Stock Market Melt Up Continues as Anticipated, Gold Lurks, Changes to Come in 2024

The macro market backdrop is not likely to go the way trend following market watchers currently anticipate

In fact, with patience it could turn out to be like shooting contrary fish in a barrel. The stock market rally – which NFTRH had anticipated a year ago on a larger basis and since October of this year for its next leg on a more compact time frame – is doing a wonderful job of holding to its seasonal pattern (see below). The rally is sucking in the holdout FOMOs who, one by one are falling for the duel pleasantries of a softening Fed and by extension, a Goldilocks-like “soft landing” scenario for the economy.

Okay fine, dear come-lately bullish soft-landers. But please consider that the author you are reading at this very moment called Goldilocks nearly a year ago, at the dawn of 2023 in this post, among others:

“This would be a whiff of the ole’ Goldilocks regime. A whiff, mind you. I don’t think we are going to see the likes of the 2013-2018 experience. She’ll eventually get nabbed with a bowl of ‘just right’ porridge in her hands.”

With a year’s worth of positive reinforcement (of their trend following natures) today’s economists are 76% percent in the belief that the chances of a recession are less than 50% and BoA is predicting a “soft landing” rather than a recession. BoA, in line with Cramer and a growing group of shiny happy economic people.

As with the post linked above that proves yours truly was very early to the Goldilocks party, I was also in time for the declining Treasury yields aspect of the Goldilocks play. Like, calling the top in the 30yr yield exactly to the day (dumb luck, but technically educated). Again, any perma-bear can rail on about the contrarian bearish play developing. But it means more when it comes from someone who was prepared (and prepared NFTRH subscribers) for the bull a year ago, and interpreted that an initial response to declining yields would be in the Goldilocks/sentiment relief vein.

Am I touting my accomplishments of the last year? Sure. I admit that freely. I am also someone who fesses up to my bad calls. Credibility is important because amid the noise of social media, the mainstream financial media and even the smaller niche media, few remember who may actually have proof behind their words and who may be simply jumping the train in ‘me too!’ fashion.

So I think we understand each other. NFTRH got the 2023 rally right. What’s more, all this “soft landing” crap was part of the plan. As the stock market rises, analysts and commentators find the need to re-tool their outlooks lest they no longer be analysts and commentators. Many are selling their ability to harvest your eyeballs (not to mention your heart and mind), after all, more than their ability to provide timely and accurate guidance about the markets.

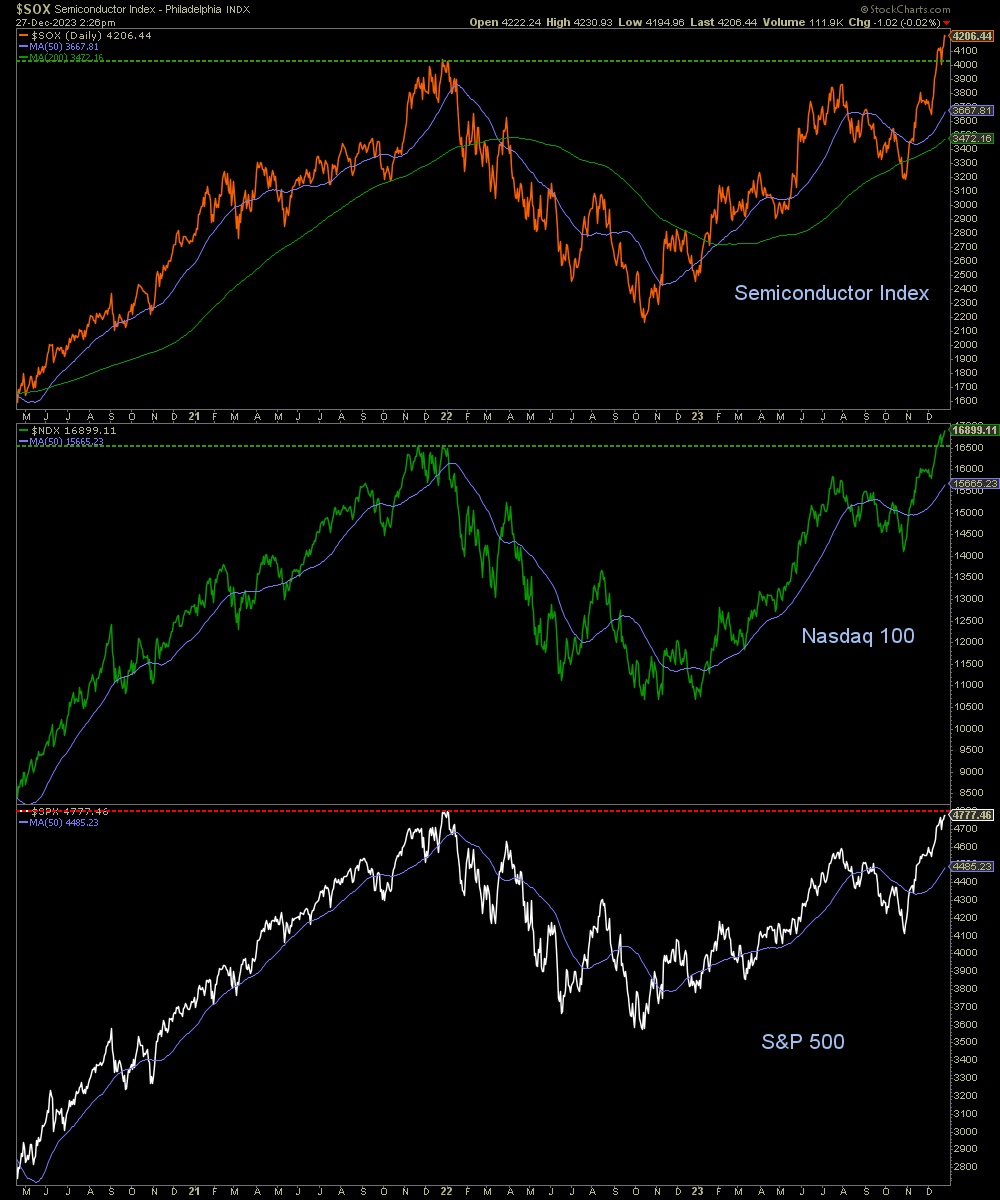

That necessary preamble out of the way, let’s move on to the 2024 market view. One of the most important guides we use has been the Semiconductor (SOX) > Tech (NDX) > Broad (SPX) leadership chain. In ratio to each other, Semi is still leading Tech, which is still leading SPX. Nominally, SOX and NDX (and the DJIA) have all recently dinged “NEW ALL-TIME HIGHS!!!” Cue the media touts when SPX joins the party and the last of the FOMOs cannot take it anymore and jump in.

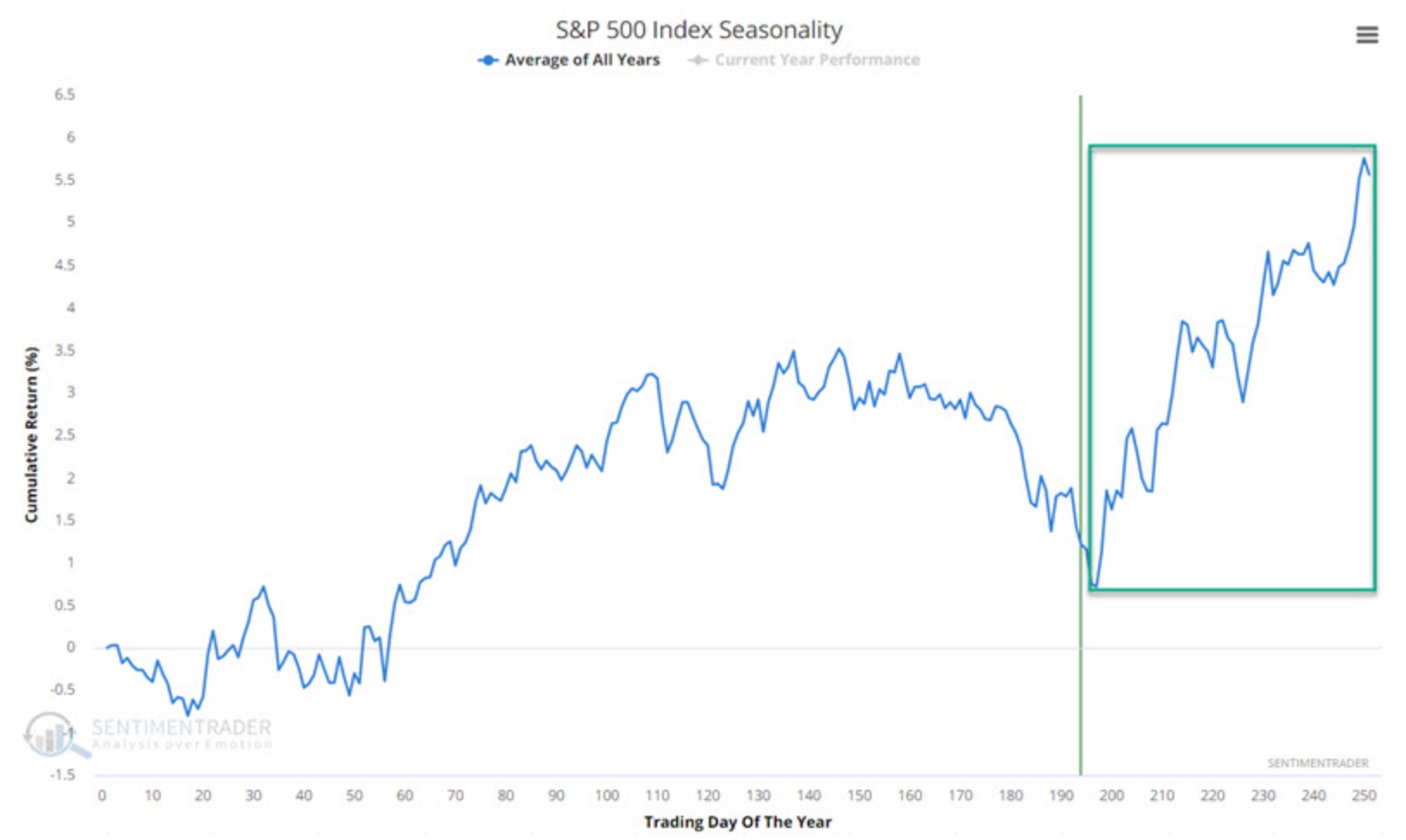

Consider that this is happening during the holiday seasonal…

Sentimentrader.com

…that was set up to bull on cue in October due to moderately over-bearish dumb money sentiment that is now extremely over-bullish.

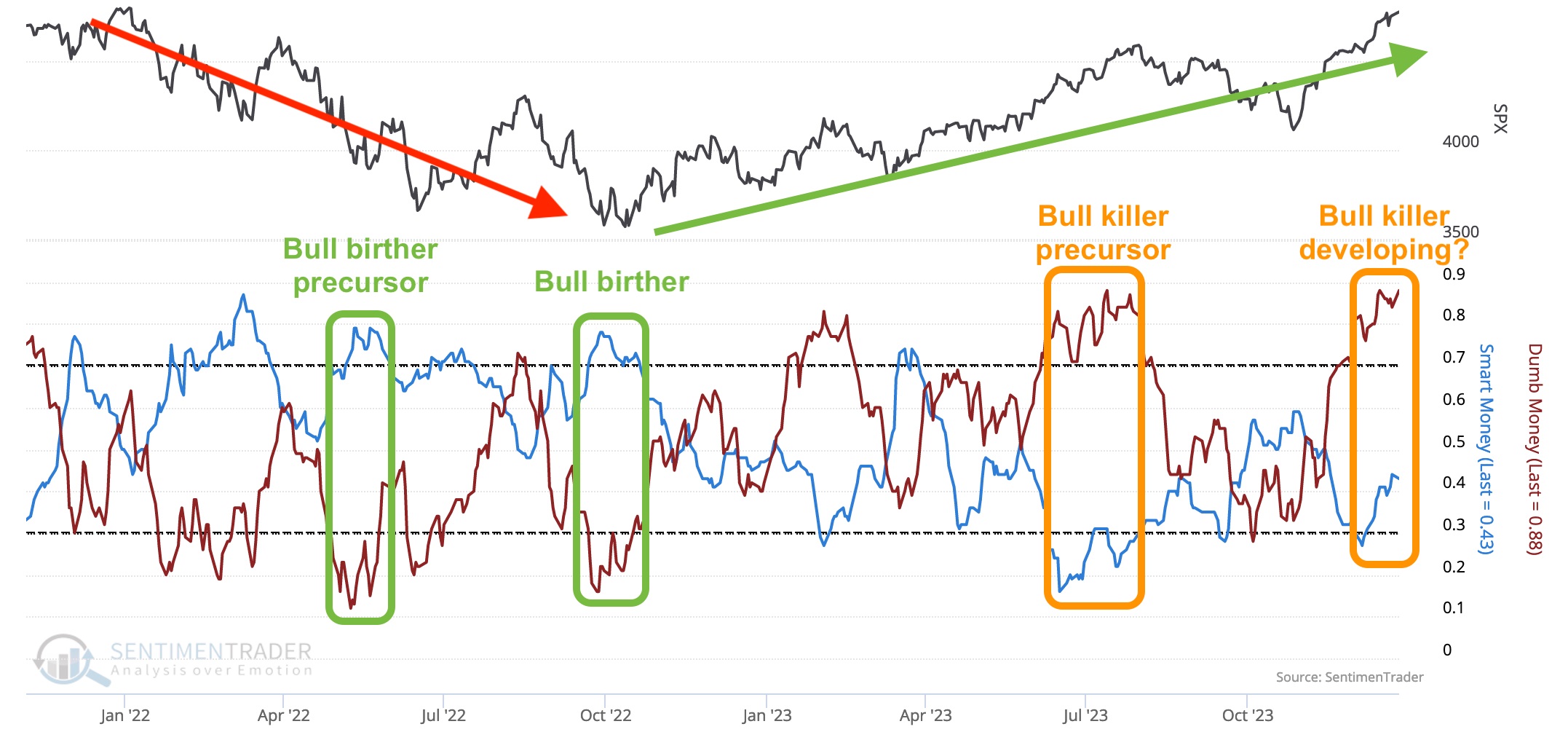

Sentimentrader.com (w/ my mark ups)

You know that a contrary play is worth its salt when it forces someone who anticipated it as just a play to consider whether it might actually be what the majority think it is. Markets always push the limits and I have lately considered elements that could drive a bullish market out to spring time (the anticipated timing of the Fed’s first rate cut, which is when market traditionally tank). But with all the rules the market has broken since 2020 it is under no obligation to wait that long before it cracks.

Our favored view continues to be that it will not wait that long. The seasonal extends into February and sentiment is blazing hot. Markets often blow out to the upside after a FOMO-driven melt up. Witness the Nasdaq in 2000 and Silver in 2011, as two examples. As a disclaimer so that we understand each other, I am not short one single thing right now. I am long several sectors that make sense for the times. That includes the gold stock sector, especially, although if you reference the recent interview I did with Jordan Roy Byrne, you’ll see that my expectation is for the bull market in the miners may be rudely interrupted as well in the coming months.

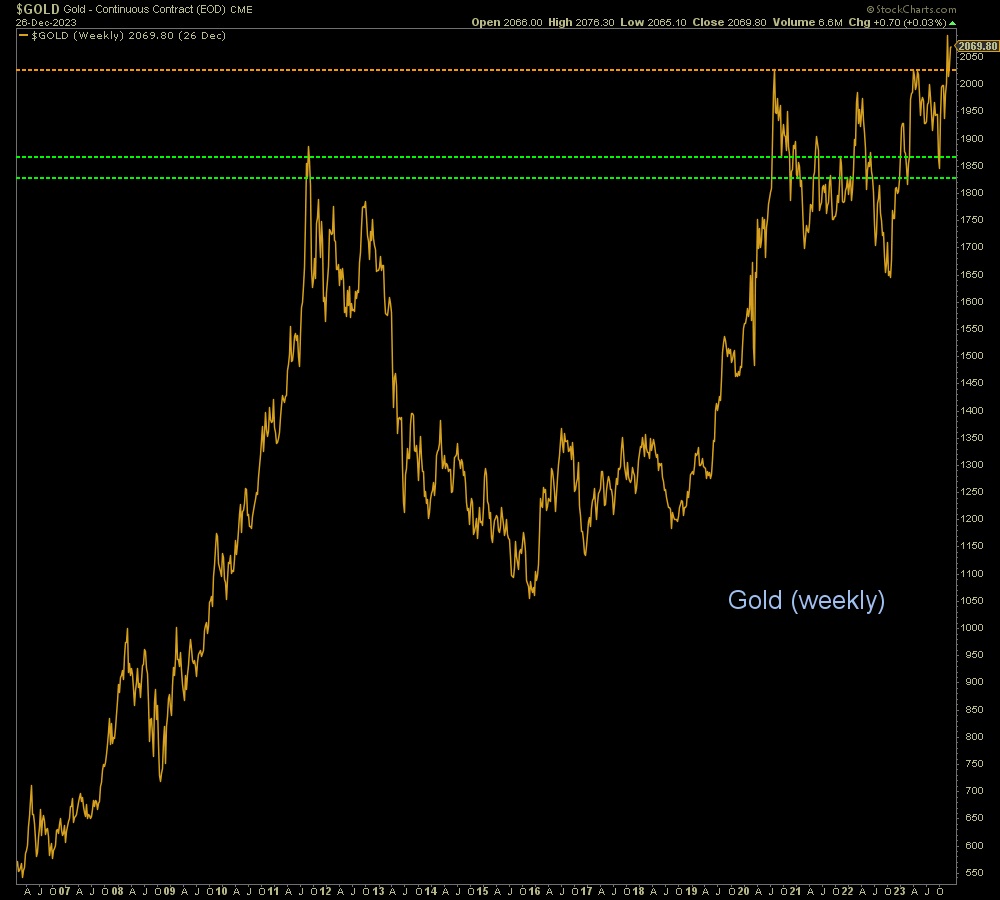

On a related matter, the monetary metal that the miners dig out of the ground is hanging around, while silver (for which we have a nice interim upside operating target) decides whether or not to take short-term leadership. On a related note, when it does come time for asset markets to crack, silver (more cyclical, more inflation sensitive) will very likely nose dive in relation to gold (with more monetary, liquidity and value characteristics).

While the gold price is generally flat lining vs. major stock indexes, although not vs. some broader stock market measures, it is logically out-performing commodities during a disinflationary 2023, and is likely to continue doing so into 2024 as the year starts off amid the Goldilocks/disinflation/”soft landing” happiness that is less friendly to cyclical, inflation sensitive assets like commodities.

We have been anticipating a seasonal bounce in many commodity/resources related equities, however, and that view appears to be on track (have a look at Canada’s TSX-V and its speculative resource stocks, for which we have an upside target that the index is currently steaming toward).

Nominally, gold simply lurks at all-time highs and awaits the rest of the macro to sort itself out. For an asset that is usually trumpeted far and wide in perma-bullish fashion, it sure does seem like it is doing so in relatively quiet fashion as even many of its most ardent supporters are either jumping the Bitcoin train or trained to expect the worst of the the Anti-Bubble, AKA gold.

Gold is a mirror reflection of the speculative assets that it is a counterweight to. It’s relative performance will be dictated by risk in ‘risk on’ markets, when that risk is realized.

As a final note, economic soft-landers are cheering and extrapolating today’s holiday cheer well into, if not through 2025. But the 10yr-2yr yield curve is still inverted, and Goldilocks lives during a curve flattening and inversion. It’s the coming de-inversion and steepener that brings the changes; unpleasant ones, either deflationary, inflationary or a combination of both.

There are different options and time frames for 2024’s market, but it is not likely to be friendly to those “experts” polled in the CNBC article linked above now trend-following to the “soft landing” economic view. That is and has been a necessary component of our view that will ultimately turn bearish for stocks after a perhaps spectacular upside stock market blow off at most, or a roll over sometime after SPX joins the “ALL-TIME HIGHS!!!” brigade.

Happy New Year.

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. Subscribe by Credit Card or PayPal using a link on the right sidebar (if using a mobile device you may need to scroll down) or see all options and more info. Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter@NFTRHgt.

*********