Why M1 Money Supply (Cash) Is Skyrocketing Like No Other Time In History

In my last Patron post, which I eventually made available to everyone, I revealed a little-known (at the time) fact that M1 money supply (the most liquid forms of cash — bills, checks and basic savings accounts) had grown faster than any time in history. I showed that using a graph like the following, which is now brought up to the most current data:

With part of December now in the picture, you can see the faintest hint at the top of the steep late-November climb that shows the climb may be rounding off.

I noted,

That is a massive amount of new cash money — historically massive — done almost covertly in the quickest burst ever — and yet it did not even cause the stock market to blink!… The graphs … make it clear why inflation under the new regime could become a much more serious problem than the limp moves seen over all the years of the Great Recovery, the difference being how fast the Fed’s QE is now converting into cash

… and I asked,

Why did such an enormous surge in money supply happen in the last two weeks of November with no financial articles being written about it and no statements from the Fed about it? What is going on behind the scenes at the Fed and/or US treasury right now?

…and I promised I would look into and get back to you on it.

I think that I may have found a couple of answers, so I am getting back to you on that as promised.

This could be due to Biden’s promised termination of tax welfare to the rich

The first answer is my own surmising based on an article I just read about major tax-planning moves that are happening now in anticipation of Joe Biden’s promise finally to curtail the massive welfare to the rich that has gone on since the Reagan era (as the core of Reaganomics) in the form of that special tax cut they benefit from almost exclusively — the special capital-gains tax rate that is lower than tax on regular income.

As I’ve said many times on this site, the special cap-gains tax rate — more than any other cause — is why we have such huge growth in disparity between the rich and the rest. Capital gains are where the top 10% make most of their money — not in wages like the rest of the populace — yet they pay a much lower rate on that kind of income-earning than the much of the middle class pays on their kind of income.

Biden has promised he will end this obscene social welfare program that has been deepening the social divide in this nation for decades. That prospect has the top ten percent, and especially the one percent, scrambling for cover!

Rich Americans Who Fear Higher Taxes Hurry to Move Money Now

Rich Americans are rushing to make large transactions before the end of the month, trying to get ahead of any moves next year by President-elect Joe Biden and Democrats in Congress to raise taxes or close loopholes.

Some advisers say they’re busier than ever in the last weeks of 2020, especially with helping clients transfer wealth to the next generation tax-free while they still can. Appraisers, who are crucial for valuing assets used in these estate planning strategies, have been inundated….

It stands to reason that the richest of the rich and even just the regular rich are scared their overinflated lives will take a hit now that they see almost forty years of tax welfare possibly coming to an end. So, they are, like never before, scrambling to cover their asses — excuse me, convert their assets. The process of selling assets now while the gains realized on those assets can still be taxed at a much lower rate is bound to raise a lot of interim cash.

As I noted in my Patron Post, banks have been allowed to take money out of their reserve accounts as the Fed’s reserve ratio was dropped for COVID this year. That makes it easy for them to create more liquid cash to facilitate large financial transactions.

NewsMax notes that requests for property appraisals have quadrupled at one New York appraisal firm. Some of that, I would suggest, must be due to the new COVID migration. especially out of New York City. Some of it is due, according to NewsMax, to people selling investment properties in order to avoid higher capital-gains taxes down the road. The article notes that,

By late November, he had to start turning away clients. “We physically can’t handle all the year-end deadlines at this point,” Miller said. “We started doing this [turning away the overflow of clients] after the Thanksgiving holiday and it’s been extremely frustrating.”

Exactly the timing of the massive increase in the nation’s cash (M1) money supply.

The article notes that this rush into real-state sales, even after the COVID rush has surprised many advisors. Biden planned to restore a little balance to the budget by taking away this social welfare to the rich, but …

The results suggested Biden may have a difficult time fulfilling campaign promises to raise trillions of dollars in new revenue from the wealthy.

…but the rich are jumping ship in anticipation to avoid paying back some of the years of specially privileged tax cuts they almost exclusively have benefited from.

Naturally, the running of the rich is going to create some large temporary piles of cash as money moves from one kind of asset into whatever the rich are planning to do with all this money. (Maybe give it to their entitled children before estate taxes rise again — a major tax gift the aging Trump gave to his kids?)

The Biden administration could also try to close the many loopholes that make the U.S. estate and gift tax easy to avoid. “I can see a situation where Treasury issues regulations that make it more difficult to do effective estate planning….” The 2017 Republican tax law signed by President Donald Trump doubled the amount the wealthy could pass to heirs without paying the estate and gift tax…. The main reason for rich taxpayers to make moves by Dec. 31 is the threat that tax changes under Biden could be retroactive to the beginning of 2021.

The article also notes a big rise in the rate at which the rich are trying to sell businesses as assets as well as other investments. So, it is not just a move to sell expensive real estate … but any kind of asset on which they would see gains.

So, the rich are rushing to cash out. Though the article mentions nothing about the biggest rise in the nation’s history in supply of the most liquid forms of cash, I suspect the rush of the rich to cash out assets now has something to do with the rapid rise in cash balances. In that case, it may just be temporary, as other assets become purchased with the gains down the road.

There is reason to think some could remain in cash form. When the rich cash out, those that are charitably inclined send some of that cash to charities, especially now when tax deductions for such gifts can be applied 100% as an offset to income. That is money that often goes into operating accounts of thousands of different charitable institutions and so straight into the mainstream economy.

If it continues to be held in M1 cash form, then, being easier to spend and move down the road, it could create the kind of inflation I warned about where there is too much (cash) money chasing too few goods during a time of COVID shortages. We’ll have to remain vigilant to see. It is a matter of how the cash circulates.

Money creates price inflation where money circulates. If it stays in financial circles, there still will not be much inflation outside of financial circles; but if it goes in early gifts to rich kids, in lieu of inheritance to rich kids who profligately choose to spend it all on fancy vacations after COVID settles down and pretty toys, then it moves into the mainstream economy and can create high inflation if people start having more dollars than there are goods to buy in a time when the recent COVID scrooge has bogged down production and transportation.

It’s time to be vigilant.

It may also be time to forbear

Another article I read this week, dove into its own explanation for the rapid rise in cash, and it makes sense to me that this, too, is part of the reason, and it raises the same concerns about the prospects for hyperinflation:

The amount of dollars in checking accounts in the US banking system exploded by 25% from Nov. 16-30, the fastest rate in history, including the immediate post COVID-19 printing bonanza. The money, an unbelievable $1.3 trillion, came from savings accounts.

By “savings accounts,” the author must mean certificates of deposit and other term deposits, because ordinary savings are part of M1 (immediately liquid cash). I read another article that said money was moving from M2 to M1. That doesn’t make any sense because M2 is all forms of cash, including M1. So, money cannot move from M2 to M1 because M1 is part of M2. The difference is that M2 is simply broader so that it includes less liquid forms of cash, such as CDs, which you can cash out immediately, but on which you pay a small penalty if you do.

M2 is a broader money classification than M1 because it includes assets that are highly liquid but are not cash. A consumer or business typically doesn’t use savings deposits and other non-M1 components of M2 when making purchases or paying bills, but it could convert them to cash in relatively short order.

The author of this Seeking Alpha article also notes,

The transfer coincides with the expiration of most mortgage forbearance plans….

The author suggests the money is moving from savings (I believe he means term savings) to checking to start making way for sudden massive payments of rent and mortgage that have been postponed under forbearance. Forbearance was set to wind up at the end of the year, unless extended in a new COVID aid act.

As we just saw this week, it is no given such an extension will happen, though it seems ultimately likely the Federal government will not let people still in the throes of COVID unemployment that was forced upon them also be forced out of their homes … or forced to release all of their limited security to paying these backlogged payments off.

It appears Trump is deploying a “pocket veto” to the CARES Act 2, wherein no legislation is veto proof because the president can stop legislation from becoming law — without any possibility of a veto-override vote — by just not responding to it during the time of a congressional adjournment, as typically happens from now to New Years and then after New Years as congress closes for the next elected congress to begin. If the president “pockets” the legislations and doesn’t officially veto it for ten days while congress is adjourned, the legislation is automatically vetoed for good. (Just the way the constitution works.)

The point in this second article is that uncertainty about whether forbearance will be extended into 2021 may have some people scrambling to cash out any longer-term deposits they were retaining for security in such uncertain times in order to be ready to pay their back payments on mortgages and rent.

Could be. I don’t think the author proves the point, but it makes some plausible sense. That would also be a potential inflation problem as large amounts of the original CARES money may have gone into investments and term deposits, and those investments (per the first part of this article) and term deposits may be cashing out now. If forbearance is not continued, then that cash in the banks will all suddenly dump into the mainstream economy as it pays rents:

Checking deposits are used for payment, savings deposits for investment, suggesting more spending and less investment, meaning stagflation is about to pick up in a big way.

The author writes like someone who makes money buying and selling gold and concludes that holding gold is what you need to do. Maybe, but the stagflation he warns of is not a given. It will still depend on whether forbearance ends and whether rent and mortgage back payments are really why much more money is suddenly being held in its most liquid form.

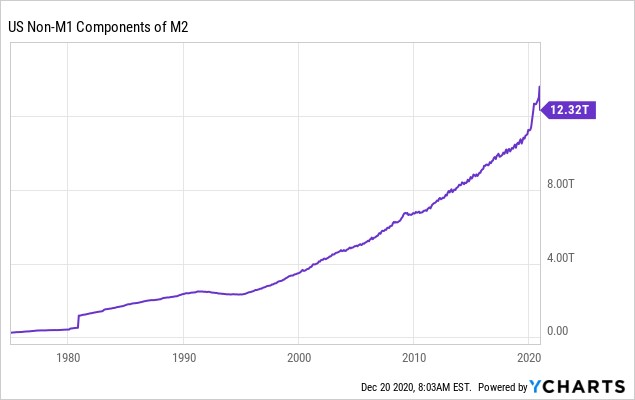

To prove that the increase in M1 money is coming out of term savings, the author posts this graph:

What I see in this graph is that the “non-M1” component of M2 (in other words the term savings component) shot up early in the year under the CARES Act and has now fallen by enough to account for the sudden rise in the M1 component. So, maybe he is right, but that does not establish whether the move is due to people preparing for the end of forbearance. It could be for any number of reasons. The basis for that reason is timing.

Notice the plunge at the end of the chart. We can see here that over the same two-week period, savings deposits contracted by about the same $1.3 trillion [as M1 rose by]…. An absolutely unprecedented amount of money is suddenly being vacuumed out of savings and into checking. The obvious question is why, and what are the implications?… For such a gargantuan amount of money to have been transferred from savings to checking in just two weeks likely means there are suddenly a whole lot of big bills coming due all at the same time.

From there, he goes on to make his conclusion that the timing means people are getting ready for the end of forbearance. He may be right, just as the timing may as easily indicate people are exchanging assets and freeing up cash to facilitate sudden December moves to get ready for tax changes. Either reason has rational plausibility, but we don’t know. It may be both.

No Conclusion

So, there you have it — two possible solid explanations for the sudden and historically massive rise in M1, the most liquid kind of cash. The good news, then, is that none of this huge move in money appears to be due to something breaking — a concern I expressed in my Patron Post — but it does mean the possibilities of high inflation that I finally started warning about this year, particularly in my Patron Posts, are something we need to watch out for because the COVID situation is much different than when banks were clearly and solely pumping money into assets. It will depend on what shores this tidal wave of cash now flows onto.

It also means Santa could have claws this year for stock investors, too, in lieu of his usual gift to stockholders IF stocks become some of the assets that are being sold off to realize gains now before any possible tax changes. (See “ Market AGAIN More Precariously Euphoric Than Any Time In History .” So, far the moves appear to be restricted to physical assets.

Keep an eye out for WHERE inflation is happening, and I will, too. We know it has been happening in housing and home construction materials. That, however, may just be a COVID migrational anomaly that proves short lived, given that the housing market took a huge drop in November after several months of huge rises.

I hope all of you, especially in this weird COVID year, will look for and find and give some Christmas cheer, in spite of everything.

*********

David Haggith publishes The Daily Doom and writes satire. The Daily Doom contains economic, social, and political news about our troubled times--a non partisan weekday collection of the most consequential stories about our complex times with insightful editorials and weekly economic analysis. As an equal-opportunity critic of America's sharply divided, two-ring political circus, David divides his satire into sister publications so you can pick the one you find agreeable and ignore her sassy sister.

Support David Haggith by subscribing on Substack.