Wealth: Perception or Reality?

Once again, the lapdog media is agog over increased consumer spending data stemming from what it calls ‘rising wages’. We’ve been down this road before a time or three and we know the major debunking points of this particular government statistic. What is curious this time around is that the reports are in direct contradiction with recently released consumer sentiment data, which took the plunge last month. Then there is all the nonsense about a government budget (or lack thereof), wars all over the Middle East and rumors of wars in Syria, Iran, and who knows where else. Be on the lookout for big companies inking deals that involve trespassing on the property of sovereign nations. Find these deals and you’ve probably found the next war. But I digress. There’s going to be a lot of that this week. There are at least five topics flying around in my head, so please bear with me.

To that end, I have asked ‘Two Cents’ readers for their thoughts regarding the resumption of my weekly podcast ‘Beat the Street’. I am happy to announce that it will in fact resume – most likely on Wednesday October 9th, 2013. More details will be forthcoming. The goal of the show will be the same as when I started it back in 2007: to provide additional information on topics that I just don’t have time to write about. The podcasts will be 30-45 minutes long, depending on what is going on. There may be some very short snippets as well, which will be event-driven.

The Wealth Effect and Its Concomitant Trends

There is a definite trend in the propaganda business and the major epicenter, at least in my opinion, is Bloomberg News. And it would appear that outfit has one particular group of ‘reporters’ that are responsible for the majority of the spin stories we see on Bloomberg. I’m not simply taking potshots at Bloomberg here either. The fact of the matter is that many other sources get their story ideas from Bloomberg, CNBC, and the other major networks. So any sources of misinformation need to be called out because you can bet that stuff is going to be repeated, which is the whole idea. Goebbels would be proud. Pick a lie, make it a London Whale of a lie (no apologies to JP and the boys), and then repeat it like crazy. Eventually it’ll become the truth. That is precisely what is going on here.

All of this revolves around the ‘wealth effect’, which I’ve been harping on recently, and with good reason. It is one of the mechanisms, along with the perception of value of an intrinsically worthless currency, that the powers that be count on to perpetuate the sham that is the global economy in 2013. The goal here is to look at what is really going on and to demonstrate how economic actions are following the perceptions rather than reality. This is an extremely bad prognosis for the future of this country (and the world in general), but extremely good news for the establishment that profits from such actions.

Consumer Spending Increases – Faux Statistics at Their Finest

Directly from the Bloomberg article linked here:

“Household purchases, which account for about 70 percent of the economy, climbed 0.3 percent after a revised 0.2 percent advance in July that was more than previously estimated, the Commerce Department reported today in Washington. The advance in August matched the median forecast of economists in a Bloomberg survey. Incomes rose 0.4 percent, the most in six months.

Rising home values, stock market gains, and an improved job market are cushioning the effects of this year’s payroll tax increase and giving households the means to sustain purchases. At the same time, spending growth has shown little momentum since the end of the second quarter.”

What we see above is the ‘wealth effect’ I have hammered so many times in the past. It is not a difficult concept. If people feel secure, they’re more likely to engage in additional spending. The redux here occurs in the fact that there is solid data that points to the fact that people aren’t feeling more secure about their overall situations. In fact, as most data points, more and more people are feeling much less secure. And another thing we have to look at is debt load. The debt load carried by the consumer, after taking a break a few years back, is on the rise again.

What is also disturbing is another trend we’ve been watching develop over the last several decades. I’m going to use car loans as an example, and that is the duration of loans in general. The number of months has increased dramatically from less than 3 years in 1971 to roughly 5 years today. So what? Well, that is a 67% increase in the length of the loan and that means 2 more years of interest payments. This data doesn’t include lease arrangements. These are just outright purchases of new vehicles through finance companies. Given a 5-year loan period, it is a pretty safe bet that the average family is always making a car payment now since it is nearly unheard of for your average family to have less than two vehicles. Back in 1971 the number of single income homes was much higher, which translated into more households having just one vehicle.

So where is all of this going and what does it have to do with consumer spending? These are all spinoffs of the wealth effect, with one important divergence: debt load no longer appears to detract from the wealth effect; at least in the aggregate. The stigma of carrying debt has been all but eliminated. It has become a way of life. A cost of doing the business of life. We suspected this at the anecdotal level, but the data are really starting to back up that assertion.

The not-so-USFed, of course, will take quick credit for the next graphic and pat itself on the back and state what a great job it is doing helping the consumer with its debt load. Interest rates on credit cards have fallen considerably to a smooth 12% as of the most recent measurement. Keep in mind this is an average and doesn’t account for many non-traditional types of borrowing such as payday loans. Let’s run some quick scenarios. We know the average college student with credit card debt leaves school with a balance around $4K. They get married, so now we can multiply everything by two. While it is a good bet that they pay more than the average, let’s assume they are charged the average rate. That translates to $480/year in interest or $40/month. No big deal, right? Given that the minimum payment on many of these loans (I have seen the statements) is $25, see the problem here? This is just one example.

Now let’s be more realistic and assume they’re paying 20%, which has been more in line with what I’ve seen in my business of dealing with these situations. That $480/year suddenly becomes $800/year or close to $70/month for each person. Just in interest. Then they have their $54,000 average of student loans (for a two person household) at an average of around a 3.9%. Granted, this is due to the government subsidizing this market even further and much of the debt was incurred before this happened and as such is at a much higher rate, but again, we’ll be conservative. At 3.9%, that $54,000 in loans requires $2,106 or $175.50/month in interest payments. Now let’s be realistic. Let’s say the average student has an equal split of subsidized and non-subsidized loans. Their average rate would be 5.35%. Applying that to their $54,000 balance, we hike the numbers to $2,889/year or $240.75/month.

Add that to the realistic credit card interest and suddenly that new grad household is paying almost $400/month just in interest. How wealthy are these folks feeling? Yet they spend like crazy, taking on even more debt as they purchase cars, and in some cases, homes – all before their student loans are even dented. The stigma is gone and the spending ensues, despite the rotten job market for many of these grads.

That is the counterpoint to the above – consumer sentiment. Despite the increasing debt loads and stagnant labor market (covered below), people, in general, feel better about things than they did in 2008. So, is the sentiment following reality or is it following the perceptions aided by the fictitious ‘wealth effect’? You decide. Based on all the information we have to date, your answer is going to based almost entirely on which half of the country you’re in. America is being split in two. The middle class is disappearing. The perceptions of those closer to the top are going to be much different than the growing numbers at the bottom. And looking at the chart below, a lot of where we’re at has to do with whom the University of Michigan folks are talking to; which they don’t tell us.

The bottom line is that you can’t look at any of these ‘statistics’ and use them to decide your personal position. You need to gauge your personal sentiment off the factors that are directly affecting you.

The Booming Job Market – The Most Cruel Hoax Yet

A second factor that Bloomberg cited for the boost in consumer spending is the growing labor market. We can have all kinds of fun with this one and have many times in the past. I’ll spare the gory details, opting instead to provide just some cursory analysis and you can draw your own conclusions about how ‘healthy’ the job market is. I will say as an aside that America is clearly going in two directions in this regard. I recently posted an article on my blog regarding the unemployment rates for high wage earners versus that for lower wage earners. I’d encourage everyone to take a few extra minutes and read that article. It is a key piece of the puzzle when one endeavors to figure out in what direction the country is headed. This is a trend, not a fad.

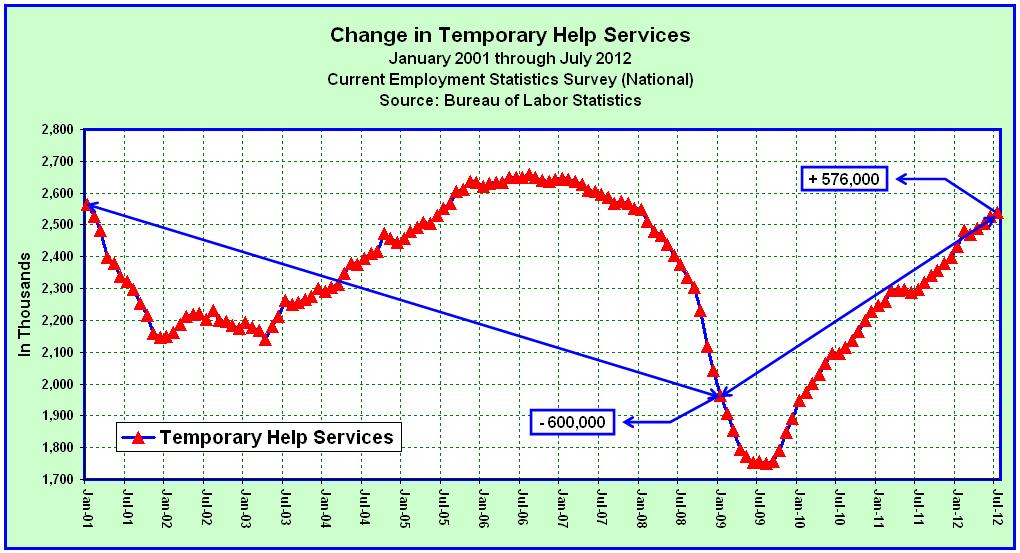

On to the job situation. I’m going to keep this relatively short with the idea of covering it during a podcast in the near future. It is well known that one of the biggest reasons the ‘jobs’ numbers have improved is because of the explosion in temporary positions. These jobs are tailor-made for firms that don’t want to deal with having benefits administrators, retirement plans, etc. or are just in need of temporary help because their businesses are seasonal or cyclical. The emphasis is on the fact that these jobs generally don’t pay very well and don’t offer benefits. I wouldn’t go as far as to say they’re not ‘real’ jobs; however, there is definitely a quality versus quantity argument to be made here.

What is interesting is that the economy shed nearly 600K of these jobs from 2001 through the middle of 2009. That was an 8-year period. The economy regained nearly all of those lost temp jobs in just three years. On the surface, this might appear to be a good thing and support the notion that the economic recovery was robust and healthy. I would turn it around and opine that the economy never was healthy to begin with during the 2001-2009 period, and just returned to that unhealthy imbalance after the 2007-2009 ‘glitch’ period during the crisis. Backing this up is the fact that according to my in-house alternate GDP model, which is based on the Cobb-Douglas output function, the US entered the ongoing recession in 2006 and has yet to emerge from it.

A second big area of growth is the service area. While some of these jobs pay very well, this area is indicative of our economic inclination if you will, in the aggregate. We’re still oriented towards the service economy model rather than the goods-producing model. Even our service model economy hasn’t returned to levels anywhere near those before the crisis. What recovery? The old adage ‘he who produces gets to consume’ still applies folks. We’ve been sustaining this unsustainable paradigm with debt, deficits, and all sorts of monetary mischief. It will end. Nope, I don’t know the day, but the day is irrelevant. If you knew the day you’d wait until the day before to worry about it. It is better if you don’t know. The more important fact is that it will break. Sadly, we’ve learned absolutely nothing from our European counterparts with regards to this issue.

If an economy is going to base 70% of its ‘growth’ on borrowing money to consume, then a) someone has to be willing to continue lending and b) someone has to be willing to produce knowing that they’re going to get ripped off by inflation. I’d say we’ve got the perpetual lender status covered. The not-so-USFed will lend because it costs it nothing to do so. It expends zero labor, land, capital, or resources to contrive that which it lends. In return it has a growing population of debt serfs, who have no problem with that servitude because its yoke appears easy and its burden light. But like every other big lie there is that precious moment of awakening.

Then there is the problem of who is going to produce all the stuff we consume knowing they’re getting a rotten deal because the paper tickets we continually ship them in exchange for their very real expenditures of land, labor, capital, and scarce resources are worth less every day. I’m going to throw something out there in closing that people might want to consider. We have a legion of debt serfs and all this talk about jobs returning to America. Anyone want to be bold enough to connect the dots? Think about it. Temporary jobs, stagnant wages, unsustainable debt loads, and few choices. Sounds like a perfect recipe for the 21st century equivalent of ‘slave labor’ to me. Maybe we’ll be the new China – a country of people working for next to nothing to ship those products overseas to where the wealth has accumulated to pay off our debts. If you see a FoxConn factory going up in your town, then it is really time to start worrying. Just some food for thought.

If you got something out of this article or the ‘Two Cents’ column in general, I humbly ask you to think about tuning in to the new podcast when it goes online on 10/9/2013. We’re going to be talking about all of these things and much, much more, including things you can do to help yourself. I’m not talking about market secrets or get rich quick schemes, but things that can be realistically done to improve your situation. Your input will be not only welcomed, but also actively solicited.

********

Andrew W. Sutton, MBA Chief Market Strategist Sutton & Associates, LLC www.sutton-associates.net[email protected]