Troubling Trends In 2022

During the past two years the world has changed. Events that have changed our lives in a substantial and unexpected manner, permanently in most cases so far, are not so frequent. Within living memory, or at least life span, of people still alive, these events are the invasion of Poland in 1939, the fuel price shock of 1973, September 11 of 2001 and the invasion of Afghanistan, Lehman Brothers as a symbol of prudence overcome by greed and now the Covid-19 virus. Of all these events, the past two years are having(have had?) the greatest and probably most lasting effect on the whole world. 2022 ought to show if there happens to be evidence of the extent of the changes to come and the direction.

If we were to wind back the clock to early 2019 and cast an eye over the state of the world at that time, with a specific focus on the USA, and compare what we see with what we know of the current state of the world around us, there are clearly more than a few significant changes. In a sense, three years ago we still lived mostly in a sense of harmony and innocence. On a national scale, most countries were rather peaceful and international relationships were generally rather good compared to the stresses of the post cold war period and before China became the global factory.

Yes, Trump was taking on China and planning to restart manufacturing in the US to ‘Make America Great Again’, which caught many large US corporations on the wrong foot. If Trump were to penalise corporations which used foreign cheap labour to boost their profits at the expense of the US economy, they would have been compelled to dispose of their facilities in China and build new manufacturing complexes in the US, at great cost. But the tension never got remotely close to becoming a shooting war.

Probably the most glaring change from three years ago is the way Covid has resulted in major divisions among the people of many countries – these developed between sections of the population and against the way governments have changed to become much more dictatorial and in some harshly suppressive. Australia, for example, once a peaceful bulwark of democracy, is now almost as much a police state as the USSR used to be and as China is still being reported in the west.

There can be no doubt that dire projections of the virulence of the new ‘Chinese virus’, based on a panic reaction of Chinese authorities to the outbreak in Wuhan, forecasts from epidemiologists and, perhaps most of all, stoked by the media frenzy, created a global panic not seen recently. China had immediately instituted harsh methods to try and curb the spread of the virus and these methods were implemented by most other governments where the virus was infecting people as if nothing else would do.

During the first year of the pandemic, national economies were throttled down as so many workers were forced into home isolation; only essential activities for survival of the infrastructure and health services were exempt. In most countries, the people had divided reactions to these measures. A large part, fully conditioned by the media, was panic stricken and meekly accepted the pandemic regulations to protect their lives. A second group, generally consisting of fewer members, believed that the threat of the virus was over-blown and that the biggest disaster of the pandemic was the wrecking of the economy.

This first phase set the stage for what was to come in 2021. Governments considered themselves as sanctioned to forget about public opinion and go full steam ahead with what they considered necessary to combat the pandemic – under advisement of the experts in the health services, who received their guidance from Big Pharma. People, also in most countries, found themselves at serious odds with their neighbours and even their relations and within their families. Driven by fear on the one side and by the belief that the threat was limited on the other, neither side listened to the sense.

When vaccines became available, initially in limited quantities and mostly as ‘first come first served,’ governments were easily coerced into signing multi-page contracts that had to be kept secret from even the democratically elected representatives of the people. From what has been leaked, the terms are supremely onerous, hence a need for secrecy. Apparently, governments are i.a. under a mandate to prevent the use of any alternative medication for prevention or treatment of Covid, with severe penalties if they were to fail in this respect or in any of the other terms of the contract.

The Executives of most governments operate with a certain amount of secrecy, even to withhold information from Congress or Parliament as the case might be. Their signing, under duress of the circumstances, of the extremely one-sided vaccine contracts may have had the effect that the real decision makers in governments now saw themselves as ‘above the law’; being given (near) dictatorial powers under the emergency. This is particularly evident in Australia and to some extent also in the Netherlands, Austria and in Germany. There the attitude towards individuals who disobey and resist the mandate to become vaccinated somehow reminds of Hitler’s Germany, Mao Zedong in China and Stalin in the USSR.

With the availability of the vaccines, the initial division between people caught up in fear and those who considered the virus little more than a more severe winter flu intensified. Believers in the ability of the vaccines to protect them from infection, or if infected from severe illness and death, saw the unvaccinated as spreaders of the virus and a risk to their own health. Even with a nominal risk of being very ill or dying, any thought of contracting the virus is anathema and this has to be prevented at all costs. The message from Big Pharma and the media has become so ingrained that news of gatherings of fully vaccinated people who then experienced outbreaks of Covid has not had significant effect on this belief.

At the same time, people who for whatever reasons do not want to accept the vaccines are resisting the mounting pressure from government, the media and their neighbours by becoming increasingly vocal in their demonstrations; mostly well controlled and not violent, but often violently countered by the police and even soldiers on occasion. That the measures to ensure vaccination and to control dissent often are far reaching, as in some Australian states and also elsewhere in Europe, is becoming a reflex action that in time will be institutionalised and more like to spread widely than to taper off.

Whether after Covid or during an extended Covid-like series of variants, the world has changed. The balkanisation of many countries into three main distinct power groups is not going to be easy or quick to bring the different groupings together in a climate of unity again. Governments will get to love the idea of effectively ruling by edict and more than just a show of force, which might have even people who support the official policies maintain a distance from government. The third ‘force’ will continue to foster resistance to any policy they do not believe in or simply refuse to accept, unless they can be convinced that a policy and related action are actually needed; not by media blather or hype, but by hard facts and proper science.

That is, unless the situation deteriorates so much that governments implement the solution, popular in the 1930s, of putting dissenters into camps as the only practical way to maintain peace and order.

The above speculation about the future is not expected to be realised as described; however, it attempts to generate a scenario that is plausible in terms of some of the trends that have developed during the past two years. Should the facts and actions that underlie these still developing trends change soon, the scenario will collapse. But so far the lines between the three groups appear drawn in the sand. The rest of 2022 should be more interesting while this remains so.

Here is a link to the history and timeline of the Covid-19 virus since the early 2000s. It makes for interesting reading not widely available in the popular media, if at all.

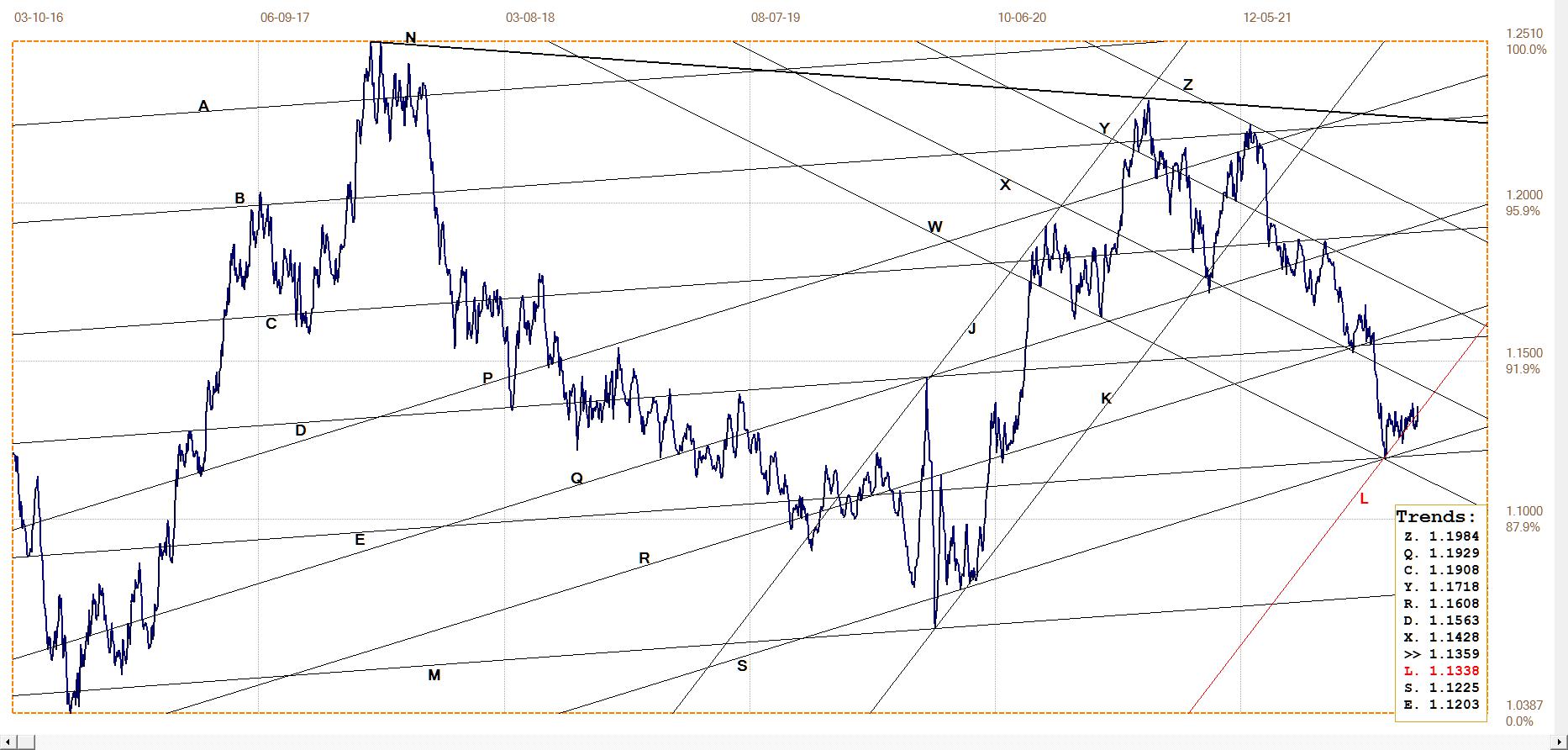

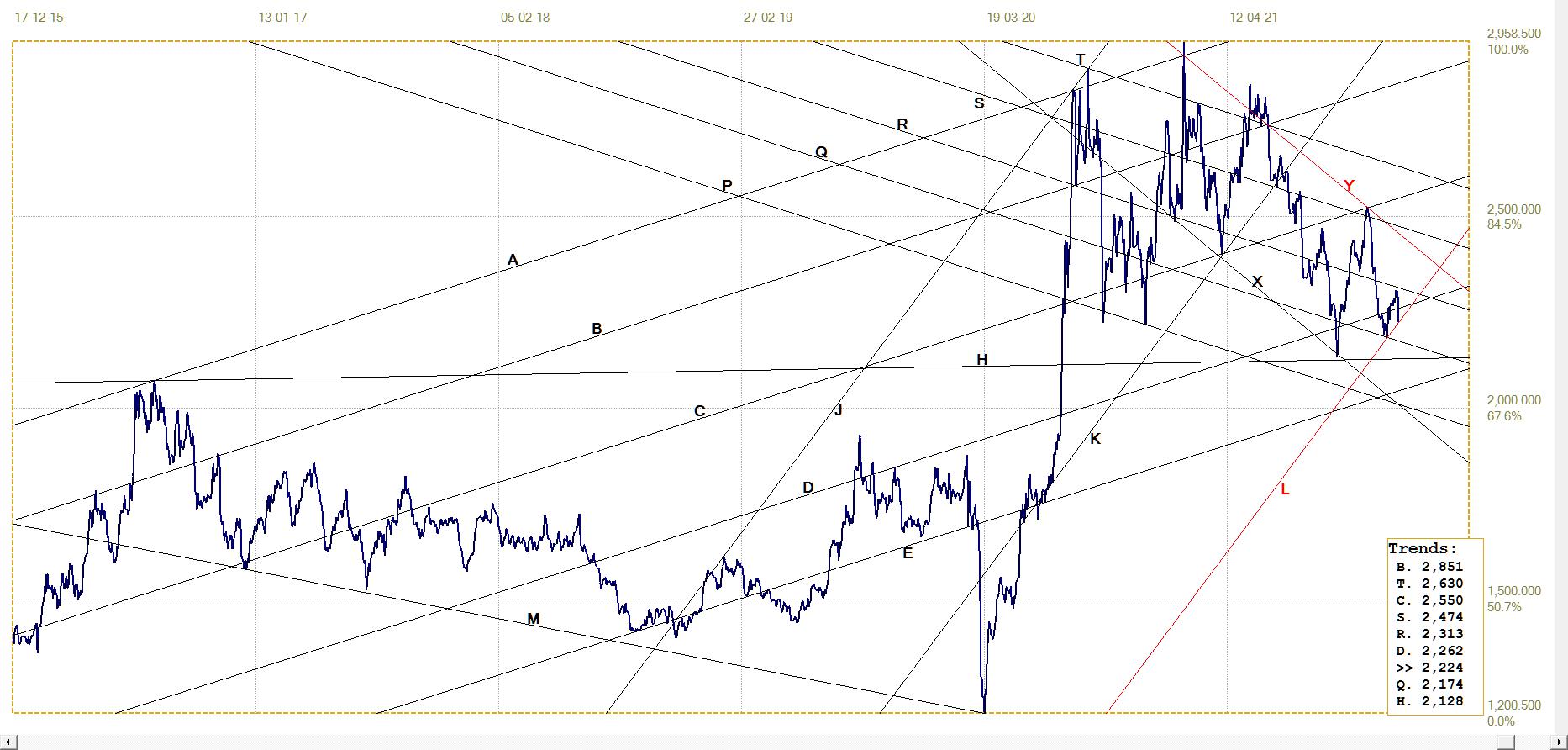

Euro–Dollar

Euro–dollar, last = $1.1359 (www.investing.com)

The euro’s reversal higher off lines W, E and S soon ran out of steam and then also failed to hold in its bull channel KL. However, last week the euro rebounded off the new low, first to briefly touch line L and then resume with more vigour to break back into channel KL.

The minor formation below line L that is left behind by the behaviour of the price is a known chart pattern, a ‘bifurcated low.’ When it develops at the end of a bear trend – and with its inverted form, a bifurcated top at the end of a rally, it signals a change in trend. When it occurs during a trend, as a break below the trending support line, it is a signal that the trend is likely to be sustained. That it happened here suggests that the dollar is about to weaken.

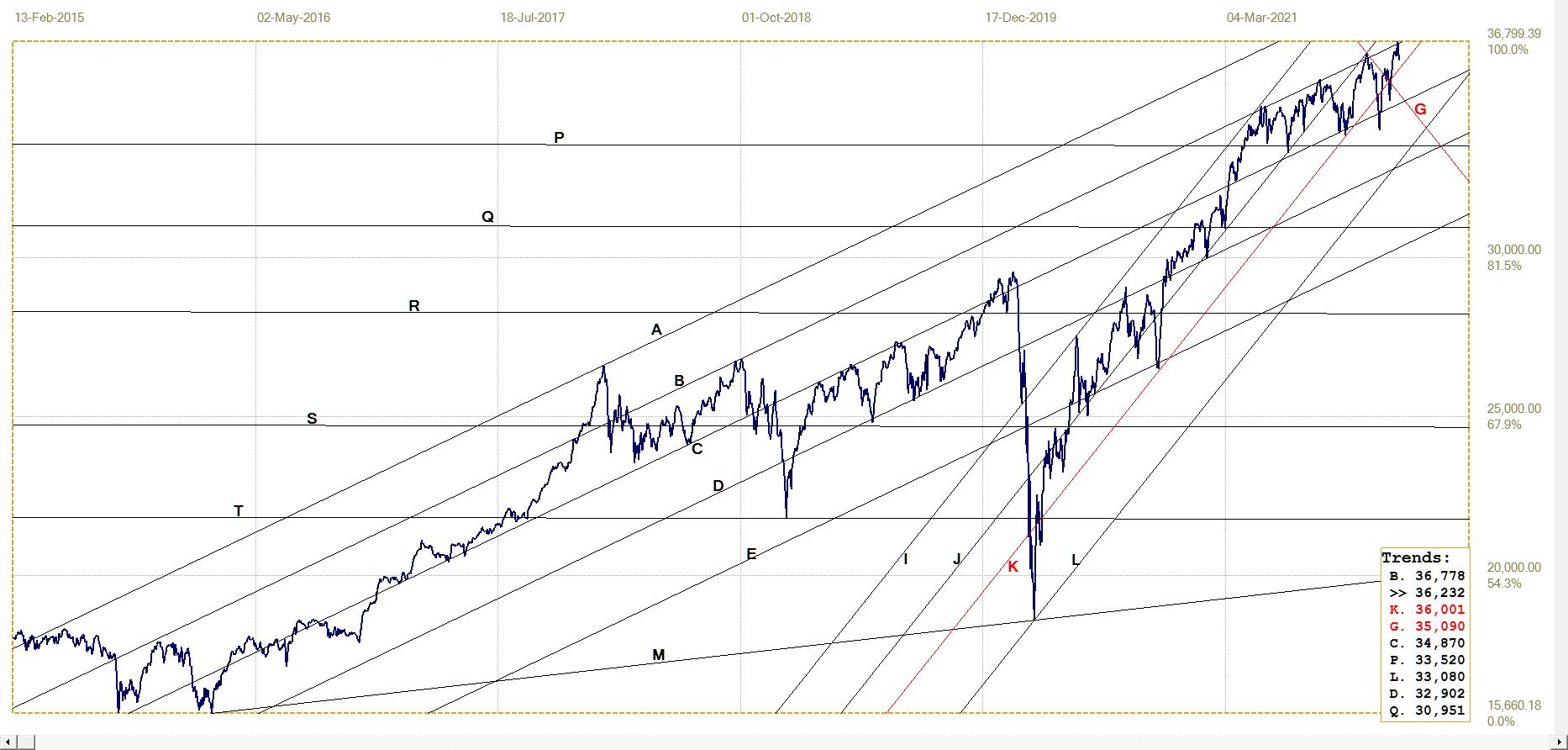

DJIA daily close

DJIA last = 36231.66 (money.cnn.com)

Wall Street started 2022 on a high note, extending above the all time high the DJIA had achieved at the end of 2021. But after two bullish days, the market turned softer. The overall loss by Friday is less than a thousand points and this is not nearly enough to be considered a sell-off.

The meme that, ‘As January goes, so goes the year,’ probably has been quoted by a number of commentators, as usually happens, perhaps so more in hope rather than because history has shown there to be a high positive correlation between what Wall Street does during the first month and then in the full year. The spectre of increasing rates during 2022 is certain to make many large investors nervous, with pension fund managers who have reduced their actuarial shortfall in particular pondering the hard decision whether to take their gains off the table.

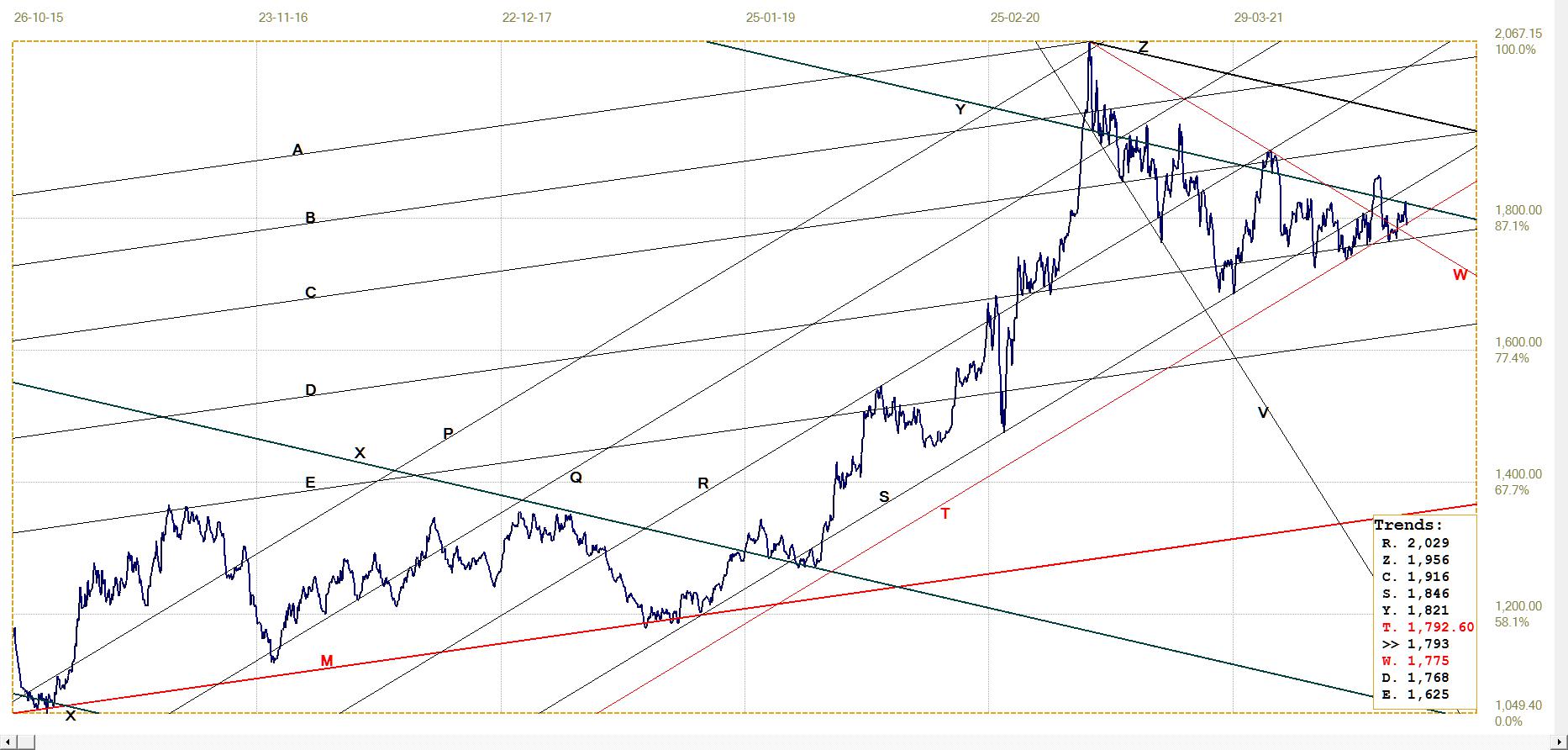

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1792.60 (www.kitco.com)

The ceiling price of $1800 remains elusive. The price of gold only manages to break marginally above that level before getting bashed down again. So far, there has been room to do so while the price still held in bull channel ST. The last minor rally failed to break above line Y, which represents technical resistance in addition to a psychological factor that the Cabal exploits. They know that large round numbers often represent a target that speculators set as a target to take profit.

Let us hope that the technical support of channel ST proves more resilient than the resistance along line Y to soon result in a definite break higher above line Y. Perhaps if the dollar does weaken, as expected from the chart of the euro, this may well happen.

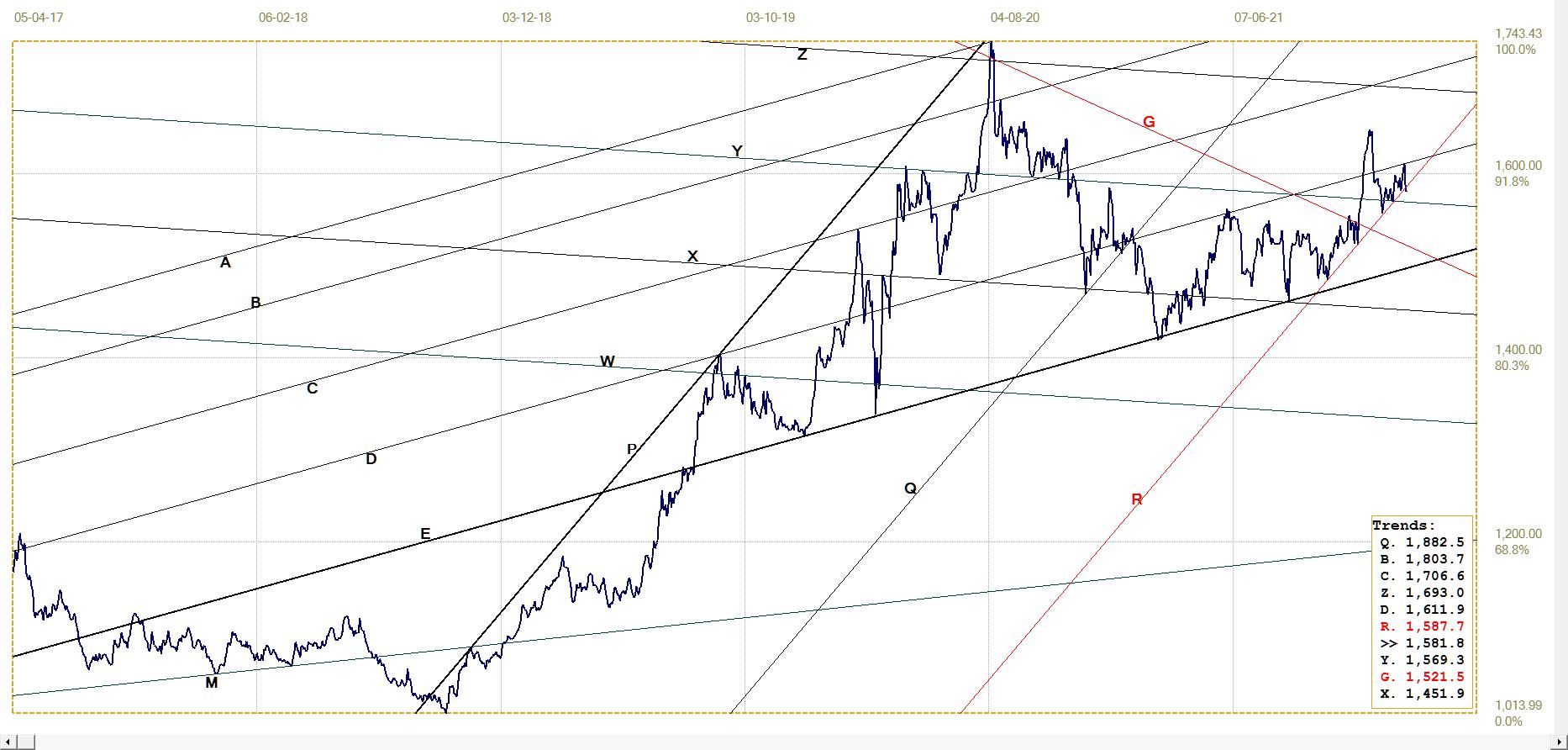

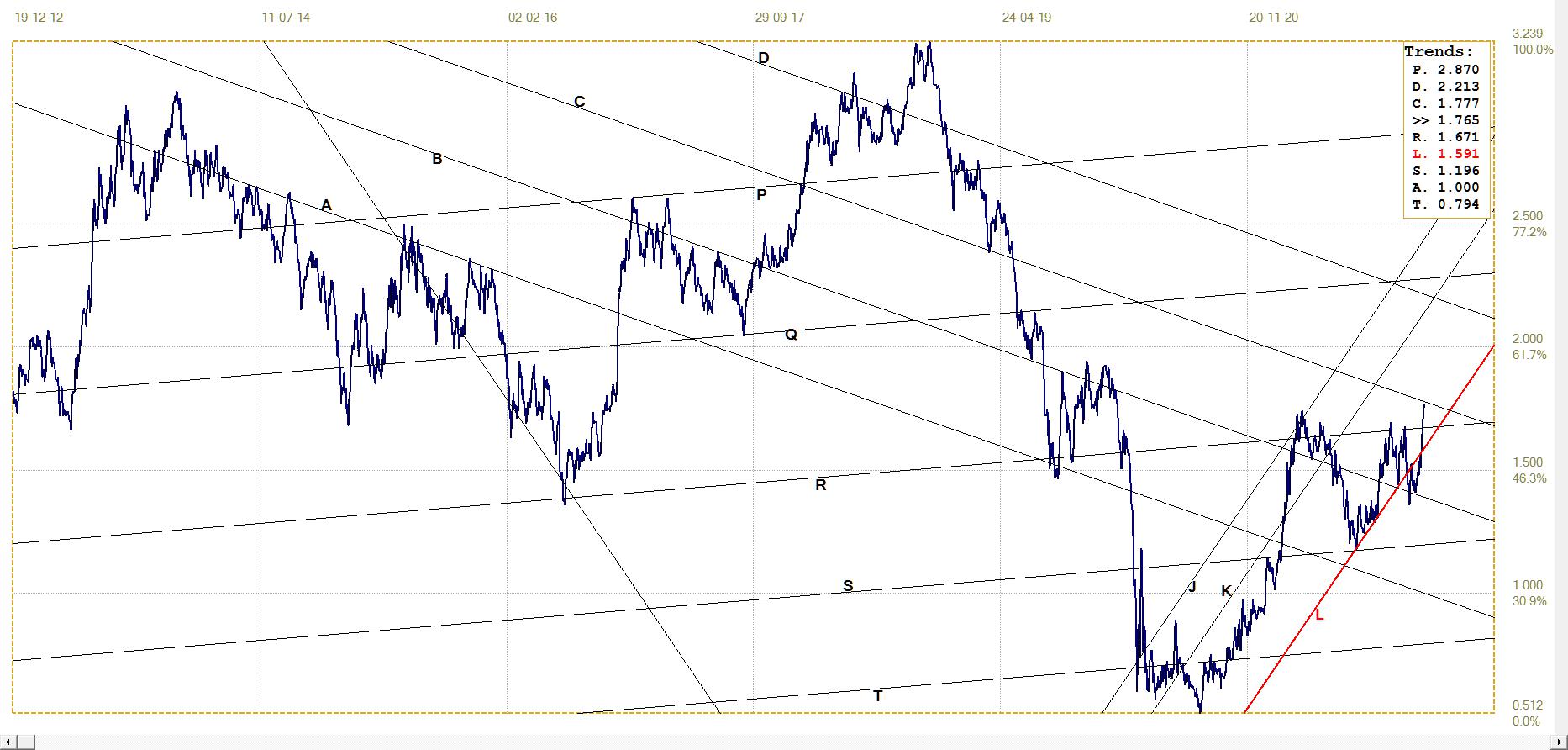

Euro–gold PM fix

When the euro price of gold rallied a second time off line R, it speedily broke to above the resistance of lines Y and T to form a spike high. The rally could not be sustained and soon broke back below lines D and Y to again find support at line R. The euro then meandered higher, keeping close to line R, and managed to break above line Y again, but line D did hold.

It is now in much the same situation as dollar gold: holding in a bull channel, but then failing to break above resistance. Here too, should the dollar weaken as anticipated, the euro price of gold could benefit.

Euro gold price – PM fix in Euro. Last = €1581.79 (www.kitco.com)

Silver Daily London Fix

Silver daily London fix, last = $22.295 (www.kitco.com)

Silver issued a warning of weakness when the break above line S soon reversed off resistance at line C and the top of bear channel XY. The weakness carried the price steeply lower to again break below line D, nevertheless then held and reversed higher off the old line Q. The price struggled to make headway bit by bit, but then did break briefly above line R to return to line L.

Silver now joins dollar and euro gold, holding close to the support of a bull channel, yet with resistance not far ahead. The key to what happens is again the dollar. Should the euro analysis that indicates a possible weaker dollar hold true, silver might join gold in taking off on a rally early in 2022.

U.S. 10–year Treasury Note

10–year Treasury note, last = 1.765% (Investing.com )

The break below steep channel JKL reversed direction to leave a bifurcated low below channel Kl. When this happens at the end of a market trend, it signals that a reversal is taking place. Here, along the side of the bull channel, the signal usually is the trend is expected to continue higher. The break above line R is first confirmation that the yield has set off in a new direction, however it still has to penetrate and hold above line C before the trend higher is in place.

West Texas Intermediate crude. Daily close

Much like the yield on the 10-year Treasury, it seems that the crude oil market also now has accepted that higher inflation is here to stay. Preparation for inflation in the energy sector obviously has a large probability of being a self-fulfilling prophecy about it. Fear of inflation could infect the dollar as well, which might imply that a weaker dollar could be on the cards and the energy sector and bond market are preparing for that.

WTI crude – Daily close, last = $78.90 (www.investing.com)

©2022 daan joubert.

*********