The Recycling Of The US dollars Financing The US Deficits Is Going To End (Part 3)

Conclusion why the US dollar’s reserve status is at risk

What is at stake is the reserve status of US dollar following:

-

Loss of dependency on Saudi oil because of the US becoming an oil net importer as early as 2019 making the Petro-Dollar contract less of importance.

-

The introduction of the Petro-Yuan-Gold contract planned for March 26.

-

Trade tariffs that will reduce the flow of US dollars into foreign central banks and as such the recycling of US dollars into financing US deficits.

-

The increasing budget and trade deficits that need financing from foreign investors (good for 48% of treasuries ownership), because Americans don’t save with a savings quote of 2.7%, and demanding higher interest rates. Also because the increasing US dollar hedging costs.

-

The blowing out of the Libor-OIS spread, the global yardstick for cost of credit and uncertainty, risk in the global credit markets.

-

Accelerating inflation, looming higher interest rates and the exhaustion/tapering of the QE measures that will not miss their impact on the tightening credit conditions resulting in the debasement of the currencies and especially the reserve currency.

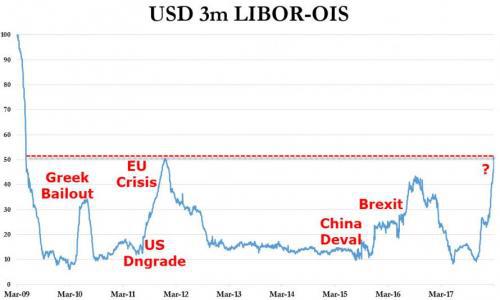

Ad 5 - I discussed points 1 to 4 and will discuss point 5 next. Why are people worried with respect to the increasing Libor-OIS? The Libor rate for three-month loans in dollars has climbed to 2.20%, a level it hasn’t reached since 2008.

Next to that the spread over the OIS rate or Overnight Index Swap rate (or Fed’s Fund Rate), has also widened quite dramatically following a Congressional deal on the U.S. budget and debt ceiling on Feb. 8, one of the most closely followed leading indicators of an imminent funding crisis and global credit crunch, broke above its 6 year range, when the USD Libor-OIS spread on Friday March 16, rose to 51.4bps. And in my point of view this time it is not offshore causes, like Brexit or the Greek Bailout, that triggered the spread to blow out but onshore causes such as the increasing difficulty to finance the US deficits. Next to that I want to emphasize that it is especially the speed of the move that is giving some investors pause for thought. Remember it is always the rate of change that worries investors because of the inability to adapt to the new situation.

Defining the two rates, Libor (officially known as ICE (InterContinental Exchange) Libor since February 2014) is the average interest rate that banks charge each other for short term, unsecured loans. The rate for different lending durations – from overnight to one-year – are published daily. The interest charges on many mortgages, student loans, credit cards and other financial products are tied to one of these Libor rates. In fact, over $350 trillion dollars' worth of financial derivative contracts, mortgages, bonds and retail and commercial loans have their interest rates tied to Libor.

Libor is designed to provide banks around the world with an accurate picture of how much it costs to borrow short term. Each day, several of the world’s leading banks (thus not only US banks!!!) report what it would cost them to borrow from other lenders on the London interbank market. Libor is the average of these responses. Libor also indicates how much trust there is in the banking system, between the US and Row, because these Libor rates will rise when banks don’t trust the creditworthiness of their counter-party banks anymore.

Though it should be noted that there has been an initiative to replace Libor with the repo rates. I wonder why? I am facetious of course because it is all about control! An industry body, the Alternative Reference Rates Committee or ARRC, convened by the US government, has chosen a new benchmark interest rate to replace the scandal-ridden Libor gauge as a reference for trillions of dollars of financial instruments. The decision brings to a head efforts to establish a new reference interest rate after Libor became tarnished by revelations of widespread rigging by the banks that set it, as traders sought to manipulate it to their benefit. And where do you think most of that rigging took place and what makes you think that won’t happen with the repo rate? Despite reforms to Libor, the ARRC took the decision to move away from the rate, as the market for unsecured transactions between banks has dwindled, recommending a brand-new, broad Treasuries “repo” rate, which will reflect the cost of borrowing cash secured against US government debt, as a replacement for the US dollar Libor rate. The new rate will be based on live, actual transactions and published by the Federal Reserve Bank of New York in co-ordination with the Office of Financial Research, in an attempt to reduce the risk of manipulation. This is in my point of view purely done in order to bring these benchmarks for credit purely under control of the Americans thereby reducing the influence of foreign banks. It is one big scam! Remember the more you control the less you are in control!

The OIS, meanwhile, represents a given country’s central bank rate over the course of certain period; in the U.S., that's the Fed Funds rate – the key interest rate controlled and fixed by the Federal Reserve currently ranging between 1.25% to1.5% and most likely to be increased by 0.25% on Wednesday. The OIS is derived from the overnight rate, which is typically a fixed rate by central banks. As a result, the OIS lets LIBOR banks borrow at a fixed rate over a specified time.

If a commercial bank or a corporation wants to convert from variable interest to fixed interest payments – or vice versa – it could “swap” interest obligations with a counterparty. For example, a U.S. entity may decide to exchange a floating rate, the Fed Funds Effective Rate, for a fixed one, the OIS rate. It should be emphasized that in the last 10 years, with interest rates at historical lows, there's been a marked shift toward OIS fixed rates for certain derivative transactions.

Because the parties in a basic interest rate swap don’t exchange principal, but rather the difference of the two interest streams, credit risk isn’t a major factor in determining the OIS rate. During normal economic times, it’s not a major influence on LIBOR, either. But we know that this dynamic changes during times of turmoil, when different lenders begin to worry about each other’s solvency. In the end it becomes about the return of your money and not the return on your money!

Prior to the subprime mortgage crisis in 2007 and 2008, the spread between the two rates was as little as 0.01% points. At the height of the crisis, the gap jumped as high as 3.65%.

So why does it matter that the Libor-OIS spread is widening! Short-term borrowing costs in the U.S. have risen to levels unseen since the 2008 financial crisis, and recent moves in two closely watched indicators -- the London interbank offered rate and its spread with the Overnight Index Swap (OIS) rate -- are causing some consternation. The spread has expanded to its widest level in more than a year, raising questions about whether risks might be brewing within credit markets.

The 51.4bps spread surpassing the 2011/2012 highs (and the widest level since May 2009), when the latest European sovereign debt crisis was roiling the markets and forced the Fed to open unlimited swap lines with the rest of the world to avoid a global dollar funding crisis and effectively bail out the world, which according to the BIS is synthetically short the USD to the tune of over $10 trillion - for the second time in 4 years.

Whatever the cause of the ongoing blow out in Libor-OIS, this move is having defined, and adverse, consequences on both dollar funding and hedging costs. This alone will have a severe impact on foreign banks, because as Deutsche Bank wrote recently, "the rise in dollar funding costs will damage the profitability of hedged investing and lending by [foreign] financial institutions.

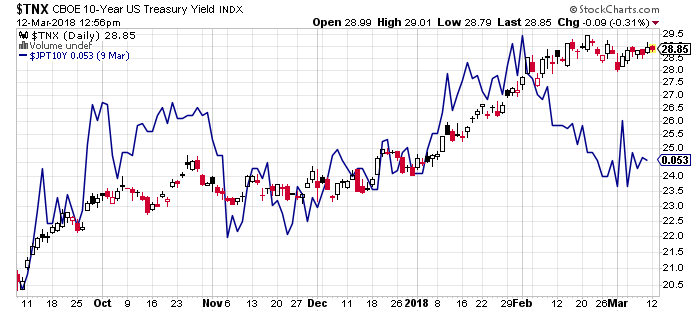

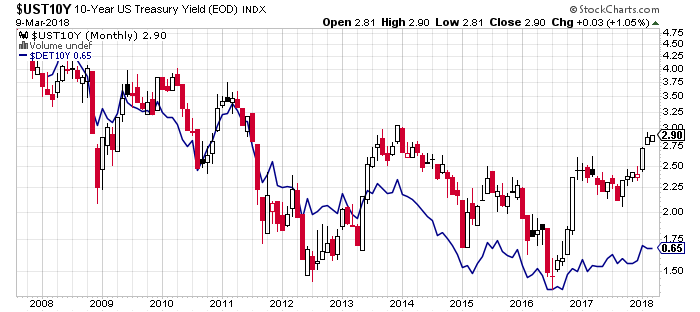

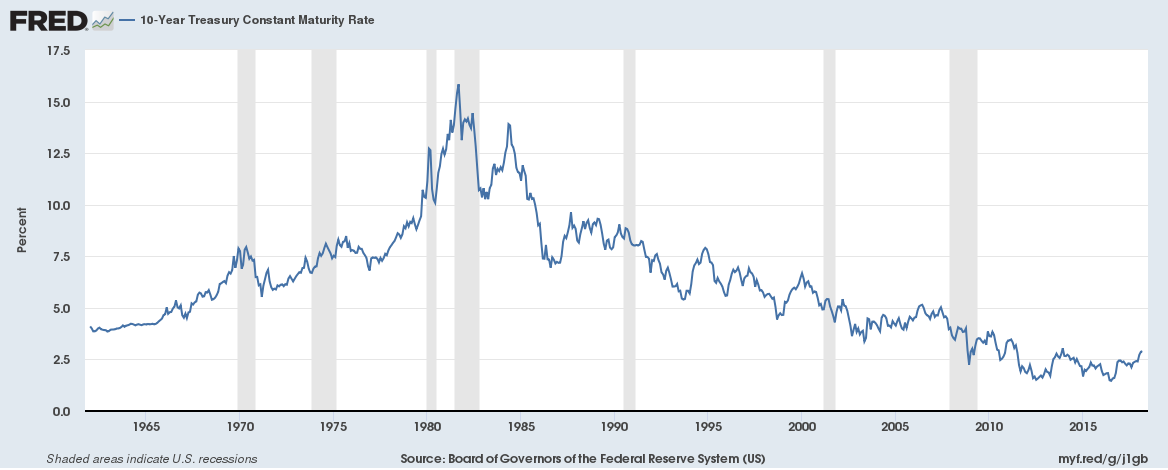

For example, one of the most immediate consequences is that it is now more economical for Japanese investors to buy 30Y JGBs, with their paltry nominal yields, than to purchase FX-hedged 30Y US Treasuries which as of this moment yield less than matched Japanese securities. The same logic can be applied to German Bunds, as the calculus has made it increasingly unattractive for European investors to buy FX hedged Treasuries. In other words the hedging costs for the US dollar are so high that it has become a deterrent to invest in treasuries and thus kiss even more goodbye to financing the US budget deficits. See below the charts of the 10y Treasury yields compared to the 10y Japanese and Bund yields.

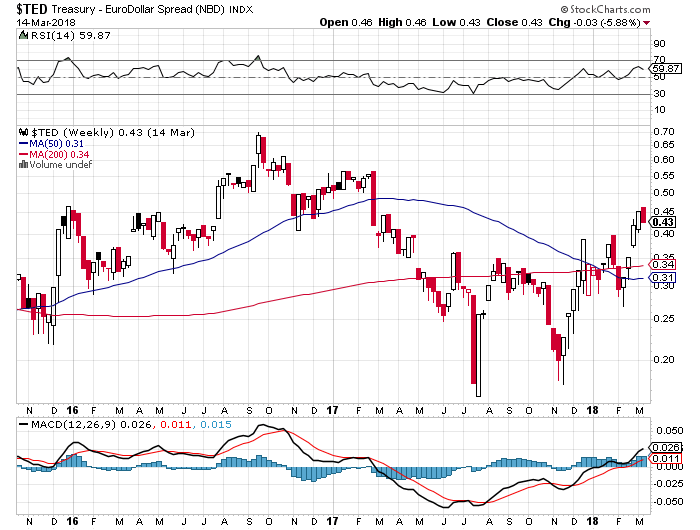

For completion purposes I will also briefly refer to the TED spread. The TED spread measures the difference in yield between the U.S. 3-month Treasury currently at 1.76% and 3-month Libor at 2.15% or 39bp. Since September 2009, the TED Spread has typically ranged between 10 and 20 basis points. During economic crisis it gets much higher. It spiked as high as 457 basis points in the fall of 2008, when Lehman and Bear Stearns were collapsing.

As mentioned the 3 Month LIBOR-OIS spread is the difference between Libor, now at 2.15%, and the overnight indexed swap (OIS) reflecting the Fed Funds Rate, which is 1.42%, or 73bp. As for the Libor-OIS spread, it typically ranges plus or minus 10 basis points. As mentioned during the fall of 2008, it got up to 365 basis points or 3.65%.

Importantly, the LIBOR-OIS spread, like the TED spread, tells investors how nervous banks about each other’s credibility. If LIBOR heads higher, widening the spread to the Fed Funds Rate, it’s a signal of shrinking liquidity and banks back off from credit transactions.

Ad 6 – The fear of accelerating inflation (especially following the implementation of trade tariffs) and thus even more pressure towards higher interest rates and the exhaustion (read loss of effectiveness) of the QE measures will not miss its impact on contracting credit conditions and the debasement of the currencies but especially the reserve currency.

As I already indicated in the previous point there is an upward pressure on the Libor and TED rates signifying increasing uneasiness with the credit conditions in the markets. The exhaustion of the efficiency of the QE measures and their tapering in the US and in Japan and Europe will not miss their impact on interest rates currencies and especially the reserve currency and thus also have a very positive effect on gold and silver.

Since I haven’t really referred to silver I just would like to comment on silver. Everything that applies to gold also applies to silver except that silver is extremely cheap at slightly above $16/oz. and unlike for gold silver has a lot of industrial applications representing about 60% of total demand in 2017 or about 520m oz. The Silver Institute projects continued growth in 2018 and not the least because of silver’s unique qualities that seem to improve and enable new inventions and thus increase its demand. For example because of silver’s excellent electrical conductivity, strong demand is forecast from the automotive segment as vehicles become more electrified and computerized. Strong demand is also expected from photovoltaic applications. Large-scale solar capacity additions and uptake from individual households, particularly in China, should also boost silver demand. I think that silver is one of the most undervalued assets there are at the moment hence also why I show the chart here below which shows a technically very attractive picture. And as a last remark on silver, it is in general gold that is confiscated and not silver next to that silver will most likely rise quicker to $160/oz. (10x) than that gold will rise from $1,310/oz. to $13,100/oz.

While everyone still believes that stocks will hold up, the bond market is constantly hovering between 2.80% to 2.90%. When we break the 3% level the way is open to its next major resistance level of 4.25% (I refer to MSA’s excellent momentum research by Michael Oliver) resulting in all markets undergoing a severe price readjustment.

The reason that all markets will be affected is that bonds, not stocks, represent the bedrock, the foundation of the financial system. Bond bear markets are considered to be much worse and last much longer than bear markets for stocks because everything is benchmarked/valued against interest rates: bonds, mortgages, stocks, currencies, commodities etc. etc. Bond markets have a much deeper more profound impact on the economy and peoples finances than stock markets. And the other important factor that will worsen the impact is that the breakout of yields out of their long-standing multi-decennia trading ranges is not just happening in the US but is also happening in Germany, Japan, and other countries, see charts below.

The breaking out of the interest rates out of their long-term trading ranges is a global phenomenon, as is the case with the global corruption of the politicians which often is a sign of the end of a cycle. Just read the “The decline and fall of the roman empire” by Gibbon. The reason I allude to the corruption of the majority of the politicians is that they seem to be solely concerned about the numerous benefits they can acquire being a politician like expense reimbursements, full pensions (Congressional pay was $174,000 per year in 2016, for just 133 days of “work”, which, at an 80% rate, equates to a lifelong pension benefit of $139,200!!) and a light workload, rather than looking after the interest of the people that have elected them to fulfill their election promises.

You just have to look at the Congress and the Euro Parliament. Especially the fringe benefits and the lax rules of the European Parliament are disgusting and can basically be defined as pure thievery. And how can one expect from these people that first look after themselves that they have the best interest at heart of the societies they are so-called representing in parliament. Everything is tuned to their own interest. We see the same in the USA with the Deep State and more unambiguously the Clinton Foundation that has only ponied out half a percent of all the funds they have received and bought so called (very cheap) HIV drugs sourced from a bogus company in India that were useless to solve the HIV problem in Haiti. The Clinton Foundation is solely a charity for the Clintons and nobody else. “We were broke when we left the White House” remember the interview with Hillary Clinton!

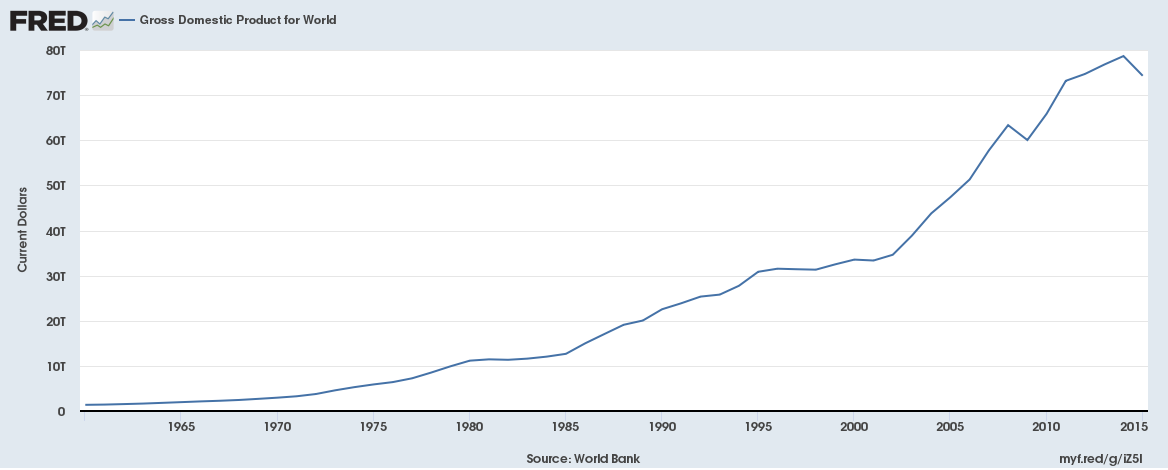

As if we haven’t learnt anything global debt has increased from $150trn in 2008 to $230trn in 2018 a CAGR of 4.37% whilst over the same period global GDP has grown from $63.5trn to $79.6trn or a CAGR of 2.29%.

And this is with historic low interest rates! Just imagine worldwide interest rates increasing on average by only 1%. That would mean that global interest charges, the US in general sets the tone in interest rates, will rise by 1% over $230trn or $2.3trn ($2300bn), that is an amount that the world can’t stomach. $2.3trn over global GDP of $80trn is 2.9% that is equal to roughly the projected global GDP growth percentage for 2018; the World Bank is forecasting GDP growth of 3.1% for the world in 2018! In other words the worldwide debts can never be paid back and thus we will face either a debt implosion or the debt will be inflated away or we will get a debt jubilee whereby a lot of debt will be forgiven. In any case someone (a few more people) will incur losses and it will not be pretty hence why the authorities are doing everything to keep the gravy train going till they can’t anymore. There is no painless solution. You have to ask yourself what you need to preserve your wealth when the paper money will lose all its credibility.

As I have referred to many times gold stands for discipline and has value of its own, not dependent on the corruption and incapabilities of the politicians and monetary authorities, whilst paper of fiat money doesn’t represent discipline (can be printed at will) and doesn’t have value of its own (paper doesn’t have any value it is available in abundance) and whose value is purely relying on the counter party promise of the Fed to ensure that the nominal value mentioned on the green paper keep its purchasing power.

Though as we have seen in earlier charts the purchasing power of the US dollar has fallen by an astounding 84% following increasing deficits since we abandoned the gold standard in 1971. Remember politicians don’t have any discipline when they can solve the shortage problem by printing a few more dollars! In fiscal year 2000, Treasury receipts in the Oct-Feb period were $741.8 bn, nearly matching outlays of $741.6 bn though in fiscal 2018 receipts in the Oct-Feb period were $1.286 trn whilst outlays had risen to $1.677 trn. Receipts are growing an average 4% per year, whilst outlays are rising an average 7%.

Source: Reuters

Hence why we witnessed a most troubling double-digit jump in interest expenses on the public debt, which in the month of February jumped to $28.4 billion, up 10.6% from last February and the most for any February on record. In the first five months of this fiscal year, October 1, 2017 to September 30, 2018, interest expenses have already accrued to $203.2 bn, up 8.0% y.o.y and the most on record for any Oct-Feb period.

Source: Reuters

Though it should be stated that February is traditionally not a good month for the US government, that's when it usually runs a steep monthly deficit as tax returns drain the Treasury's coffers. However, this February was worse than usual, because as spending rose and tax receipts slumped, the US deficit jumped to $215 billion, the biggest February deficit since 2012. For fiscal 2018 (4Q17-3Q18) the US fiscal or budget deficit is forecast to increase to approx. $800bn - $1trn or 5.1% of 2018 GDP (was $666 billion, or 3.5% of GDP).

The sharp increase comes as the US public debt rapidly approaches $21 trillion. And with the effective interest rate now rising with every passing month, it is virtually assured that this number will keep rising for the months ahead. Wait till we break the 3% yield on the 10y Treasury and we go to its next technical resistance level of 4.25%. It will defy all those people that always say “oh but interest rates are still relatively very low”.

What isn’t understood in my point of view is that as a result of these historically low interest rates debt levels have risen astronomically ending in the end resulting in a huge absolute interest amount on a huge debt, low interest rates or not. And don’t underestimate that going from 3% to 4.25%, is equal to a 42% increase.

I believe that the 2018 trade deficit (exports – Imports) will remain equal or will be lower than the 2017 deficit. In 2017 the trade gap in goods and services rose to $566 billion, the highest level since $708.7 billion in 2008. Imports set a record $2.9 trillion, swamping exports of $2.3 trillion. The goods deficit with China hit a record $375.2 billion in 2017, and the goods gap with Mexico rose to $71.1 billion.

And thus, most likely to still incur a half trillion trade deficit, the USA will need strong capital inflows to compensate for these shortfalls or deficits, because Americans have a very low savings rate (2.7%), in order to prevent the free-fall of the US dollar, because the alternative is monetizing the deficits, which will also result in much higher interest rates. On top of the deficits we have the other factors that are having a tightening effect on the dollar liquidity leading to higher rates: the launch of the Petro-Yuan-Gold contract, the trade tariffs and inflation that seems to be awakening.

Nonetheless I strongly believe that it is counterproductive to penalize allies towards ‘supporting and underwriting the dollar system’ as history has taught us. It is my strong conviction is that it is just a matter of time before the increased risk in the US markets and the drying up of debt funding from recycled US dollars will push US interest rates up or force the US to monetize the increasing and out of control debt levels. Well both situations are not an expression of fundamental strength hence why I believe that the downside on the US dollar will much higher than the upside.

I hope that the abovementioned has illustrated why the US dollar and thus the US, who was a major beneficiary of the global trade and FX regime, could be more than ever before on the brink of losing its reserve status.

What's coming will be much worse than 2008, everything is converging and is coming to a head. All the tools in the toolbox are exhausted!

March 19, 2018

© Gijsbert Groenewegen

Silverarrowpartners