Return Of The Epocalypse

In August of 2015 I started writing about The Great Recession 2.0 that was coming upon us. I called it “The Epocalypse” to signify an economic apocalypse that would be epic in scale and that would begin a new epoch on earth — a time of treat global financial decline.

I led into my series on the coming Epocalypse by writing, “Far more people listen to their aspirations than listen to my beliefs about a coming global economic collapse.”

I warned that dire times would descend when the Fed stopped juicing the economy with massive injections of new Fed money (quantitative easing/QE) and began to remove that money, as they promised they would.

Now we know the Fed cannot ever unwind. We saw its failure when it tried throughout 2018 and caused a stock market crash at the end of 2018. As soon as the Fed got up to full speed in rewinding its “money printing” of the past decade, the stock market started too fall right when I said it would, and it didn’t stop falling until the Fed stopped raising interest rates and promised it would not go as far was it said it would with sucking money back out of the economy. For the time, the market settled down.

Things did not go as badly as I said they would back in 2015 because, even back then the Fed did not go as far as I felt it had led the world to believe it would go; but now that the Fed finally did go that far, all of that is coming back around to where I think it is time to revisit what I said about the Epocalypse, bringing it up to date with current events.

The big market breakdown that could be seen from miles away

The lead-in to the series was an article titled, “How the Coming Global Economic Collapse will Play Out” in which I began,

Ask yourself this if you’re inclined to listen to Cramer or Larry Kudlow or Larry Summers or Federal Reserve ex-presidents or the other big, giant heads: Did they tell you that the Great Recession was coming back in 2007? Did they tell you that the stock market was going to enter deeply troubled times last fall when it plunged but then rebounded? Did they tell you that you could take that earthquake to be a signal that the top of the market had been reached and that it would trade sideways and round off into a fall and then take a huge plunge … all in 2015? Did they tell you after that September-October plunge that stocks would overall lose value this year and be a bad investment?

The answer to all of that, of course, was no; but the stock market broke that year for exactly the reason I said it would — Fed QE ended! Simple as that. For two years, the market did nothing but bust along sideways until the Trump Rally finally boosted it again with the hope of massive stock buybacks that would be fueled by corporate tax breaks to essentially replace the QE the Fed had discontinued.

The two-year broken bull looked like this:

The world, however, did not end financially as I said it would because the Fed didn’t do all it said it would. (It has today, however, so everything I said would happen when it finally did do all it had said, now comes back into play.) For the time, the Fed kept all QE in place by continually rolling over all the bonds it had purchased, which I did not realize was its intention, and I don’t think it really had ever communicated it would do that.

I understood what the Fed meant by saying it would end QE was that they intended to let the bonds as their means of injecting money into the economy roll off their books as they matured since they said they would do no more bond purchases. What they really meant for the time wash that they would do no more bond purchases that would add to their balance sheet. they meant they would stop adding to the global money supply, but not that they would start diminishing it by no longer rolling over old US bonds as they matured with the purchases of new bonds.

Ah, well, no one’s perfect. Diminishing money supply, it turned out was phase two, which did not get seriously under way until 2018, which is when all the big trouble began to break out before our eyes. First in the stock market, then at the end of the year a foreshock deep at the heart of banking in the most fundamental and boring of areas where banks loan money to banks in what are called repo loans:

Something wicked this way comes

All the Fed really did was quit increasing QE. Even so, you can see all growth in the stock market died immediately, and the economic landscape became quite rough and barren in terms of the stock market. Imagine if they had actually tried to roll back QE then, as I thought they meant when they said they would end it. Everything would have crashed into a pit of ruin — the pit I was calling The Epocalypse.

That’s where we are now … with the help of a viral shove into the pit, but we need to recognize we are falling into a pit we spent years digging out. I will get into that in my next article, which brings this series back to our attention while updating it to present circumstances. In the rest of this article, I’m going to briefly recap how we dug the pit.

Even though no one I read back in 2014 saw that two-year breakdown in the market coming, I’ve been roundly criticized on some sites for saying the sky was falling in late 2014 when that first little dip in the graph appeared just as we approached the period when QE was supposed to end. I felt that dip as a foreshock of fear in the marketplace over what was about to begin.

Of course, all the criticism came later on during the Trump Rally; but who can really call that long stretch in between the rally we were ending in 2014 and the Trump Rally a living, breathing bull market? At the end of that two-year stretch your stocks were worth EXACTLY what you paid for them two years prior. If that still deserved being called a bull market, it was a bull lying on the ground, panting, sweating and bleeding out at the end of the Obama years.

If you missed out on that two-year stretch in the broken market because you listened to what was written here, you missed out on nothing but a lot of tail-bone splintering bounces to nowhere. Consider the period a prolonged foreshock, foreboding what lies ahead now that the economy has collapsed on the back end of the Repocalypse.

And the market wouldn’t have recovered if not for Trump getting elected and breathing new hope into the market, though it was vain hope because we only dug the pit of debt much deeper to find the material used to build a new rally over it. The more we dug that debt, the more we were undermining the rickety structure we were building over it. Still, the structure soared temporarily to great heights and impressed many.

The end of QE did not bring the end of the world financially, as I had said it would only because QE didn’t really end. (The Fed kept rolling over the bonds it had purchased under its QE program and keeping them on its books. So, it constantly renewed QE for a few more years, but just didn’t expand it. In fact, it actually did tweak expansion a little in that it also rolled over the interest it earned on the bonds it had purchased — both government and corporate MBS.) So, money supply actually continued to grow very slightly throughout 2015, 2016 and most of 2017.

We all know, however, what happened as soon as the Fed finally did attempt to roll back some of that QE. The stock market crashed as soon as the roll-back got up to full speed in the fall of 2018. Then banks plunged into the Repo Crisis (or Repocalypse) in the final quarter of 2019 just as the Fed finished rolling back some of its QE. The Fed, in fact, had to stop rolling back QE sooner than it said it would and had to start lowering interest again. Within only a few months, the Fed even had to resume QE, which it did by pumping up the repo market every day and then going back to government bond purchases in the fall while claiming it was not resuming QE, which had been nothing but bond purchases for year.

It gave up all pretense of not resuming it as soon as the coronacrisis hit and when back to purchases government bonds of all maturities and all the rotten mortgage-backed securities and all other forms of rotten debt it had consumed during its original Great Recovery effort. It has returned to everything it had to do during the Great Recovery at levels that are digging out pits of debt far faster than ever before in order to pile up supply of new “money.”

The rally to nowhere

Then came the Trump Rally, funded by massive corporate tax breaks and the equally massive one-off repatriation of foreign profits. All of that accomplished nothing but to pump up stocks via buybacks, exactly where I said all the money would be spent before the tax breaks even became established law.

That’s when people scoffed, “Ha! You were wrong. The world is great again. Watch us now fly like Icarus toward the sun!”

For awhile, they were right because a vast ocean of newly available money began pouring through the flood gates into stocks. However, even though the market was rising downstream, I pointed out continually that the underlying economy was slowly drowning. I noted how GDP got a two-quarter boost when the tax cuts first hit, then went completely stagnant quarter after quarter while corporate profits began a long decline. I noted how the drop in unemployment bottomed out to flat for months and how more and more corporate debt was sliding toward a junk rating. Housing slumped for a year. Auto sales crashed. Restaurants starved as retail shuttered its doors. The economy was ever-so-slowly folding inward the entire time.

That’s because none of the saved taxes went into anything that could boost actual business or productivity. Again, I had said before the cuts became law, that the Trump administration would have required no buybacks from corporations taking the new tax breaks if the administration really wanted to boost the economy and not stocks. It would have made sure the money went into building the economy and not just vainly inflating stock prices. Trump could have let corporations choose, which was best for themselves — do buybacks and stay with the old tax rates; or don’t do them and claim the lower taxes — but he didn’t even do that.

The rally was entirely hollow because it was not built at all on growing business or a growing economy. The economy was completely stuck at a mediocre 2% growth, not the 3, 4, or 5% Trump had promised we’d see. Corporate income only grew as mirage created by the effect of having less taken out off the bottom line from taxes and the effect of buying back shares so that earnings were distributed over fewer shares, making it appear earnings were higher. (Not really. The number of shares they were divided over was lower.)

Because there was no underlying economic growth in those companies or in the overall economy to support their rising stock values, most of the paper wealth created by those buybacks evaporated in just one month as soon the coronavirus. The tragedy there is that there is now NOTHING left to show for pouring all those tax savings into stock buybacks. Nothing!

The tax cuts resulted in no new factories, no shiny new equipment inside old factories, no new markets opened up, no expansions of research and development, so noe great burst off new innovation that wasn’t already happening without the tax breaks, no new industrial paradigm like the industrial revolution or the blossoming of great tech economy.

It’s all gone! Just like that! All the money has literally evaporated with nothing to show for it at all because we didn’t built anything with it other than stacks of paper wealth.

A perfectly matched codependency

Now the Fed and government are working overtime to reinflate it all, and we’ll have to see how that works; but there is no underlying economic strength created during the Trump Rally that will help pull us out of the depression that is opening up due to the coronavirus global shutdown.

We created no savings among consumers nor any reduction of consumer debt — so, nothing that left consumers in a stronger position to weather the storm that is now assailing them. We did just the opposite throughout the Fed’s Great Recovery and the Trump Rally. The Fed enticed people to go deeper into debt. And now many are piling up debt to save themselves as their income has been reduced or, in some cases, eliminated. As a result, consumers will have less power to consume when we open back up for business.

We built no new businesses, speaking in net terms. We actually saw IPOs decline in the corporate realm during the days of the Trump Rally, and we saw retail stores and restaurants and auto manufacturers and dealers decline the entire length of the rally. Businesses of those kinds that were alive but marginal just before the coronavirus hit the world like a meteor, will not reopen after the virus is subdued by our global shutdown. They could barely survive without the additional debt created by the shutdown and without the costs of reopening.

Businesses and consumers ended the Trump Rally more deeply in debt than ever. So, we are not in a strong position for recovery because we used all of that potential energy to create mountains of virtual wealth that papered over caverns of enduring debt, and the paper wealth that covered the debt can evaporate overnight, as it did!

The Fed is not in as strong a position either. As Reagan’s former budget director, David Stockman, likes to see, the Fed entered this situation out of dry powder. It had not managed to lower its balance sheet or to get interest rates back up to it has almost nowhere to go with interest, and who knows what side effects will come from doubling the size of its balance sheet in the next year or two over what it was at the height of their recovery efforts? But there will be bad side effects from taking so much medicine. There will be greater distortions in the market than we saw during the Great Recovery (a term I mean only sarcastically by the way, as it was a colossal failure in that it made all our underlying problems worse just to give us an adrenaline push for years).

Now the Fed and government are doing everything they can to pump those stocks back up again. It’s a good thing for the US government that the Fed needs to “create money” to bail out institutions because the Fed does that via purchasing government debt. Our dollar is really just based on debt, not gold — just trust in the Almighty Fed as it creates money in bank reserves out of thin air to vacuum up government bonds.

That times out well because the government right now needs to sell more bonds than ever to finance its fiscal economic salvation efforts, while it has fewer buyers. So, the Fed is the government’s Financier of First Choice.

The US government has not only added over $2 trillion to 2020’s deficit in just one month with its bailout/aid package — all of which the Fed will have to finance — but it has pushed off tax day by ninety days. That means it is going to indebt itself about four times faster than its past deficit over the next three months at a time when there is no nation out there wanting to buy US government bonds because they have enough of their own problems to try to finance.. So, Trump needs Powell more than he has never needed him.

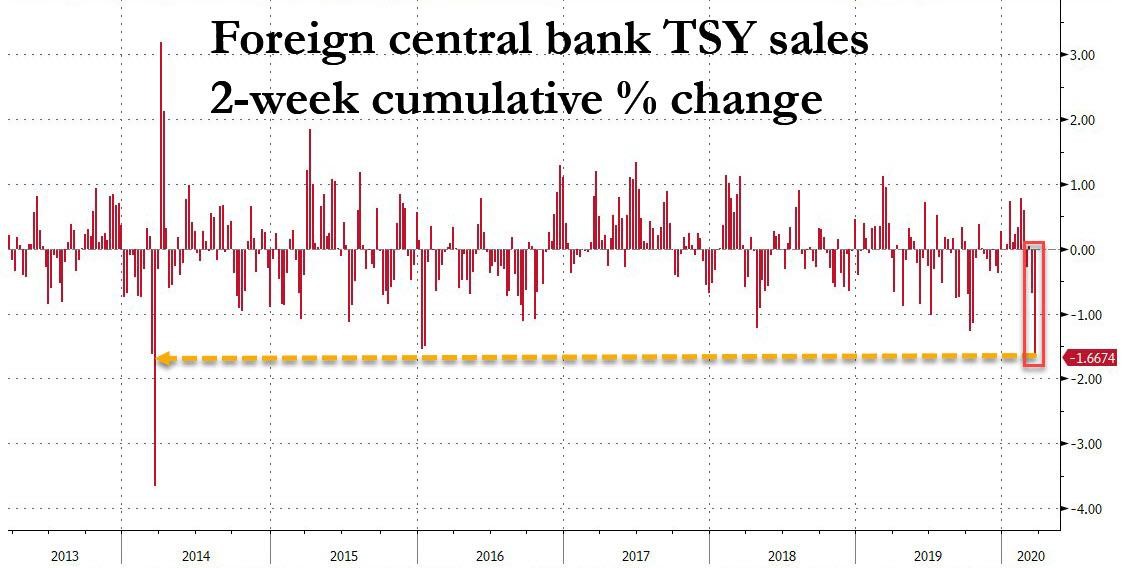

They are, in fact, offloading US bonds, not buying them:

One look at the Treasury securities held in custody at the Fed shows that the past two weeks have seen a whopping $50BN in foreign central bank sales, a 1.7% drop which was the highest in six years since Russia pulled over $100BN in TSYs from the Fed in response to US sanctions imposed over the Ukraine conflict in 2014 which was precipitated by the US state department.

As Bloomberg observes, the selling may have contributed to record volatility in the Treasury market and prompted the Fed’s intervention. More importantly, it also means that the biggest buyer of US Treasurys in the past decade, foreign official institutions (i.e., central banks and reserve managers) are now sellers, so now the U.S. government needs private investors to soak up the ever increasing debt issuance. And since those are busy avoiding a deadly virus, it means that only the Fed now can fund the exploding US budget deficit… which is precisely what it is doing.

So, we are now in a situation where the Fed is going to have to become a vacuum cleaner to suck up all US debt. Trump and Powell will now become fast friends. During the Trump Rally, Trump was continually begging and cajoling Powell into more money creation to save his rally from the snags it was starting to hit due to the trade wars. Talk of trade wars is completely dead. Now, Trump and Chump are finally both on the same team. Each are willing to spend and create debt as fast as possible — Powell to save dying banks and dying businesses, Trump to boost the rally that he wore as his badge of success back into life and to save the economy.

Powell will be Trump’s new chumpanzee — his organ-grinder monkey.

Return of the Epocalypse or not?

So, it is time, at last, to revisit what I said the Epocalypse would look like. How far into it we descend depends, I suppose, on how successful Team Trump and Chump are at jacking things back up; but it appears to me fires are erupting everywhere faster than Powell can put them out, and Trump has his hands full of a viral infection.

We enter the new recovery period with no reservoir of strength built up from the entire Great Recovery the Fed engineered or from the Trump Rally because all of that was paper wealth, and all of that is gone! So, we crawl into recovery with both of our legs cut off, taking what may be deadly amounts of FedMed to kill some of the pain, but the medicine is not as effective as it used to be.

On to the Epocalypse …

*********

David Haggith publishes The Daily Doom and writes satire. The Daily Doom contains economic, social, and political news about our troubled times--a non partisan weekday collection of the most consequential stories about our complex times with insightful editorials and weekly economic analysis. As an equal-opportunity critic of America's sharply divided, two-ring political circus, David divides his satire into sister publications so you can pick the one you find agreeable and ignore her sassy sister.

Support David Haggith by subscribing on Substack.

More from Gold-Eagle