Storm Warning?

Indications are that the Battle of the Bulge is over. Market trends are returning to normal…and the rear guard action has failed to extend or even to hold. This week the focus turns to what every reader surely has seen announced and discussed – the on the spur meeting of the FOMC Monday morning; ostensibly to discuss rates, for the benefit of those who still believe in fairies. Will the meeting raise rates? Not even a small chance! Will they cut rates back to zero? And, by doing so, to trigger a massive panic because it would mean the Fed sees a collapse in the economy that has to be ‘fixed’ urgently, before the next scheduled meeting just three weeks later? No – it does not make sense. Leave the rate unchanged after a call for a panic meeting? Even the Fed is not that silly.

If Yellen wanted to call the hawkish governors to tow the party line, she would have done that with a phone call or even an email. So that leaves only one alternative – there is a major global financial crisis erupting somewhere unless the Fed is really being silly and there is some other reason of little consequence for the markets. It seems that the likely source of such a crisis is Deutsche Bank with its $78 trillion of derivatives, as the black sheep amongst other banks in their many shades of grey. Or, hopefully, perhaps something similar, but of lesser magnitude.

It is well-known there are large derivatives positions that have the Japanese yen as a leg; presumably, arbitrage that is either long yen and short something else, or with a short position in the yen against another long. Since the end of January, the yen has firmed by 10.7% against the dollar – and a 1% move in quite a short time is a Big One in the major currencies! A 10% move against a large derivative position is more than likely to sink even one of the global megabanks – if it were to be caught on the wrong side by such a move, then either reacted too slow or found that there is no willing counter-party with whom to offset the losing position.

The odds thus favour that if a large player in the derivatives market, be it a bank or a hedge fund, suddenly finds itself in deep enough trouble to trigger an emergency FOMC meeting, then the cause of the problem lies with the Japanese yen. Note that since the euro, by comparison, is steady against the dollar, it is not a weakness in the dollar that is the problem; the decline in the dollar index is mostly due to the yen.

Whatever the reason for the meeting, later on Monday we should know whether the above speculation was close to the truth or not. Should there be a derivatives meltdown, perhaps with the yen as factor, please let it be some smaller institution than Deutsche Bank – something where the fallout can be contained.

With gold clawing its way back above $1,240/oz and the DJIA showing signs that it is close to topping out, it seems as if the rear guard action against some trends that are fuelled by fundamentals, is starting to retreat again. While this is good news for gold bulls, it is not such good news for retirees who, desperate to obtain some form of return on their nest egg, have invested on Wall Street.

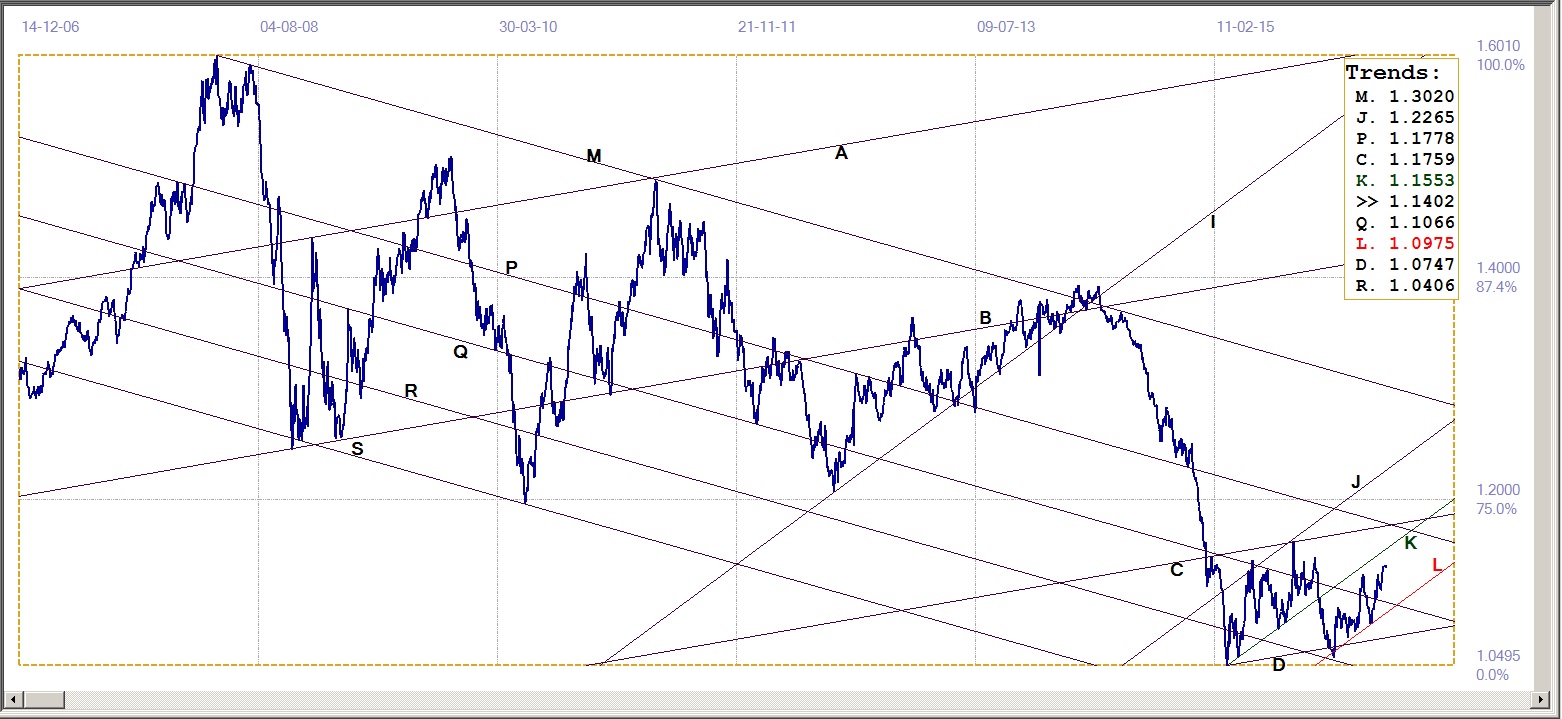

Euro-Dollar

Euro-dollar, last = $1.1402 (www.investing.com)

The euro’s steep recovery off key support at the bottom of channel KL ($1.0975) has restarted the failed bullish trend in channel JK ($1.1553) within the lower part of channel JKL. The second break above resistance of line Q ($1.1066) is holding sideways at the new intermediate high.

The new rising trend has to break clear above line K to be confirmed and then has new resistance at lines C($1.1759) and P ($1.1778) with which to contend. There is, however, ample room to move sideways below lines K and P ($1.1778) before the support at the bottom of channel KL would come into play.

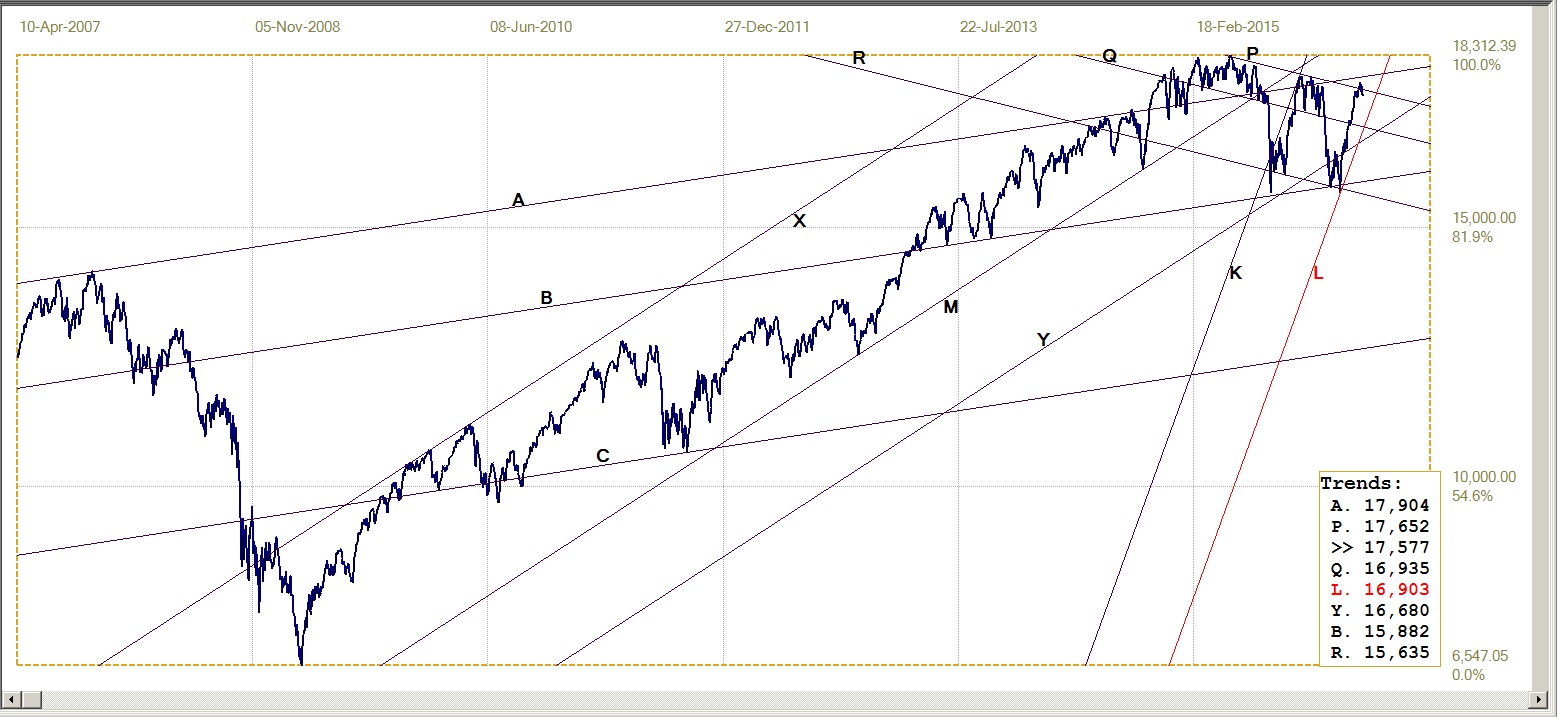

Dow Jones Industrial Average (DJIA)

The steep and remarkable levitation on Wall Street, following a reversal off 15660 at the support at line L, broke above resistance at line P (17652), top of the current bear channel. The break higher was bullish, but the DJIA then did not challenge the resistance at line A (17904). Instead, it reversed trend to break back below line P to return to the bear channel. Holding the break lower would confirm that the DJIA is no longer a participant in the Battle of the Bulge and it has given up on the race for 18 000. The FOMC meeting Monday morning is likely to determine what happens.

Dow Jones Industrial Index, last = 17577 (money.cnn.com)

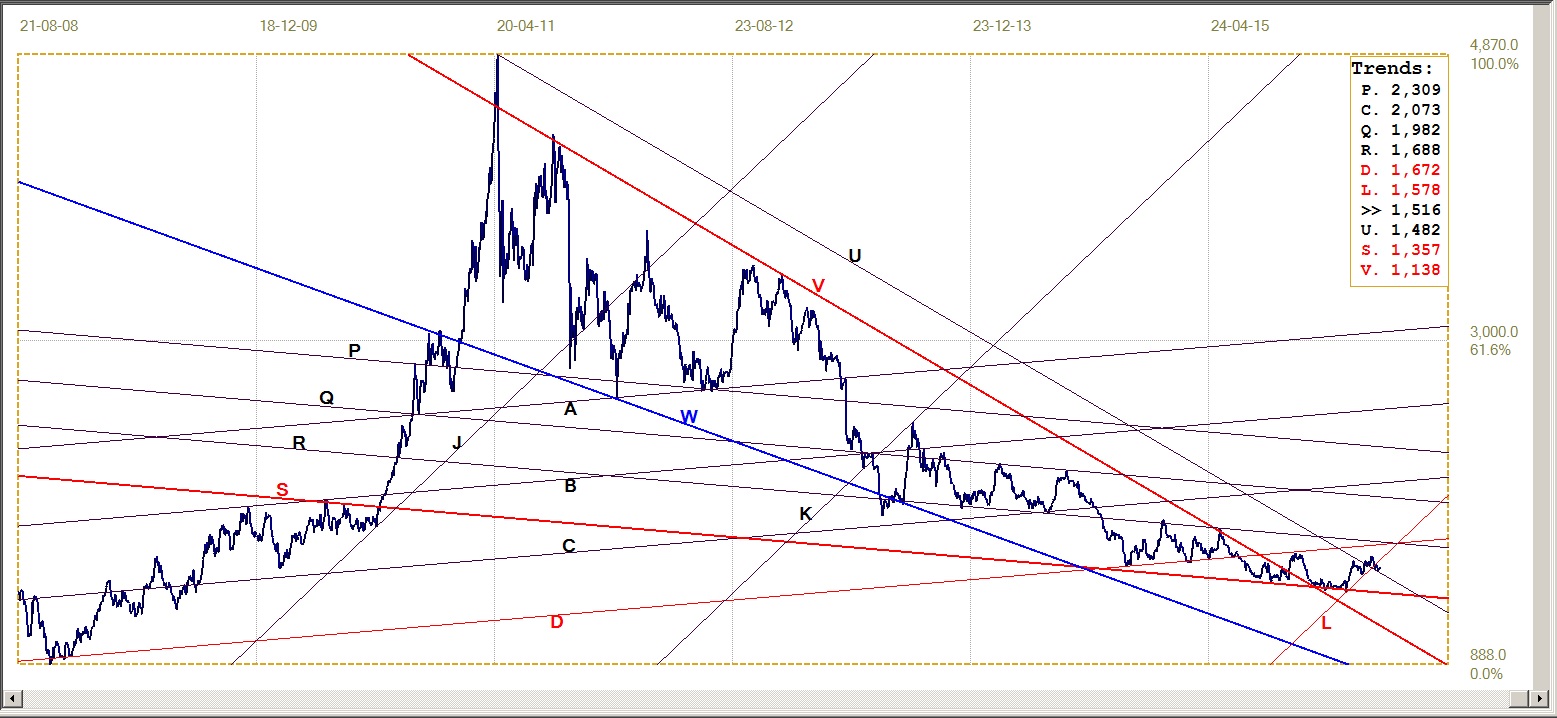

Gold PM fix - Dollars

Gold has been under severe pressure since before the April options expiration and the first notice day for delivery. It is thought that the price of gold had to be kept low to prevent owners of open April contracts to take actual delivery rather than to take a cash settlement – perhaps with a small premium to make this attractive and thus protect the limited gold supply in the Comex vaults.

Doing so by sustained selling has that advantage, but on the other hand, it means that the short open interest accumulates to present a larger problem later in the futures contract cycle. Without knowledge of how critical the situation has become in terms of the time factor, there is now way of knowing how the trade-off between a continued low price for gold – and perhaps more importantly, also that of silver – and a much greater problem with open interest at a later time will play out.

After recently failing to hold the break above resistance at line C ($1274), the price of gold fell back to find support along the bottom of channel KL($1230). Last week, a few PM fixes broke marginally below that support, but by Thursday, the gold price had moved back above $1240 to build a bit of a cushion above the rising support. If channel KL can hold this week, the outlook for the metal will be much improved.

Gold price – London PM fix, last = $1239.50 (www.kitco.com)

Gold PM fix - Euro

Euro gold price – PM fix in Euro, last = €1087.6 (www.kitco.com)

Despite continued dollar weakness as measured by the yen-influenced dollar index, the euro last week remained quite steady against the US currency. Initially, a weak gold price had the euro price of the metal under pressure, sufficiently so to cause a break below the support of bull channel KL (€1095). A recovery in the price of gold to around $1240 was not enough to bring the euro price back into the bull channel, but at least, it closed the gap between the desired support level and the euro price.

With a generally weak US dollar, further recovery, back into the bull channel, would have to rely on further improvement in the dollar price of gold. It is not anticipated that the euro would sink lower against an already weak dollar unless circumstances in Europe change substantially; for example if the speculation about Deutsche Bank turns out to be correct. An interesting week ahead, it seems.

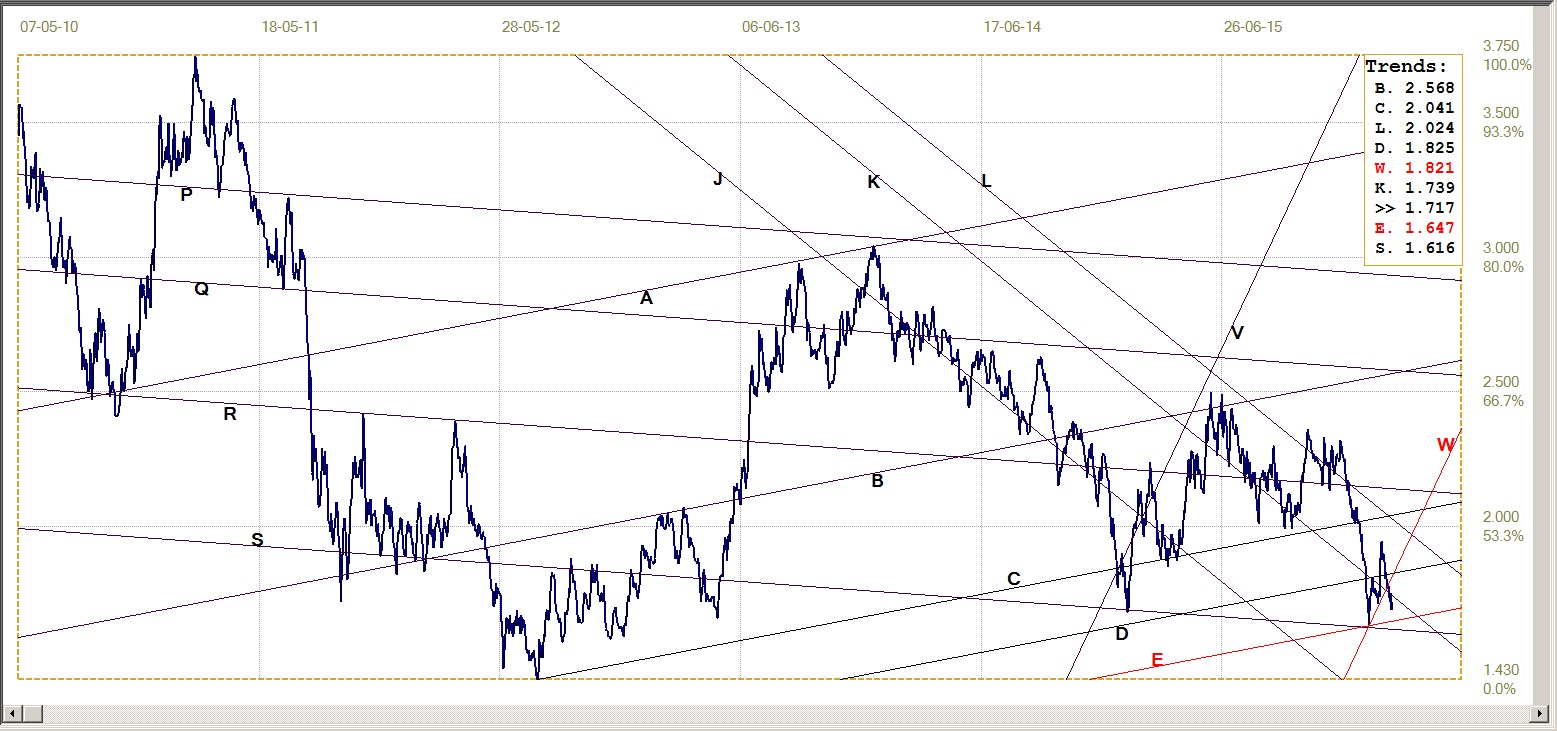

Silver Daily Fix Chart

Silver remains the poster child for massive intervention in the PM markets. While gold started a recovery last week that held the price in the steep bull channel, the price of silver has now broken below its own bull channel, KL ($15.78). The low fix last week, at $14.96 on Monday, was right on the support of line U, $14.95 at the time and now at $14.82. At least, silver has improved since Monday to move back above the $15.0 level, but any increase is met with strong action to take the price lower. A recovery back into channel KL this week, if that should be possible, will be very good news.

Silver daily fix, last = $15.16 (www.kitco.com)

US 10-year Treasury Note

A fresh rally in the bond market had carried the yield of the US 10-year Treasury note lower to a close ten days ago that was just below bear channel VW (1.821%). The rally continued last week, to extend the initial marginal break lower to end the week at 1.717%, after breaking below the 1.70% level on Thursday, but failing to hold the break.

Monday’s FOMC meeting is expected to have some effect on the yield, even should, as seems very unlikely, the meeting really be scheduled to talk about Federal rates, as the announcement has it. Should speculation that there is an imminent crisis in the financial markets be correct, it is difficult to anticipate its overall effect on the US bond market in particular, but also in the other markets. If the current firmer trend is to continue, there is market resistance ahead at line E (1.65%) that is then likely to come into play. Nearby market support is at line K (1.74%), with lines W (1.82%) and D (1.83%) as backup.

US 10-year Treasury note, last = 1.717% (www.investing.com)

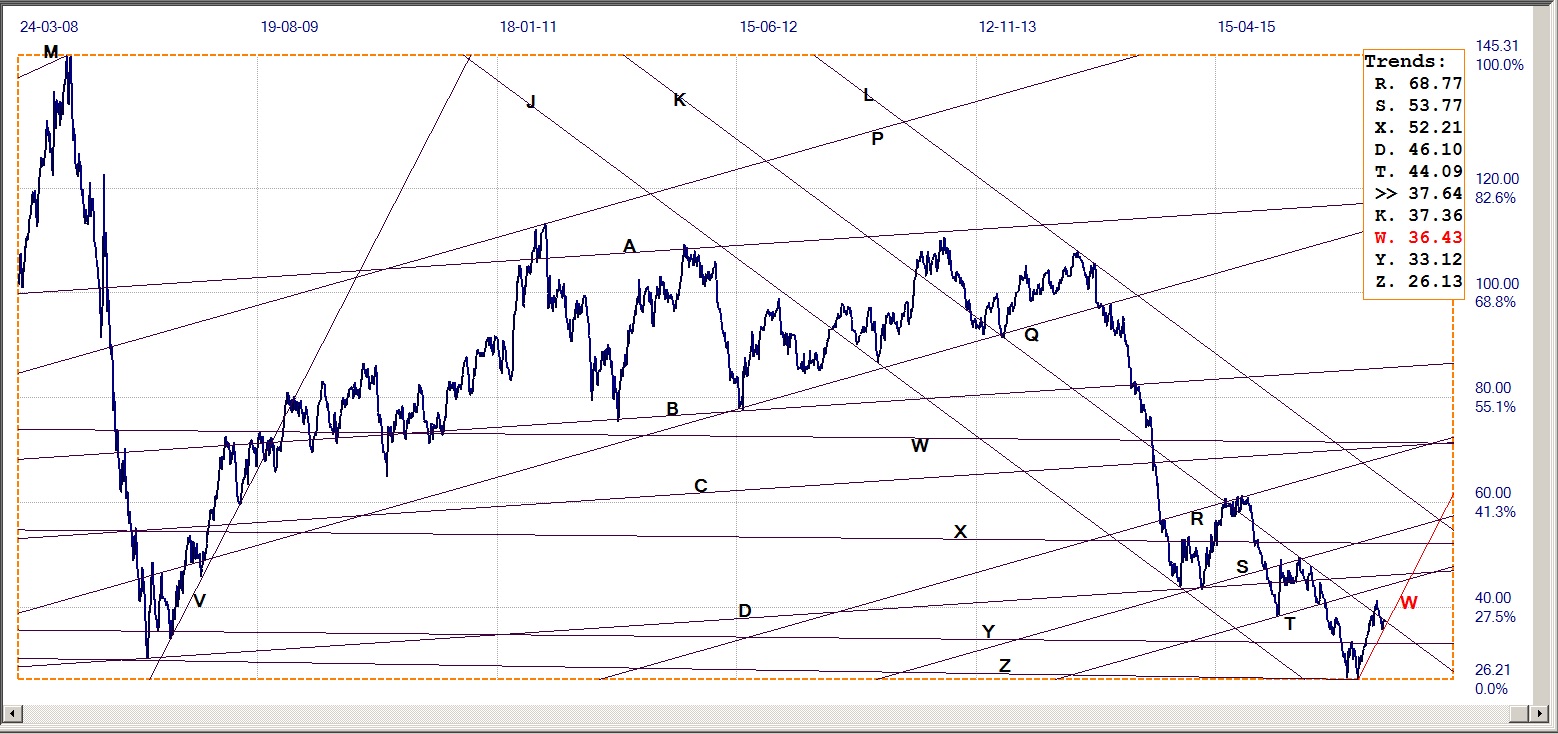

West Texas Intermediate Crude. Daily close

After breaking, below line K ($37.36), the WTI price of crude is now holding along support of the bottom of bull channel VW ($36.43), trying to break back above line K. The price has started to move higher on a report of declining reserves in storage at Cushing, which of course has immediate impact on the US market. However, the news from OPEC and others is that production is still high and expected to increase further as Iran tries to recapture market share by lowering prices. This week crude has to either break above resistance at line K, to confirm a rising trend, or to break below channel VW. The latter is not necessarily bearish, as the price could extend sideways rather than move lower.

WTI crude – Daily close, last = $37.64 (Investing.com)

©2016 daan joubert, Rights Reserved

chartsym (at) gmail(dot)com