An Uncertain Future

Prior to the presidential election, I expressed my concerns regarding how things would change should Biden be the winner. That of course came to pass. I have tried to keep my comments to a minimum until more is known of the changes that are to be made on his watch. Two things, one a trend and another a policy change, are now pointing to potential and real problems ahead for the US.

The US has – so far – been spared the new global peak in Covid infections, with India been hit especially hard. With summer on the doorstep, this good fortune should hold for the next few months at least. Much could still depend on the measures different states elect to use to contain the spread of the virus.

The trend problem is the way that Biden canceled and reversed most of the changes brought about during the Trump administration during the first few days and weeks of his presidency. He produced a spate of Executive Orders to dismantle much of what Trump had wrought, with an end to the construction of the Wall and a welcome to all migrants as a major change. Progress on the Keystone oil and gas pipeline was halted on 20 January almost before Biden could properly settle into the Oval Office. In doing so, he affirmed an Obama decision to revoke the permit for the pipeline on grounds of its presumed effect on climate change.

He is messing with Israel to the extent that Netanyahu hinted that Israel and Russia – who has new sanctions imposed – could live op to the saying that, “An enemy of my enemy is my friend.” South Korea is not happy with their relationship with the new US of A and have said they will follow their own path. By all accounts Biden has not been too popular with leaders in Europe and apparently has not been received there with the status of Leader of the Free World.

Canada can’t be too happy with his curtailment of the Keystone pipeline. Mexico too sits with a problem after the initial “open door” policy regarding migrants from the south changed in response the extent of the problems that developed at the border. Now Mexico has to deal with the migrants from further south that have dead-ended at the Wall – where construction might continue, in another reverse twist.

A new Big One is that Pres Biden during a virtual summit with 40 other world leaders will commit the US to cut climate emissions by half by 2030. He intends to make the announcement to begin the summit on Earth Day, to proclaim America’s resumption of global leadership on climate change and to urge other countries to make similar cuts. I wonder how this decision will be received by American industry and how many corporations will shelve the plans they have made during the Trump years to return their manufacturing base to the US, back from countries with cheaper labour.

This decision is also bound to reduce the prospects for new well-paid job opportunities for the large number of unemployed who have given up looking for jobs that either do not exist or for which they are not suitably qualified. This implies that the helicopters will keep flying to distribute ‘stimulus’ for the economy to out of work households. On the cards is a $1.9 trillion here and a $3 trillion there end before we know it, the pork gets loaded into the state and municipal budgets and the households get a pittance – or so it reads between the lines.

It is not only the Federal Government that are implementing measures that target US businesses and put workers out of work. In the LA region locally mandated increases in the pay of grocery workers in large stores – so-called “Hero pay” of almost half the minimum wage rate – have resulted in the closing of marginal grocery stores that are situated in economically depressed areas. Not only have these communities lost jobs, they also no langer have access to local shops for food and other groceries.

The examples of Russia and the USSR, China before their industrial revolution and Cuba amply illustrate that centrally managed economies do not work. Whenever the government dictates how aspects of the economy must be conducted and do so with little regards for the economic realities, it acts as a brake on the generation of wealth and economic growth and increases the amount of poverty in the country.

On the international front, it seems as if the US is set on increasing tension and losing friends and allies. New sanctions on Russia appear to play up to the beliefs that the Russians had aided Trump in the election. The Turks are upset because Biden has now made the 100 year old atrocities against the Armenians a new cause; India wants to know whether the US is a friend or merely a partner. They believe friends share like and like when times are tough, while a partner sticks to the terms of their contract, irrespective how much by doing so will cost the other partner.

The gist of this all is the new administration has created a climate in which socially commendable objectives are pursued to achieve near term political advantages. Yet these impromptu decisions have unintended negative consequences. At the Mexican border, the almost immediate problems resulted in a reversal of earlier decisions. It seems likely the same will happen when the consequences to other decisions also become unpalatable. The next year is going to be interesting, if painful at times.

An interesting week lies ahead for gold and specifically for silver. The big question, also discussed by David Morgan in an interview, listed in Midas, is whether a squeeze by the REDDIT groups on the May futures is likely to succeed. Last year, the 4 month bull market started in May; whether there is to be a repeat will be largely determined by what happens this coming week, in part by how many of the Comex options and contracts end up in the money and then standing for delivery. .

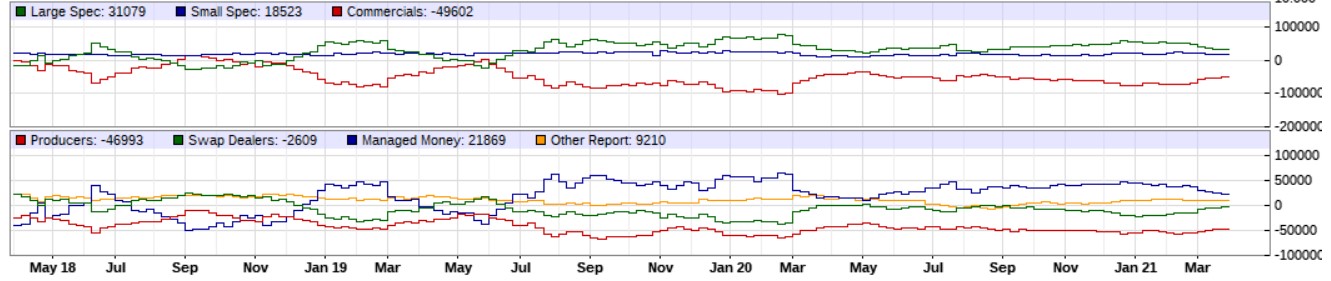

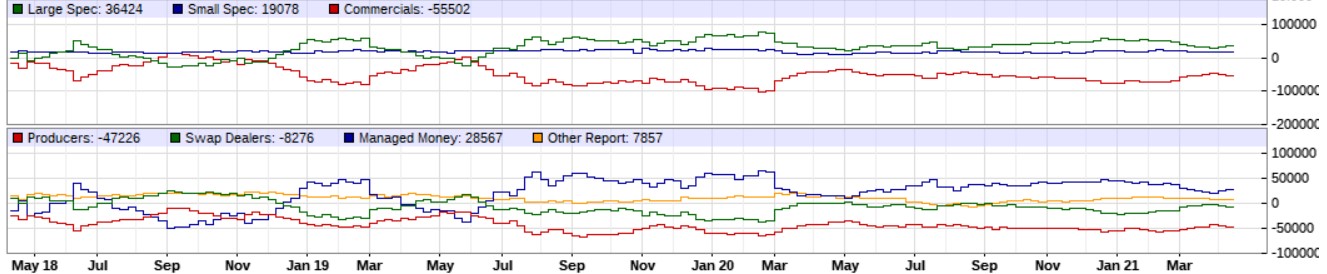

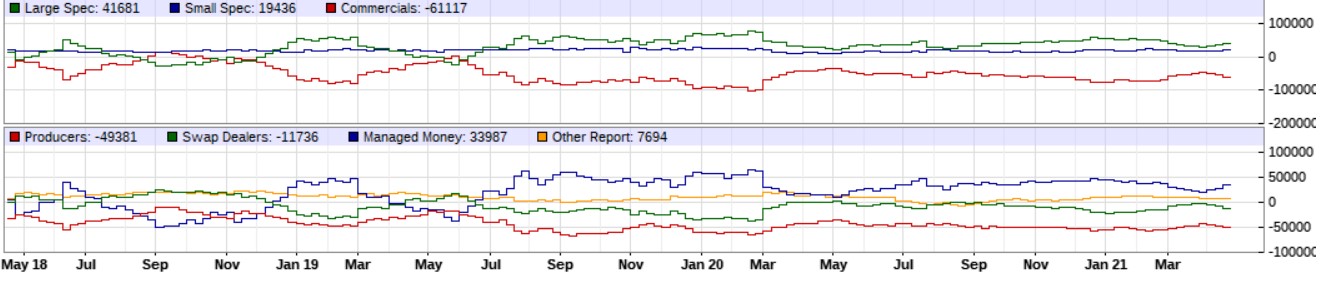

At the end of March, the prices of gold and silver were pushed to recent lows in order to limit the profitable April options and contracts, mostly for gold. This time the focus is more on silver, as May is a silver month. In previous issues we examined the ratio of commercial short positions against the large specs using the charts for silver below, ranked from older to more recent. The top chart is from 3 weeks ago, then from last week and lastly from Friday. Each chart consists of two parts: the upper half shows net positions for the Large Specs against the Commercials while the lower half splits short positions between producers (and the banks) and swap positions.

Initially, going into the end of March, the Large Specs went less net long as the price of silver declined, as the Commercials were hoping to happen for them to reduce their net short position. Then, as the price of silver began to recover, the Large Specs went more long again and the Commercial net short position increased again – a clear sign that the price was again being suppressed.

More recently, as the price of silver tried to hold above $26, these trends developed further – Large Specs more net long and the Commercials more short.

The question now is whether the Commercials have gained enough leverage in terms of recent longs that will be compelled to liquidate their positions when the silver price is pushed lower, perhaps even lower that it was at the end of March, near $24. They have to balance the gains of doing so against the risk of having new longs pile in at the lower price. Based on the above and the price back above $26, it is almost certain that there will be an attack as the week progresses, primarily aimed at the more than 56000 futures contracts still standing on Friday.

As mentioned previously, while May could see a further recovery in the prices of silver and gold, it should take a longer time for the squeeze at retail level and to take hold and spill over into contracts standing for delivery. May is nevertheless an interesting month, as can be seen by comparing the changes in the month of May on the above charts. There is a consisting narrowing of the difference between the net long and net short positions in May, as if the suppression of prices has the Large Specs tending to be less net long at this time, to result in the Commercials being less net short. Then, as summer takes hold, the Commercials do their seasonal buying so that the spread opens up again.

If that trend repeats this year, the month of May could again change the PM market.

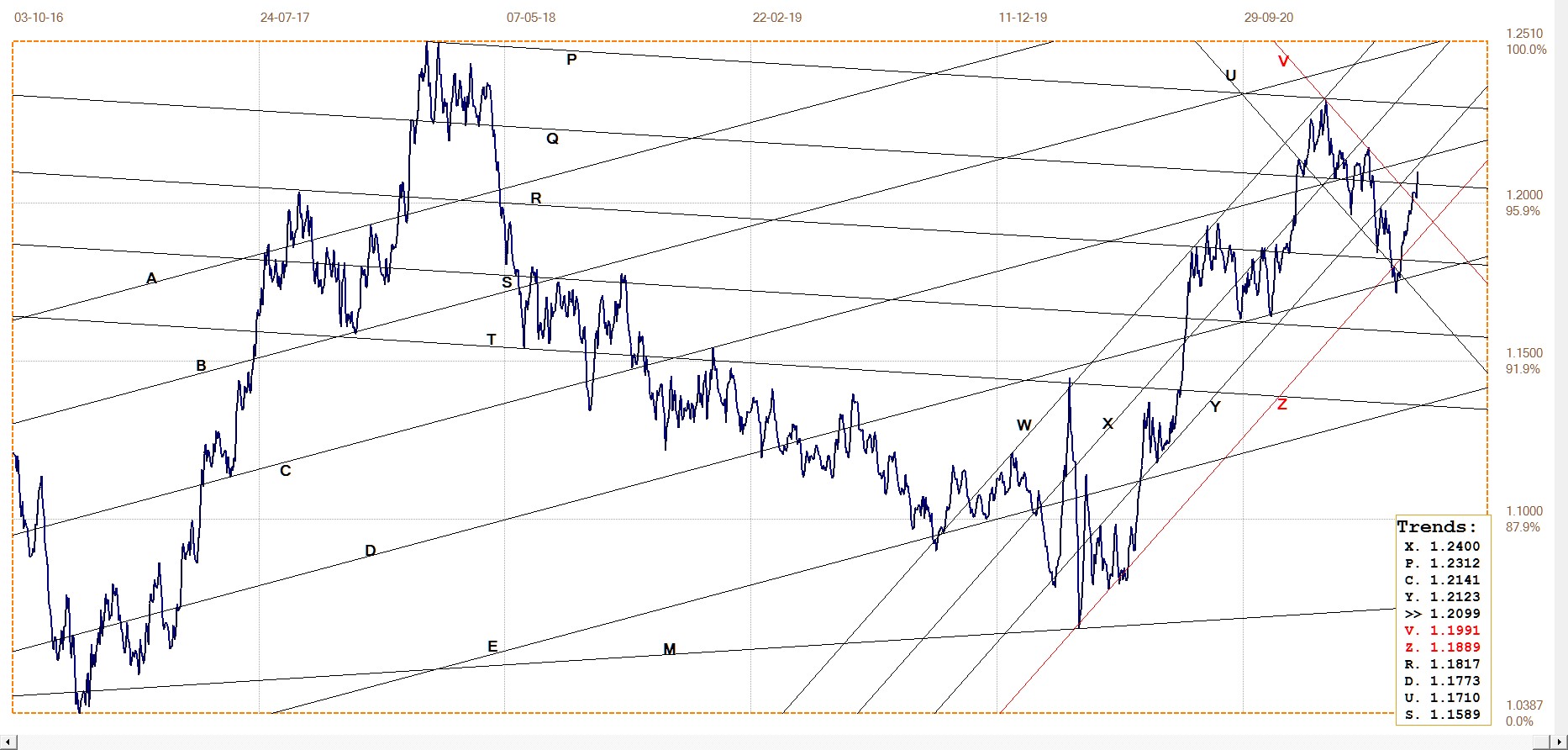

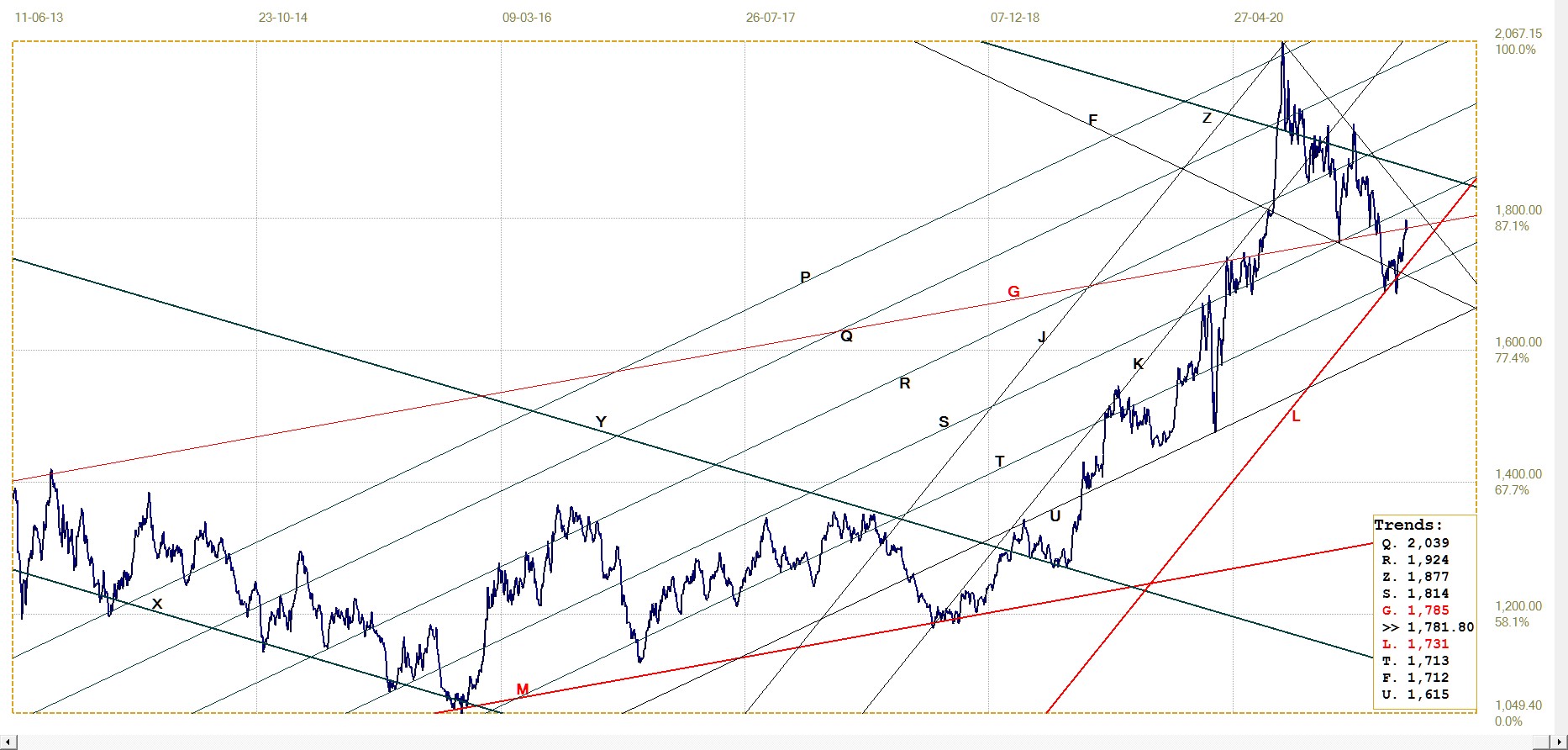

Euro–Dollar

Euro–dollar, last = $1.2099 (www.investing.com)

The recovery in the value of the euro continued last week. The extension to the rally has now broken above bear channel UV. Further dollar weakness could see the euro breaking into channels XY and BC to approach the recent high.

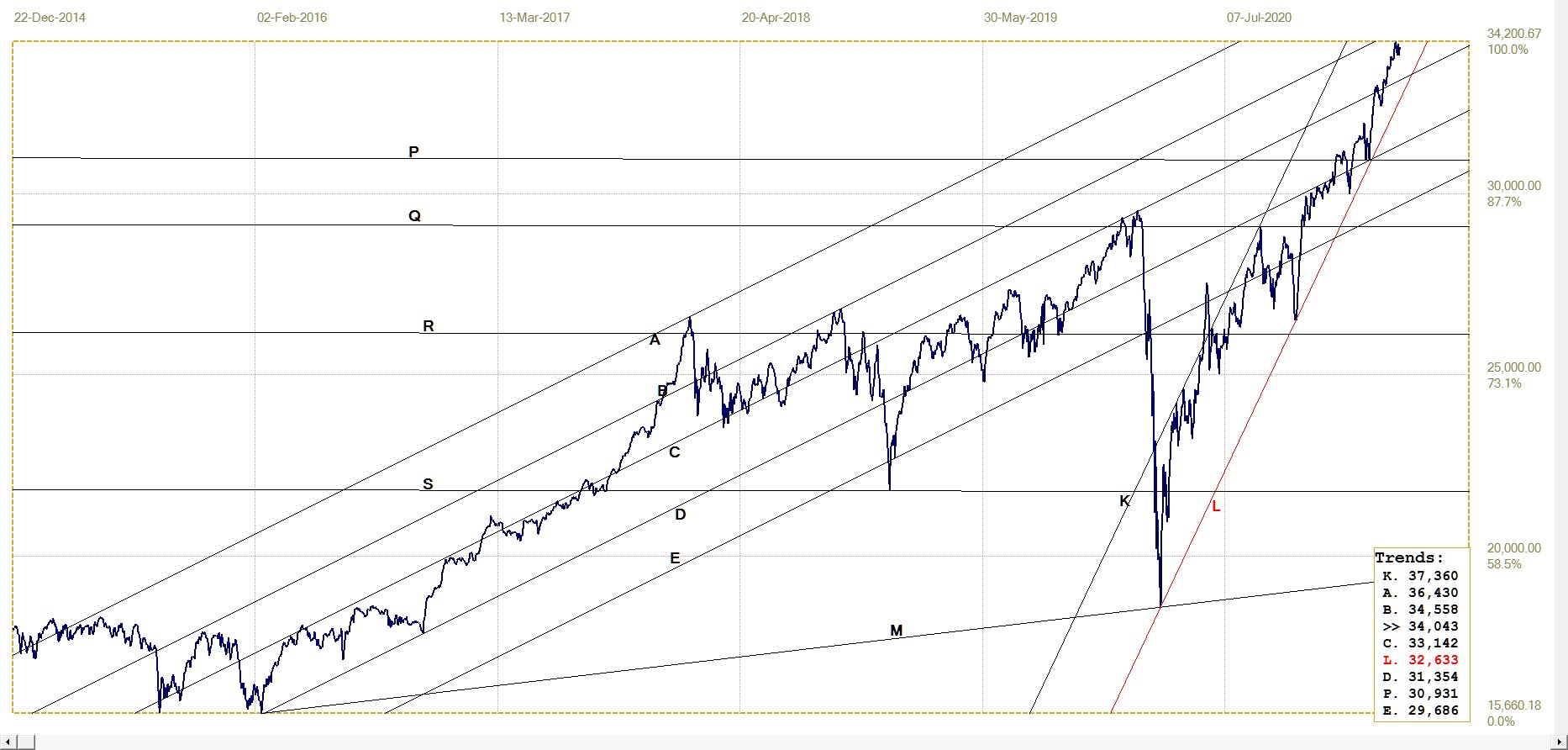

DJIA daily close

The DJIA has again entered a period of consolidation. During the past week or so, the market made substantial gains on one day, only to give back much of the previous gain or even more on the following day. With a PE around 30 on the S&P500 index, it is not clear whether the improving economy can be sustained to justify Wall Street’s very high valuation.

It is still too early for the summer doldrums to set is, but the more aware investors might be taking timely action to reduce their equity exposure. The next few weeks can be expected to show what the prospect for the summer will be.

DJIA. last = 34043.49 (money.cnn.com)

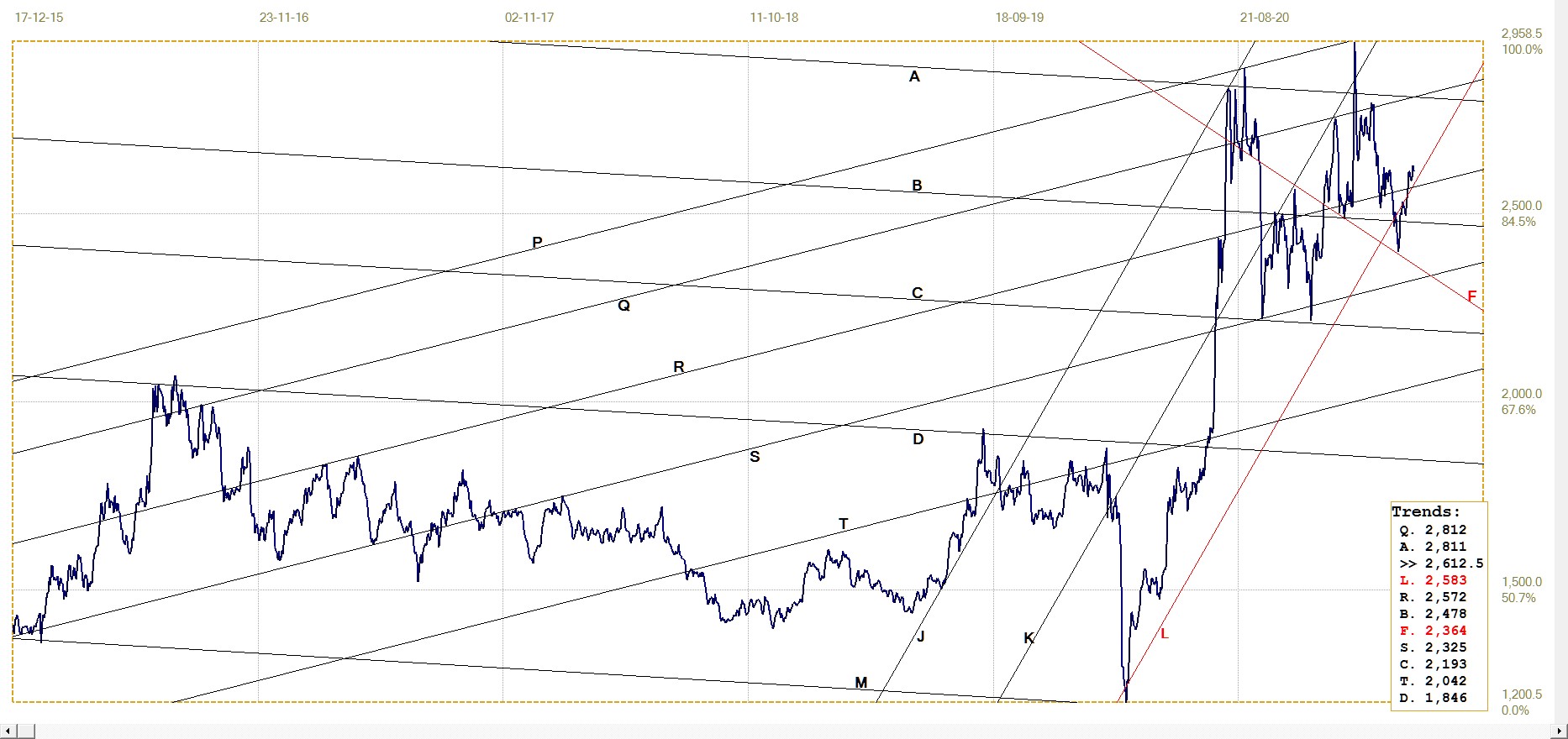

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1781.80 (www.kitco.com)

It required 21 months for the price of gold to move from the low in September at line M to break above the top of channel GM in early June last year. Last week, the price recovered from the steep panic sell off at the end of February by again breaking above the broad channel. The price again faces an new attack this week and the odds are the break higher will not be able to hold.

If so, what will be important is how long it will take to repeat the break higher. Based on last year’s performance, May should be a good month for gold – and will be a great deal better if by some miracles the support at line G manages to hold into May.

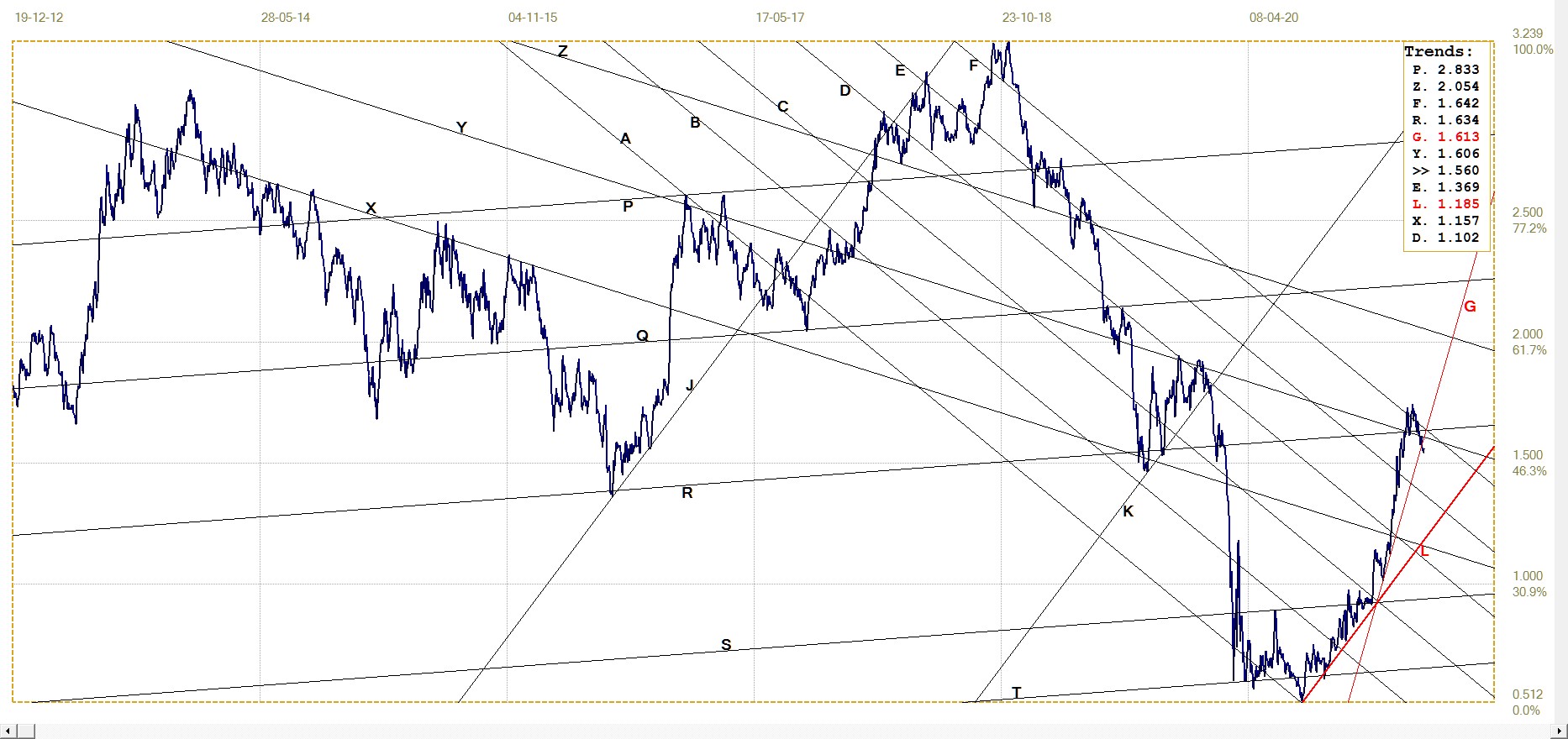

Euro–gold PM fix

Euro gold price – PM fix in Euro. Last = €1477.29 (www.kitco.com)

With April to end this week and Comex looming, the odds are that the euro price of gold will dip below main bull channel JKL for a third time and hopefully again only for a brief time. The same applies to lines G and X, where the price recently broke higher after a period of small daily gains, creeping higher along line L.

While it can be assumed that the price will not hold above these support levels during the week to come, if that actually should happen, a steep rise to reach the next level of resistance at line D can be expected.

Silver Daily London Fix

Ten days ago, the price of silver spiked higher from $25.585 to $26.14 in one day on the London silver fix, to break above channel SR and to hold in steep bull channel KL. Since then, the price has been battling to hold above $26, not always succeeding and also likely to drop lower during the coming week. Here too the odds favour a break below channel KL and line R, with a recovery to happen during the new month.

Silver daily London fix, last = $26.125 (www.kitco.com)

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 1.560% (www.investing.com )

There has been little change in the market for the 10-year Treasury note during the past week. The yield has drifted lower, but has still held mostly within bear channel KL and close to the top of the main bull channel AF.

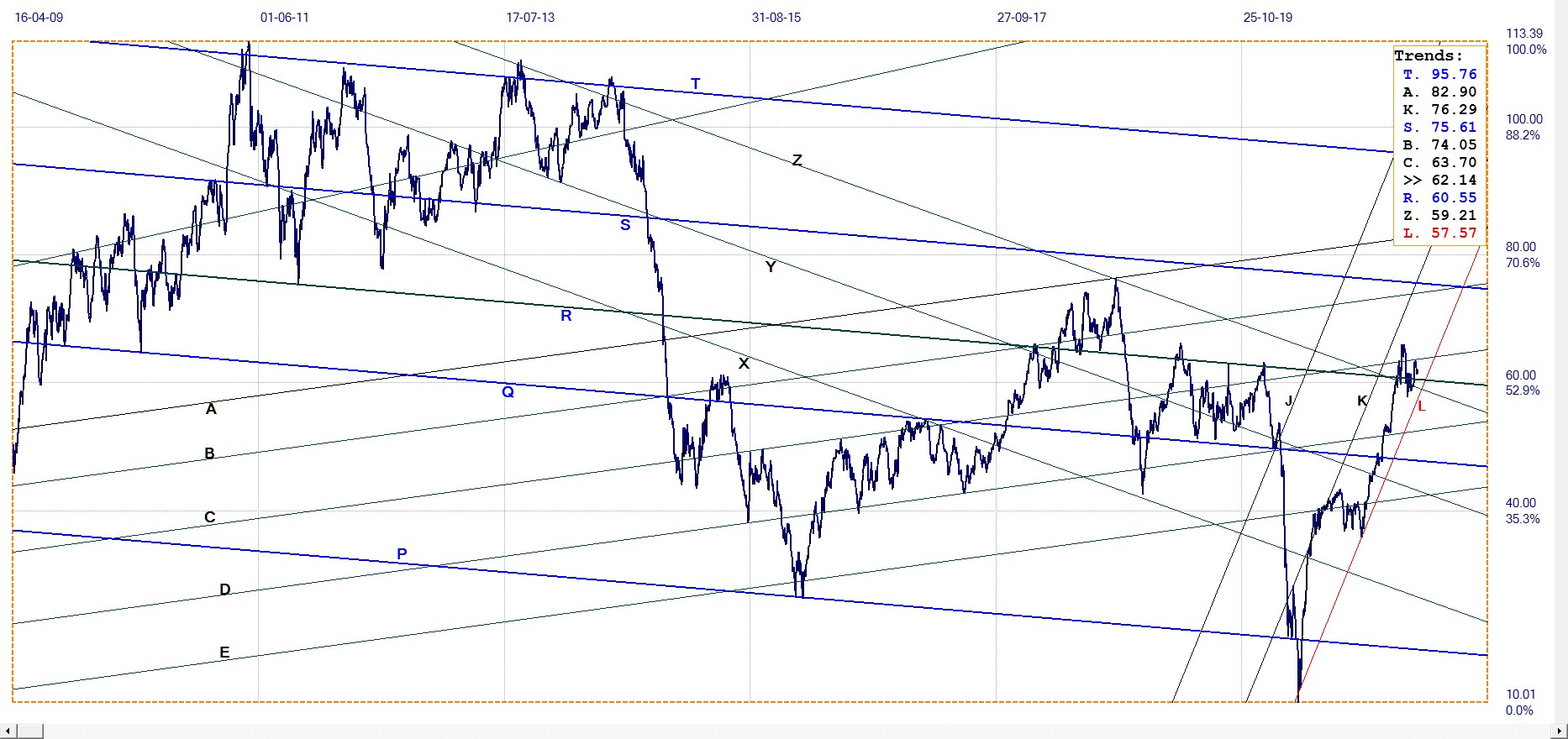

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $62.14 (www.investing.com )

After the minor break above main bear channel XYZ a few weeks ago, the price of crude is now still consolidating around the top of the bear channel, near lines R and Z. At the moment, the price is above these two lines, but holding below line C, which was briefly penetrated at the end of the main rally. The prospect of further price increases remain in place while channel KL holds.

********