Vindicated…At Last

For many years, now, perhaps the main theme in my writing has been the inequity visited on working US households by the newfangled CPI introduced during the first Clinton administration. This change meant wage and salary increases would lag the real increases in the cost of living by a wide margin. Much of the past decade, I was like a voice in the wilderness – for a long time there were nothing more than rare expressions of concern about the financial position of middle class America. Often mainly with reference to their increasing load of debt. While such concern recently has become more widespread, a report by CNBC of a study that has been done has now at last given substance in the MSM to what I have been saying for more than a decade. Could this be the thin edge of the wedge in the reporting of this problem?

The CNBC article is appended at the back of this Report. The heading and a few facts are sufficient for now: Social Security benefits buy 34 percent less than in 2000, study shows. This comes as no surprise, except how low the figure is. Using data from https://www.ssa.gov/OACT/COLA/colaseries.html, the average COLA adjustments from 2000 to 2017 is 2.14%. The link between 2.14% and the real increases in the out of pocket ‘cost of living’ since 2000, as the term ‘COLA’ playfully suggests, is at best tenuous and can only have meaning in a bureaucrat’s mind.

That article gives at least some credibility to my theme that working America – at least 80% of US households, according to a chart that was shown here recently - is being impoverished over a period of two decades. Not by some chance event long ago or by those sneaky Russians hacking the BLS computers, but as a recognised side effect of the US government’s efforts to “balance the budget”, i.e. to be able to reduce the increases of all payments under various entitlements, including that of Social Security, to be smaller than actual increases in the cost of living. This was done well knowing that households that enjoyed steak soon would have to settle for hamburger and later perhaps even for dog food.

Now after more than two decades of this modified CPI, the budget is much further from being balanced than it used to be in the early 1990s, while recipients of Social Security – and other people on entitlements AND employees who receive increases linked to the CPI, to a greater or lesser degree – officially are now 34% worse off than they were in 2000. This consistent shortfall in the purchasing power of Social Security has increased by 4% from January 2016 to January 2017, so the average annual rate in impoverishment of say 2% since 2000 has now doubled.

The longer term outlook for the US and in effect for at least the western part of the globe, as discussed here during recent weeks, included danger signs of things that can go wrong, with a strong focus on the impoverishment of working America – and likely a similar trend in other countries as well. The CNBC report states a measure of how bad the situation has become while the rate of declining purchasing power is speeding up. This implies the time for the situation to be recognised as a crisis – as only then action is taken either by the government or by impoverished Americans – is now running out. The question is what the trigger for action will be.

If the trigger is to be some other event or a new trend that brings the crisis to the boil, there are candidates waiting in the wings. One is the threatening trade war, which, if it does develop much further and the effects begin to bite, with prices rising faster, could suddenly bring the impoverished state of many US households to the front page.

Another trigger could be a purely financial crisis, similar to 2007/8, which suddenly spills over into the broader markets with near disastrous effects. There is one such in Europe, in the form of the wobbling Deutsche Bank, which is just waiting for the right moment to go belly up. When that happens, it won’t be just another Lehman event that can be resolved and kept under control with a few tens of $trillion from the US Federal Reserve, perhaps with help from the ECB.

Thirdly, will any revelations from the close examination of the DoJ/FBY by Congress bring much larger game into the open and within striking range of the sword of the blindfolded lady? Given the strong polarisation in the US with Trump as the focus, clear and strong evidence that those casting most stones in his direction happen to be doing so from within their glass houses, could elicit a real witch hunt with many far ranging side effects. Not something that one wants in an already unstable social and economical situation. Time will tell.

Euro-Dollar

Euro-dollar, last = $1.1654 (www.investing.com)

From various comments on the web, it would seem the financial situation in Europe is fraught with risk, much of it arising from a precarious situation in which Deutsche Bank finds itself. It is several times larger than what the Lehman collapse was back in 2008 and this time around the global debt situation and central bank balance sheets will not (easily) contain the crisis a Deutsche Bank in severe trouble could cause.

The euro has lost its gains of two weeks ago when it rebounded off the recent low, ending at a tight double bottom. The double bottom has to live up to its technical reputation and hold, to trigger a new recovery, else the euro soon will be on its way lower, perhaps to test its support at lines R ($1.1460) or L ($1.1402).

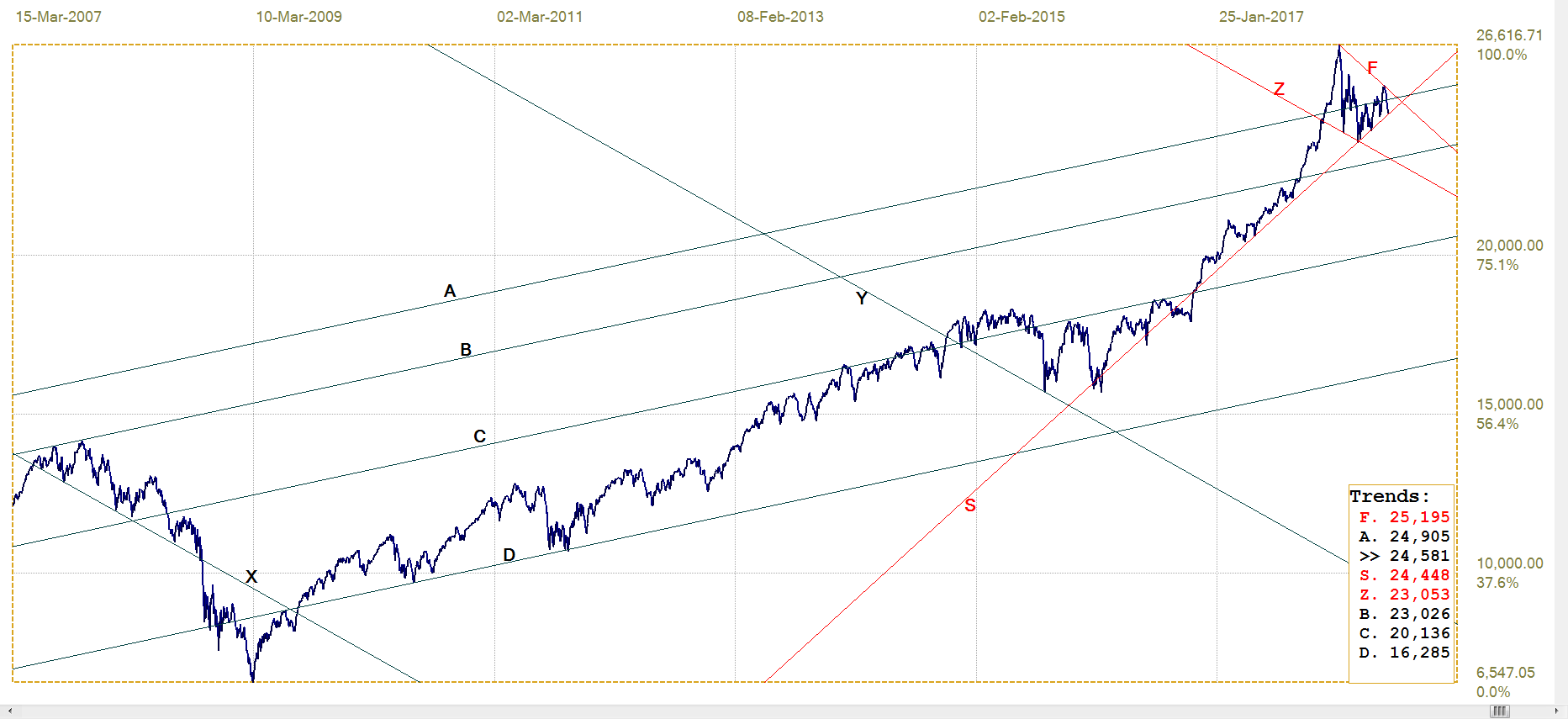

DJIA

DJIA, last = 25090.48 (money.cnn.com)

The DJIA has now evolved into a situation that can be represented by a simplified analysis. The volatile and mostly sideways correction or incipient bear market since the all time high has tested the support along line S (24 448) on three occasions after steep falls and so far has failed to break lower. The DJIA also sits within the wedge shaped pattern between lines Z and F (25 195) which in principle should break higher after the DJIA has completed leg 4 of the wedge pattern by testing the support at line Z by breaking clear below line S. The importance of line S so far, however, could imply that a break lower would resume and extend the bear trend.

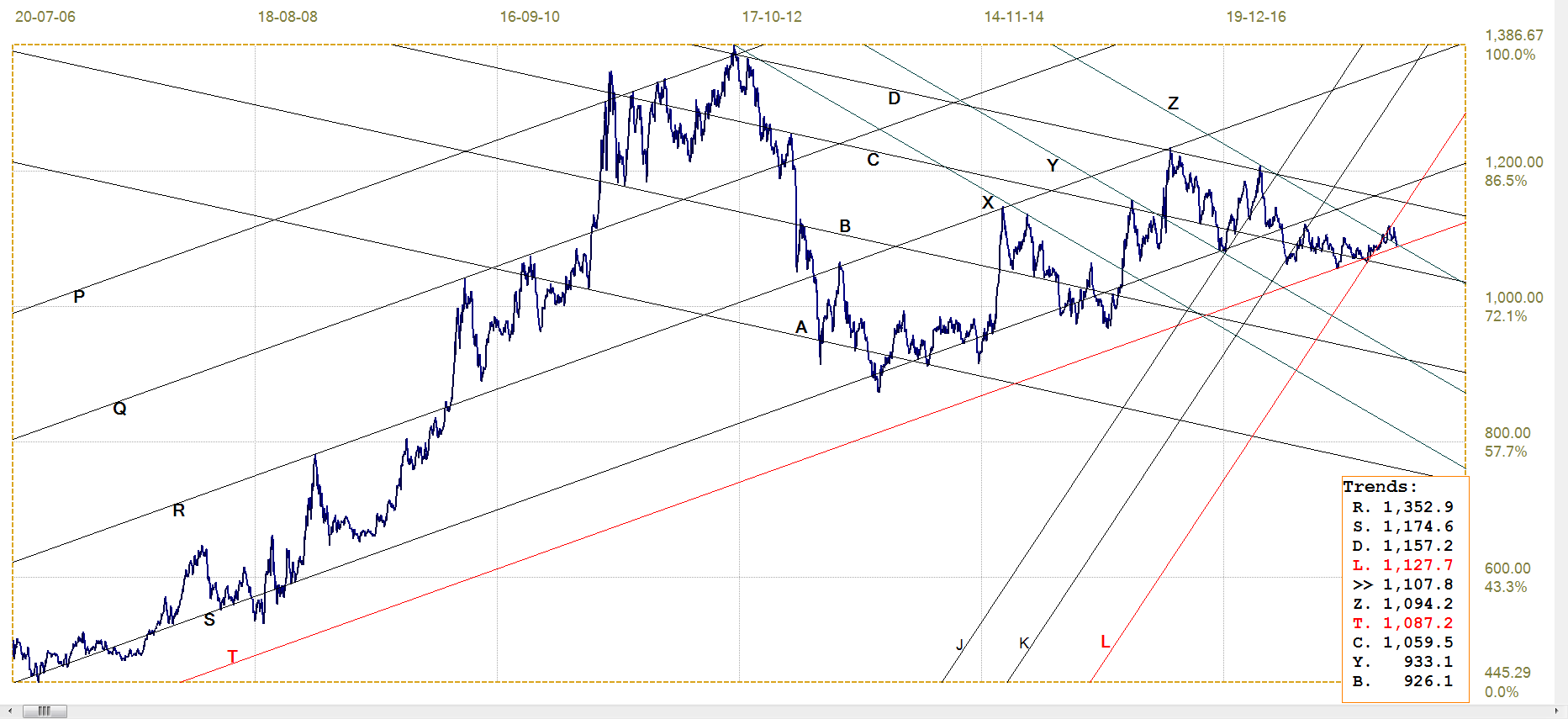

Gold PM fix - Dollars

There is little more to say except that the triple witch that includes EFTs, the expiry of Comex options and futures and the pending June half year end have combined to push the price of cold clear below the long term support of line T ($1295). The price is still holding short of the support along line D ($1256), which is a slight positive for the metal, but then the end of the month is only at the end of this week – much can still happen.

The best, of course, would be for gold to rally back above line T before the end of the month, just to show what can be done despite the manipulation; then to hold the break and extend higher, even with customary head-wind of the NFP number due to be announced a week later. If wishes were horses . . .

Gold price – London PM fix, last = $1269.15 (www.kitco.com )

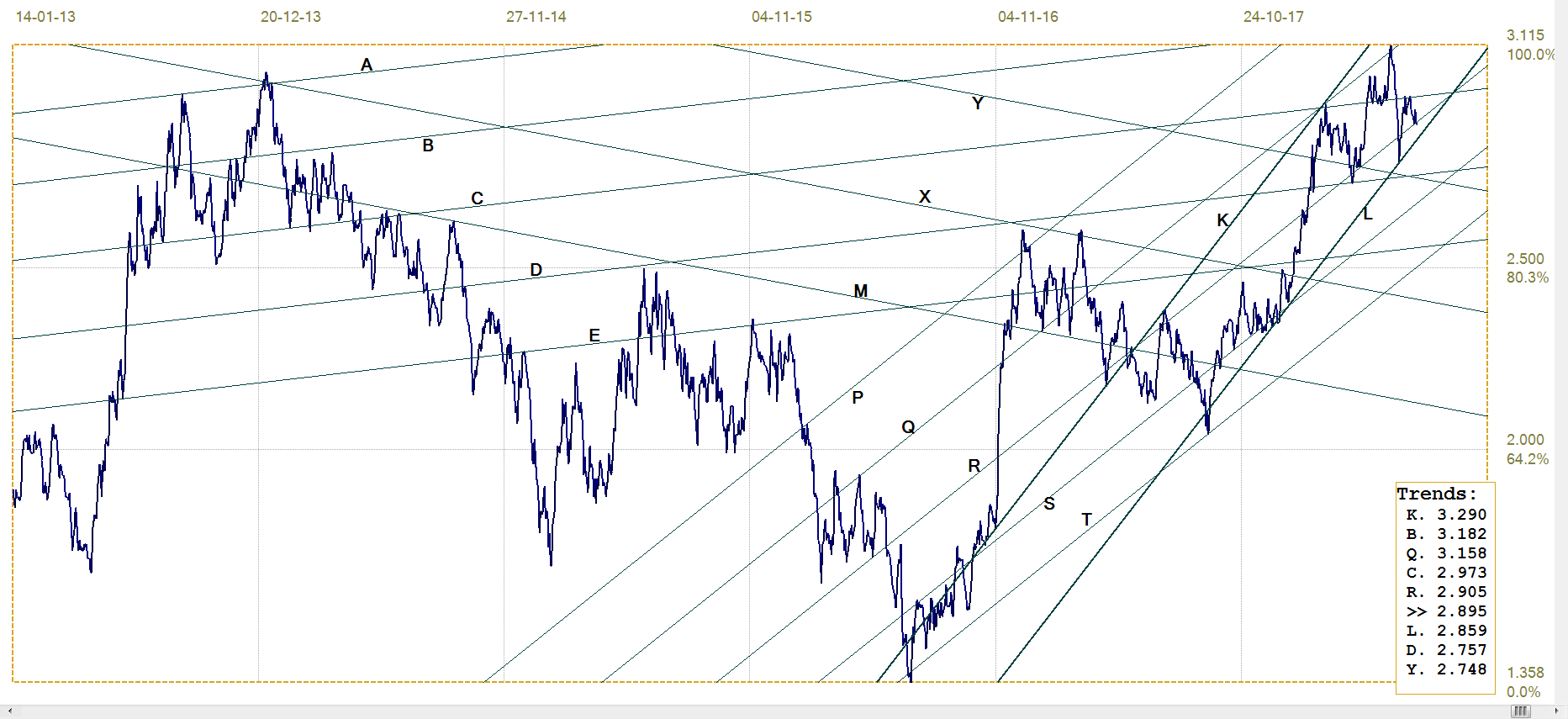

Euro-gold PM fix

With the dollar price of gold in the dumps, the fact that the euro price of gold could hold at and even rebound a little off support along lines Z (€1094) and T (€10887) is only due to a very weak euro. This is at least a glimmer of light for gold, but to keep some value in a suffering currency like the euro is not much of a performance.

The odds seem rather low for a recovery into bull channel KL (€1128) and so the best near term outlook for the euro price of gold is to meander sideways and higher above line T and probably well below line D (€11257). This would of course require that either the dollar price of gold improves or the euro weakens further – or combination of the two.

Euro gold price – PM fix in Euro, last = €1107.8 (www.kitco.com)

Silver Daily London Fix

Silver daily London fix, last = $16.425 (www.kitco.com)

The combination of events during the past two weeks and still to come as June runs out and the date in July for the NFP announcement comes due, means that silver has spent most if not all of this time completely below the $16.50 threshold that has served as the net for a symbolical ‘tennis match’ for a long time. Month end on Friday is also end of the half year and likely to see expiry of many OTC contracts and other reasons to keep a lid on the price of silver (and gold).

Then next week has the Fourth of July on Wednesday serving to distract everyone’s attention from the markets, followed by the NFP number on Friday. This implies we have to wait for the following week at least before there might be indications that the month of July will smile on the precious metals. The waiting game continues, but there will be an end to it.

U.S. 10-year Treasury Note

U.S. 10-year Treasury note, last = 2.895% (www.investing.com )

The change to the analysis shows that the yield on the 10-year has held closely to the bear channel KL (2.859%). A recent rebound higher off line L, to end the steep but brief rally off the current high in the yield, has so far failed to break above line C (2.973%) and is testing line R ( 2.925%), a little above the bottom of channel KL.

Channel KL has been in place since May 2017 and the Bear is in control as long as this channel holds. The future direction of the market is to be indicated when the yield breaks out of the range between lines C and L and – with more rate hikes to come in 2018 – the odds favour a break higher to remain the bear channel.

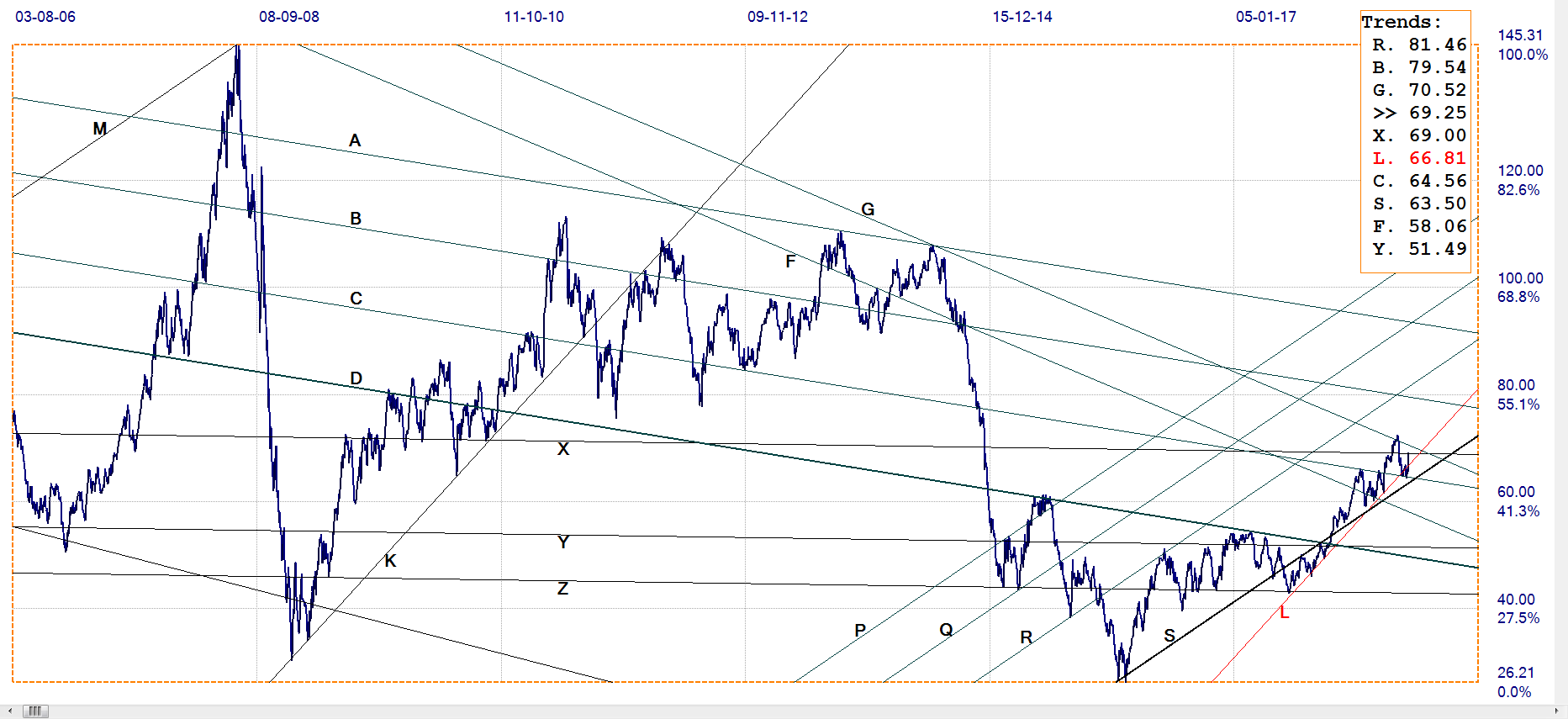

West Texas Intermediate crude. Daily close

The break above the horizontal resistance at line X ($69.00) and then also at line G ($70.52), seemed the start of a bull trend. But the positive break above line G failed to extend or even to hold and a reversal lower soon had the price back below line G and also line X. After some testing, the price has held above line L ($66.81) and is trying to get back above line X to turn bullish again.

News that OPEC intends to increase production in order to assist the US in Trump’s effort to improve the economy, is likely to scupper the rally and send the price of crude lower, perhaps even to test the important support at line S ($63.50).

WTI crude – Daily close, last = $69.25 (www.investing.com )

--------------------------------------------------------------

©2018 daan joubert, Rights Reserved chartsym (at) gmail(dot)com

Social Security benefits buy 34 percent less than in 2000, study shows (CNBC via Midas)

Housing and medical items top the list of fastest-growing expenses for retirees.

Older Americans experienced a 4 percent loss in Social Security buying power from January 2017 to January 2018.

For 2019, benefits are expected to increase by at least 3.3 percent, which could help reduce the year-over-year effect of higher cost.

About 47 million older Americans receive Social Security. Overall, the benefits comprise about a third of income among those age 65 or older, according to the Social Security Administration.

The annual report from Johnson's group examines the costs that typically comprise household budgets of older Americans and compares their price change with annual COLAs. Based on those comparisons, the research found a 4 percent loss in Social Security buying power from January 2017 to January 2018 and a 34 percent decrease since 2000.

While COLA increases since 2000 cumulatively have equalled 46 percent — matching inflation over those years — typical retiree expenses grew by 96.3 percent, the study shows. Of the 39 costs analyzed in the report, 26 grew faster than the percentage increase in COLAs from 2000 to 2018.

********

More from Gold-Eagle