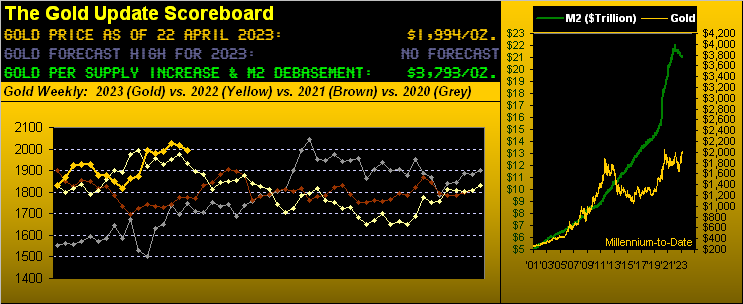

A Time to Add to One’s Gold Stack; (for the S&P, Prepare Hard Hat)

Yes, per last week’s 700th missive, an All-Time High for Gold remains nigh, (i.e. above 2089). Yet en route to said notion of nigh, we also penned our expectation for Gold to first recede into the 1900s, price indeed having traded this past week to as low as 1981 before settling yesterday (Friday) at 1994.

Nonetheless with respect to a new Gold high being nigh, might price still a bit further slide? After all, per The Oxford English Dictionary (circa 1879 as The New English Dictionary) “nigh” is simply defined as “near”. And contextually, “near” is not that far from here. Or numerically, 2089 is not that far from 1994, i.e. +95 points.

‘Course ’tis always about “The When”. In round numbers, let’s say Gold basically from here has to pop up +100 points to eclipse its existing All-Time High. Can that happen quickly? Historically since 2001, there have been 25 mutually-exclusive (for you WestPalmBeachers down there that means “non-overlapping”) occurrences wherein Gold has gained better than +100 points within just five trading days, the most recent case being in just three sessions from 1815 on 09 March to 1920 on 13 March. “You can bank on that.” (Ouch).

But in terms of Gold’s present ranginess, our EWTR (“expected weekly trading range”) is now 63 points; thus solely by that metric, a new All-Time High above 2089 in a week’s time is a bit of a stretch. Moreover, we’ve the following near-term technical concern.

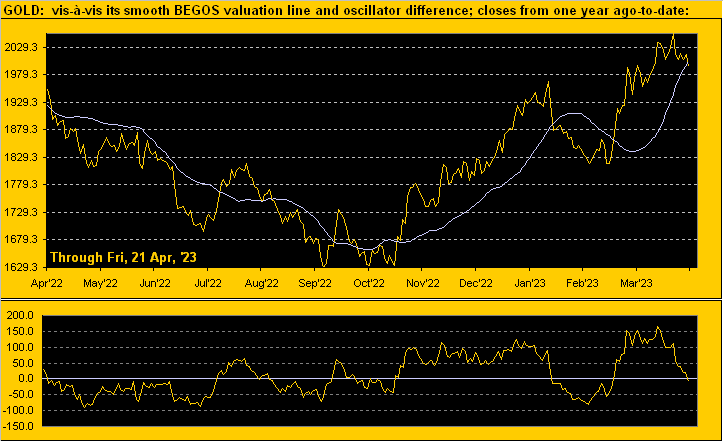

Recall a week ago our “continuing coverage” of Gold having significantly deviated above its smooth BEGOS valuation line. Here they are paired in the upper panel from one year ago-to-date:

The lower panel is the oscillator (price less valuation), at one recent point showing price as better than 150 points too high. Thus as anticipated, price this past week came back to this near-term method of valuation. However, upon price penetrating to close below valuation as just occurred yesterday, the “rule of thumb” is to expect still lower levels. Such negative penetrations have happened six times since a year ago to an average downside deviation of -77 points … which from here at 1994 “suggests” 1917, (just in case you’re scoring at home). But: our sense is — in staying with the theme that a new Gold All-Time High is nigh — we’re not anticipating much material downside. Rather, some of the levels we noted a week ago (such as 1953 and 1975) seem more reasonable, especially given our perception of Gold awareness being on the increase amongst the non-Gold crowd.

Moreover, as we turn to Gold’s weekly bars from one year ago-to-date, the blue-dotted parabolic Long trend continues to ascend such that we continue to seek the new All-Time High along this bend, leading further toward the mid-2100s before reaching an end:

‘Course, there’d be no market for Gold were it not for “The Other Side of the Trade Dept.” represented just yesterday in Barron’s by one “AA” (and you know who you are out there) who penned “Gold is Hitting a Wall” such that the 2050-2075 zone somehow is “formidable resistance”. From our purview, such “resistance” is really the two tops formed first ’round COVID in 2020 and second ’round RUS/UKR in 2022 … and now thrice ’round Common Sense/Fundamental Undervaluation (per our opening Scoreboard level of Gold 3793). Thus we still see a wee dip … but then up with it. ‘Tis a time to add to one’s Gold stack. For as we’ve quipped of late quite a bit: “Triple tops are meant to be broken.”

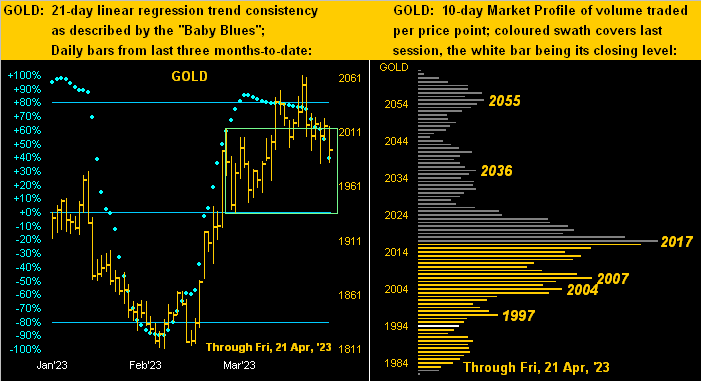

And again, our immediate sense too for the precious metals is a wee bit lower. Yet by our title we imply a chance to buy given the All-Time High being nigh. First to Gold and our two-panel graphic of price’s daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. For the bars we’ve put in an arbitrary green box encompassing a reasonable support area for Gold, even as the declining “Baby Blues” of trend consistency become less so. As for the Profile, what had been notable overhead resistance at 2039 has since shifted lower to the now-dominant 2017 level:

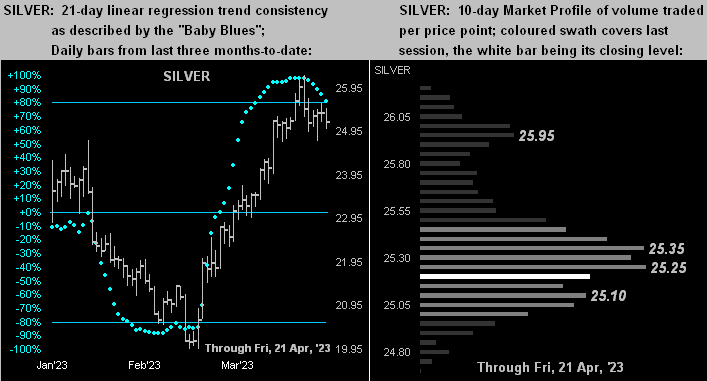

Second with the same graphical drill for Silver, her Baby Blues (below left) are poised to cross below that key +80% axis, suggestive of a price run down into the lower 24s. And in her Profile (below right), those denoted lower 25s now show as trading resistance:

‘Course all that said, we’ve this from the “Who’s Next? Dept.” Upon whichever bank next suddenly zooms to the above-the-fold newspaper position shall swiftly send the precious metals back on the upside track, in turn putting the S&P flat on its back. Not that Gold nor Silver need that to happen: the yellow metal (1994) again by the Scoreboard valuation (3793) is presently priced at but 53% that, whilst the S&P 500 by earnings-to-historical value is arguably more than double that.

We’ll thus wrap it for this week with one of our (again updated) all-time favourite Gold Update graphics toward the next All-Time Gold High being nigh!

Cheers!

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.