Basel lll And Gold

“Basel lll is an internationally agreed set of measures developed by the Basel Committee on Banking Supervision in response to the financial crisis of 2007-09. Like all Basel Committee standards, Basel lll standards are minimum requirements which apply to internationally active banks.” https://www.bis.org/bcbs/basel3.htm

It is anticipated to reduce or even stop the suppression of prices of gold and silver.

What happened in the US banking system over the period 2006 to 2009 came close to wreaking havoc in the global banking system. Two of the more significant features of the development of that crisis, from the perspective of the BIS (Bank of International Settlements) are the disregard for conservative accounting practices when it came to the issuance of mortgages on private property; secondly, the creation of investment vehicles, based on mortgages on homes. These were then sold to fund managers of all kinds, but, when the mortgages were not serviced, these investments fell miserably short of the thumb-suck ratings assigned to them by the rating agencies. All of this made the BIS very sensitive to anything that could precipitate a new banking crisis.

The crisis exploded in the US in 2006/7. However, the seeds for what then happened were sown in the late 1990s during two Clinton administrations – the same time when the official CPI as measure of inflation and de facto CoL index was changed to signal lower inflation. In his effort to ensure his re-election, Clinton went over-board with no regard for the longer term consequences of the changes to boost the economy.

The CPI change resulted in more optimistic numbers for the GDP, which suited Clinton fine. Lowering or eradicating trade barriers, cancelling the restrictions on banks that were instituted after the 1929 Crash boosted the banking system, and lowering tight requirements when buying a house also helped to get the economy going. Imports from countries with a lower cost structure assisted the new CPI to keep inflation low. Finally, the rapid growth in IT was Clinton’s windfall bonus that could help him claim that he had balanced the budget – with silent assistance from Social Security funds.

This period also saw a change in the overall zeitgeist of the US. A “Can do” mentality resulting from WWII and massive growth in the manufacturing sector which gave US workers of the 70s the best relative standard of living in history, faded during the 1990s, to be replaced by a feeling of “We have done it.” When the Iron Curtain rusted through to leave the US the sole global force, Clinton took personal advantage of the changes with a promise of greater prosperity for all and was re-elected.

Today we know that his promise was a pipe dream; the changes he brought about have helped the US become a country with massive real unemployment and much greater inequality than at any time since the 1800s. Clinton revoked Glass-Steagal which resulted in the “Too Big to Fail” banks and their role in precipitating the 2007 crisis. If the Fed had not stepped in with trillions of dollars in March 2009, the global financial system might have resembled a set of falling dominoes.

It has taken all of 12 years for the experts at the BIS to finalise new rules to ensure that international banks can be expected to survive any new crisis that might develop. The main thrust of the rules is to reduce potential credit risk for the banks, i.e. to ensure the banks will be able to survive events that pose a threat to their survival.

These new rules will go in effect in Europe on Monday and in the US on 1 July. The UK will follow at the end of the year. One aspect of the Basel LLL rules that have attracted quite a bit of dissent from Commercials, is a new rule on gold ownership by the banks.

The BIS is fully aware of the suppression of the prices of gold – and silver – and it is presumed it also participated in this. They are aware of the degree of risk to some Banks due to their short positions and what this could mean for the financial system. They are certain to realise, given heightened tensions between countries and their relative gold holdings, that gold could be weaponised and used in an attack on the integrity of the big bullion banks. It seems from the clause 96 below that this risk must be defused to achieve the goals of Basel LLL on the integrity of the big banks.

The clauses 95 and 96 in the new rules state, 95. The standard risk weight for all other assets will be 100%, with the exception of exposures mentioned in paragraphs 96 and 97.

96. A 0% risk weight will apply to (i) cash owned and held at the bank or in transit; and (ii) gold bullion held at the bank or held in another bank on an allocated basis, to the extent the gold bullion assets are backed by gold bullion liabilities.

After special groups of assets are discussed in preceding clauses, the risk weight of the bank’s ‘other’ assets is set to 100% in clause 95. This implies that if any of the ‘other’ assets lose 100% of its value, the bank should still be able to survive because it must have collateral for the full value of that asset. Excluded here is cash that is owned by the bank or in transit. Cash that is owned poses no default risk and has a 0% risk weight; cash therefore requires no other assets to stand as security.

Also with a 0% risk weight is gold that is owned by the bank and held at the bank or at another secure place, but then only when clearly identified as allocated to the bank. Any gold liabilities to which the bank is subject have to be subtracted from the gold owned by the bank – only the remainder of the bank’s gold that is owned in the clear with no liability has a 0% risk weight, else the gold also has a 100% risk weight.

It is widely accepted the large short positions carried by the Big Banks through their participation on the Comex futures exchange are effectively naked shorts. I also do not know whether they have an effective ‘no limits’ dispensation from Comex, either in their own right or as proxies for government. Alternatively, they might claim that they have off-setting long positions of some kind at the LBMA (which then leaves the LBMA with a large naked short position over and above the gold it actually owns. It would be a cynical joke if the LBMA then report to their regulator that their shorts are protected by unallocated long positions they own at the US banks!!)

Whichever is true, if either, the fact is that if the Big Banks had their short positions covered, we would not have seen the panic reactions in March last year when Covid hit, or in February/March this year when the REDDIT Apes started squeezing silver. Or right now as Basel lll threatens. On this evidence they do have a serious problem.

For the time being, after Basel lll takes effect, there is no immediate or increased risk – except to the bottom line. Having to carry 100% cover for all the unallocated gold on their books means that a disproportionate amount of their assets remain tied up as security. Secondly, they only obtain a 0% risk weight on unencumbered gold they own or have been allocated, which is likely to be much less than what they have at risk.

The number of open gold contracts on Comex for the Commercials is 202 382. At 100oz each, this represents more than 20 million ounces of gold, or more than $36 billion, with gold at $1800/oz. If all of these were to be viewed as potential liabilities to the Commercials except as offset by owned or allocated gold, their short positions will make a major hole in their available assets. Even if actual liabilities are confined to only the active July contract, this will make little real difference since the July OI is greater than 75% of the total gold OI. These positions now become a heavy financial burden to carry.

It is reasonably credible that clause 96 on how gold is only counted as a 0% risk free asset, like cash, when fully owned with no gold liabilities, was motivated by the large risk posed by the volume of contracts sold short on Comex and probably in the OTC market. It therefore seems near certain that the banks will pay a heavy price should they persist in carrying these large short positions that they no longer can off-set with long positions in other paper gold.

The BIS is concerned with gold specifically as a monetary metal and it seems Basel lll is not concerned with a similar situation in silver. However, various regional regulators pose stress tests to evaluate the soundness of their banks. It is conceivable in light of the concern of the BIS with respect to gold that the stress tests soon might have very similar constraints for large uncovered short positions in silver. Should similar changes be introduced in these stress tests, the situation for the banks involved in suppression of prices will become even more expensive. The profits they make from this practice, if any, will then no longer be as attractive.

So far, the behaviour of the Big Banks has shown little sign of increasing concern; yet they continue to lean on the prices of gold and silver, to keep the price of gold below $1800 and silver close to $26. The intention seems two-fold: to maximise the number of options and contracts that do not expire in the money; secondly, to induce as many longs as possible to close their positions. Another objective will be to induce the black boxes of the hedge funds to switch positions from long to short. So far, the successes they have had are likely to be far less than what they had hoped would happen.

Once Basel lll kicks in, the Cartel banks must juggle what they stand to lose because of the change in risk weights against what it would cost to reduce their short positions – the later either by more stringent suppression of the gold price or eventually, when the situation deteriorates enough to warrant it, by becoming buyers of contracts in the open market. This of course will propel prices steeply higher.

It has been hinted at times that the OTC PM market is larger than the Comex futures exchange, which implies that what one sees on Comex is only what is visible above the water, as in the case of an iceberg. Of course, this will only apply to ongoing OTC contracts that were entered into without taking the effects of Basel lll into account. If there happen to be such contracts, the banks will pay for their negligence.

It would be optimistic to expect that there will be significant changes in the PM market taking place on July 1. The banks surely will not want to reveal that they are forced to react on the new constraints; doing so could trigger a buying frenzy as gold bulls and other investors open new positions in anticipation of a free PM market. Yet, should the above analysis point to rather severe problems for the banks, they cannot afford to wait too long before acting to protect their interests. 2h ? of 2021 will be interesting.

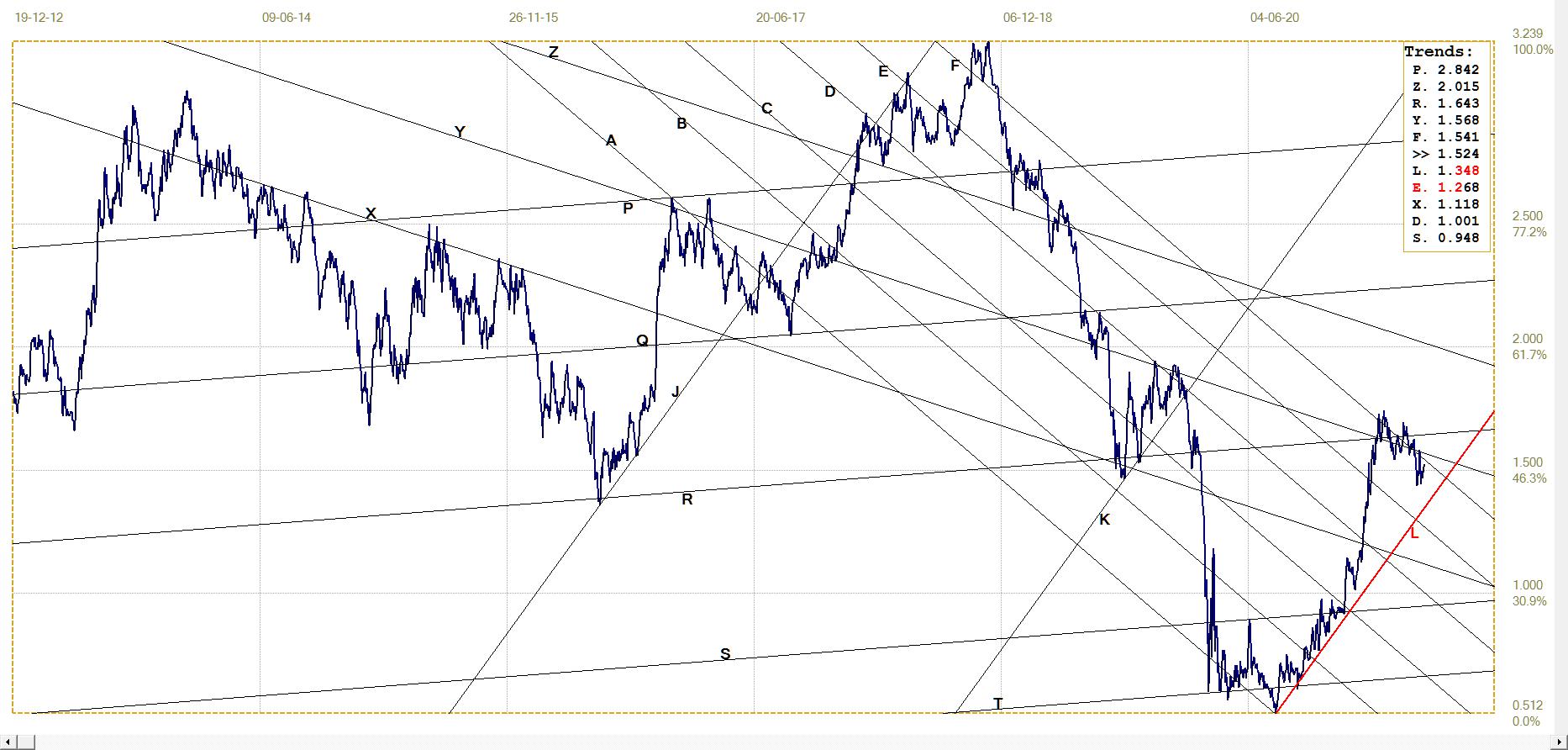

Euro–Dollar

Euro–dollar, last = $1.1933 (www.investing.com)

The third reversal practically at line R implies that the shallower gradient of the new bull channel is more appropriate than the earlier steeper channel. There is much talk of the volume of dollars being printed that is to trigger increased dollar weakness in due course. Should the euro hold above line R and manage to break into channel BC and hold, this would warn of further dollar weakness to come.

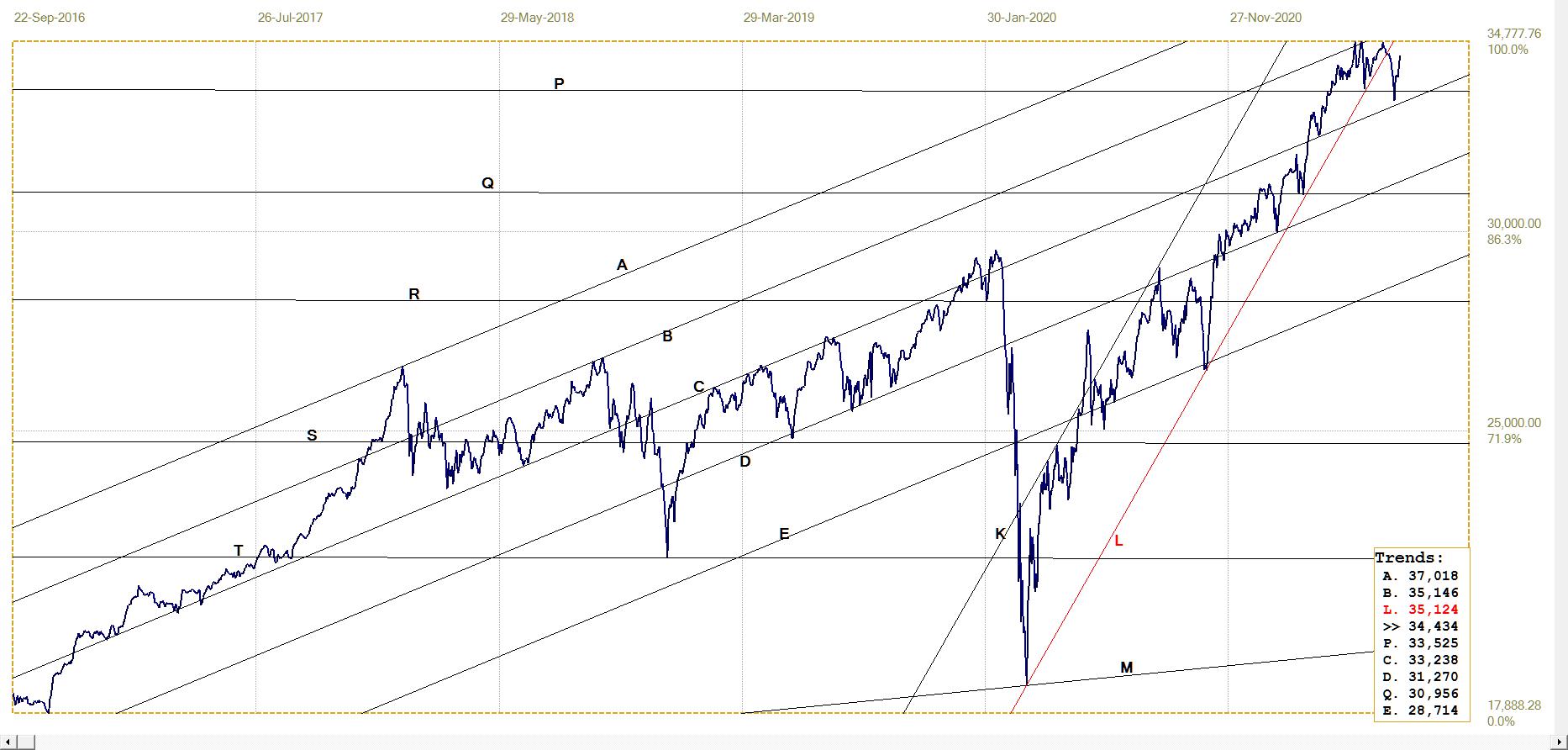

DJIA daily close

DJIA. last = 34433.84 (money.cnn.com)

While the DJIA is still struggling to reach a new all time high, the S&P500 and the Nasdaq set new all-time highs on Friday. This means the attention of investors and speculators has drifted away from the Dow 30 to hunt for better prospects among the second tier and technical stocks.

Long term technical indications are that the S&P500 on Friday hit a major resistance level. If the DJIA fails this week to challenge the near triple top that is in place and the S&P500 reverses lower, the timing might be right for the long anticipated bear market to begin. Should Wall Street really begin a bear trend, the liquidity that will be released when selling of stocks increases, ought to seek a home in the cryptos and in gold and silver – perhaps not from week 1, but not too long after the Bear finally has taken over.

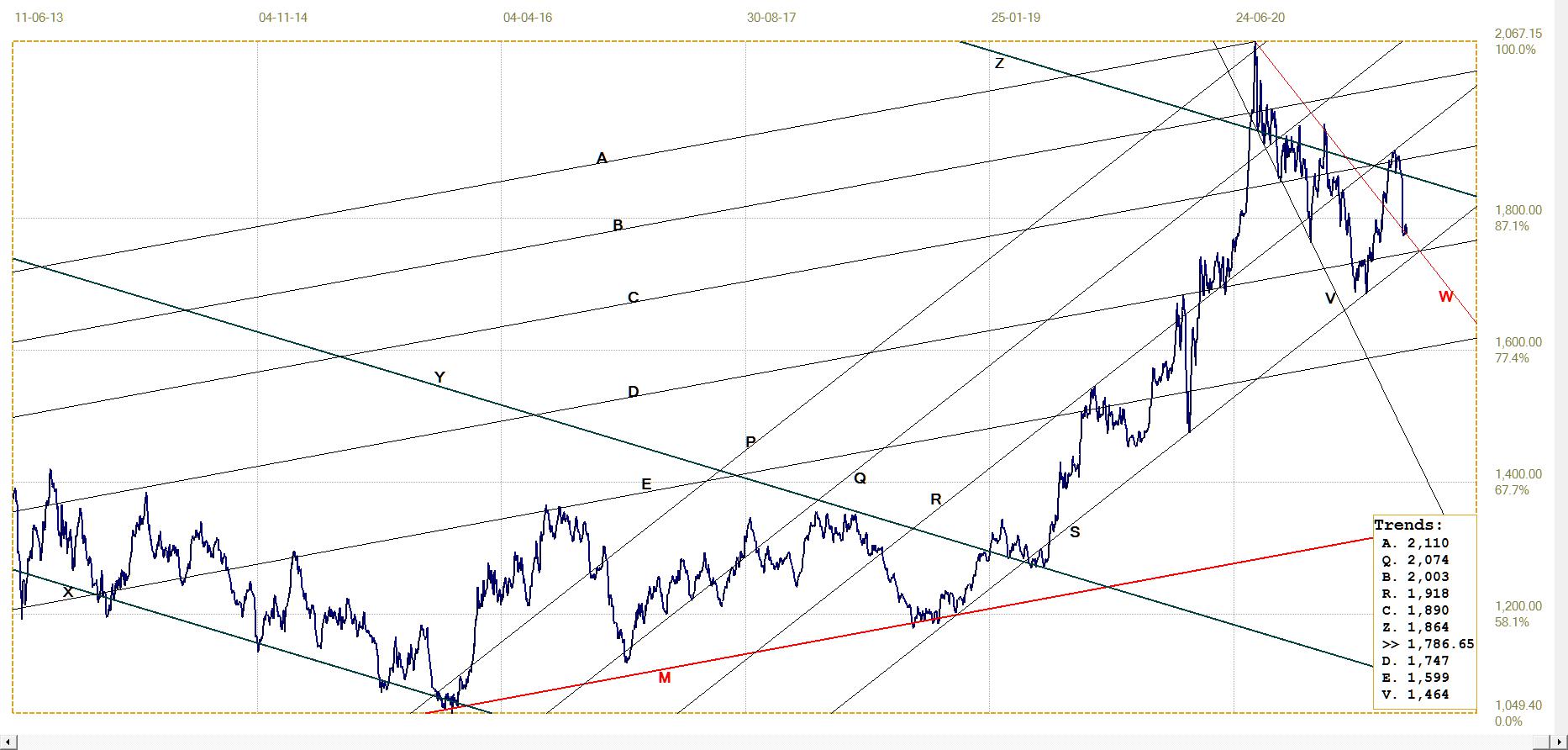

Gold London PM fix – Dollars

During early June, after having protected their profit in the June options and futures, the Cartel relieved pressure on the price of gold, rather surprisingly allowing it to close in on the $1900 level. Then, as if realising their mistake, the price was attacked again to take it back down to support at line W, top of the very steep megaphone VW.

The price is still holding in bull channel RS, with the key resistance now again at line Z after having failed to hold the recent break higher. The outlook remains bullish while holding in channel RS and above line W, but the analysis fails to anticipate a recovery soon. At the moment there is too much scope for a sideways move in channel RS.

Gold price – London PM fix, last = $1786.65 (www.kitco.com)

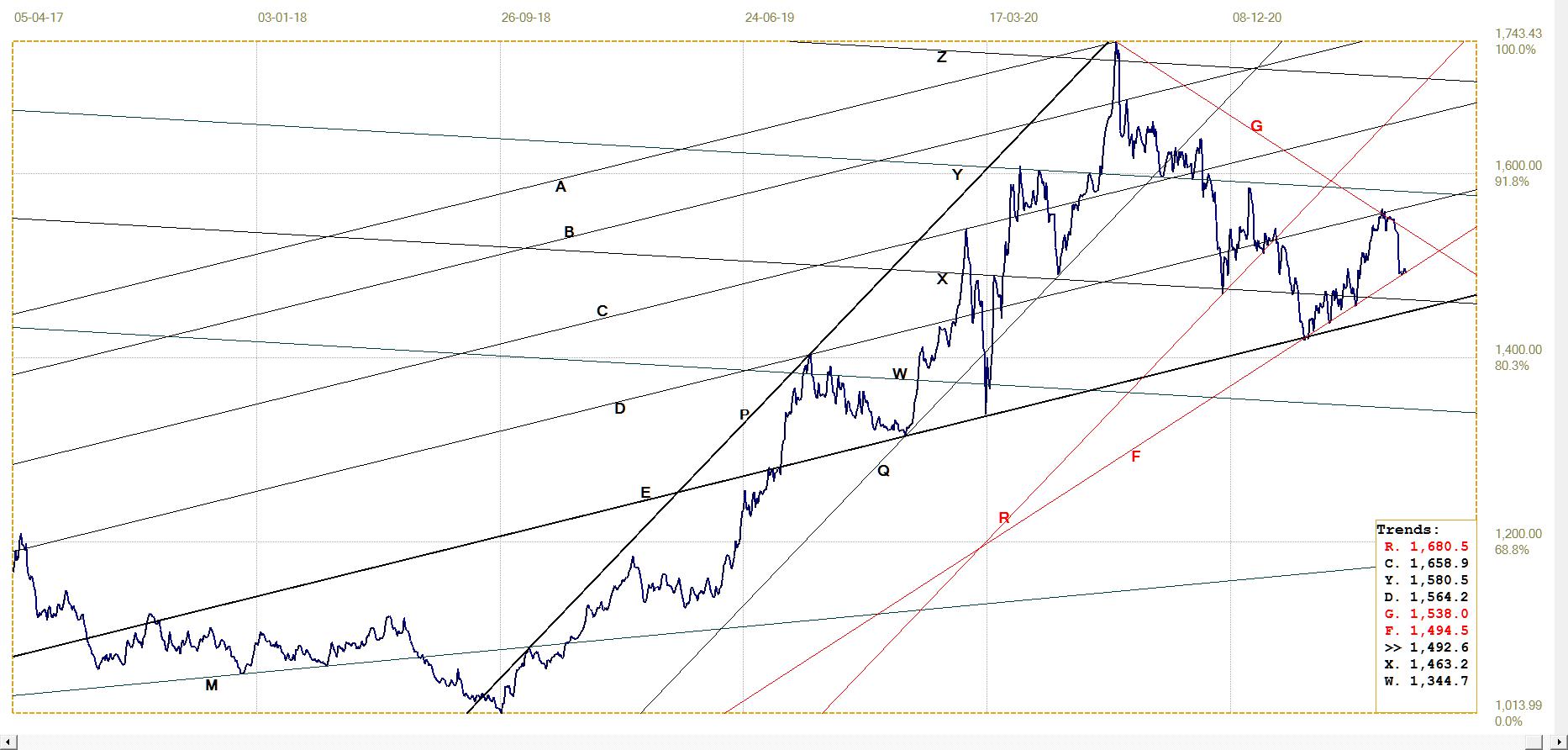

Euro–gold PM fix

The recent euro weakness was not enough to overcome the weakness in the price of gold to result in an improving euro price of gold – at least not until the euro price held at the line F to barely hold at the new support last week. The euro itself rebounded off support, as shown earlier. If that bounce is due to continue this week, the dollar price of gold now has to improve with a rebound off line W in order to hold the euro price above its support at line F.

If the current support is to hold for the euro and the euro price of gold, the implication is that while the euro is to be steady to firm against a weaker dollar, the price of gold has to improve its intrinsic value by more than only a mild response to a weak dollar. The futures July expiration will soon be over and perhaps that will enable gold to rally a little on its own strength as the week progresses until NFP day, and perhaps later.

Euro gold price – PM fix in Euro. Last = €1492.57 (www.kitco.com)

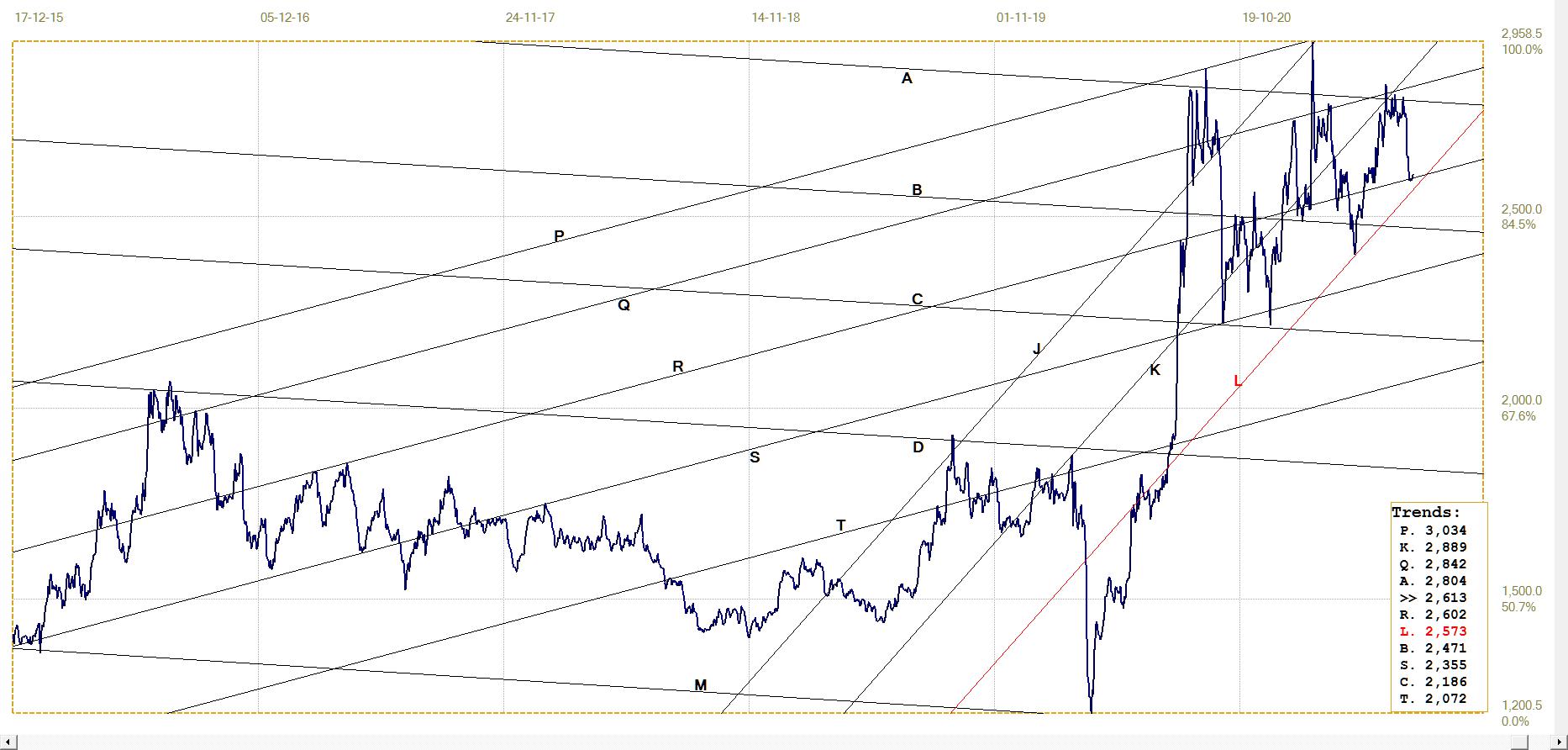

Silver Daily London Fix

Silver daily London fix, last = $26.13 (www.kitco.com)

Interestingly, this chart now also required a shallower steep bull channel as indication that the rear guard action in favour of the dollar and against the rallies in the metals meant that neither metals nor euro could sustain their initial medium term steeper bull channels. The fact that the price of silver managed to reach and then hold – so far – at the support of line R, without challenging the bottom of channel KL, is a good sign.

Similar to the price of gold in dollars and euro, the price of silver now has to recover from the month end gyrations and attacks to hold in the new shallower bull channel and then resume the rising trend off line R.

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 1.524% (www.investing.com )

The weakness in the bond market that had carried the yield above line Y – and briefly also lines R and Z – has abated, with the yield now holding within channel YZ. There is some volatility after the break back into channel YZ, as if the bond market is not clear on what the direction should be.

The recent sustained weakness that culminated in the temporary breaks higher surely has to be a reaction to all the money printing since Covid started to have effect all of 16 months ago. This printing of dollars resulted in a combination of excess supply and early concerns about inflation placing pressure on the bond market. Technical breaks higher have failed to hold; since the printing of dollars is continuing amid greater fears of inflation, one can guess that the limited and volatile rally in the bond market might be evidence of intervention not to let higher yields spook the investors.

Given that the degree of inflation is understated by the CPI, a fact that is well known to serious investors, one can also expect that the rising trend in the yield will resume at some point in the not too distant future and extend much higher once the breaks are again in place.

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $74.05

(www.investing.com )

The price of crude has been moving consistently higher in narrow and steep channel KL, now to approach significant resistance at lines B and S. This establishes the price of energy as a significant driver of inflation, because of the wide range of knock-on consumer price increases that result from more expensive energy.

An increase in the price of crude – probably as demand increases while supply could be slowed or interrupted by government edicts to prevent climate change – that will break above the nearby resistance can be expected to reflect in a higher CPI one or two months down the line.

********