sooner when there was any rally. Yet, in due course as the prices of the metals improve with greater freedom, silver will be a much better investment.

The first levels of resistance at lines D ($16.57) and R ($17.03) is still quite some distance away. Silver has to improve as much again as it did last week to challenge resistance at line D. Should the rising trend accelerate, it can be done even in this shortened US week, as silver will trade on Monday. That break from Comex might just be what the metal needs!

Silver daily fix, last = $15.64 (www.kitco.com)

U.S. 10-year Treasury Note

The Treasuries market used to be rather opaque, with information on who is selling or buying and how much not easy to obtain. In a busy market, the assumption can be that the Fed is the buyer while foreign holders of Treasuries – central banks in most cases- are selling; no longer the buyers they used to be.

2016 has seen a change. With Wall Street now suddenly more volatile with a strong bearish bias, investors have been selling equities to run for safety in Treasuries. As a result the yield on the US 10-year Treasury note has been falling for some time – to reach a low right at resistance at line E (16.75%), Channel pair CDE is divided in an exact 500:500 ratio, which implies that line E should be firm if the rally resumes after the slight weakness on Friday. This might imply the recent bull trend is now over, with the yield rising again or sideways at best.

U.S. 10-year Treasury note, last = 1.746% (www.investing.com)

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $31.00 (Investing.com)

The sharp spike lower held and reversed just short of support at line F ($25.92) to turn bullish as fast as the price fell to below $20/bbl. The new rally failed even to approach that resistance before reversing lower as quickly again – reaching almost all the way back to line F on Thursday, closing almost as low as before at $26.10.

On Friday, the news that the possibility of reduced out put by Opec spread through the market and gave a major boost to the price of crude and to Wall Street. Given today’s market ethics, one wonders whether it was truly the intention of the Opec countries to do so. Could it be that some have either reached pumping capacity and can only boost their revenue if they can get the price higher by raising a possibility of production cuts and then talking about it for weeks with little or no action, but with many press releases?

This may not push the price much higher, but at least keep it sideways above the technical support and prevent it from falling further. Given the really low prices at the moment, even a sideways trend would be a relief for the producers.

©2016 daan joubert, Rights Reserved

chartsym (at) gmail(dot)com