Risk Management In An insane World…

Firstly, my home town of Toronto was recently hit with a “Mad Driver” that killed ten people and injured fifteen in an absolutely insane illustration of “New Millennium” violence. What was and is instructive about this act is that once CSIS (Canadian Security Intelligence Service) got hold of this nutbar’s computer, ALL PUBLIC INFORMATION ceased. We had excellent reporting from the local media on the act but once the “authorities” got hold of the data, all reporting went into “lockdown”. As a former resident of one of the most ethnically-diverse “major cities” on the globe, I find this type of news censorship reprehensible and not in the general best interests of the public. It is also rumoured that the lockdown occurred immediately after the perpetrator’s computer was impounded and the hard drive analyzed driving speculation that his actions were not triggered by his pitiful sex life but rather by something far more sinister like Islamic jihad or an ISIS association. This is once again an example of Big Brother controlling our minds and opinions but it goes a lethal step beyond those by suppressing information that affects public safety.

To decide behind closed doors and under cloak of secrecy that the contents of this murderous bastard’s PC remains “classified” is analogous to the Harper government telling the world back in 2008 that the Big Five Canadian banks were “unaffected” by the sub-prime meltdown while their U.S. subsidiaries were inhaling TARP money faster then one can say “monopoly”. Or the Bank of Canada maintaining their “accommodative” policy long after the 2008 crisis had passed in order to allow the banks to expand their mortgage books by creating the biggest bubble in history with skyrocketing real estate prices across the country. The actions of the global central banks propping up stocks and bonds while suppressing precious metals is yet another example of these numerous violations of what I depict as the “natural order” of things (that should be left alone).

I was reading about the ramifications of introducing new species into habitats where they have not previously flourished and the first example that comes to mind is the lamprey eel which found its way into the Great Lakes by way of the lift locks built along the Saint Lawrence River decades ago. This creature would attach itself to those massive lake trout and sturgeon that were indigenous to Lake Ontario and in the 1940’s and 1950’s, it had a devastating impact upon the Great Lakes fisheries. Similarly, the introduction of European rabbits to Australia had a similar impact on agriculture where they became feral pests in the absence of any natural predators. The introduction of beavers into Patagonia created a massive overpopulation that threatened the forestry and environment for the same reason. Whenever mankind tries to mess with the natural order, either intentionally or not, it creates disastrous and unintended consequences. This is what I have been haranguing about for nigh on ten years now since the bailout of dozens of “Too-Big-To-Fail” institutions in New York and London. The financial experiment carried out by the central bankers with their “quantitative easing” travesties was anything but a natural method of dealing with corporate bankruptcies and that is really all the 2008 Financial Crisis was – a massive insolvency brought on by bad business decisions and inadequate risk controls. Had it been a bunch of farmers in Iowa or shipbuilders in Glasgow, they would have been out of business but since it was the campaign contribution specialists in New York, these golden geese were rescued at the risk of an outcome we have YET to assess. Remember that, if nothing else. The repercussions of indiscriminately printing trillions upon trillions of dollars, yen, yuan, and euros HAVE YET TO BE FELT.

Damage caused in Patagonia by beaver dams built by creatures imported from Canada

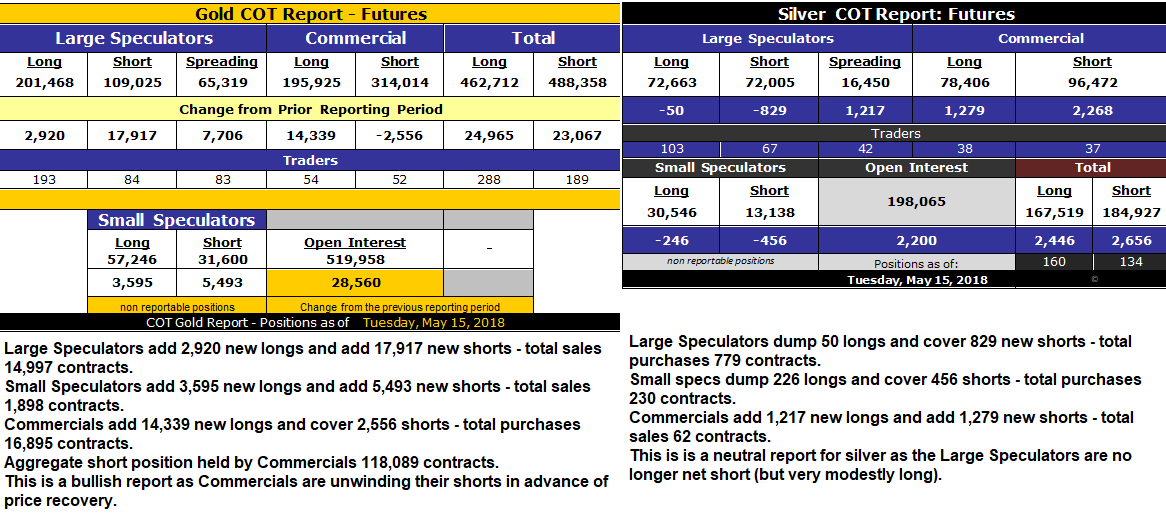

Last week’s COT report was wildly boring and after reading Gary Tanashian’s beautiful rebuttal of the bullish implications behind the silver COT of a month ago, I must confess that he made a great deal of sense in how he views the COT reports as “sentiment gauges” as opposed to “directional indicators”. It was five weeks ago with silver at $16.50 that I pontificated myself to a near-death state about how the Large Speculators were going to be S-Q-U-E-E-Z-E-D once the Commercials got sufficiently long. As always with the silver market, it just kinda-sorta “didn’t happen” (at least for very long) and after a very brief probe above $17.00 (like 2 days), it collapsed fitfully over the next eleven days to a new reaction low of $16.07. If you ever watched a hockey fight from the 1970’s, enforcers would pull the opponent’s sweater over his head and proceed to “windmill” the poor slob who was unable to either see or defend resulting in an exceedingly one-sided bout, closely resembling the manner in which silver investors are pummelled by the bullion banks time after time after time. No matter how brilliant the LOGIC is in one’s analysis, the outcome is ALWAYS the same; silver has a brief pop and then drops despite overwhelming evidence that global demand is “robust”. Groundhog Day, indeed.

https://ca.investing.com/equities/52-week-low

I have made it a habit to randomly canvas the new-high/new-low list for the TSX Venture Exchange in an effort to determine what is happening beneath the surface of the junior mining markets and today was a real shocker as there were over 200 companies making new 52-week lows today. Among them were some notables such as B2 Gold, Balmoral Resources, Pretium, Hive Blockchain, Novagold, Stakeholder Gold, West Red Lake Gold, and Tinka Resources. These are names that were highly-visible during the last few years and investors seem to be throwing them all under the closest bus. On the new high list, there were more than a few of the junior and senior oil stocks that popped up but with the big reversal in companies like Marathon and Diamond Drilling today, the oils might just have a negative effect on the S&P over the balance of the week. The bottom line is that the juniors are going to need some sort of catalyst to inject any type of financing life into them. I can recall explaining to the CEO of a junior explorer back in 2010 why he should stop drilling and simply sit on his (then) $10 million working capital position. “The only reason you drill is to earn the right to get to the next financing AT HIGHER PRICES. If market conditions dictate that no matter what your results are, you are not able to raise additional money, then drilling is a waste of time, money, and shareholder resources.” This particular CEO determined that the guy (me) that took him from a $90,000 working capital position and $3.2m market cap to a $10 million working capital position and $150m market cap was wrong and he proceeded to “drill, drill, drill” until all of that precious working capital was gone and the share capital had to be rolled back. That company, btw, was on the “NEW LOW” list today with a print of $.03 per share. (We exited in 2010-2011 pre-1-for-5-consolidation at $.50-plus per share.) If a proposed drill program cannot advance the stock price or working capital position or both, you preserve your treasury and live to fight another day.

Finally, I am officially revisiting the “volatility trade” (VIX) but unlike February where I used the UVXY as my proxy for the increase in volatility, I am using the TVIX because it is a double leverage ETF for the VIX but has better leverage than the UVXY. UVXY used to be a triple-leverage play on volatility but the slippage due to its dependence on futures became too difficult to navigate and they cut the leverage from 3:1 to 2:1. I had a 250% gain on this in February but gave back 9.84% in April. I am long 50% of the TVIX position from yesterday at $4.95 and am using the opening this morning to add another 25% in the $5.25 range. I will again use a 10% stop-loss but since the 52-week low is $4.66, that will be the exit level. Upside target will be $8.00 remembering of course that the 52-week high was $26.56.

The month of May is rapidly coming to a close which starts what is historically the worst six months of the year. With the situations in Turkey and Italy worsening, with the North Korean summit in question, central banks engaged in “quantitative tightening”, rising oil prices, and the possibility that the China-U.S. trade talks go south, markets are going to be in peril as summer illiquidity arrives. For this reason, gold “should” be the go-to asset but I am banking on volatility rather than gold as the preferred method of riding the correction.

********