Trump 2.0, Powell and the Bond Market

He’s at it Again

Trump is badgering Powell relentlessly about interest rates. Aside from being great theater (of the absurd), the odds are near zero that the Fed will cut in June and very small they’ll cut in July. CME Group, which we have noted tends to be more of a wind sock than an accurate prediction tool, currently sees the winds blowing to the tune of 97.4% “no cut” in June and 83.3% “no cut” in July. Come September they start to favor a .25% cut.

Meanwhile, he’s at it again.

Suddenly Trump wants to be more like Europe? This is a president who wants what he wants and is used to getting what he wants. I believe he built his empire out of sheer force of will. I also believe he doesn’t know WTF he is doing. He’s just doing it, because “winning… duh”.

“Go for a full point, Rocket Fuel!” Trump wrote in a Truth Social post.

Trump is speaking as if to children, and playing to the crowd. In this case a crowd that is not at all sophisticated in the workings of the financial markets. Various Republicans who are versed in economics (Rand Paul comes to mind) are gathering among the legions of sycophants in the party to raise their voices against Trump’s spending bill (and its new trillions in debt), and I imagine they are also shaking their heads about this delusional demand for 1% rate cut.

Trump wants to punish paycheck-to-paycheckers, savers and grandma’s “safe” income. Is there enough cutting in the tax bill for the little guy to offset this? Meanwhile, with trillions more due to be added to the national debt, Trump is also planning to continue the punishment of future generations. I am not being anti-Trump. I am stating facts, just like I did with Biden, Trump 1.0 and so on and so forth.

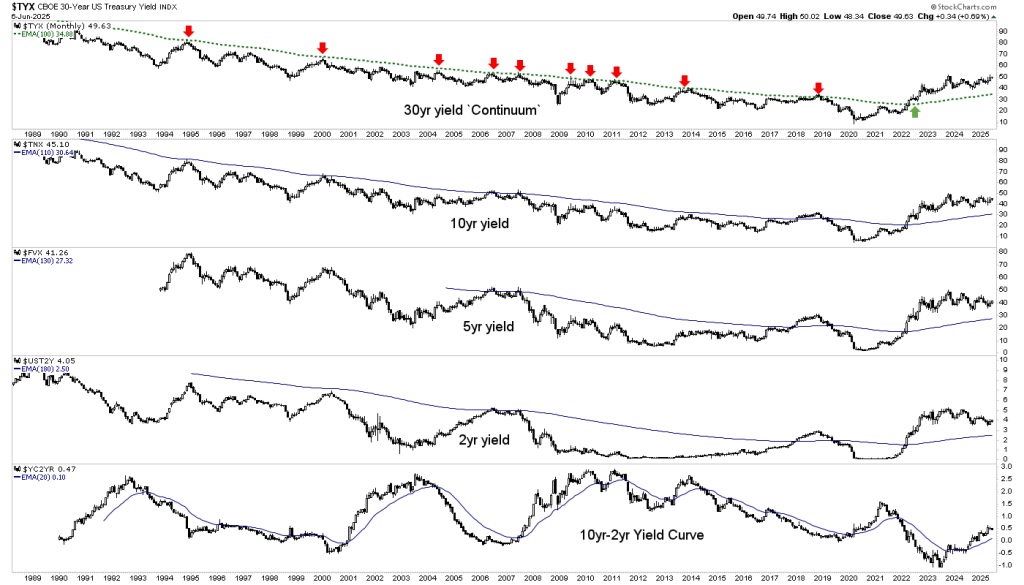

Meanwhile, the long bond’s yield is trending up on a daily chart.

Yields are elevated across the Treasury spectrum, and the 10yr2yr yield curve is un-inverted and steepening.

Yield Curve Warning Still in Play

However, a comment from Friday’s post on the yield curve:

Yes, need to be bearish. Or at least a need to not be dismissive of the bear case and jump the bull bandwagon, FOMOing the relief rally that we knew was coming due to unsustainable sentiment and Trump’s waffling jawbone. We planned for it well ahead of today’s MOMOs who are playing it, FOMOs who are chasing it, and true believers who… well, believe in it. We planned for it while most people were affixing their crash helmets.

I don’t see the yield curve’s big picture as anything less than a warning that the last two real bear markets came as/after the curve had de-inverted and started steepening. The signal remains.

“He’s always late”

Trump is right. Powell was late in 2018 when Trump harangued him relentlessly to cut rates despite the Continuum flashing “code red” about inflation anxieties. Back then Powell listened to the bond market, as the Fed will.

But soon after, the bond market did indeed begin to drop rates, finally climaxing in the deflationary liquidation of Q1, 2020. At the behest of the deflation-signaling bond market, Powell sprang into action and gunned the system with inflationary rocket fuel that persists to this day in some areas.

Now I call your attention to my “tardy Fed” shtick, circa 2021-2022, when 2 year Treasury yields began to rise while the Fed sat on its ass with absurdities like “transitory inflation” emanating from its multiple orifices, along with a political angle as Treasury Secretary and former Fed chief Yellen parroted those words from her own orifice.

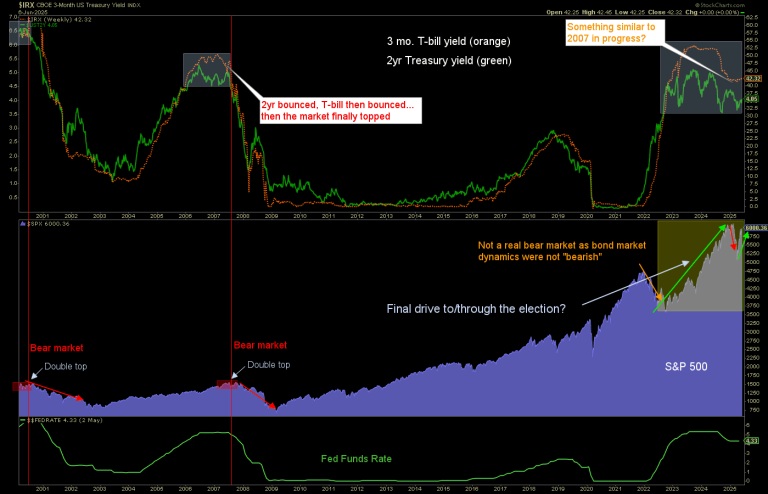

The bottom line is that the Fed will likely be tardy again. As it was in 2000 and in 2007. But economic items like Friday’s payrolls report (moderately positive vs. expectations, before revisions) keep bond yields firm for now and thus, keep the Fed firm. Sort of like 2007, eh?

Trump as “market seer?”

Ah, no. Trump as the boy in the sandbox who wants all the best Tonka Trucks and other toys. Indeed, he wants the whole sandbox. Trump cannot be taken seriously when he at once touts the strong economy (due to tariffs) amid the bond market’s fears of inflationary effects, but calls for rate cuts as in Europe.

Is America not “great again”? Or are we led by a man who is another in a long line of ‘debt-for-growth’ (at all costs, especially to future generations) proponents? Trump built his fortune in real estate, after all. That means debt leveraged for growth. He built an empire out of debt (and a strong personality). But this is a sovereign country and economy, not a real estate empire. Yet Trump wants what he wants, and he wants it now.

Trump is an easier target than the Biden/Yellen operation was. They played the game, hid behind an opaque presentation of normalcy. They gunned their agenda as well, only they were sneakier about it. Trump is a battering ram. He is, in my opinion, no better economically, but maybe not so much worse. What he is… is out in the open. But I do not believe he “sees” much of anything, other than his agenda with so many moving parts it is hard to believe that there is a sensible conclusion built into the plan.

NFTRH 866 then went about its usual duties, fleshing out market indications and technical analysis on stocks, commodities, precious metals and currencies.

For “best of breed” top-down macro analysis and market strategy covering Precious Metals, Commodities, Stocks and much more, subscribe to NFTRH Premium, which includes a comprehensive weekly market report, detailed NFTRH+ updates and chart/trade setup ideas, and Daily Market Notes. Receive actionable (free) public content at NFTRH.com and subscribe to our free Substack. Follow via X @NFTRHgt and BlueSky @nftrh.bsky.social, and subscribe to our YouTube Video Channel. Finally, check out Hammer’s trade (long and/or short) setups.

********