The Stock Market Is Seriously Overvalued Based On This Benchmark

As Americans place a record amount of bets into a stock market that continues to rise towards the heavens, few realize how much the Dow Jones Index is overvalued. While some metrics suggest that the Dow Jones Index is very expensive, there is another indicator that shows just how much of a bubble the market has become.

If we compare the Dow Jones Index to the price of oil, we can see how much the market has to fall to get back to a more realistic valuation. For example, if the Dow Jones Index were to decline to the same ratio to oil back to its low in early 2009, it would need to lose 14,500 points or 65% of its value.

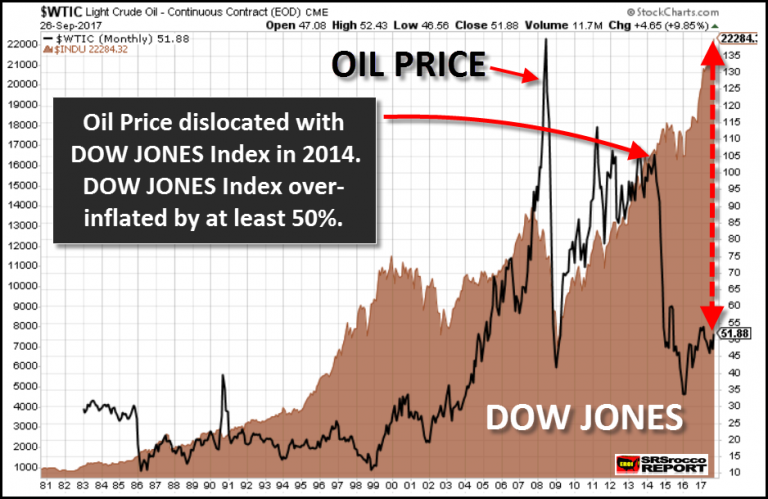

To get an idea just how overvalued the Dow Jones is compared to the price of oil, look at the chart below:

The oil price (BLACK line) increased with the Dow Jones Index (BROWN area) until it peaked and declined in 2008. Even though the oil price line overshot the Dow Jones by a wide margin in 2008, after it corrected and moved higher in 2010, both the Dow Jones and oil price moved up in tandem.

If you look at the movement in the oil price and Dow Jones Index from its low at the end of 2008 to 2013, you will see just how similar the two lines moved up and down together. While the oil price shot up higher than the Dow Jones during the peaks (2010-2013), they paralleled each other quite strongly.

THE BIG DISCONNECT: Dow Jones Index And The Oil Price

However, the BIG disconnect between the Dow Jones and the oil price took place when the price of oil fell from over $100 in the middle of 2014, to a low of $33 at the beginning of 2016. Currently, the Dow Jones Index will buy 430 barrels of oil. However, at the peak of the market in 2007, the Dow Jones Index could only purchase 175 barrels of oil:

We can see that the Dow Jones Index currently can buy nearly 200 more barrels of oil than it did at the peak before the stock market crash and Great Depression in 1929. At the depths of the Great Depression, the Dow Jones Index could only purchase 90 barrels of oil in 1933.

Interestingly, the lowest ratio was reached in 1980, when the Dow Jones Index could only buy a mere 25 barrels of oil. The ultra-low Dow Jones-Oil Ratio in 1980 took place during the huge inflationary period as a result of two Middle East oil price shocks. In 1980, the price of oil reached $36.83 a barrel versus the average 902 points for the Dow Jones Index.

However, after Fed Chairman Volcker raised interest rates to double-digits, the price of oil, gold, and silver plummeted over the next two decades. And by 1999, the Dow Jones-Oil Ratio surged to a high of 534. The high Dow Jones-Oil Rato came as a result of a low $19.34 oil price versus the Dow Jones Index average reaching a new high of 10,339 in 1999.

Now, let’s explore what has occurred more recently. As the price of oil increased from 1999 to 2007, the Dow Jones-Oil ratio declined to 175, even though the market reached a new high of 14,200 points. Furthermore, during the first quarter of 2009 when the stock market collapsed to a low of 6,500, and the oil price fell to $42, the Dow Jones-Oil Ratio only declined to 155… 20 barrels less than at the peak in 2007.

Regardless, the current Dow Jones Index can purchase 430 barrels of oil, which is in serious bubble territory. What is even more interesting is how the Dow Jones-Oil Ratio corresponds to the Shiller PE ratio. The Shiller PE Ratio is the price-earnings ratio of the average inflation-adjusted earnings from the previous ten years of the S&P 500 Index. As we can see in the chart below, the Shiller PE Ratio is currently at 30.68, higher than the peak in 1929 on Black Tuesday before the Great Stock Market Crash:

However, if we compare the Shiller PE Ratio chart to Dow Jones-Oil Ratio chart below, we can see some interesting similarities:

The peaks and valleys in the Shiller PE Ratio chart correspond to the highs and lows in the Dow Jones-Oil Ratio chart. For example, the Shiller PE Ratio reached the first high of 30 in 1929, as the Dow Jones-Oil Ratio was 236, but both indicators fell to a low in the early 1980’s. Lastly, the Shiller PE Ratio in 1999 and today correspond to the peaks in Dow Jones-Oil Ratio as well.

What does this mean? It means that the earnings of the S&P 500 and the Dow Jones Industrials are based upon the price of oil. That being said, the situation today in the oil industry is much different than it was in 1999. Again, the reason for the very high 534 Dow Jones-Oil Ratio in 1999 was due to a very high Dow Jones Index and low oil price. However, the oil industry in 1999 could make money on a weak oil price of $19, whereas today, they are losing money at a price that is more than double.

FINANCIAL TROUBLE BREWING: ExxonMobil’s Financial Situation Deteriorates

I decided to look at the U.S. largest and most profitable oil company, ExxonMobil, to see how the company’s financials in 1999 compared to 2016. The table below provides evidence that the current oil price is causing financial distress on ExxonMobil’s balance sheet:

With the price of oil at $19.34 in 1999, ExxonMobil was still able to enjoy positive $1.84 billion in U.S. upstream earnings versus a loss of $4.15 billion in 2016, based on a $43.29 oil price. Upstream earnings represent the profits ExxonMobil made from its U.S. oil and gas fields. So, even with an oil price of $19, less than half of what it was last year, ExxonMobil still made profitable earnings in 1999 on its U.S. oil and gas fields.

Now, if we consider other financial items, ExxonMobil’s current situation is in much worse shape today than it was in 1999. For instance, ExxonMobil made a larger net income of $7.9 billion in 1999 on total revenues of $185 billion versus $7.8 billion on higher sales of $226 billion in 2016. Furthermore, ExxonMobil’s long-term debt has surged over the past few years to $29 billion versus $8.4 billion in 1999:

Moreover, if we consider the staggering amount of capital expenditures ExxonMobil has invested since 1999, overall liquid oil production is actually lower:

In 1999, ExxonMobil spent $10.9 billion on capital expenses and produced 2.52 million barrels of oil per day (mbd) versus $16.1 billion in 2016 with 2.36 mbd of liquid production. Just think about that for a minute. ExxonMobil spent a staggering $190 billion on capital expenditures from 2009 to 2016, while production declined:

ExxonMobil Total Liquids Production 2009 = 2.39 mbd

ExxonMobil Total Liquids Production 2016 = 2.36 mbd

As the price of oil fell from over $100 a barrel in 2014 to $43 in 2016, ExxonMobil slashed its capital expenditures in half from $33 billion to $16 billion. By severely cutting its capital expenditures, future oil production at ExxonMobil has only one way to go… and that’s down.

Now, what I have shown here is a deteriorating financial situation at the largest and most profitable oil company in the United States. ExxonMobil is the biggest and is supposed, the best of the best. So, can you imagine what is taking place in the marginal U.S. shale oil companies? Yes, it’s a fricken disaster.

Of course, I continue to receive correspondence from individuals who tell me otherwise. For some strange reason, brilliant people are unable to CONNECT THE DOTS. The world is full of very bright, but exceedingly stupid people. I hate to be so harsh… but there you have it.

I used to believe that if the facts were presented, then these supposedly brilliant people would alter their incorrect assumptions on the U.S. Shale Oil Industry. While my followers, who are open-minded, have updated their opinions on the U.S. Shale Oil Ponzi Scheme, many continue to waste time regurgitating worthless information.

GOD HATH A SENSE OF HUMOR…..

In conclusion, the Dow Jones Index is currently overvalued by orders of magnitude we have never seen before. The only thing propping up the stock market and the economy is the Fed and Central Bank money printing and asset purchases. Moreover, there are Trillions of Dollars in currency swaps that aren’t even included that make a bad situation even worse.

For the precious metals investors who are disillusioned by a stock market that continues to rise towards the heavens while the gold and silver prices remain in the doldrums, you have my sympathies. However, fundamentals and the truth always win out in the end. Although, it has been quite difficult to follow an investment strategy based on ethics and integrity… it seems that many people today believe it is okay to sell one’s soul or integrity to make a buck.

SO BE IT….

COURTESY OF SRSrocco Report.

Independent researcher Steve St. Angelo (SRSrocco) started to invest in precious metals in 2002. Later on in 2008, he began researching areas of the gold and silver market that, curiously, the majority of the precious metal analyst community have left unexplored. These areas include how energy and the falling EROI – Energy Returned On Invested – stand to impact the mining industry, precious metals, paper assets, and the overall economy. He has written scholarly articles in some of the top precious metals and financial websites. Visit his website SRSrocco Report.