Stocks and Bonds are Going Up, at Least for Now.

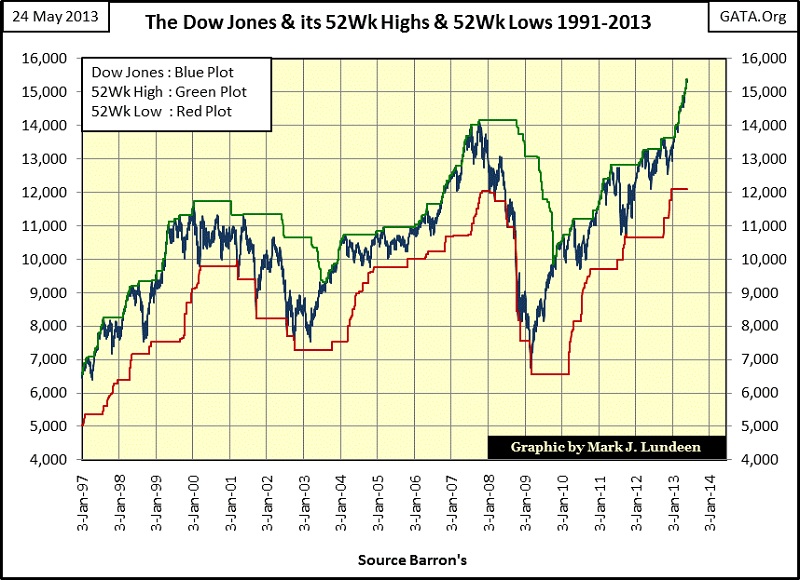

I like looking for market extremes, as they usually occur prior to a major change in the market’s price trend. One market extreme to follow is the number of 52Wk highs or lows an index is making, as we can see in the chart below where the Dow Jones plot is bound by its 52Wk extremes. The Dow Jones (Blue Plot) with its 52 Wk highs (Green plot) and 52Wk lows (Red Plot) make for an interesting view of the stock market from 1997 to today.

Currently, the Dow Jones is seeing an extreme number of 52Wk highs. This can’t last forever; it didn’t in 2000 or 2007, but those market tops happened a long time before the investing public heard of Quantitative Easings. Looking at the three market tops in this data (2000, 2007 and now 2013), the Dow Jones saw prolonged periods of new 52Wk highs creation, but if you take a moment and compare the tops in 2000 and 2007 with what is happening today, there is a difference. Since early January (five months now) the Dow Jones has been making frequent new 52Wk highs; sometimes two or three a week on this big move up, though usually the new 52Wk highs are not coming that fast and furious. But look at the chart; this is a hot stock market!

Should today’s mania follow the same pattern of past market tops, we’ll see a period where the Dow Jones will continue making new 52Wk highs, but these new highs will be less frequent, spaced out by weeks or a month, with a visible pullback in the Dow Jones between them. In other words, the bulls will begin to tire as the next big decline approaches. But for the past five months, the bulls have shown no signs of needing a rest, so their yet unknown last all-time high is still a ways off in time should this model hold. Still I’m reluctant to say that the stock market is in a bull market. Bull markets have broad public participation, as seen in growing trading volume. Trading volume for this market stinks, which suggests that most of the demand for the shares traded at the NYSE is coming from the Federal Reserve system.

The 2000-02 and 2007-09 bear markets are interesting too. The 2000-02 bear market had the Dow Jones walk down its 52Wk low plot (Red Plot) in a series of steps. Not so with the 2007-09 bear market, which in May 2008 (seven months after the 2007 Dow Jones’ top) began a total collapse in market value that didn’t bottom until March 2009. The reason the Dow Jones bottomed in March 2009 is for the same reason it has gone up ever since; Doctor Bernanke thinks it should, and he has control over the engine of inflation needed to make bull markets happen. But Doc B is playing a mug’s game, because he can’t keep the stock and bond markets up forever. Not with Europe’s banks in a total mess; banks who have massive counterparty risks for the Federal Reserve System. Japan and China also contain massive risks for the Federal Reserve System that will someday make the current amazing levitation in the American markets impossible. I don’t know when this will happen, but before it does, we should see the number of new 52Wk highs become less frequent, just as it has happened in 2000 and 2007.

Moving on to gold, it’s evident that my step-sum’s strong buy signal of a few weeks ago fell flat on its back, with the sharp decline in both gold’s price and step sum trends. That is the bad news. The good news is that the lows of last month are still holding even as in the past 15 trading days, gold has seen twelve down days and a 5.63% decline. I’d expect to see that many down days to have taken more than just 5.63% in the price of gold, but they didn’t!

What I would like to see from here are more down days than up, taking the gold step sum below its current range that began in August 2011. Currently gold’s step sum is at 267. I’d like to see it go below 260, maybe even with gold’s price trend reversing to the upside. It happens. But I know that should the global central bank guild decide that the price of gold needs to go down, it will go down as long as the paper gold futures markets are intact. But the days of having the price of gold being fixed by paper future contracts in New York or London are numbered.

Silver’s step sum chart is a story of defeat and despair, for the longs anyways, and that has been the case now for now over two years. Still it’s remarkable that silver’s step sum (market sentiment) has stayed up as well as it has. It wouldn’t hurt to see silver’s step sum decline below 450.

Well, silver is in a bull market, and we are looking at a bull market correction in the chart above that is closer to its end than to its beginning. Geeze Louise, government mints in the US, Canada and elsewhere can’t keep up with the demand for gold and silver coins, and annoying shortages in supply don’t happen in bear markets. If you can purchase your metal at a price that is close to what the COMEX paper market claims gold and silver are at, I expect you’ll have something to brag about in a few years.

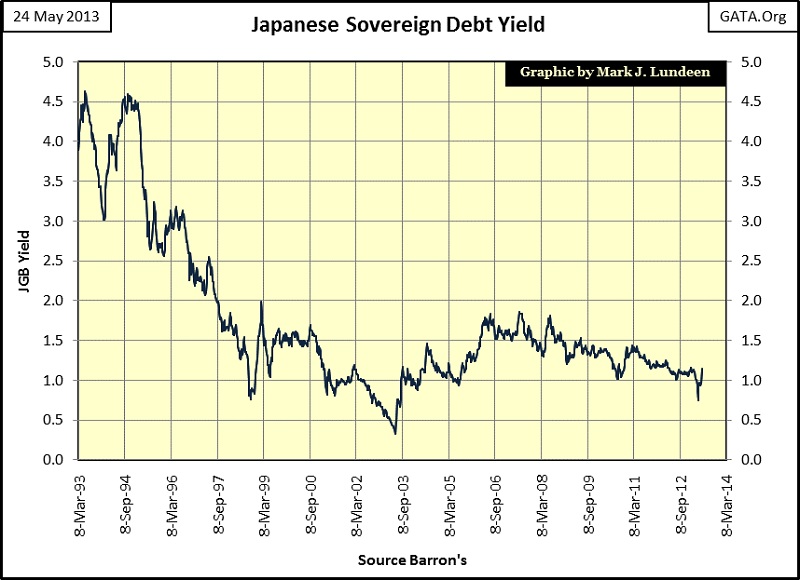

There are some interesting developments in the bond market everyone should be aware of; one of them is what is happening with the Japanese Government bond yield. Japan has been struggling since its real estate and stock market bubbles popped in 1989. That was a quarter of a century ago. A quarter of a century after WW2, Japan went from being a bombed out target in the most destructive war in history in 1945, to a global competitor in steel, ship building, automobile manufacturing and electronics. Much can happen in a quarter of a century. But then nothing has to happen in a quarter of a century; as has been the case where modern finance has refused to allow Japanese banks to fail when they were instrumental in creating massive bubbles during the 1980s.

Little remembered today, but the Japanese banking system during the 1980s was probably the most powerful financial center in the world, with its reserves backed by the “wealth” created by its real estate and stock market bubbles. The crash of October 1987 was a global event, but Japan at the time was largely unaffected by it. Japan’s “samurai economy” seemed destined to go on forever, or so the “experts” assumed, until its banking system’s reserves became illiquid after 1989 when the bubbles they inflated went bust. Like the American banking system since the credit crisis, Japan’s banks have been wards of the state ever since, and for the same reason – the banks were needed by an entrenched political class to fund their election campaigns.

Instead of allowing bankruptcy and liquidation to clean the huge burdens of unserviceable debts from the economy in the course of a few years, the Japanese taxpayer was drafted into decades long service to save the banking system. To make this work, the Japanese government began a program of debt expansion by its treasury as the Bank of Japan began to monetize its government’s bonds. The increases in debt and money were used for public works programs and other make-work programs that never solved the problem of their economic malaise.

We can see the result of this program in the chart below, collapsing bond yields for Japanese government bonds that did little to restore prosperity to the Japanese consumer, but did keep the banks in business that the Japanese government should have allowed to go bankrupt a quarter of a century ago.

This is the same rescue program selected by America’s “policy makers”, who must by now know that what didn’t work for Japan won’t work for America either. Still they do it, because everyone knows that in any financial crisis, “we have to save the banks at any cost.” This corrupt practice of attempting to inflate the banking system back to health also provides ample opportunity for insiders to make vast fortunes. That the people who mismanaged the banking system are allowed to take home a billion dollars for destroying the economy seems not to bother too many people, but it does me.

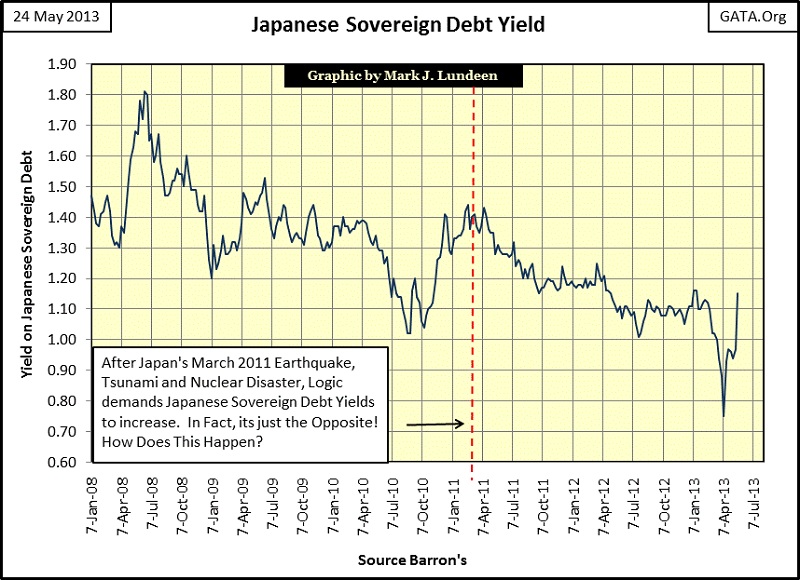

Here is a shorter term chart for the JGB yield. Bond yields today have little to do with pricing debt risks. Changing bond yields today should be understood more as “policy statements” by central bankers than market realities. This was evident in the aftermath of Japan’s March 2011 triple disaster of a massive earthquake, tsunami and nuclear-power plant meltdown. One would have expected the yield for the JGB to increase after March 2011, and one would have been wrong. But then something strange happened beginning in early 2013; JGB bond yields saw a spike soon after the Bank of Japan announced that they were going to greatly increase their currency in circulation in the next few years. This wasn’t supposed to happen, but then 70 trillion new yen in circulation may have been one QE too many for current holders of Japanese sovereign debt. They want no part of this, and so they are selling their bonds. Someday, this will happen in the US Treasury bond market too, as the public will only take so much when it comes to monetary inflation.

This increase in yield is receiving some attention in the financial media as it should. After all, the Bank of Japan has inflated a bubble in its government’s bond market, and with time all credit-created bubbles go bust because there are limits to how much debt any society can carry. In fact Japan may have reached its debt saturation point. Zero Hedge is reporting that the JGB futures market on several recent occasions have halted trading as sellers have overwhelmed buyers. The results can be seen in the chart above after 07 April 2013. This increase in JGB yield may be the start of a general global credit collapse, however studying the charts above we see even larger increases in yields occurring many times since 1993 without resulting in a crisis. But one of these days it may as the global financial system is now bound together by fraudulent derivatives. A 4.5% yield in the JGB, last seen in 1994, may bring down the global financial system.

It’s not just the Japanese bond market that is showing signs of stress, money managers for American Universities have recently placed some distance between their endowment funds and the US Treasury bond market. That includes Princeton University, the home of Doctor Bernanke and Paul Krugman.

"According to the Financial Times, many university endowments have scaled back their holdings of Treasury securities from as much as 30 per cent in 2008-09 to zero in some cases, say people familiar with their investment strategies."

The article went on to quote an unnamed university fund manager as saying, "Treasuries were a core holding. Now everyone is holding less than 5 per cent." That same manager added, "Today government bonds should come with a warning about interest rate risk."

- Jim Woods of Profitable Trading

What, a trust fund manager from a prestigious university seems to be unaware that Doctor Bernanke’s stated policy is to guarantee that US T-Bond yields have no interest rate risk? Do these universities’ trust-fund managers know something most people don’t? I believe it’s safe to say that when Doctor Bernanke or Paul Krugman come home to Princeton University, their homies are not awed by their wisdom and economic insight as are members of the media. Clearly they are putting some distance between Bernanke and Krugman’s economic wisdom, and the investments in their trust funds.

I wonder if the alumni and former faculty from these same universities that now manage US “fiscal and monetary policy” see the irony of their alma maters distancing their trust funds from the consequences of their “public service?” Most likely they don’t, and these universities most likely fail to see the connection of their need to exit the US Treasury bond market with the economic quackery they’ve promoted for decades – but I do!

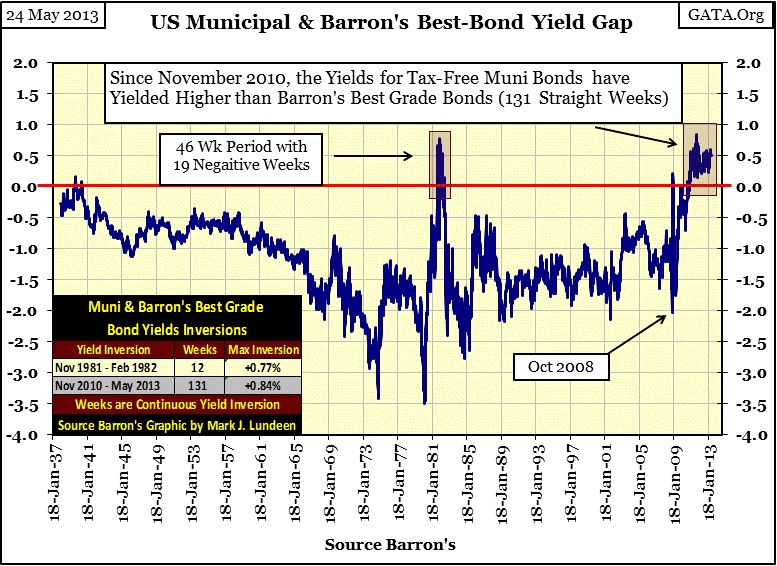

But it isn’t just Uncle Sam and Japan that are seeing confidence in their bonds being questioned in the markets. State and local government tax free municipal bonds have seen their yields increase above those of Barron’s Best Grade Corporate Bonds. This has happened before, as we see in the chart below. But since 1937, a yield inversion between high grade corporate and muni bonds has never before lasted for two and a half continuous years.

What is the problem? Bankers, economists and politicians have had their way with local government finances for decades. Here’s a USA Today link for 10 cities in California that are at risk of defaulting on their bonds, but this problem in local government solvency is a growing national problem, and will only get bigger when the coming crisis in the US Treasury market arrives, raising all dollar bond yields to levels that are unthinkable today.

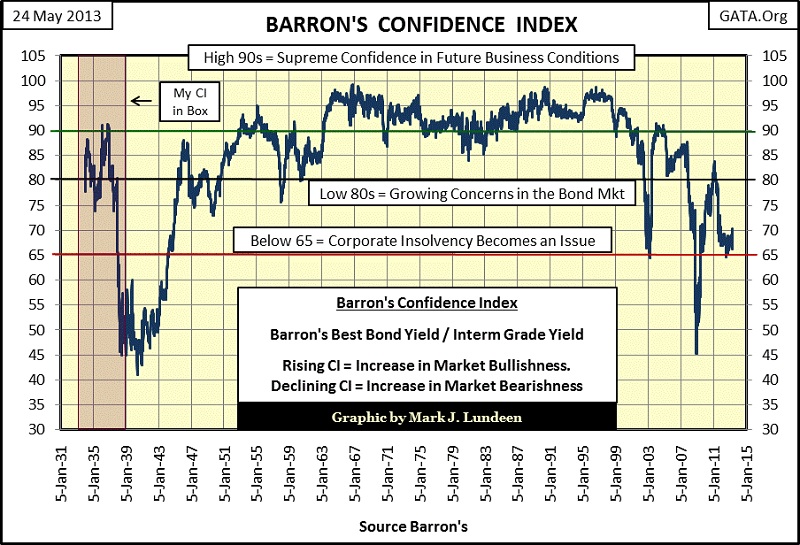

There are problems in the corporate bond market too, if we can believe Barron’s Confidence Index (CI), which I do. The CI is not a bond market timing indicator. From the early 1940s to 1980, the CI went from 40 to 90 as yields for high-grade corporate bond increased from below 3% up to over 14%. So, this means that the CI actually improved during a prolonged bear market in bonds. Then since 1999, the CI has badly deteriorated as yields for high grade corporate bonds fell from over 7.5% to 3.5% in a strong bull market. However, Barron’s CI is not a bond market indicator, but an economic indicator that measures the financial strength of corporate America with less than stellar grade credit. The CI is * NOT * looking at junk grade debt, but intermediary grade investment bonds issued by companies that have no problems servicing their bonds during good business conditions, but may have should the economy enter into a prolonged time of trouble.

With that in mind, the eighty-year plot for CI below makes total sense . I don’t have this data during the 1929-32 crash, but the CI must have cratered as the credit structure collapsed, resulting in a nationwide bank holiday in March 1933. But using what I have, we see the tail-end of the 1932-37 economic rebound where the CI increased to above 90. As the 1930s depression resumed (1937-41), the bond market had growing concerns for the indebted companies who had issued intermediary grade bonds. From 1941 to 1963, bonds may have been in a bear market that wouldn’t end until October 1981, but the bond market itself was losing its fear of default from intermediary grade corporate bonds, a fear that wouldn’t return until after the 2000 high-tech market crash, and continues to this day.

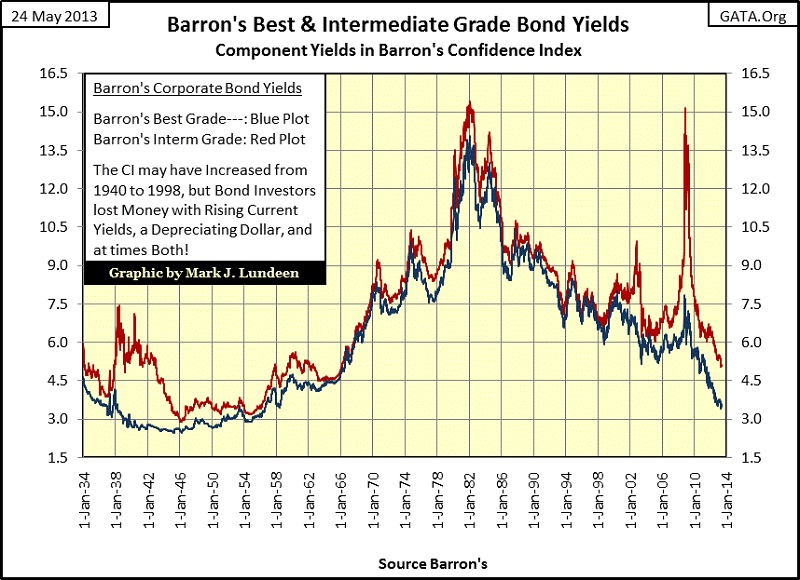

Currently retired people who have saved money during their working years for income cannot find a low risk rate of return that pays the bills. At 0.25%, a million dollars in a bank’s 12 month CD only returns $2500 a year. Being a millionaire in 2013 isn’t what it used to be. This is due to Doctor Bernanke’s low interest rate policy which he claims will save the banks (and the corrupt world we now live in.) This has forced people seeking income to reach for yield by purchasing lower quality bonds, such as Barron’s intermediate Grade Bond index below (Red Plot). Note; these are not junk bonds, but during the 2008 credit crisis their owners suffered junk grade losses of their principal.

I don’t understand why anyone today is messing around with stocks and bonds. They are only going up because a former professor of economics from Princeton, who now controls the Federal Reserve’s “monetary policy” believes that declining financial asset valuation is THE problem, and is creating the inflationary demand needed to make the prices of stocks and bonds go up. Ultimately, the Federal Reserve will be no more successful than has been the Bank of Japan in “stimulating” their economy weighed down by toxic assets in the aftermath of an economic bubble their central bank created decades ago.

What is actually needed is for banks, insurance companies and pension funds to mark-to-market their reserves in a market free from Central Bank “liquidity.” This action would place most of these institutions in receivership, as currently a good portion of their reserves have no active market except when the Federal Reserve purchases them via a QE operation. But the problem is not the market, but the financial system that created these worthless “assets” and sold them in the public market place for decades to a trusting public. So Doctor Bernanke’s QE isn’t the solution to our current problem, but actually a continuation of the problem itself. The refusal to allow dubious assets to find a true market price, and forcing financial institutions to take the loss when a price can’t be found is only postponing the final day of reckoning. But that is the current plan of the day, at least for now.

Mark J. Lundeen

More from Gold-Eagle