The ‘Usual’ Persists

The ‘usual’, also called the ‘new normal’ is persisting despite some thoughts that the game rules will have changed now that September is the month. The DJIA is not allowed to decline below 18000 without some serious expenditure of effort – and, presumably, dollars – to bring about the umpteenth recovery out of the claws of the bear since 2011. On the other side of the playing field, gold and silver are not allowed to approach the important hurdles of $1350 and $21.00 respectively. Events of the past week make it very clear that it is Election Year; seeing that the Democratic standard bearer is battling her own shadows even more so than what Trump brings to bear. It seems all reserves have been pulled in to ensure success for the establishment – at least so far, but with less than two months to go.

A majority of Americans – those who believed that Bernie Sanders would have been on their side and most of those who support Trump – find it difficult to accept that the US economy is not in decline; that is their first hand experience. The promise that there is growth, that they too can enjoy its benefits as soon as the economy shifts up to the next gear, as it will do because Wall Street keeps on moving higher above 18000, might be all that stands between them and a vote of desperations for Trump to live up to his promises. The DJIA HAS to remain strong, as does the dollar and so too the bond market, even while some weakness sets in.

So far, too, gold and silver have not seen much of the promises that the month of September was supposed to realise. As mentioned last week, September could be a good month every year because of the long lead time to December delivery month. But the extremely heavy foot on the necks of the metals have not let up; it is as if the degree of desperation has become so intense that the normal breathing space in the fall is taboo this year. The metals are given no chance to achieve momentum in case there is a bullish breakaway. As is so often stated, it depends on supply of the actual metal to pull off successfully, but despite examples of shortages, there is still enough metal reserves available to the short sellers to keep on doing what they know so well how to do.

It is getting beyond monotonous, but that is what passes as markets in this era.

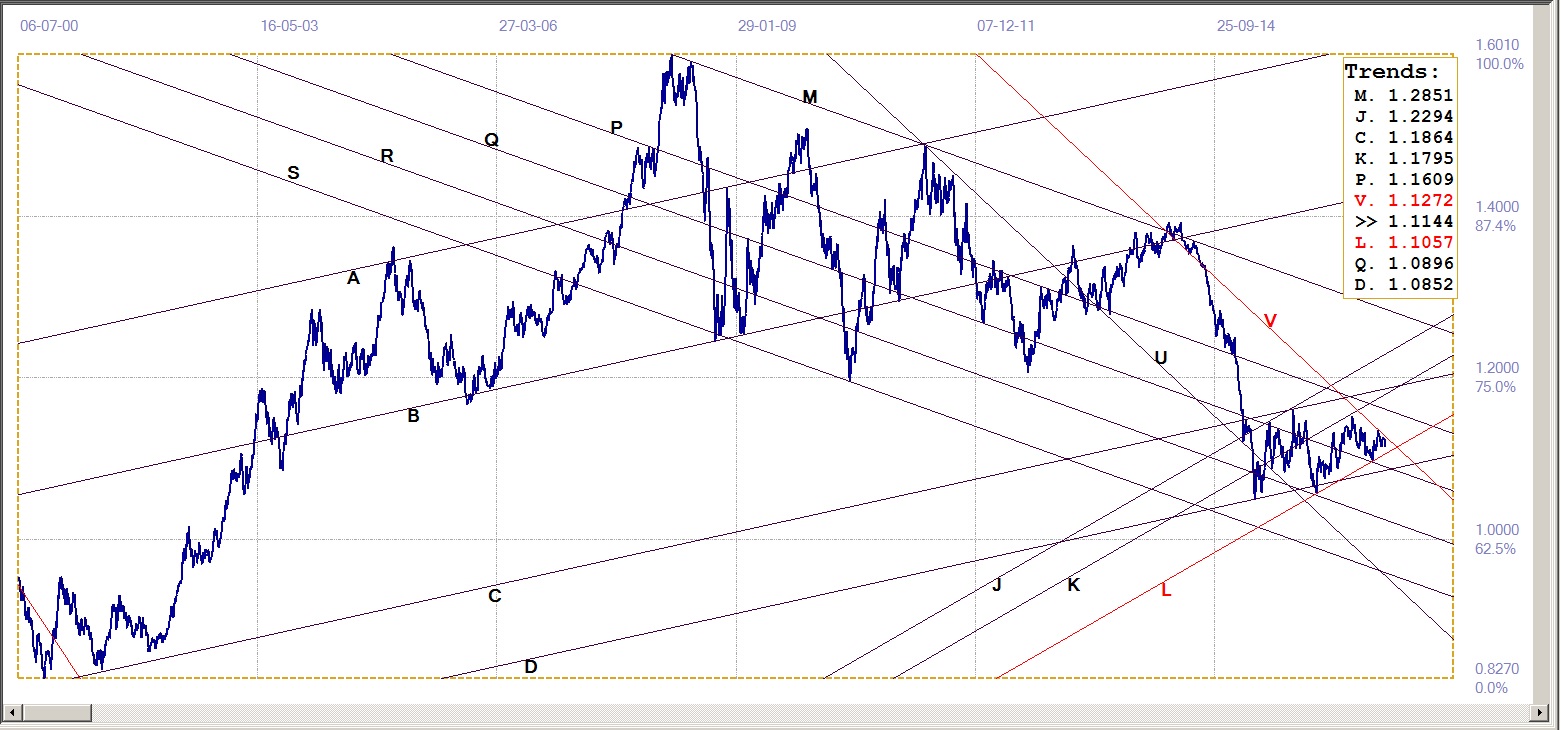

Euro-Dollar

Last week the comment was that given the post-summer season and that there was the steep rebound higher off support at line L ($1.1057), a break above channel UV ($1.1172) to resume the bull market rated a good probability. Given the new clamp down on the markets discussed in the introduction, this was not to be; resistance at the top of channel UV held form to contain the euro bear trend.

A test of the support at line L is not imminent, unless the weakness persist into this week; however, the room to move sideways without a break is disappearing fast and a break to show new direction during this week would not be a surprise – bearish?

Euro-dollar, last = $1.1144 (www.investing.com )

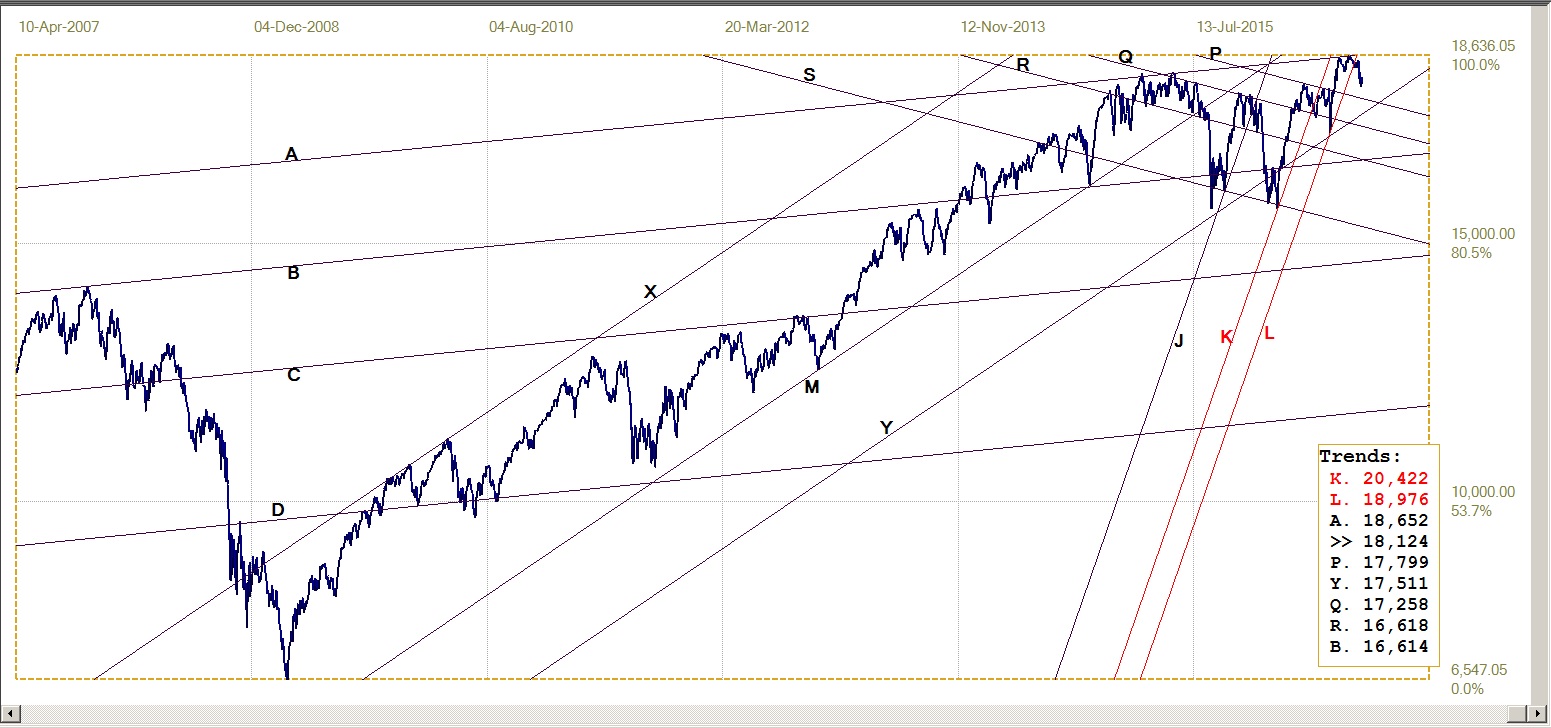

DJIA

DJIA, last = 18123.80 (money.cnn.com)

The steep move lower that followed the close double top along line A (18 652) did not extend, as was seen as a possibility last week. Instead, volatility picked up in some wild swings to and fro as the tussle between bulls and bears heated up. So far, it is a quite even match, with the bulls coming out slightly the better. If the buyers in a market have deep enough pockets and they are not very concerned about not finding the greater fool later to whom they can sell again, the bears cannot really set a direction for the market.

Sellers have a limited number of shares they can sell – those they own or that they can borrow to sell short. Buyers with no real limit to their available funds can keep on buying all the stock that gets dumped into the market and be ready for more. A bullish bias has to be the result. It probably is only when their buying can be clearly seen as intervention that they have to back off and, while many close watchers of Wall Street strongly suspect intervention, it is as yet not widely accepted. That may change and have an effect on the market direction, such as when the DJIA breaks cleanly below 18000.

Gold PM Fix - Dollars

Gold Price – London PM fix, last = $1308.35 (www.kitco.com )

Friday’s PM fix of $1308.35 broke marginally below bull channel KL ($1327) and was thus an early sign of weakness. However, the fix was also the new leg of a very small and near term double bottom. We should know quite soon this week whether the price will recover off the small double bottom or extend the break lower. Should there be a bounce, it would not necessarily mean a recovery into steep bull channel KL as it already sits at $1327 for the Monday PM fix.

The number of waterfall attacks last week and the fact that all rallies soon run into strong selling make it clear that the price suppression this time is continuing into what in most years is the best month of the year for gold. Half of the month is over and gold has gone nowhere. Time is running out to conform the statistics!

Gold PM Fix – Euro-Gold

The euro price of gold at first held sideways to bullish after testing support at line W (€1177), because the price of gold held up better that the euro against a firm dollar – at least until Friday. The low gold PM fix that broke below its bull channel, despite a weaker euro, also had the euro price below support at line W. The euro price fell to just short of key support at the bottom of its bull channel KL (€1165).

If the euro price bull channel can hold, perhaps with a gold price bounce off its new double bottom, this might put a positive slant on gold for the rest of September. It would then however not be because of a general dollar weakness that favours both the euro and the gold price, but because of a stronger performance from gold itself. It is the gold price that has to drag the euro price higher – not a weaker dollar that like the tide raises all ships.

Euro Gold Price – PM fix in Euro, last = €1170.8 (www.kitco.com)

Silver Daily Fix Chart

Silver daily fix, last = $18.91 (www.kitco.com )

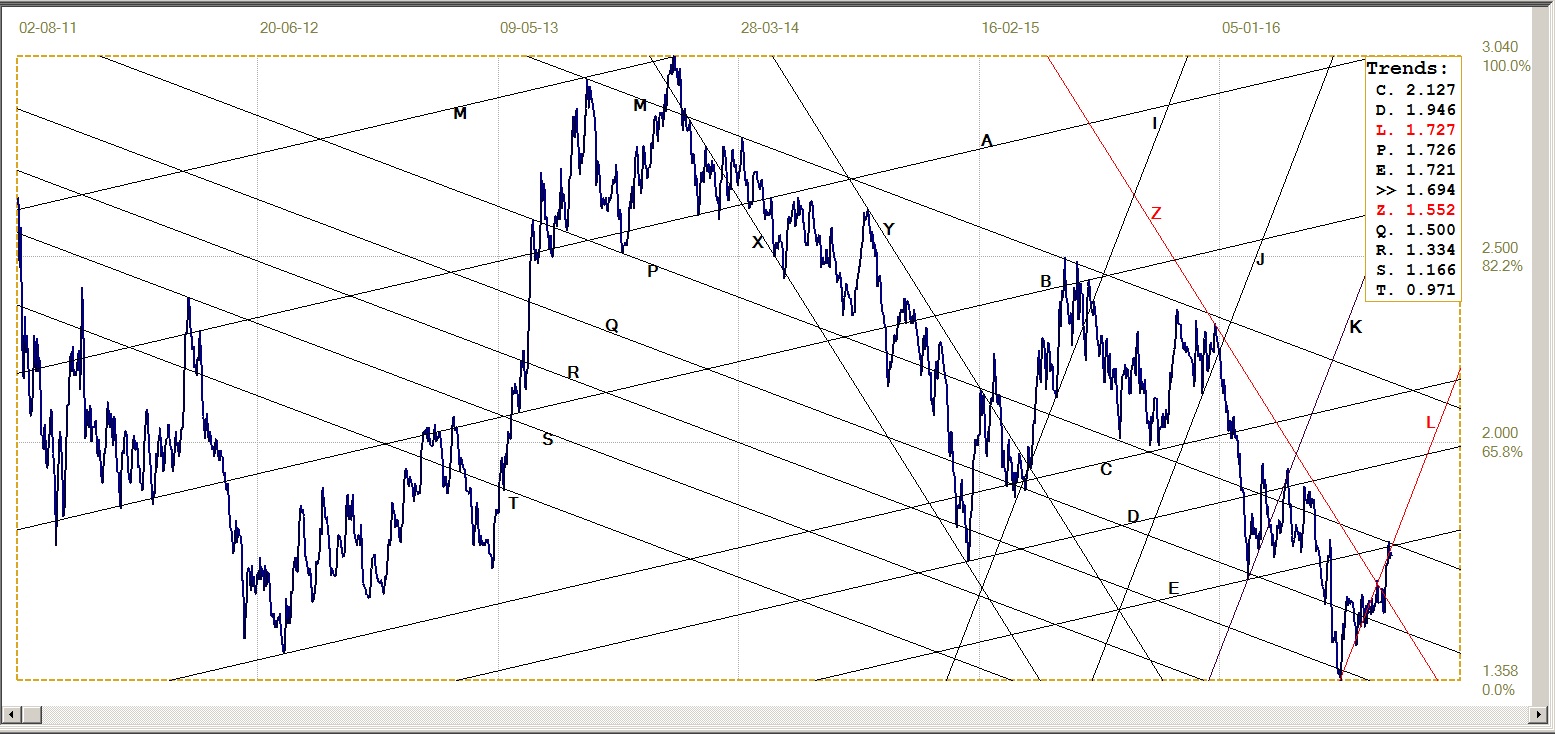

US 10-Year Treasury Note

US 10-Year Treasury Note, last = 1.694% (www.investing.com )

Brexit started a rally in the US 10-year Treasury not that by July 8 reached an all time low yield of 1.358% - but for only one day. Whoever sold heavily on that day ye reverse the trend and send it back up to 1.513% two days later, smiled all the way to the bank! After that date, the trend remained quite volatile, but still with the bearish trend – until support at the top of bull channel YZ (1.552%) halted the slide to keep the yield close to the 1.6% level, while breaking clear below the steep bear channel KL (1.727%).

That support triggered a new rally that soon had the yield back down at 1.539%. It did not last and a new sell-off broke clear above bull channel YZ to rise higher while keeping mostly along line L. Then support at lines E (1.721%) and P (1.726%) has kicked in to halt the slide. Things are steady while the support holds, but a break to above these two lines and perhaps back into channel KL would look very bearish.

The bond market is also critical to the success of attempting to paint lipstick on the economy. While a bear correction in the bond market traditionally is associated with a rally on Wall Street, this link was not constant for much or most of 2016. This is when too many investors see no safety in the asset markets and either go to cash or escape to another currency. That has a bearish effect on the dollar; when both the bond market and the dollar are weak, it makes all foreign holders of Treasuries very nervous – a condition the US tries to avoid at all costs. Some interesting times ahead in these markets!

West Texas Intermediate Crude. Daily close

The effort some weeks ago to hold above the new support at line D ($47.04), failed to hold. The price of crude fell steeply and bottomed ten days ago just short of the steep support at line L ($40.25) to rebound higher. That rally broke back above the new resistance at line D, but for only one day, before falling again as steeply as two weeks ago.

This time the price reached a new low at $43.03 on Friday, right at rising support of line G ($42.98).These volatile weekly swings in both directions, suggest that there is either violent difference of opinion on the proper direction for the market, driven by news that is constantly changing in context – or there is intervention to prop up the market in opposition to the bearish market trend.

Of course, if the latter happens to be true, then rapidly changing news could also contribute to the volatility; strong intervention forces will use all means to sway the opinion of interested parties, including the media. If so, misinformation on the state and prospects of the market could be counter-productive if drillers and/or the banks were to make incorrect decisions based on such information.

The link between the price of crude and what happened on Wall Street some time ago was strong enough to be widely commented on in the financial media. This link has broken down for a while, but trying to get crude bullish might again seem to be a good card to play to ensure that the DJIA remain above 18 000. So far, though, without lasting success in resurrecting the crude bull.

WTI Crude – Daily close, last = $43.03 (www.investing.com )

©2016 daan joubert, Rights Reserved

chartsym (at) gmail(dot)com