What Should the Federal Reserve Do Now?

share

share

share

share

share

share

share

share

share

share

Inflation in the United States has fallen from its elevated levels a couple of years ago, although not quite all the way to the Federal Reserve’s target average rate of two percent per year. The Federal Reserve has been raising the federal funds rate progressively since early 2020 to lower inflation. It is well known that these increases affect the economy and inflation only over time. The effects of these increases still are playing out.

The Federal Reserve did not change the federal funds rate at its most recent meeting. Information provided after the recent meeting suggests, though, that the Federal Reserve might increase the Federal Funds rate by 25 basis points from its current range of 5.25 to 5.50 percent. This 25 basis point change would be a sideshow. There is no real reason to think that raising the range by 25 basis points will have much of an effect. The direct effects on the economy of any 25 basis point change in the rate are small. The effects on the Federal Reserve’s reputation for being concerned about inflation would be small as well at this point. That said, a higher rate – more than 25 basis points higher – may be desirable in the future if inflation does not come down from its current level.

An important question: When inflation is down to 2 percent, what is the appropriate level of the federal funds rate? The federal funds rate is a nominal interest rate, a rate in terms of dollars. This nominal interest rate equals the expected real interest rate plus the expected inflation rate. If the Federal Reserve is to maintain an expected and actual inflation rate of two percent, then the federal funds rate should be set at an appropriate level for that inflation rate. If the real interest rate is two percent, then a federal funds rate of 4 percent is appropriate. If the real interest rate is three percent, then a federal funds rate of 5 percent is appropriate.

The real interest rate on federal funds is the real return on a particular financial transaction. It is not the same as the real return on quite different financial instruments. It also is not the same as the real return on physical capital, which is often equated to the federal funds rate in standard economic models.

This makes the problem of the appropriate federal funds rate somewhat more difficult, because it cannot be estimated by straightforward inferences from returns on stock or physical capital. for example. Instead, complicated estimates of various risk and liquidity premia are used to make inferences. There is always reason to doubt the accuracy of the estimates.

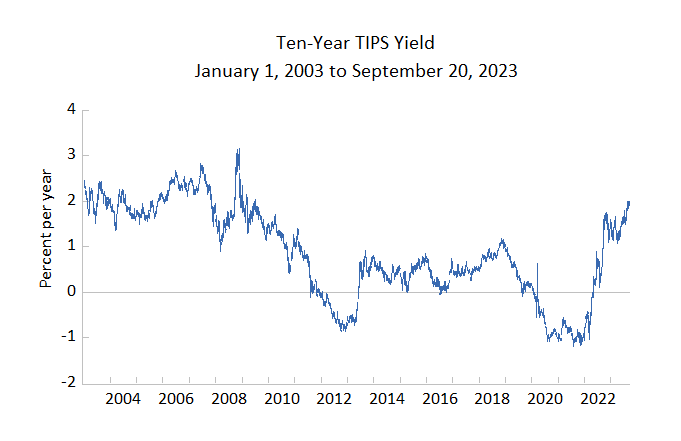

A simple, rough way to proceed is to use the interest rate on long-dated Treasury Inflation Protected Securities (TIPS). These rates are estimates of expected real interest rates on TIPS over the term to maturity. It might seem that these TIPS are risk-free because they are government securities and compensate for inflation, but they are not. The rates and prices can change. These changes can be correlated with other changes that either increase or decrease investors’ overall risk. Investors are risk averse and the rates on TIPS reflect that risk in either higher or possibly lower rates. Hence, the rates are only estimates of expected real interest rates for federal funds. But they are pretty good estimates. They are the rates investors today are willing to receive net of inflation on government securities.

The figure above summarizes the returns on the constant maturity 10-year TIPS rate since 2003. These rates have changed a lot over these two decades. The rates on 5-year TIPS have behaved similarly. These data suggest that if the Federal Reserve is to attain its goal of 2 percent inflation, a federal funds rate of about 4 percent would be the right neighborhood eventually. A more complicated analysis using more detailed data from the US Treasury reaches a similar conclusion.

It would be premature to lower the federal funds rate right now. Inflation is running above 2 percent by any measure, and a current temporarily higher rate on short-term securities can reassure markets that the Federal Reserve is aiming at a lower inflation rate.

Still, these market signals provide an indication of the route that will be taken if inflation recedes to 2 percent. Longer term, a federal funds rate on the order of 4 percent is consistent with market participants’ current expectations of real interest rates on government securities.

Courtesy of AIER.org through Creative Commons Attribution 4.0 International License. Article originally published here.

share

share

share

share

share