Review Of The Current Bear Market In Stocks (Part 1)

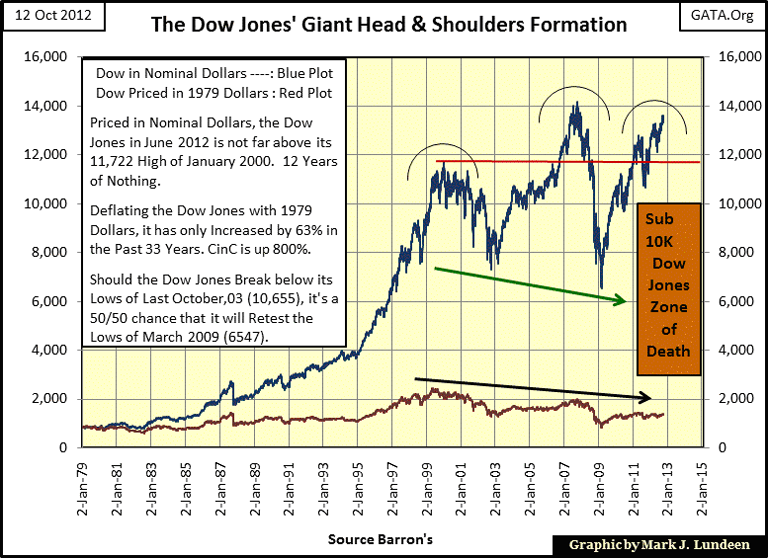

Let's look at the stock market first, with a chart of the Dow Jones' monster head and shoulders chart. I first posted this chart in the summer of 2011 with the Dow Jones's over 12,500. Soon after, the Dow began going down and bottomed at 10,655 on 03 October 2011, declining 1800 points.

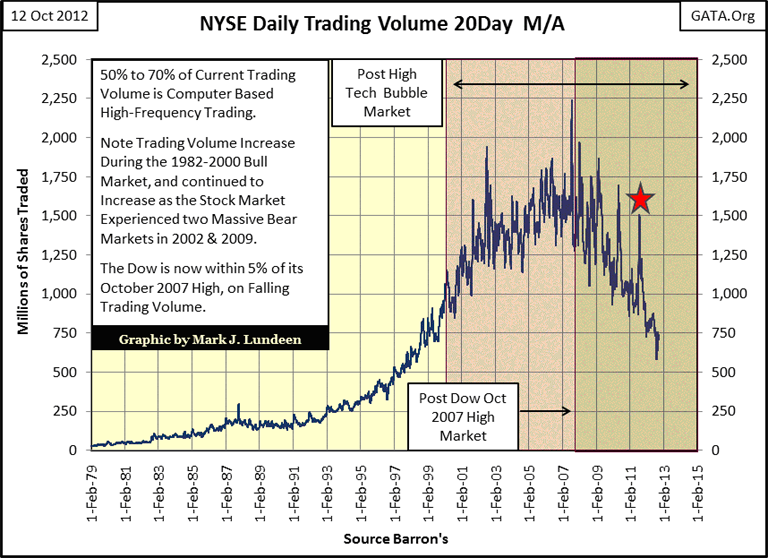

A year ago, it looked like the Dow Jones was going to break below 10,000 and keep going down. But the "policy makers" made sure that didn't happen. I can say that as this decline, like all other Dow Jones declines since 2000, have occurred on rising trading volume.

Look at the NYSE Trading Volume chart below; I placed a star over the trading volume increase during last year's late summer 1800 point drop in the Dow Jones. Compare the price action of the Dow Jones above with the NYSE Trading volume below. As soon as the value of the Dow Jones stabilized in October, and resumed its rising price trend that continues to this day, trading volume also resumed its relentless decline.

This incredible twelve year violation of the law of supply and demand has been a fixed feature of the American stock market since the beginning of the High-Tech Wreck in January 2000. In the shaded area of the chart below, volume spikes almost exclusively identify market declines - and this just isn't natural. So, it must be a "market policy", implemented at the highest levels of government (the PPT), to prevent the stock market from declining to valuations far below what Washington and Wall Street needs them to be.

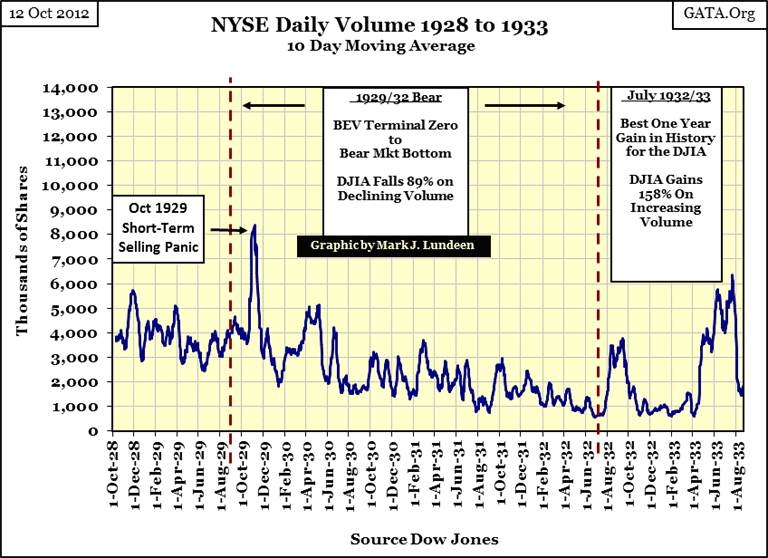

To better make my point, below is a chart showing NYSE trading volume during the Great Depression crash, and for the Dow Jones best year ever (July 1932-33):

- The Dow Jones Valuation Declines with Trading Volume

- The Dow Jones Valuation Increases with Trading Volume

From January 1900 to January 2000 (100 years), this was how the stock market worked, but not for the past twelve years!

I believe market commentators no longer cover trading volume either because they are unaware of its historical relationship to market valuations, or because they would be embarrassed having to explain trading volume's pole-reversal twelve years ago.

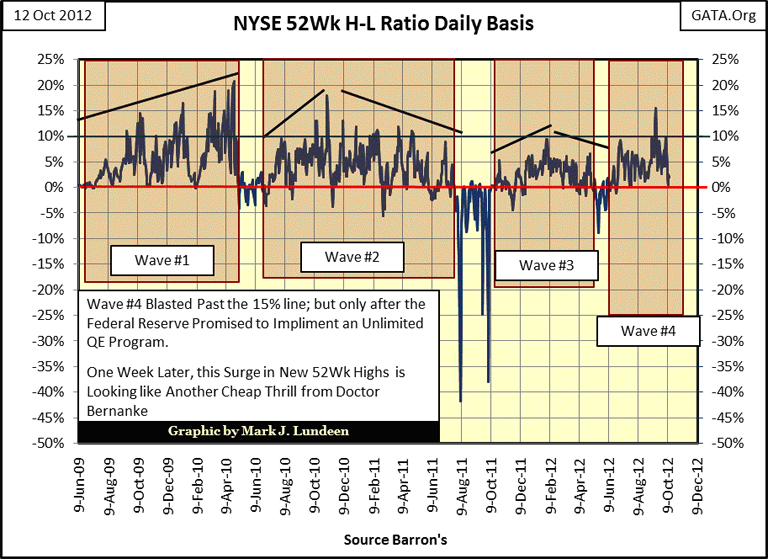

Now on to the NYSE's 52Wk H-L Ratio; the ratio has been positive since June 26, or seventy seven consecutive trading days. Yes, the ratio did break above 15% for one day in wave #4, but since the correction of August-October 2011 (waves #3&4), the number of stocks making new 52Wk highs at the NYSE has been pretty lackluster. Look at waves #1&2. These waves occurred during the time when CNBC could see "green shoots" as far as the eye could see, and the market bulls had plenty of energy to charge upwards toward a new all-time high in the Dow Jones. But it's obvious that after the Aug - Oct 2011 correction, the market bulls haven't been eating regularly, and new NYSE 52Wk highs are difficult to come by.

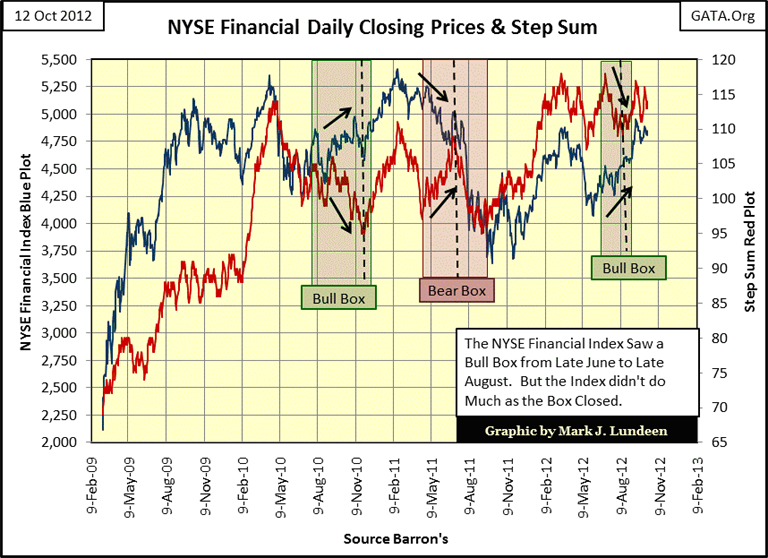

Here is a chart I haven't shown for a few months, the NYSE Financial Index's step sum chart. This index fell 78% during the credit-crisis market crash, from 9982 in June 2007 to 2110 in March 2009. During the crash, the SEC prohibited naked short-selling of financial companies. They had to as the big banks were shorting their competition into extinction; these people eat their own! By the way, with this prohibition of naked short-selling, the SEC admitted that they do look the other way when the big banks commit illegal actions, like selling shares short without actually obtaining them. Do you doubt that the SEC is looking the other way as the big banks are nakedly short selling the mining companies listed on the XAU? There can be no doubt that they are!

The NYSE Financial Index was a real money maker from March - October 2009, but hasn't done anything for anyone since. Gold, silver and mining shares have been much better investments since their credit crisis bottom. Keep in mind that these companies were ground zero of the credit crisis. The entire stock market crashed for no reason of its own, but because these financial companies were writing fraudulent mortgages for years. The only reason they stopped was because they ran the banking system into the rocks, with trillions of dollars of illiquid-toxic mortgage backed paper for their reserves.

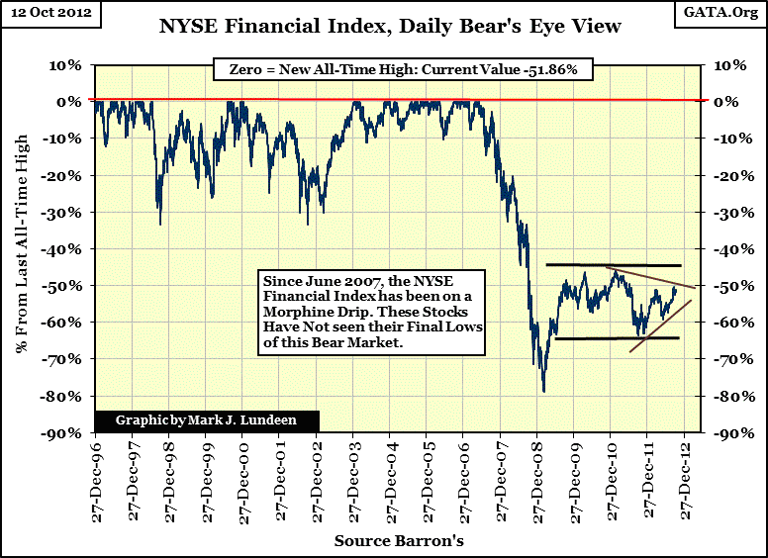

Keep in mind that other than changes in accounting rules, to allow banks to post worthless assets at face value, and that the Federal Reserve is willing to purchase these worthless assets at face value from the banking system to keep the banking system "liquid", nothing has changed. Look at their Bear's Eye View chart below. They crashed 79% during the credit crisis, and have gone nowhere between their BEV -65% & -50% lines since for the past three years. A word of advice to anyone considering buying J.P Morgan or another big bank on the recommendation of the financial media; someone is selling you damaged goods.

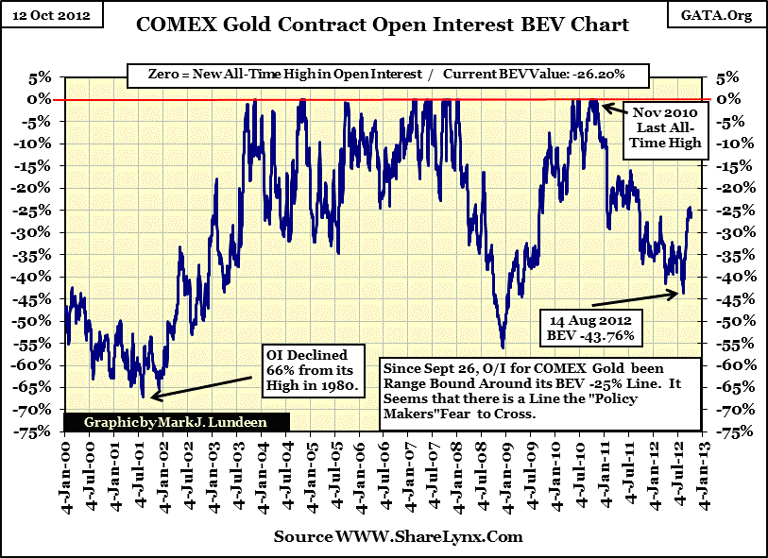

Let's move on to gold and silver. Since August 14, open interest exploded as the price of gold began breaking out in late summer, but since late September open interest stopped increasing. As open interest is the number of actively traded contracts in a future market, increasing open interest increases supply, which is bad for the price of something, unless demand increases, too.

We know that the "policy makers" want the price of gold, and silver, to fall back down, so why don't they continue increasing the number of contracts trading in the COMEX gold pits? It might be that the big banks who love to short the gold market are afraid that demand for gold will continue to increase with the supply of their paper gold contracts, trapping the banks in a losing trade that they can't exit from. Should demand for gold overwhelm supply, there would be a spike in the price of gold, which would be very expensive to anyone shorting gold. It might be that a big spike up in the price of gold could bankrupt the banks on the short side of this trade, and they know it.

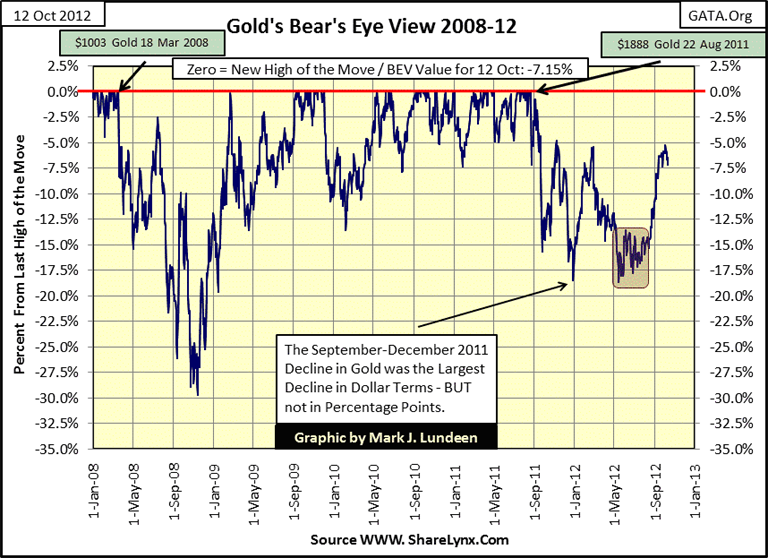

For all the increase in gold's open interest since August, the price of gold had a nice advance, and could use a little rest. Price corrections can happen in one of two ways:

- The price trend declines

- The price trend goes sideways for some weeks or even months, allowing the bulls to take a well-deserved rest.

Gold currently seems to be correcting in the horizontal fashion, which is fine with me.

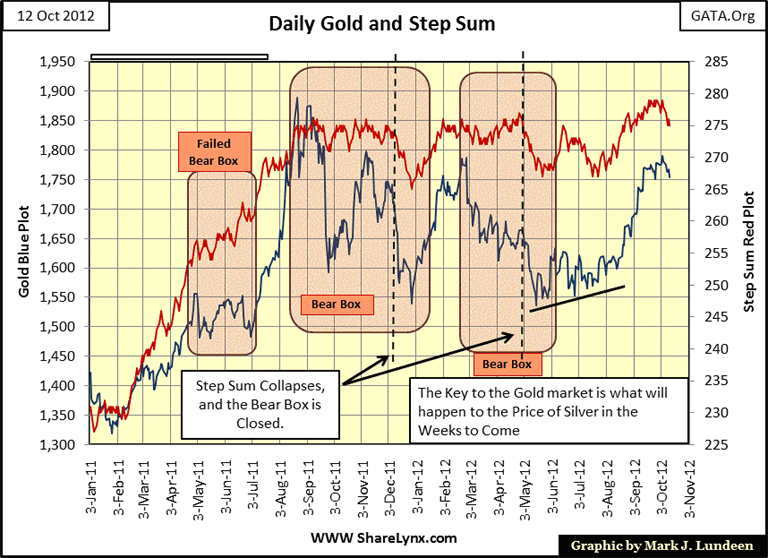

Not much going on in gold's step sum chart. The price and step sum trends both agree that the gold market needs a little rest.

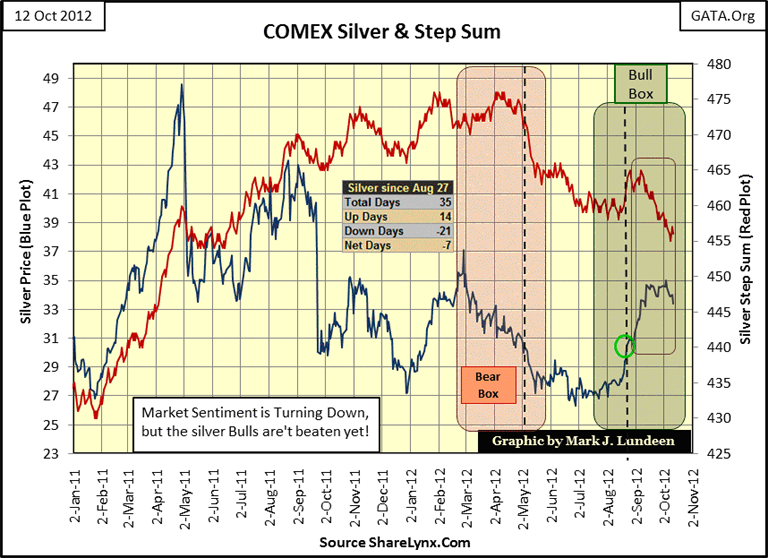

I think the key to the short-term future in the price of gold is found in the step sum chart for silver. Look at the bull box for silver below. I first closed this box in August as silver's step sum finally reversed upwards with the rising price of silver, and then had to open the bull box again just few days later. What does that mean? Simple, the silver bears are determined to prevent the price of silver from rising. I seem the silver's rising price is an especially sore point for the "policy makers."

There is a real battle for Stalingrad going on in the silver market. The bears are refusing to admit defeat, and at Friday's close the bulls have begun to bend under the pressure. Will the bulls break, causing a waterfall decline in the price of silver? Or do they have what it takes to come back, and stick it to the bears with a market close well over $35 an ounce. I have no idea how this bull box will be resolved, it could fail with a big decline in the price of silver as silver's step sum continues going lower. This is a real possibility, but it's just as likely that the bears will once again lose the battle, with a sharp upward reversal in the step sum as the price of silver leaps over it $35 resistance level. This is really something to watch, because if the silver bulls win this battle, gold and the mining shares will probability see a nice payday too. Like you, I have to wait and see how this battle royal ends, maybe next week.

Mark J. Lundeen

[email protected]

[email protected]

More from Gold-Eagle